February 4, 2026

Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage renewal crisis of 2026 is no longer a distant threat—it’s here, and Toronto first-time homebuyers are facing unprecedented payment shocks. Imagine opening your renewal notice to discover your monthly payment has jumped by $1,200, $1,500, or even $2,000. For many young homeowners who purchased their first property in 2021 or 2022, this nightmare scenario is becoming reality. This Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing provides the roadmap you need to navigate these turbulent waters and protect your financial future.

With close to 60% of Canadian mortgages set to renew in 2026[4], and mortgage holders facing average payment increases of 15%-20%[2], the time to act is now. The good news? Strategic refinancing can transform this crisis into an opportunity for stability.

Key Takeaways

✅ Payment shock is real: First-time homebuyers with five-year fixed mortgages from 2021 could face monthly payment increases of $1,000-$2,000 when renewing in 2026[1]

✅ Refinancing offers relief: Extending your amortization period through refinancing can significantly reduce monthly payments and prevent financial distress

✅ Equity is your advantage: Toronto’s real estate market has built substantial equity for recent buyers, creating refinancing opportunities that weren’t available at purchase

✅ Timing matters: Starting the refinancing process 120 days before your renewal date gives you maximum negotiating power and options

✅ Professional guidance pays off: Working with a Toronto mortgage broker can unlock solutions and rates that banks won’t offer directly

Understanding the 2026 Mortgage Renewal Crisis

What Makes 2026 Different?

The mortgage renewal wall hitting Canada in 2026 represents a perfect storm of economic factors. Over 2 million Canadian mortgages are coming up for renewal in the next two years[1], with the majority concentrated in 2026. This unprecedented volume creates unique challenges for first-time homebuyers who entered the market during the low-rate environment of 2020-2021.

Why first-time buyers are most vulnerable:

- 🏠 Higher purchase prices: Many bought at market peaks in 2021-2022

- 💰 Maximum leverage: First-timers typically use minimal down payments (5-10%)

- 📊 Rate shock exposure: Locked in at 1.5%-2.5%, now facing 4%-5.5% rates

- 🎯 Limited equity cushion: Less time to build home equity compared to experienced owners

- 💳 Tighter budgets: Often carrying student loans, car payments, and other debts

The Real Numbers Behind Payment Shock

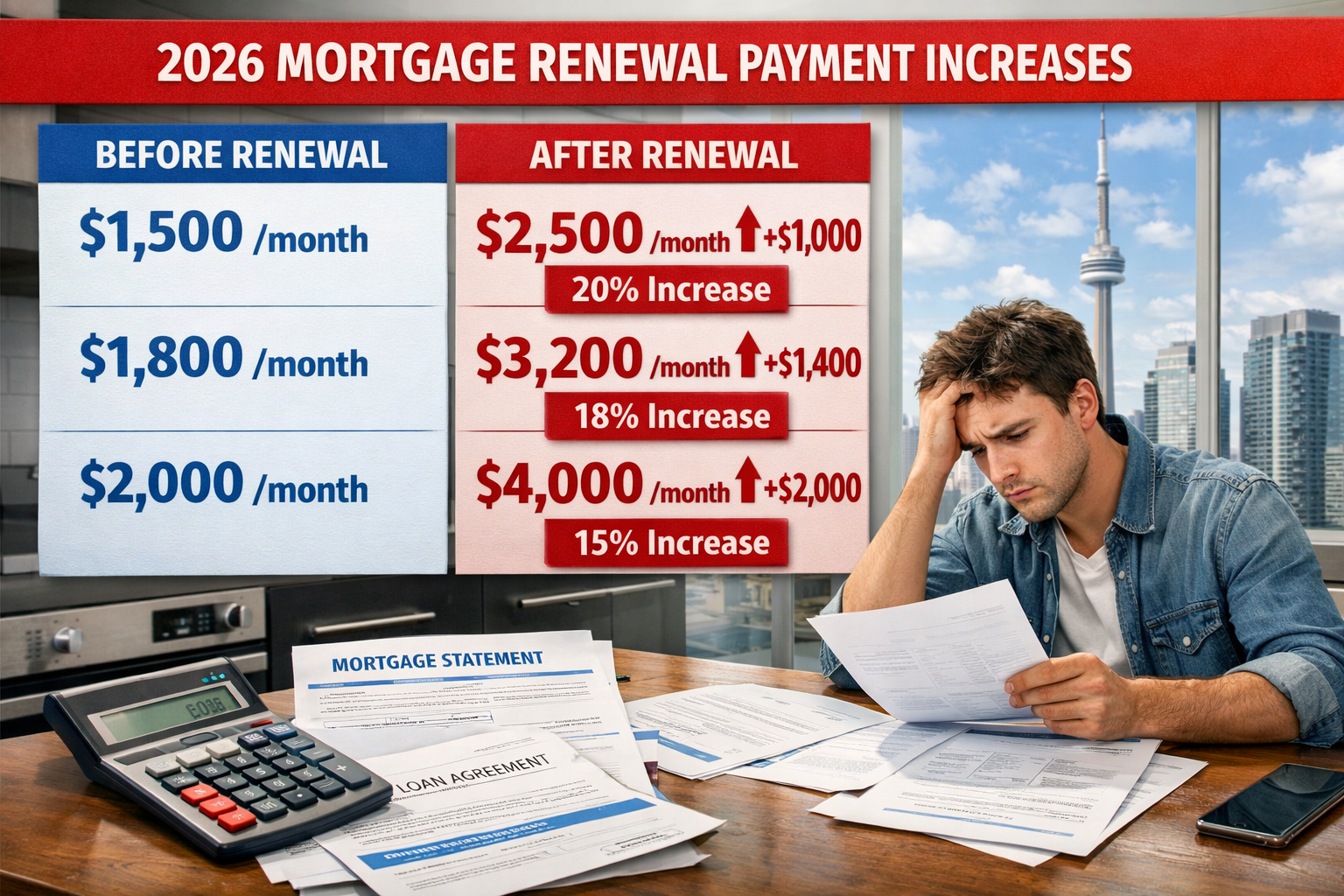

According to Bank of Canada analysis, mortgage holders with a five-year, fixed-rate contract renewing in 2025 or 2026 could face an average payment increase of around 15%-20% compared with December 2024[2]. But what does this mean in actual dollars for Toronto homebuyers?

| Original Mortgage Amount | Original Rate (2021) | Original Payment | Renewal Rate (2026) | New Payment | Monthly Increase |

|---|---|---|---|---|---|

| $500,000 | 2.0% | $2,120 | 5.0% | $3,280 | +$1,160 |

| $650,000 | 1.8% | $2,630 | 4.8% | $4,150 | +$1,520 |

| $800,000 | 2.2% | $3,290 | 5.2% | $5,340 | +$2,050 |

These aren’t hypothetical scenarios—they’re real case studies from Toronto homeowners facing renewal in 2026[1]. The financial strain is immense, particularly for households already stretched thin by inflation and rising living costs.

Who’s Most at Risk?

The Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing particularly applies to those who:

✓ Purchased their first home between January 2020 and March 2022

✓ Opted for a five-year fixed mortgage at historically low rates

✓ Bought in Toronto’s competitive market with minimal down payment

✓ Have seen income growth that hasn’t kept pace with payment increases

✓ Carry additional debts (student loans, car payments, credit cards)

Understanding these vulnerabilities is the first step. Many first-time buyers made common mistakes that now compound their renewal challenges, but refinancing offers a proven path forward.

How Refinancing Can Save First-Time Homebuyers in 2026

The Power of Strategic Refinancing

Refinancing isn’t just about getting a lower rate—it’s about restructuring your mortgage to match your current financial reality. For Toronto first-time homebuyers facing the 2026 renewal shock, refinancing offers several powerful advantages that a standard renewal simply cannot provide.

Key refinancing benefits:

🔄 Extended amortization: Stretch your mortgage from 22 remaining years back to 25-30 years

💵 Lower monthly payments: Reduce payments by 20%-35% even at higher rates

🏦 Debt consolidation: Roll high-interest debts into your mortgage at lower rates

📈 Access to equity: Tap into home appreciation for renovations or emergencies

🎯 Better terms: Negotiate prepayment privileges and flexible payment options

Real Toronto Case Study: The $1,500 Monthly Savings

Meet Sarah and James (composite based on actual Toronto clients):

- Purchased: $720,000 condo in 2021

- Original mortgage: $648,000 at 1.9% (5-year fixed)

- Original payment: $2,730/month

- Renewal rate offered: 5.1%

- Standard renewal payment: $4,250/month (+$1,520 increase)

Their refinancing solution:

Instead of accepting the standard renewal, Sarah and James worked with a mortgage broker to refinance their mortgage. Here’s what they achieved:

- Accessed built-up equity: $85,000 (Toronto market appreciation)

- Extended amortization: From 22 years remaining to 28 years

- Negotiated rate: 4.7% (better than bank’s renewal offer)

- New payment: $3,380/month

- Monthly savings vs. renewal: $870

- Avoided payment shock: Yes ✅

This Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing approach transformed an unaffordable situation into a manageable one. The extended amortization means paying more interest over time, but it preserves cash flow and prevents default—the priority for first-time buyers facing payment shock.

Understanding Your Refinancing Options

When exploring refinancing strategies, Toronto first-time homebuyers have several paths forward:

Option 1: Traditional Refinance with A-Lenders

Best for: Homebuyers with good credit (680+) and stable employment

- ✅ Lowest interest rates (currently 4.5%-5.2%)

- ✅ Maximum amortization (up to 30 years if qualified)

- ✅ Best prepayment privileges

- ❌ Strict qualification requirements

- ❌ Full income verification needed

Option 2: Alternative Lender Refinancing

Best for: Self-employed or those with credit challenges

- ✅ More flexible qualification criteria

- ✅ Stated income programs available

- ✅ Faster approval process

- ❌ Higher rates (typically 5.5%-7%)

- ❌ May require larger equity position (20%+)

For those who need alternative solutions, exploring B-lender mortgage rates in Toronto can provide viable options when traditional banks say no.

Option 3: Home Equity Loan Strategy

Best for: Preserving your low existing rate while accessing cash

Instead of refinancing your entire mortgage, consider a home equity loan for debt consolidation:

- ✅ Keep your existing low-rate mortgage intact

- ✅ Access equity at separate rate (typically 6%-8%)

- ✅ Consolidate high-interest debts

- ❌ Two separate payments to manage

- ❌ Higher rate on the equity portion

Leveraging Toronto’s Real Estate Appreciation

One crucial advantage Toronto first-time homebuyers have is significant home equity growth. Despite market fluctuations, Toronto real estate has appreciated substantially since 2021:

Average Toronto home price appreciation (2021-2026):

- Condos: +12% to +18%

- Townhouses: +15% to +22%

- Detached homes: +18% to +25%

This equity is your secret weapon for refinancing. With 20% or more equity, you unlock:

- Better interest rates

- More lender options

- Ability to extend amortization

- Opportunity to consolidate debts

- Removal of CMHC insurance premiums

Even if you started with just 5% down, five years of appreciation plus principal paydown typically brings you well above the 20% equity threshold—making refinancing a powerful tool in this Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing.

Step-by-Step Action Plan for Toronto First-Time Homebuyers

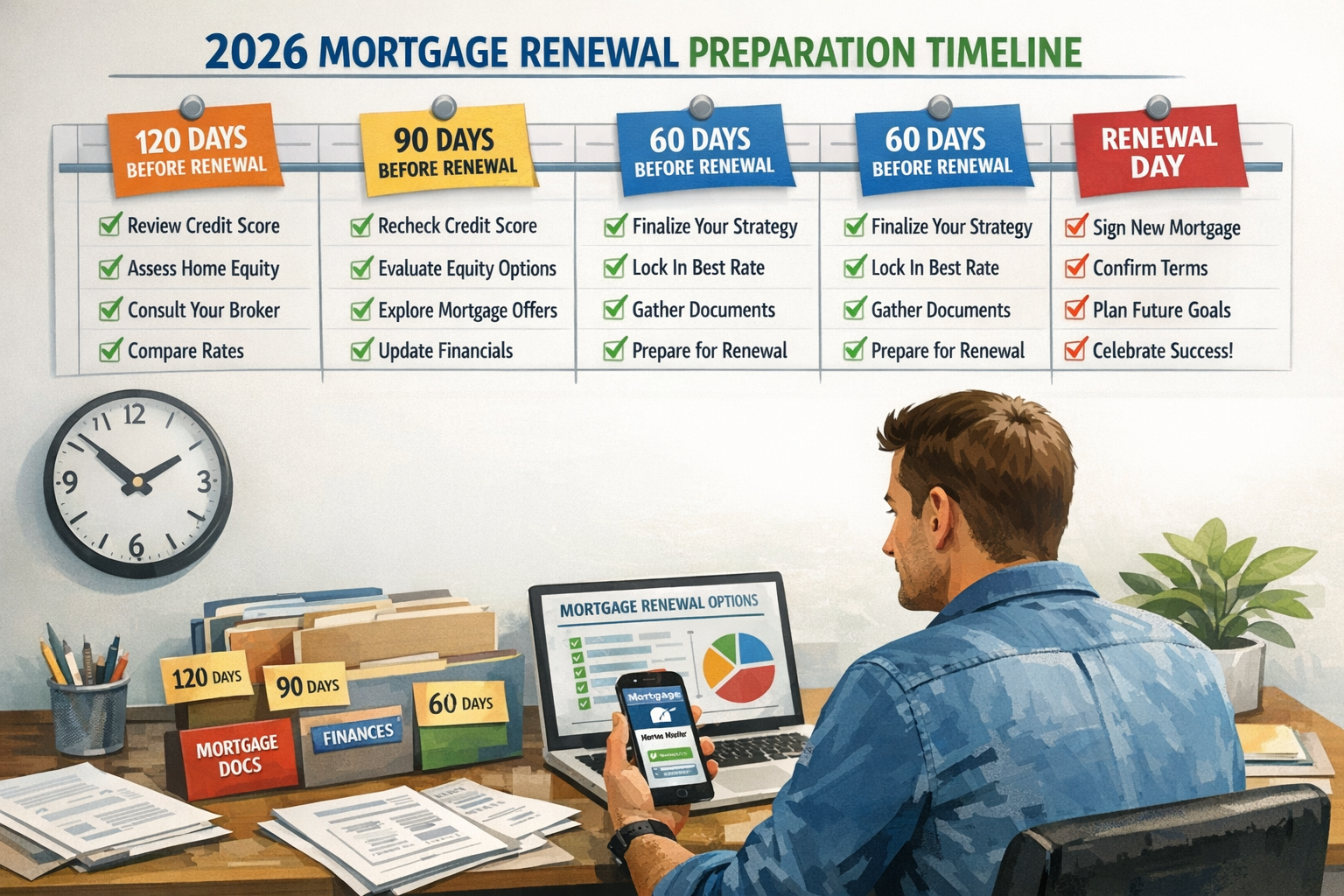

Timeline: 120 Days Before Your Renewal Date

The most successful refinancing outcomes happen when homebuyers start early. This section of the Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing provides a detailed timeline to maximize your options.

🗓️ 120 Days Out: Assessment Phase

Week 1-2: Gather Your Financial Information

Create a comprehensive financial snapshot:

- Current mortgage statement (balance, rate, payment, maturity date)

- Recent pay stubs (last 3 months)

- T4s and Notice of Assessment (last 2 years)

- Credit card statements (to calculate debt ratios)

- Property tax bill and condo fees (if applicable)

- Current credit score (check for free through borrowell.com or creditkarma.ca)

Week 3-4: Calculate Your Equity Position

Understanding your equity is crucial:

- Determine current home value: Check comparable sales on Realtor.ca or HouseSigma

- Calculate equity: Current value minus remaining mortgage balance

- Determine equity percentage: (Equity ÷ Current value) × 100

Example calculation:

- Current home value: $750,000

- Remaining mortgage: $615,000

- Home equity: $135,000

- Equity percentage: 18%

If you’re below 20% equity, you may need to bring additional funds or accept CMHC insurance costs.

🗓️ 90 Days Out: Exploration Phase

Consult with a Toronto Mortgage Broker

This is the single most important step. A Toronto mortgage broker has access to:

- 30+ lenders (vs. 1 if you go directly to your bank)

- Exclusive rates not advertised publicly

- Alternative solutions for unique situations

- Expert negotiation skills

Questions to ask your broker:

- What refinancing rate can you secure for my situation?

- How much can I reduce my monthly payment through refinancing?

- Should I extend my amortization, and by how much?

- Can I consolidate other debts into my refinance?

- What are the total costs (legal fees, appraisal, penalties)?

- How does refinancing compare to just accepting my renewal?

Review Your Current Mortgage Terms

Check for:

- Prepayment penalties: IRD (Interest Rate Differential) or three months’ interest

- Portability options: Can you transfer your mortgage if you move?

- Blended rate possibilities: Some lenders offer to blend your old and new rates

Understanding fixed versus variable mortgage options becomes critical at this stage—your choice affects payment stability for the next 5 years.

🗓️ 60 Days Out: Decision Phase

Compare All Your Options

Create a comparison chart:

| Option | Monthly Payment | Total Interest (5 yrs) | Pros | Cons |

|---|---|---|---|---|

| Standard Renewal | $4,250 | $125,000 | Simple process | Unaffordable |

| Refinance (30yr) | $3,380 | $148,000 | Manageable payment | More interest |

| Refinance + Debt Consolidation | $3,650 | $152,000 | One payment, lower rate on debts | Longer payoff |

| Variable Rate Refinance | $3,520 | $135,000 (est.) | Lower starting rate | Payment uncertainty |

Lock in Your Rate

Once you’ve decided on refinancing:

- Submit full application to your chosen lender

- Provide all requested documentation promptly

- Schedule home appraisal if required

- Lock in your rate (typically holds for 90-120 days)

🗓️ 30 Days Out: Execution Phase

Finalize Legal and Administrative Details

- Hire a real estate lawyer (budget $1,200-$1,800 in Toronto)

- Review and sign all mortgage documents

- Arrange for funds if bringing money to closing

- Confirm exact closing/funding date

Notify Your Current Lender

Even though you’re refinancing away from them, professional courtesy (and sometimes contractual obligation) requires notification. This also gives them one last chance to compete—sometimes they’ll improve their offer.

Common Refinancing Mistakes to Avoid

❌ Waiting until the last minute: Starting 30 days before renewal limits your options severely

❌ Only talking to your current bank: Banks prioritize their profits, not your best interests

❌ Ignoring the total cost: Focus on monthly payment AND total interest over the term

❌ Extending amortization unnecessarily: Only extend as much as needed to manage payments

❌ Not improving credit first: A 50-point credit score increase can save thousands

❌ Forgetting about penalties: Calculate prepayment penalties before committing

❌ Overlooking debt consolidation: High-interest debts might be your biggest problem

For a comprehensive list of pitfalls, review common mistakes to avoid when applying for a mortgage.

Special Considerations for Different First-Time Buyer Situations

For Self-Employed First-Time Buyers

Self-employed homeowners face unique challenges during refinancing. Traditional lenders require:

- Two years of Notice of Assessments

- Business financial statements

- Proof of ongoing contracts/income

If documentation is challenging, consider:

- Stated income programs through alternative lenders

- Longer amortizations to offset higher rates

- Larger down payments to improve qualification

Learn more about self-employed mortgage options specific to your situation.

For First-Time Buyers with Credit Challenges

If your credit score has dropped since purchase (job loss, medical emergency, divorce):

- Work on credit repair immediately: Pay down credit cards, dispute errors

- Consider a co-signer: Parent or family member with strong credit

- Explore alternative lenders: More flexible credit requirements

- Accept a shorter term: 1-2 year term to rebuild credit, then refinance again

Even with bad credit in Ontario, refinancing options exist—they just require more strategic planning.

For First-Time Buyers Considering Selling

Sometimes the best solution is acknowledging the home is no longer affordable. Before deciding:

Calculate your break-even point:

- Current home value

- Minus: Remaining mortgage balance

- Minus: Real estate commission (4-5%)

- Minus: Legal fees ($1,500-$2,000)

- Minus: Land transfer tax on new purchase

- Equals: Net proceeds

If selling leaves you with minimal equity and you’ll face similar or higher costs to rent or buy something smaller, refinancing to stay put often makes more financial sense.

Advanced Refinancing Strategies for Maximum Savings

Strategy 1: The Debt Consolidation Refinance

For first-time homebuyers carrying high-interest debt alongside their mortgage, debt consolidation through refinancing can be transformative.

Example scenario:

Before refinancing:

- Mortgage payment: $2,800

- Car loan: $550

- Credit cards: $400

- Student loan: $350

- Total monthly debt: $4,100

After debt consolidation refinance:

- New mortgage payment (all debts included): $3,650

- Total monthly debt: $3,650

- Monthly savings: $450

The key is that you’re trading 19% credit card debt and 7% car loan debt for 4.7% mortgage debt—a massive interest savings that compounds over time.

Strategy 2: The Equity Access Refinance

If you need funds for home improvements, emergency savings, or investment opportunities, accessing equity through refinancing can be smarter than high-interest alternatives.

Toronto home equity example:

- Original purchase (2021): $680,000

- Current value (2026): $795,000

- Appreciation: $115,000

- Principal paid down: $32,000

- Total available equity: $147,000

- Maximum you can access (80% LTV): $636,000 – $648,000 remaining = Access limited by current balance

You can refinance up to 80% of your home’s value, which means accessing approximately $88,000 in this scenario while refinancing your mortgage.

Smart uses for accessed equity:

- ✅ High-ROI renovations (kitchen, bathroom, basement)

- ✅ Emergency fund (6 months expenses)

- ✅ Investment in income-producing assets

- ❌ Vacations or depreciating purchases

- ❌ Speculative investments

Strategy 3: The Split-Term Refinance

Instead of putting all your eggs in one basket, consider splitting your refinanced mortgage:

Example split:

- 60% in a 5-year fixed at 4.8% (stability)

- 40% in a 3-year variable at 4.2% (flexibility and lower rate)

Benefits:

- Diversified rate risk

- Partial renewal in 3 years if rates drop

- Lower blended rate than 100% fixed

- Flexibility to pay down variable portion aggressively

This sophisticated approach requires guidance from an experienced broker but can save thousands over the mortgage lifetime.

Strategy 4: The Amortization Optimization Approach

Rather than automatically extending to 30 years, optimize your amortization based on:

Your age and career stage:

- Under 35: 28-30 years acceptable (long earning years ahead)

- 35-45: 25-27 years balanced (retirement planning matters)

- Over 45: Minimize extension (retirement approaching)

Your income trajectory:

- Expect raises/promotions: Shorter amortization with prepayment privileges

- Stable income: Moderate extension with annual lump-sum payments

- Uncertain income: Maximum extension for payment flexibility

Your other financial goals:

- Saving for kids’ education: Extend amortization, invest the savings

- Building retirement savings: Extend mortgage, maximize RRSP contributions

- Paying off mortgage quickly: Minimal extension, aggressive prepayments

This Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing emphasizes that one size doesn’t fit all—your refinancing strategy should align with your complete financial picture.

Preparing for Future Renewals: Building Long-Term Resilience

Creating a Mortgage Payment Buffer

Once you’ve successfully refinanced and reduced your payment, don’t just spend the savings. Build resilience:

The 50/50 rule:

- Save 50% of your payment reduction

- Use 50% for improved cash flow

Example:

- Payment reduced by $800/month through refinancing

- Save $400/month in high-interest savings account

- Use $400/month for improved quality of life or debt reduction

In one year, you’ll have $4,800 saved—enough to cover several months of payments in an emergency or make a lump-sum prepayment.

Accelerated Payment Strategies

Most refinanced mortgages include prepayment privileges:

- Annual lump-sum: Typically 10-20% of original principal

- Increased payments: Usually 10-20% payment increase allowed

- Double-up payments: Make extra payments matching regular ones

Smart acceleration approach:

- Year 1-2 post-refinance: Focus on building emergency fund

- Year 3-4: Begin annual lump-sum payments (tax refunds, bonuses)

- Year 5: Increase regular payment by 10% if income allows

This disciplined approach helps you recover the extended amortization while maintaining payment flexibility.

Monitoring Your Mortgage Health

Set up a quarterly mortgage review:

Every 3 months, check:

- ✓ Remaining balance (is it decreasing as expected?)

- ✓ Current home value (check comparable sales)

- ✓ Equity position (improving toward 30-35%?)

- ✓ Credit score (maintaining or improving?)

- ✓ Interest rate environment (are rates dropping?)

Annual deep dive:

- Review your complete financial situation

- Consider making lump-sum prepayment

- Assess whether you should refinance again

- Update your 5-year financial plan

Planning for Your Next Renewal

Your 2026 refinancing isn’t the end—it’s the beginning of smarter mortgage management. Start planning for your next renewal immediately:

2-3 years before next renewal:

- Build relationship with mortgage broker

- Improve credit score to 750+

- Reduce other debts aggressively

- Increase home equity to 30%+

1 year before next renewal:

- Lock in rate if trending upward

- Compare fixed versus variable options

- Consider shorter term (3-year) if rates are high

- Evaluate whether to switch lenders

This proactive approach ensures you’re never caught off-guard by renewal shock again.

Building Wealth Beyond Your Mortgage

While managing your mortgage is critical, true financial resilience comes from diversification:

Parallel wealth-building strategies:

💰 Emergency fund: 6 months expenses in HISA (5%+ interest)

📈 TFSA investments: Max contribution ($7,000/year in 2026) in diversified ETFs

🏦 RRSP contributions: Especially if employer matching available

🎓 RESP for children: Government grants = free money

🏠 Home equity growth: Through market appreciation and principal paydown

For Toronto first-time homebuyers, balancing mortgage and retirement savings is essential—don’t sacrifice long-term wealth building just to pay off your mortgage faster.

Working with Professionals: Maximizing Your Refinancing Success

The Value of a Mortgage Broker

The difference between going directly to your bank versus working with a broker can mean:

- $15,000-$30,000 in interest savings over 5 years

- $200-$500 lower monthly payments

- Access to 30+ lenders instead of just one

- Expert negotiation on your behalf

- Time savings (broker handles paperwork and coordination)

What to look for in a Toronto mortgage broker:

✓ Licensed with FSRA (Financial Services Regulatory Authority)

✓ Minimum 5+ years experience

✓ Specialization in first-time buyers and refinancing

✓ Access to both A-lenders and alternative lenders

✓ Transparent about compensation (lender-paid vs. client-paid)

✓ Strong reviews and testimonials

✓ Responsive communication (answers within 24 hours)

A qualified Toronto mortgage broker becomes your advocate, fighting for the best possible terms while you focus on your career and family.

The Role of a Real Estate Lawyer

Refinancing requires legal work, and choosing the right lawyer matters:

What your lawyer handles:

- Title search and insurance

- Mortgage discharge (old lender)

- Mortgage registration (new lender)

- Fund transfer and holdbacks

- Property tax adjustments

Toronto refinancing legal fees (2026):

- Legal fees: $800-$1,200

- Disbursements: $300-$500

- Title insurance: $250-$400

- Total: $1,350-$2,100

Some lenders offer cashback promotions that cover legal fees—ask your broker about current offers.

When to Consult a Financial Planner

For complex situations, a fee-only financial planner provides valuable perspective:

Consider a planner if:

- You have significant investments outside your home

- You’re self-employed with variable income

- You’re planning major life changes (kids, career shift)

- You have inheritance or windfall to deploy strategically

- Your debt situation is overwhelming

A comprehensive financial plan ensures your refinancing decision aligns with retirement goals, tax optimization, and estate planning—not just immediate payment relief.

Conclusion: Taking Control of Your Financial Future

The Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing has equipped you with the knowledge, strategies, and action steps to transform a potential crisis into an opportunity for financial stability. While the statistics are sobering—60% of mortgages renewing in 2026[4], payment increases of 15%-20%[2], and individual payment jumps of $1,000-$2,000[1]—you now have a clear roadmap forward.

Your Next Steps (Start Today)

Immediate actions (this week):

- ✅ Calculate your mortgage renewal date and current equity position

- ✅ Check your credit score and review your credit report

- ✅ Gather financial documents (pay stubs, tax returns, mortgage statement)

- ✅ Contact a Toronto mortgage broker for a free consultation

- ✅ Review your complete debt picture (credit cards, loans, lines of credit)

Short-term actions (next 30 days):

- ✅ Obtain refinancing quotes from multiple sources

- ✅ Calculate payment scenarios for different amortization periods

- ✅ Assess whether debt consolidation makes sense

- ✅ Improve credit score (pay down credit cards, dispute errors)

- ✅ Create a household budget that includes higher mortgage payments

Medium-term actions (next 90 days):

- ✅ Make refinancing decision and submit application

- ✅ Complete home appraisal if required

- ✅ Hire real estate lawyer and review all documents

- ✅ Build emergency fund with payment savings

- ✅ Set up automatic savings for future lump-sum prepayments

The Bottom Line

Refinancing isn’t about avoiding responsibility—it’s about smart financial management in the face of unprecedented rate increases. By extending your amortization, consolidating high-interest debts, and leveraging your built-up equity, you can reduce monthly payments by hundreds or even thousands of dollars while maintaining homeownership.

The first-time homebuyers who will thrive through the 2026 renewal shock are those who:

- 🎯 Act proactively rather than reactively

- 💡 Seek expert guidance from brokers and advisors

- 📊 Make data-driven decisions based on complete financial pictures

- 🔄 Stay flexible and adapt strategies as circumstances change

- 📈 Think long-term beyond just the immediate payment crisis

Remember: you’re not alone in facing this challenge. Hundreds of thousands of Canadian homeowners are navigating the same renewal shock. The difference between those who struggle and those who succeed often comes down to taking action early and getting the right professional help.

Resources and Support

For personalized guidance on your specific situation:

- 📞 Book a free consultation with a mortgage professional

- 📧 Get a refinancing assessment tailored to your circumstances

- 💻 Use mortgage calculators to model different scenarios

- 📚 Continue learning about mortgage strategies and options

The 2026 mortgage renewal shock is real, but with the strategies outlined in this Toronto First-Time Home Buyers’ Guide to Surviving the 2026 Mortgage Renewal Shock Through Refinancing, you have everything you need to not just survive—but to build a stronger financial foundation for the decades ahead.

Your home is likely your largest investment and your family’s sanctuary. Protecting it through strategic refinancing isn’t just financially smart—it’s essential for your peace of mind and long-term prosperity. Start your refinancing journey today, and transform renewal shock into renewal opportunity.

References

[1] Watch – https://www.youtube.com/watch?v=atQyYwTgCGQ

[2] Staff Analytical Note 2025 21 – https://www.bankofcanada.ca/2025/07/staff-analytical-note-2025-21/

[3] Watch – https://www.youtube.com/watch?v=BnKwllolN4U

[4] Mortgage Renewal Canada – https://www.fairstone.ca/en/learn/finance-101/mortgage-renewal-canada

[5] F9a87ba8 9962 4265 A2a9 E51303e269ca – https://economics.bmo.com/en/publications/detail/f9a87ba8-9962-4265-a2a9-e51303e269ca/