December 10, 2025

Opportunities for first-time homebuyers among self-employed Canadians

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Opportunities for First-Time Homebuyers Among Self-Employed Canadians: A Complete Guide to Homeownership Success

Picture this: you’ve built a thriving freelance business, consulting practice, or small company from the ground up. Your income is strong, your credit is solid, but when it comes to buying your first home, traditional lenders seem to speak a different language. The reality is that opportunities for first-time homebuyers among self-employed Canadians are more abundant than many realize, despite the unique challenges that come with non-traditional income sources.

In 2025, Canada’s housing market presents both challenges and unprecedented opportunities for entrepreneurial first-time buyers. With enhanced government incentives, expanded RRSP withdrawal limits, and specialized lending programs designed specifically for self-employed individuals, the path to homeownership has never been more accessible for independent workers and business owners.

Key Takeaways

• Enhanced RRSP Benefits: First-time homebuyers can now withdraw up to $60,000 tax-free from their RRSP through the Home Buyers’ Plan, a significant increase from the previous $35,000 limit

• Documentation Requirements: Self-employed individuals need 2 years of consistent income documentation including T1 Generals and Notice of Assessments to qualify for traditional mortgage approval

• Multiple Incentive Programs: Four main government programs support first-time buyers: land transfer tax rebates, shared-equity programs, RRSP withdrawals, and federal tax credits worth up to $1,500

• Flexible Lending Options: Alternative lenders offer stated income programs for self-employed buyers with 10%+ down payments, while A-lenders provide competitive rates for those with strong documentation

• Strategic Timing Advantage: The expanded GST/HST rebate for new homes up to $1.5 million (increased from $450,000) applies through 2030, creating significant savings opportunities

Understanding the Self-Employed Homebuyer Landscape in Canada

The landscape for opportunities for first-time homebuyers among self-employed Canadians has evolved dramatically in recent years. Traditional employment verification methods don’t apply to entrepreneurs, freelancers, and business owners, creating unique challenges that require specialized approaches.

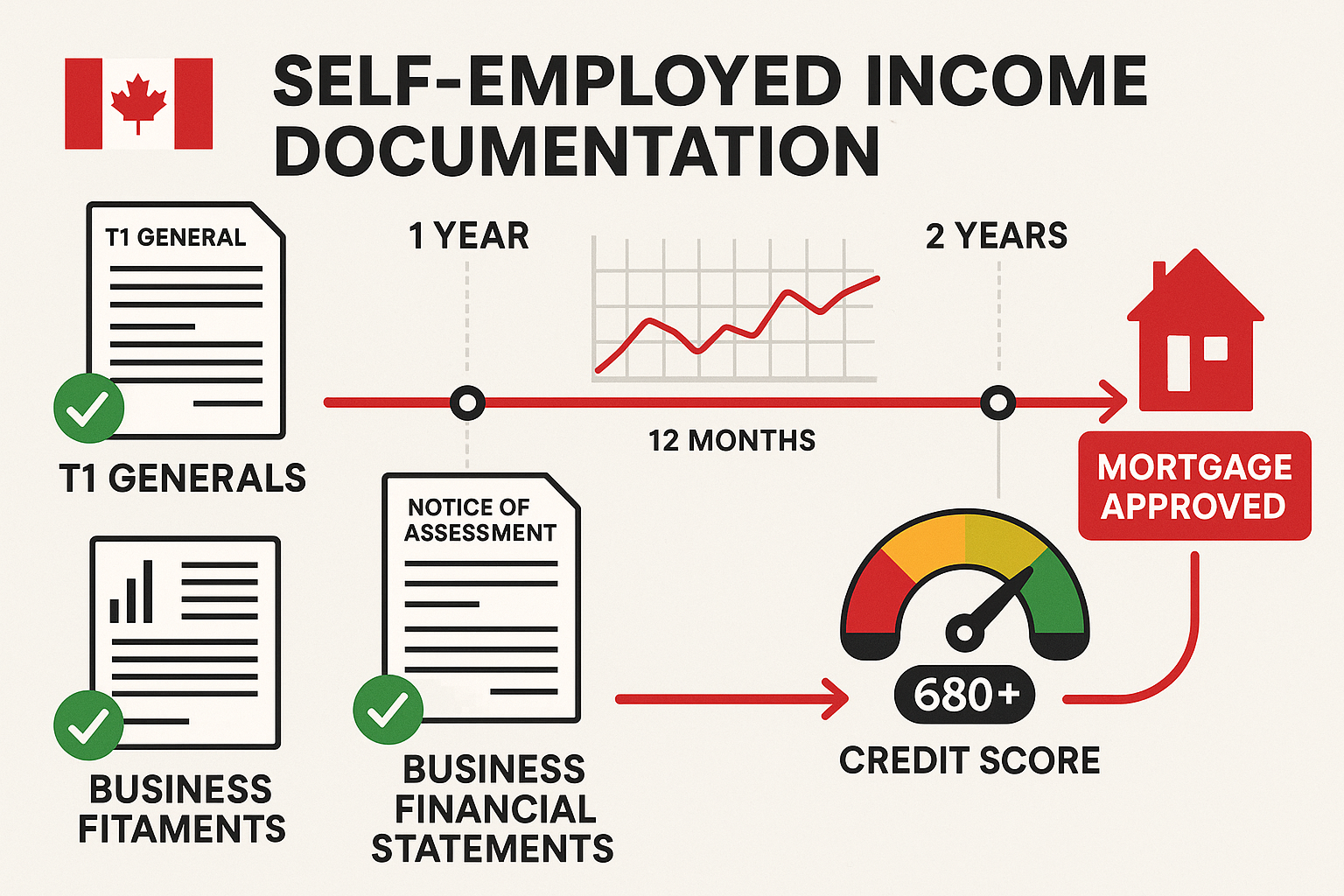

The Documentation Challenge 🏠

Self-employed individuals face stricter documentation requirements compared to salaried employees. Lenders require at least 2 years of self-employment income with corresponding Notice of Assessments (NOAs) to demonstrate income stability. This requirement exists because self-employed income can fluctuate significantly, making lenders more cautious about approval decisions.

Essential Documentation Checklist:

- T1 General tax returns for the past 2 years

- Notice of Assessments (NOAs) from Canada Revenue Agency

- Business financial statements including profit and loss statements

- Bank statements showing consistent deposits

- Credit reports with scores ideally above 680

- Proof of down payment funds and their source

Income Verification Methods

Unlike salaried workers who can provide simple pay stubs, self-employed borrowers must prove their income through comprehensive financial documentation. Lenders typically use the average of the past 2 years’ declared income as the basis for mortgage calculations.

“Self-employed homebuyers with stable income and good credit scores (680+) can qualify for the same mortgage rates as salaried workers, but the approval process requires more thorough preparation and documentation.” – Canadian Mortgage Professional Association

Government Incentives and Programs for Self-Employed First-Time Buyers

The Canadian government has significantly expanded opportunities for first-time homebuyers among self-employed Canadians through various incentive programs designed to make homeownership more accessible and affordable.

Enhanced RRSP Home Buyers’ Plan 💰

The Home Buyers’ Plan (HBP) represents one of the most powerful tools available to first-time buyers. In 2025, the withdrawal limit increased to $60,000 per person (up from $35,000), allowing couples to access up to $120,000 tax-free for their down payment.

Key HBP Features:

- Withdrawal Amount: Up to $60,000 per eligible individual

- Repayment Period: 15 years, starting 5 years after withdrawal

- Tax Implications: Withdrawals are tax-free if repaid on schedule

- Eligibility: Must not have owned a principal residence in the previous 4 calendar years

HBP Repayment Schedule:

| Year After Withdrawal | Repayment Status |

|---|---|

| Years 1-4 | No repayment required |

| Year 5 | First payment due (1/15th of total) |

| Years 6-19 | Annual payments continue |

| Missed Payments | Added to taxable income |

Federal Tax Credits and Rebates

First-time homebuyers can claim a federal tax credit of up to $10,000 at a 15% non-refundable rate, providing an effective deduction of $1,500. This credit applies to the purchase of a principal residence and can significantly reduce the overall cost of homeownership.

Expanded GST/HST Rebate Program

Starting with agreements of purchase and sale entered after May 27, 2025, the federal GST/HST rebate for new homes has been dramatically expanded. The maximum eligible home price increased from $450,000 to $1.5 million, making this rebate accessible to buyers in higher-cost markets like Toronto and Vancouver.

GST/HST Rebate Benefits:

- Eligible Homes: New construction up to $1.5 million

- Rebate Amount: Varies by province and home price

- Application Period: Through 2030

- Eligibility: First-time buyers meeting specific criteria

Shared-Equity Incentive Programs

These innovative programs provide 5% to 10% of the purchase price as government assistance with no interest charged. The government shares proportionally in any gains or losses when the home is sold or the loan is repaid.

Shared-Equity Program Structure:

- Contribution: 5% for resale homes, 10% for new construction

- Interest Rate: 0% during the loan period

- Repayment: Required after 25 years or upon sale

- Shared Appreciation: Government participates in property value changes

Mortgage Options and Lending Strategies for Self-Employed Buyers

Navigating mortgage options requires understanding the different types of lenders and their specific requirements for self-employed borrowers. Opportunities for first-time homebuyers among self-employed Canadians vary significantly depending on the lending institution and program chosen.

A-Lenders vs. Alternative Lenders

A-Lenders (Traditional Banks):

- Require comprehensive 2-year income documentation

- Offer the most competitive interest rates

- Strict debt-to-income ratio requirements

- Prefer borrowers with credit scores above 680

B-Lenders and Alternative Options:

- More flexible income verification requirements

- Stated income programs for borrowers with 10%+ down payments

- Slightly higher interest rates but easier approval

- Examples include Home Trust and other specialized lenders

Down Payment Strategies 💳

While self-employed buyers can purchase homes with down payments as low as 5%, larger down payments typically result in better mortgage rates and stronger approval odds.

Down Payment Impact on Approval:

| Down Payment | CMHC Insurance Required | Typical Approval Rate | Interest Rate Impact |

|---|---|---|---|

| 5-9.99% | Yes | Moderate | Higher rates |

| 10-19.99% | Yes | Good | Competitive rates |

| 20%+ | No | Excellent | Best available rates |

Working with Mortgage Brokers

Mortgage brokers experienced in self-employment cases significantly improve approval odds by matching borrowers with lenders offering flexible programs. These professionals understand which lenders are most receptive to self-employed applications and can present applications in the most favorable light.

Benefits of Using a Mortgage Broker:

- Access to multiple lender networks

- Expertise in self-employed documentation

- Pre-screening to avoid unnecessary credit inquiries

- Negotiation power for better rates and terms

Financial Planning and Preparation Strategies

Success in securing a mortgage as a self-employed first-time buyer requires strategic financial planning well before beginning the house-hunting process. The opportunities for first-time homebuyers among self-employed Canadians are maximized when buyers approach the process with proper preparation.

Income Optimization Techniques 📊

Self-employed individuals often have flexibility in how they structure their income and business expenses. Strategic planning can improve mortgage qualification without compromising business operations.

Income Documentation Strategies:

- Minimize Business Deductions: Reduce write-offs in the 2 years before applying

- Salary vs. Dividends: Structure corporate income to maximize reported personal income

- Consistent Reporting: Maintain steady income reporting patterns

- Professional Bookkeeping: Ensure accurate, professional financial statements

Building Credit and Financial History

Strong credit scores become even more critical for self-employed borrowers. Lenders view credit history as an indicator of financial responsibility when traditional income verification is more complex.

Credit Optimization Checklist:

- ✅ Maintain credit scores above 680 (ideally 720+)

- ✅ Keep credit utilization below 30%

- ✅ Avoid new credit applications 6 months before mortgage application

- ✅ Pay all bills on time consistently

- ✅ Monitor credit reports for errors

Emergency Fund and Cash Reserves

Lenders prefer to see self-employed borrowers with substantial cash reserves beyond the down payment and closing costs. This demonstrates financial stability and ability to handle unexpected income fluctuations.

Recommended Cash Reserves:

- 3-6 months of mortgage payments

- Closing costs (1.5-4% of purchase price)

- Moving and immediate expenses ($5,000-$15,000)

- Home maintenance fund (1-3% of home value annually)

Regional Opportunities and Market Considerations

Opportunities for first-time homebuyers among self-employed Canadians vary significantly across different provinces and municipalities, each offering unique incentive programs and market conditions.

Provincial and Municipal Programs 🍁

Beyond federal incentives, many provinces and cities offer additional support for first-time homebuyers, with some specifically designed to help self-employed individuals.

Provincial Highlights:

Ontario:

- Land Transfer Tax Rebate: Up to $4,000 for first-time buyers

- Ontario First-Time Home Buyer Incentive: Shared-equity loans

- Municipal Programs: Additional rebates in cities like Toronto

British Columbia:

- First-Time Home Buyers’ Program: Property transfer tax exemption

- BC Home Owner Mortgage and Equity Partnership: Shared-equity assistance

- Regional Variations: Different programs in Vancouver vs. smaller communities

Alberta:

- First-Time Home Buyer Incentive: Cash grants and tax credits

- Municipal Development Incentives: Reduced fees in growing communities

- Energy Efficiency Rebates: Additional savings for qualifying homes

Market Timing and Regional Strategies

Self-employed buyers often have more flexibility in timing their purchases, allowing them to take advantage of market conditions and seasonal variations.

Strategic Timing Considerations:

- Spring Market: More inventory but higher competition

- Fall/Winter: Better negotiating position, fewer buyers

- Interest Rate Cycles: Coordinate applications with favorable rate periods

- Regional Development: Emerging areas with growth potential

Common Challenges and Solutions

While opportunities for first-time homebuyers among self-employed Canadians are extensive, several common challenges require specific strategies and solutions.

Income Fluctuation Management 📈

Self-employed income naturally fluctuates, which can concern lenders. However, several strategies can demonstrate income stability and reliability.

Solutions for Income Variability:

- Diversified Client Base: Show multiple income sources

- Long-term Contracts: Demonstrate recurring revenue streams

- Seasonal Adjustments: Explain and document predictable seasonal patterns

- Growth Trends: Highlight increasing income trajectories over time

Documentation Organization

The complexity of self-employed financial documentation often overwhelms first-time buyers. Creating organized, professional presentations of financial information significantly improves approval odds.

Documentation Best Practices:

- Professional Preparation: Use accountants for financial statement preparation

- Clear Organization: Create indexed binders with all required documents

- Digital Copies: Maintain electronic versions for quick lender requests

- Regular Updates: Keep documentation current throughout the application process

Dealing with Rejection and Alternatives

Not all applications succeed on the first attempt. Understanding alternative options and improvement strategies helps maintain momentum toward homeownership.

Alternative Strategies After Rejection:

- B-Lender Applications: Explore alternative lending options

- Co-signer Arrangements: Include creditworthy co-signers

- Larger Down Payments: Reduce lender risk with increased equity

- Income Documentation Improvement: Strengthen financial presentation

Technology and Tools for Self-Employed Homebuyers

Modern technology has created new opportunities for first-time homebuyers among self-employed Canadians through digital tools that streamline the application process and improve financial management.

Digital Mortgage Platforms 💻

Online mortgage platforms increasingly cater to self-employed borrowers with specialized application processes and documentation requirements.

Digital Platform Benefits:

- Streamlined Applications: Faster processing times

- Document Upload Systems: Secure, organized file management

- Real-time Updates: Track application progress

- Comparison Tools: Evaluate multiple lender options simultaneously

Financial Management Software

Proper financial management becomes crucial for self-employed individuals planning to purchase homes. Modern software solutions help maintain the organized records lenders require.

Recommended Financial Tools:

- QuickBooks: Comprehensive business accounting

- FreshBooks: Simplified invoicing and expense tracking

- Wave Accounting: Free small business financial management

- Mint: Personal financial tracking and budgeting

Mortgage Calculators and Planning Tools

Specialized calculators help self-employed buyers understand their borrowing capacity and plan their financial strategy effectively.

Essential Calculation Tools:

- Self-Employed Mortgage Calculators: Account for variable income

- Down Payment Calculators: Include all available incentive programs

- Affordability Assessments: Factor in self-employment income variations

- Amortization Schedules: Plan long-term payment strategies

Future Trends and Emerging Opportunities

The landscape of opportunities for first-time homebuyers among self-employed Canadians continues evolving with changing government policies, lending practices, and economic conditions.

Policy Evolution and Trends 🔮

Government recognition of the growing gig economy and self-employment trends is driving policy changes that benefit independent workers seeking homeownership.

Emerging Policy Trends:

- Expanded Income Recognition: New methods for verifying gig economy income

- Technology Integration: Digital verification systems for self-employed income

- Regional Incentives: Targeted programs for specific geographic areas

- Green Home Incentives: Additional rebates for energy-efficient purchases

Lending Innovation

Financial institutions are developing new products and services specifically designed for the self-employed market segment.

Innovative Lending Solutions:

- Bank Statement Programs: Income verification through deposit patterns

- Asset-Based Lending: Qualification based on assets rather than income

- Blockchain Verification: Secure, automated income documentation

- AI-Powered Underwriting: Faster, more accurate risk assessment

Market Opportunities

Changing demographics and housing market conditions create new opportunities for prepared self-employed buyers.

Market Advantage Areas:

- Remote Work Flexibility: Access to lower-cost markets

- Renovation Opportunities: Leveraging business skills for property improvement

- Investment Potential: Building wealth through strategic property selection

- Community Development: Participating in emerging neighborhood growth

Success Stories and Case Studies

Real-world examples demonstrate how opportunities for first-time homebuyers among self-employed Canadians translate into successful homeownership experiences.

Case Study 1: The Freelance Consultant 🏡

Background: Sarah, a marketing consultant with 3 years of self-employment experience, earning an average of $75,000 annually.

Strategy:

- Maximized RRSP contributions for 2 years before applying

- Worked with a mortgage broker specializing in self-employed clients

- Chose a B-lender with stated income program

- Used 15% down payment to improve approval odds

Outcome: Successfully purchased a $450,000 home with competitive interest rates and accessed multiple first-time buyer incentives.

Case Study 2: The Small Business Owner

Background: Michael, owner of a small construction company, with fluctuating income between $60,000-$90,000 annually.

Strategy:

- Organized 3 years of financial documentation

- Demonstrated income growth trend

- Partnered with spouse’s stable employment income

- Utilized shared-equity incentive program

Outcome: Purchased a $380,000 home with minimal cash outlay and government equity participation.

Conclusion: Your Path to Homeownership Success

The opportunities for first-time homebuyers among self-employed Canadians in 2025 are more robust and accessible than ever before. With enhanced RRSP withdrawal limits, expanded government incentive programs, and innovative lending solutions, self-employed individuals have multiple pathways to successful homeownership.

Key Success Factors:

- Early Planning: Begin financial preparation 2-3 years before purchasing

- Professional Support: Work with experienced mortgage brokers and accountants

- Documentation Excellence: Maintain organized, comprehensive financial records

- Strategic Timing: Coordinate applications with optimal market and personal conditions

- Multiple Options: Explore all available incentive programs and lending alternatives

Immediate Action Steps:

- Assess Current Financial Position 📋

- Review 2 years of tax returns and NOAs

- Calculate current credit score and debt ratios

- Determine available down payment funds

- Maximize Government Incentives 💰

- Research all applicable federal, provincial, and municipal programs

- Plan RRSP contributions to maximize HBP benefits

- Understand shared-equity program eligibility

- Build Professional Team 🤝

- Connect with mortgage brokers experienced in self-employed applications

- Engage qualified accountants for financial statement preparation

- Identify real estate agents familiar with first-time buyer programs

- Prepare Documentation Strategy 📁

- Organize all required financial documents

- Create professional presentation materials

- Establish ongoing record-keeping systems

- Begin Market Research 🏘️

- Identify target neighborhoods and price ranges

- Monitor market conditions and timing opportunities

- Evaluate properties that maximize incentive program benefits

The path to homeownership as a self-employed first-time buyer requires preparation, patience, and professional guidance, but the rewards of building equity and establishing roots in your community make the effort worthwhile. With proper planning and strategic use of available programs, self-employed Canadians can successfully navigate the path from entrepreneurship to homeownership in 2025 and beyond.

Remember that each situation is unique, and what works for one self-employed buyer may not be optimal for another. The key is understanding all available options and creating a personalized strategy that maximizes your specific advantages while addressing any challenges your particular circumstances present.

SEO Meta Information

Meta Title: First-Time Homebuyer Opportunities for Self-Employed Canadians 2025

Meta Description: Discover enhanced opportunities for self-employed Canadians buying their first home in 2025. Learn about $60K RRSP withdrawals, government incentives, and specialized lending options.