December 10, 2025

Risks tied to rising delinquencies & tighter credit environment

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Understanding the Risks Tied to Rising Delinquencies & Tighter Credit Environment

The financial landscape of 2025 presents a challenging paradox: while economic indicators show mixed signals, a perfect storm is brewing beneath the surface. Rising delinquency rates and increasingly restrictive lending practices are creating a complex web of interconnected risks that threaten both individual financial stability and broader economic health. The risks tied to rising delinquencies & tighter credit environment are becoming more apparent as financial institutions grapple with mounting defaults while simultaneously restricting access to credit for borrowers who need it most.

Key Takeaways

• Delinquency rates across multiple credit sectors are reaching concerning levels, with auto loans and credit cards showing the steepest increases since the pandemic recovery period

• Tighter credit standards are creating a feedback loop where reduced access to credit exacerbates financial stress for consumers and businesses already struggling with existing debt obligations

• Systemic risks emerge when rising defaults coincide with restricted lending, potentially triggering broader economic slowdowns and reduced consumer spending

• Financial institutions face a delicate balancing act between protecting their portfolios and maintaining adequate credit flow to support economic growth

• Proactive risk management strategies are essential for both lenders and borrowers to navigate this challenging environment successfully

The Current State of Rising Delinquencies

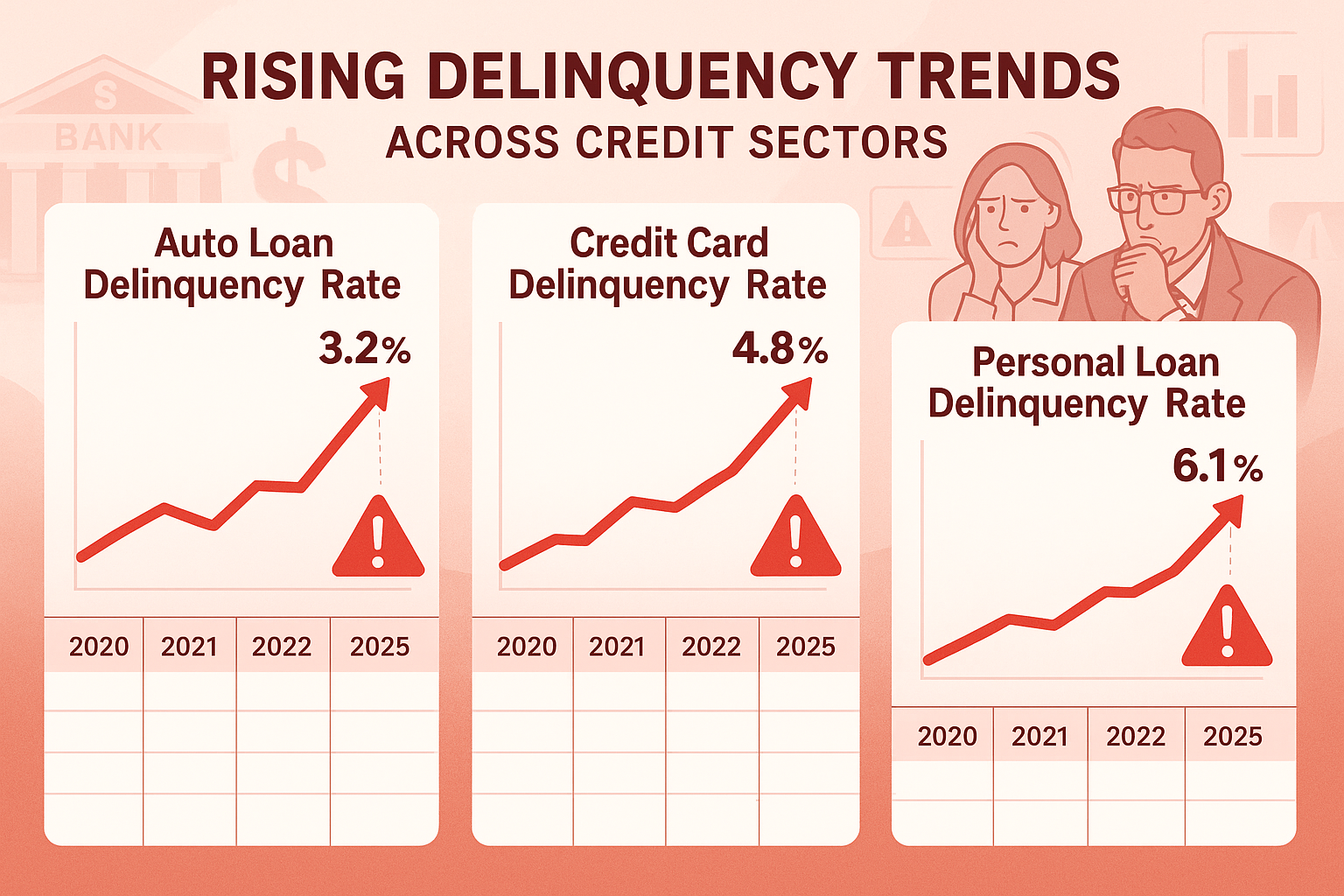

Credit Card Delinquencies Reach Critical Levels

Credit card delinquencies have emerged as one of the most concerning indicators in the current financial environment. According to recent Federal Reserve data, credit card delinquency rates have climbed to their highest levels since 2012, with particularly sharp increases among younger demographics and lower-income households.

The factors driving this trend include:

- Inflation pressures reducing disposable income

- Higher interest rates increasing minimum payment obligations

- Reduced pandemic-era savings as emergency funds become depleted

- Employment uncertainty in certain sectors

"The combination of higher borrowing costs and persistent inflation is creating a perfect storm for credit card holders who are already stretched thin financially." – Banking Industry Analyst

Auto Loan Defaults Signal Broader Concerns

The automotive lending sector is experiencing its own set of challenges, with subprime auto loan delinquencies rising at an alarming rate. This trend is particularly significant because auto loans are typically secured by the vehicle itself, making higher default rates indicative of severe financial distress among borrowers.

Key statistics include:

| Loan Category | 2023 Delinquency Rate | 2025 Delinquency Rate | Percentage Increase |

|---|---|---|---|

| Prime Auto Loans | 1.8% | 2.4% | +33% |

| Subprime Auto Loans | 8.2% | 11.7% | +43% |

| Credit Cards | 3.1% | 4.8% | +55% |

Personal Loan Market Under Pressure

Personal loans, which have grown significantly in popularity over the past decade, are showing signs of stress as borrowers struggle to meet payment obligations. The unsecured nature of most personal loans makes them particularly vulnerable during economic downturns, and lenders are responding by tightening qualification criteria.

How Tighter Credit Standards Amplify Financial Risks

The Lending Pendulum Swings

Financial institutions are responding to rising delinquencies by implementing stricter lending standards across all credit products. This defensive posture, while understandable from a risk management perspective, creates additional challenges for the broader economy.

Current tightening measures include:

- Higher minimum credit score requirements 📊

- Increased documentation requirements

- Lower debt-to-income ratio thresholds

- Reduced credit limits for existing customers

- Higher down payment requirements for secured loans

Impact on Different Borrower Segments

The tightening credit environment doesn't affect all borrowers equally. Prime borrowers with excellent credit histories may experience minimal impact, while subprime and near-prime borrowers face significantly reduced access to credit products.

Borrower segments most affected:

- First-time homebuyers struggling with higher down payment requirements

- Small business owners facing reduced access to working capital

- Consumers with limited credit history unable to establish credit relationships

- Individuals recovering from financial setbacks finding rehabilitation more difficult

The Credit Accessibility Gap

As traditional lenders tighten standards, many borrowers are turning to alternative lending sources, which often come with higher costs and less favorable terms. This shift creates a dangerous cycle where those most in need of affordable credit are pushed toward more expensive options.

Systemic Risks Tied to Rising Delinquencies & Tighter Credit Environment

Economic Growth Implications

The combination of rising defaults and restricted credit access creates significant headwinds for economic growth. When consumers cannot access credit for major purchases and businesses struggle to obtain working capital, economic activity naturally slows.

Key economic indicators affected:

- Consumer spending patterns

- Business investment levels

- Employment growth rates

- Housing market activity

- Small business formation

Banking Sector Vulnerabilities

Financial institutions face a complex challenge as they navigate between protecting their balance sheets and maintaining adequate credit flow. Community banks and regional lenders are particularly vulnerable, as they typically have higher concentrations of local lending and fewer resources to absorb losses.

Regulatory Response and Oversight

Regulators are closely monitoring the situation, with particular attention to:

- Stress testing requirements for larger institutions

- Capital adequacy ratios across the banking sector

- Consumer protection measures for alternative lending

- Systemic risk assessments for interconnected institutions

Industry-Specific Impacts and Vulnerabilities

Automotive Industry Challenges

The automotive sector faces unique challenges as both a lender (through captive finance companies) and an industry dependent on consumer credit access. Rising auto loan delinquencies directly impact manufacturer financing arms, while tighter credit standards reduce the pool of qualified buyers.

Specific impacts include:

- Reduced vehicle sales volumes

- Increased inventory levels

- Pressure on dealer financing arrangements

- Higher costs for subprime lending programs

Real Estate Market Dynamics

The real estate market is experiencing a complex interplay between mortgage availability and affordability concerns. While mortgage delinquencies remain relatively stable compared to other credit products, tighter lending standards are reducing homebuyer activity.

Small Business Credit Crunch

Small businesses are particularly vulnerable to credit tightening, as they typically rely more heavily on personal guarantees and have fewer financing alternatives than larger corporations. The risks tied to rising delinquencies & tighter credit environment are especially pronounced for:

- Startup companies seeking initial funding

- Seasonal businesses requiring working capital credit lines

- Service-based businesses with limited collateral

- Minority-owned enterprises facing additional access barriers

Consumer Behavior and Adaptation Strategies

Changing Spending Patterns

Consumers are adapting to the challenging credit environment by modifying their spending and borrowing behaviors. Debt consolidation requests have increased significantly, as borrowers seek to manage multiple payment obligations more effectively.

Observable behavioral changes:

- Increased use of buy-now-pay-later services

- Greater reliance on family and informal lending

- Delayed major purchase decisions

- Increased focus on emergency fund building

Financial Stress Indicators

Rising delinquencies often serve as early warning indicators of broader financial stress. Mental health impacts from financial pressure are becoming more apparent, with increased demand for financial counseling and debt management services.

Risk Mitigation Strategies for Stakeholders

For Financial Institutions

Banks and credit unions must balance risk management with business growth objectives. Effective strategies include:

- Enhanced underwriting models incorporating alternative data sources

- Graduated risk pricing rather than complete credit denial

- Proactive customer communication for early intervention

- Portfolio diversification across geographic and demographic segments

- Technology investments in fraud detection and risk assessment

For Consumers

Individual borrowers can take proactive steps to navigate the challenging environment:

Immediate actions:

- Review and optimize existing credit utilization

- Establish emergency fund reserves

- Monitor credit reports for accuracy

- Consider debt consolidation options

- Communicate proactively with lenders during financial difficulties

Long-term strategies:

- Build diverse income streams

- Improve credit scores through consistent payment history

- Reduce overall debt-to-income ratios

- Establish banking relationships before needing credit

For Businesses

Companies must adapt their financial strategies to account for reduced credit availability:

- Cash flow management optimization

- Alternative financing exploration (equipment leasing, factoring)

- Customer credit policy adjustments

- Supplier relationship strengthening for extended payment terms

Regulatory and Policy Considerations

Current Regulatory Framework

Financial regulators are actively monitoring the situation and considering policy responses to address the risks tied to rising delinquencies & tighter credit environment. Key areas of focus include:

- Consumer protection in alternative lending markets

- Bank capital requirements and stress testing

- Fair lending practices during credit tightening

- Systemic risk monitoring and early warning systems

Potential Policy Interventions

Policymakers are evaluating various options to address credit access challenges while maintaining financial stability:

Possible measures include:

- Government-backed lending programs for small businesses

- First-time homebuyer assistance programs

- Financial literacy initiatives to improve borrower education

- Regulatory guidance on responsible lending practices

Technology and Innovation in Credit Risk Management

Advanced Analytics and AI

Financial institutions are leveraging artificial intelligence and machine learning to better assess credit risk and identify early warning signs of potential defaults. These technologies enable more nuanced risk assessment beyond traditional credit scoring models.

Technological applications:

- Predictive modeling for delinquency risk

- Real-time transaction monitoring

- Alternative data integration (utility payments, rental history)

- Automated early intervention systems

Fintech Solutions

Financial technology companies are developing innovative solutions to address credit access challenges while managing risk effectively. These include:

- Income-based repayment models

- Micro-lending platforms

- Peer-to-peer lending networks

- Digital-first underwriting processes

Future Outlook and Emerging Trends

Economic Scenario Planning

Financial institutions and policymakers are developing multiple economic scenarios to prepare for various potential outcomes. Base case, adverse, and severely adverse scenarios help stakeholders understand potential ranges of impact.

Key variables being monitored:

- Interest rate trajectory

- Employment levels and wage growth

- Inflation persistence

- Geopolitical developments

- Technological disruption impacts

Industry Evolution

The financial services industry is likely to emerge from this challenging period with structural changes in how credit risk is assessed and managed. Sustainable lending practices that balance profitability with social responsibility are becoming increasingly important.

Building Resilience in Uncertain Times

Collaborative Approaches

Addressing the risks tied to rising delinquencies & tighter credit environment requires collaboration among multiple stakeholders:

- Public-private partnerships for credit access programs

- Industry associations sharing best practices

- Community organizations providing financial education

- Technology providers developing innovative solutions

Long-term Sustainability

The current challenges present an opportunity to build a more resilient financial system that can better withstand future economic shocks. This includes:

- Improved risk assessment methodologies

- Enhanced consumer financial education

- More flexible lending products

- Stronger regulatory frameworks

Conclusion

The risks tied to rising delinquencies & tighter credit environment represent one of the most significant challenges facing the financial sector in 2025. While rising default rates signal genuine financial stress among consumers and businesses, the response of tightening credit standards creates additional complications that can amplify economic difficulties.

Success in navigating this environment requires:

✅ Proactive risk management by financial institutions that balances prudent lending with economic growth support

✅ Consumer education and preparation to help borrowers make informed decisions and build financial resilience

✅ Policy coordination among regulators to ensure financial stability while maintaining credit access

✅ Technological innovation to improve risk assessment and create new lending models

✅ Industry collaboration to share best practices and develop sustainable solutions

The path forward demands careful balance between protecting financial institutions from excessive risk while ensuring adequate credit flow to support economic growth. Stakeholders who take proactive steps to understand and address these interconnected risks will be better positioned to thrive despite the challenging environment.

Immediate next steps for all stakeholders include conducting comprehensive risk assessments, developing contingency plans, and establishing clear communication channels for early intervention when problems arise. By working together and maintaining focus on long-term sustainability rather than short-term gains, the financial sector can emerge from this period stronger and more resilient than before.

SEO Meta Information:

Meta Title: Risks of Rising Delinquencies & Tight Credit in 2025

Meta Description: Explore the critical risks tied to rising delinquencies & tighter credit environment. Learn how defaults and restricted lending create systemic challenges for 2025.