February 4, 2026

How 2026 Mortgage Renewals Impact First-Time Home Buyers Refinancing in Toronto

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

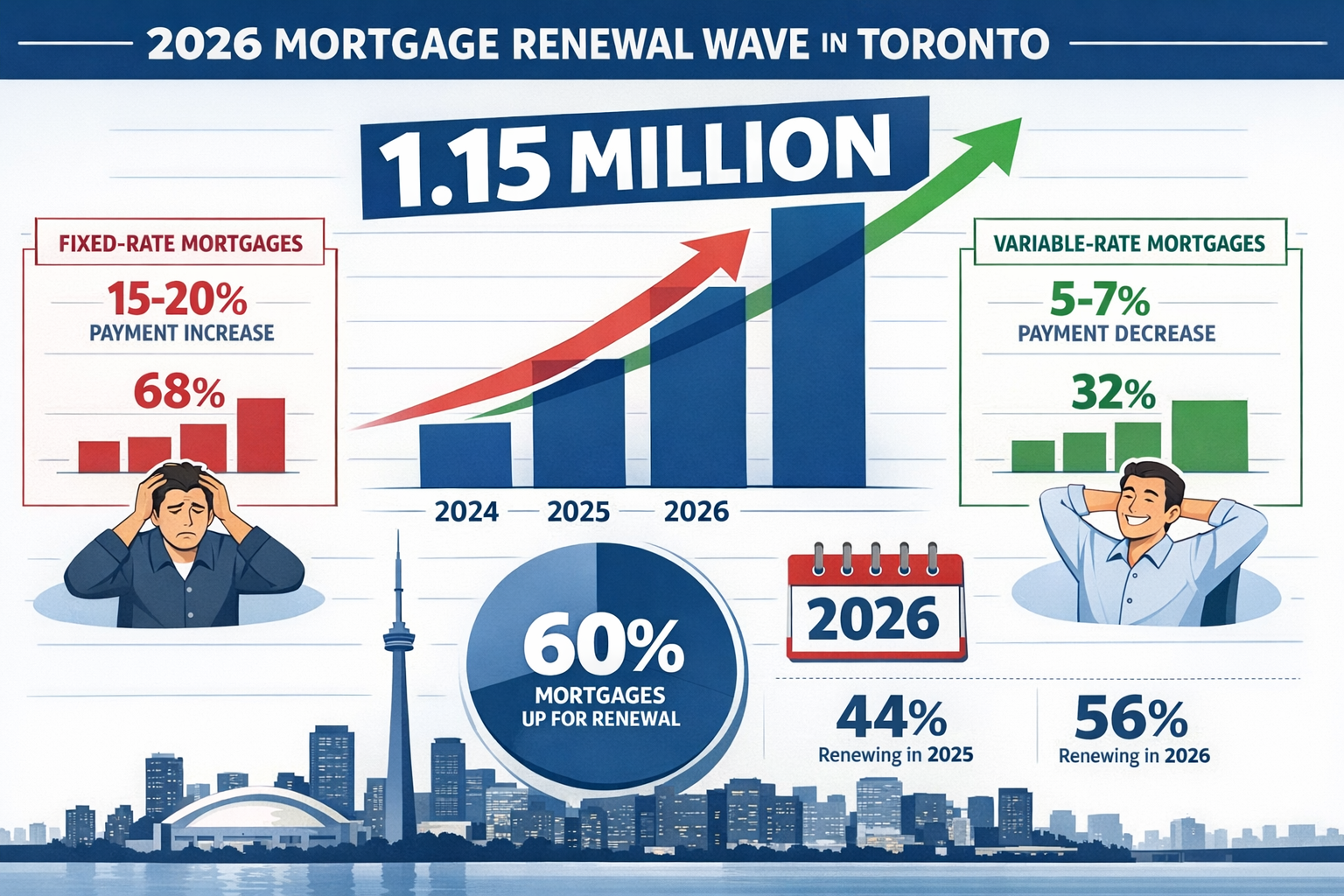

The Canadian mortgage landscape is approaching a critical inflection point. With over 1.15 million mortgage holders set to renew their contracts in 2026, first-time home buyers in Toronto face a perfect storm of challenges and opportunities.[1] Understanding how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto has never been more crucial, as payment increases of up to 20% loom for those who secured fixed-rate mortgages during the low-rate environment of 2020-2021.[3]

This unprecedented renewal wave represents one of the largest in Canadian history, with approximately 60% of all outstanding mortgages coming due by year-end 2026.[4] For Toronto’s first-time buyers—many of whom stretched their budgets to enter the market during peak prices—the stakes couldn’t be higher. However, the story isn’t entirely bleak. Strategic refinancing, lender switching, and leveraging Toronto’s unique equity dynamics can transform potential payment shock into manageable transitions.

Key Takeaways

✅ 1.15 million Canadians will renew mortgages in 2026, with fixed-rate borrowers facing average payment increases of 15-20%, while variable-rate holders may see decreases of 5-7%[3]

✅ The “loyalty tax” costs $1,860 annually for borrowers who don’t shop around, yet 69% of Canadians stay with their current lender at renewal[1]

✅ Toronto’s 25% housing value correction from early-2022 peaks affects equity positions but creates refinancing opportunities for strategic buyers[1]

✅ Extending amortization by five years can eliminate payment increases for approximately half of affected borrowers facing higher costs[3]

✅ First-time buyers with equity growth can access home equity lines of credit or refinance to consolidate debt and manage cash flow during renewal[3]

Understanding the 2026 Mortgage Renewal Wave in Toronto

The Scale and Scope of Renewals

The 2026 mortgage renewal cycle represents an extraordinary moment in Canadian financial history. Over 1.15 million mortgage holders across the country will face renewal decisions this year, with Toronto and the Greater Toronto Area (GTA) accounting for a substantial portion of this volume.[1] This concentration reflects Toronto’s position as Canada’s largest real estate market and the aggressive buying activity that characterized the 2020-2021 period.

The timing of these renewals is particularly significant. Most borrowers renewing in 2026 secured their mortgages during the ultra-low interest rate environment that prevailed during the COVID-19 pandemic, when five-year fixed rates dipped below 2% and variable rates were even lower. Now, as these terms expire, borrowers confront a dramatically different rate landscape.

Key statistics defining the 2026 renewal wave:

| Metric | Value | Source |

|---|---|---|

| Total renewals in 2026 | 1.15 million | [1] |

| Percentage of outstanding mortgages | 60% by year-end | [4] |

| Average payment increase (fixed-rate) | 15-20% | [3] |

| Average payment change (variable-rate) | -5% to -7% | [3] |

| Borrowers staying with current lender | 69% | [1] |

How 2026 Mortgage Renewals Impact First-Time Home Buyers Refinancing in Toronto: Payment Shock Realities

For first-time home buyers in Toronto, the payment shock associated with renewal varies dramatically based on the type of mortgage product they originally selected. Understanding these differences is essential for planning and mitigation strategies.

Fixed-rate mortgage holders face the most significant challenges. Those who locked in five-year fixed rates between 2020-2021 at approximately 1.5-2.5% are now renewing into an environment where comparable products range from 4.5-5.5%. This differential translates to average payment increases of 15-20% compared to December 2024 payment levels.[3]

For a Toronto first-time buyer with a $600,000 mortgage at 2% renewing at 5%, the monthly payment could jump from approximately $2,530 to $3,500—an increase of nearly $1,000 per month or $12,000 annually. For households already stretched thin by Toronto’s high cost of living, this represents a severe financial burden.

Variable-rate mortgage holders experience a more nuanced picture. Those with variable-rate, variable-payment mortgages have already absorbed rate increases through higher monthly payments over the past several years. As a result, many will see payment decreases of 5-7% at renewal as they lock in rates that are actually lower than the peak variable rates they’ve been paying.[3]

However, borrowers with variable-rate, fixed-payment mortgages face a different challenge. Approximately 10% of these borrowers will experience payment increases exceeding 40% as they confront the accumulated impact of negative amortization—where their payments weren’t sufficient to cover interest, causing their principal balance to grow.[3]

The Toronto-Specific Context

Toronto’s real estate market dynamics add unique considerations to how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto. The GTA has experienced a 25% decline in housing values from the early-2022 peak, fundamentally altering the equity position of recent buyers.[1]

For first-time buyers who purchased near the market peak in early 2022, this correction has eroded equity and may limit refinancing options. Those with less than 20% equity cannot refinance without mortgage default insurance, and some may find themselves with negative equity if they made minimal down payments.

Conversely, buyers who entered the market in 2019-2020 or earlier have likely maintained or grown their equity despite the correction, providing valuable flexibility for refinancing strategies. This equity can be leveraged through home equity lines of credit (HELOCs) or cash-out refinancing to manage payment increases or consolidate higher-interest debt.

Toronto’s employment market also plays a role. As Canada’s financial and business hub, the city offers relatively strong income growth potential, which may help first-time buyers qualify for renewals despite higher payments. However, the mortgage stress test requirements mean borrowers must qualify at rates significantly above their actual contract rate, creating qualification challenges even for employed borrowers.

Refinancing Strategies for First-Time Home Buyers Facing 2026 Renewals

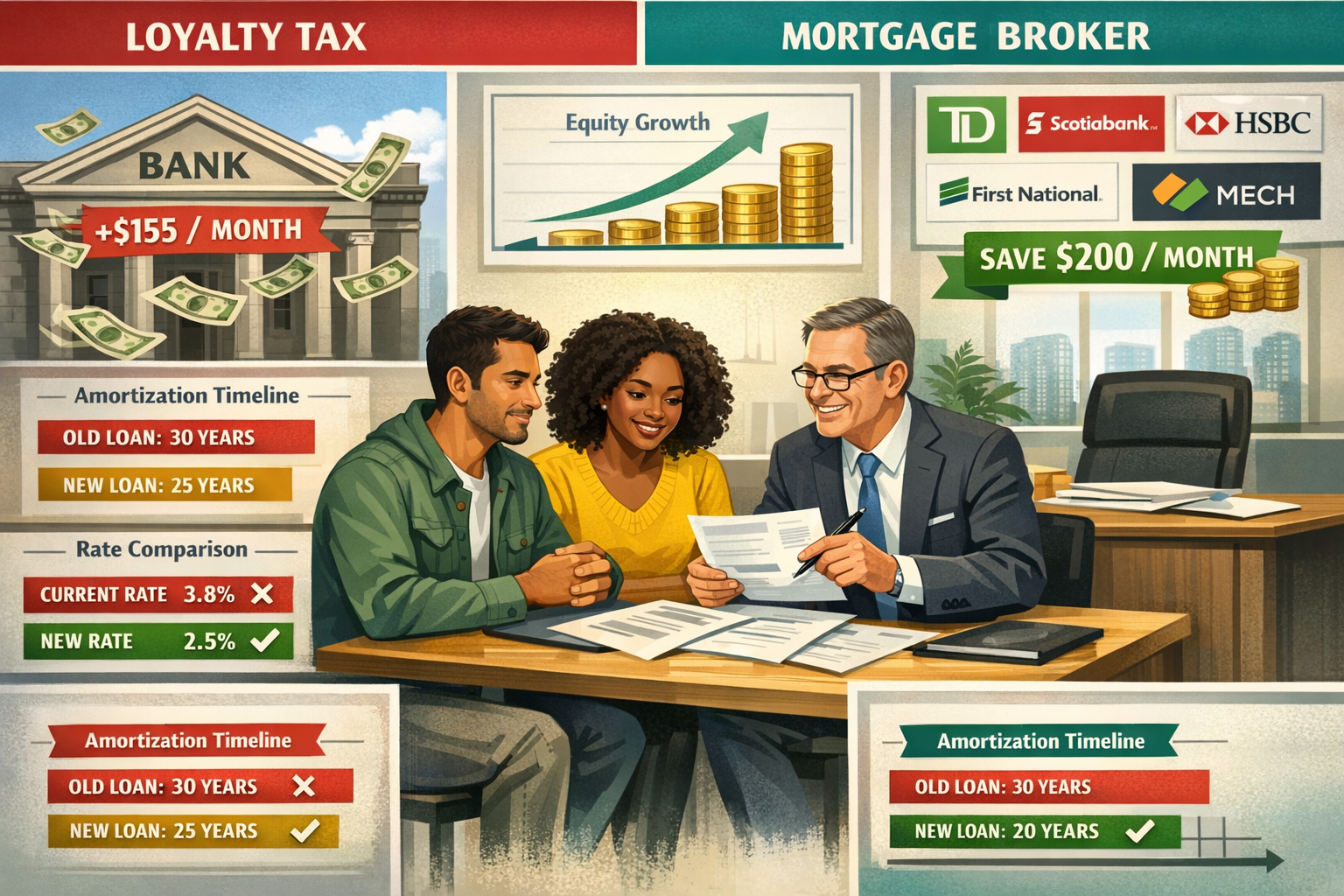

The Costly “Loyalty Tax” and Why Switching Matters

One of the most significant yet overlooked aspects of how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto is the “loyalty tax”—the premium paid by borrowers who simply accept their existing lender’s renewal offer without shopping around.

According to Ratehub.ca data, Canadians who remain with their current lender at renewal pay an average of $155 more per month than those who switch to a more competitive lender.[1] Over a five-year term, this seemingly modest difference compounds to:

- $1,860 additional cost annually

- $9,300 over the full five-year term

Despite these substantial savings opportunities, 69% of Canadian borrowers stay with their current lender at renewal.[1] This tendency stems from several factors:

🔍 Convenience bias: The renewal process with an existing lender requires minimal paperwork and effort

🔍 Information asymmetry: Many borrowers don’t realize how much they could save by switching

🔍 Relationship inertia: Long-standing banking relationships create psychological barriers to change

🔍 Perceived complexity: First-time buyers may feel intimidated by the switching process

For Toronto first-time buyers facing payment increases, eliminating the loyalty tax through lender switching can partially or fully offset rate-driven payment increases. A borrower renewing a $500,000 mortgage who saves $155 monthly through switching preserves $1,860 in annual cash flow—money that can be redirected toward other financial priorities or emergency savings.

Extending Amortization to Manage Payment Increases

One of the most powerful tools for managing how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto is amortization extension. Bank of Canada analysis suggests that approximately half of borrowers facing payment increases could eliminate them entirely by extending their amortization period by five years.[3]

How amortization extension works:

When a mortgage renews, borrowers have the opportunity to reset their amortization period, even if they’ve already paid down several years of their original term. For example, a borrower who took a 25-year amortization in 2021 would have 20 years remaining at their 2026 renewal. By extending back to 25 years (or even 30 years, if eligible), they spread the remaining principal over more payments, reducing the monthly amount.

Example calculation:

- Remaining balance: $550,000

- Remaining amortization: 20 years

- New rate: 5.0%

- Payment at 20-year amortization: $3,630/month

- Payment at 25-year amortization: $3,220/month

- Monthly savings: $410/month ($4,920 annually)

This strategy is particularly valuable for Toronto first-time buyers who stretched their budgets to enter the market and need immediate payment relief. The trade-off is paying more interest over the life of the mortgage, but for many households, the short-term cash flow benefit outweighs the long-term cost.

Important considerations:

⚠️ Qualification requirements: Extended amortizations still require stress test qualification at higher rates

⚠️ Equity requirements: Borrowers with less than 20% equity may face restrictions on amortization extensions

⚠️ Long-term cost: A five-year extension can add tens of thousands in total interest paid over the mortgage life

⚠️ Future flexibility: Borrowers can make lump-sum payments or increase regular payments to accelerate paydown when finances improve

Leveraging Equity Through Refinancing and HELOCs

For Toronto first-time buyers with meaningful equity accumulation, refinancing presents opportunities beyond simple rate renewal. Despite the 25% market correction from peak values, many borrowers who purchased before 2021 have substantial equity through a combination of principal paydown and earlier appreciation.[1]

Refinancing strategies for equity-rich borrowers:

1. Cash-out refinancing for debt consolidation

First-time buyers often carry high-interest debt from credit cards, car loans, or personal loans. Refinancing to access equity and consolidate these debts into the mortgage can improve overall cash flow, even if the mortgage payment increases slightly.

Example: A borrower with $30,000 in credit card debt at 20% APR pays $500/month in interest alone. Refinancing to incorporate this debt at 5% mortgage rates reduces the interest cost to $125/month, freeing up $375 monthly for other expenses.

2. HELOC establishment for payment flexibility

Home equity lines of credit provide a safety net for managing variable expenses or temporary income disruptions. Many households have repaid substantial mortgage principal and could access HELOCs as a short-term payment solution during renewal transitions.[3]

HELOCs typically allow borrowing up to 65% of home value (or 80% combined with the first mortgage), providing access to liquidity without the commitment of a fixed loan. For Toronto buyers facing payment shock, a HELOC can bridge temporary cash flow gaps while income adjusts or other financial strategies take effect.

3. Refinancing for home improvements

Toronto’s competitive housing market often requires buyers to purchase properties needing renovation. Refinancing to access equity for value-adding improvements can be strategic, particularly if the renovations increase property value and rental income potential (for properties with legal secondary suites).

Those interested in understanding closing costs associated with refinancing should factor these expenses into their refinancing calculations, as they can range from 1.5-4% of the mortgage amount.

Working with Mortgage Brokers vs. Banks

Understanding how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto requires recognizing the value of professional guidance. Mortgage brokers offer distinct advantages over traditional bank channels, particularly during complex renewal scenarios.

Advantages of mortgage brokers for 2026 renewals:

✅ Access to multiple lenders: Brokers work with dozens of lenders, including banks, credit unions, and alternative lenders, providing comprehensive rate comparisons

✅ Negotiating power: Brokers can leverage competition among lenders to secure better rates and terms than individual borrowers typically obtain

✅ Specialized knowledge: Experienced brokers understand nuances of different mortgage products and can match borrowers with optimal solutions

✅ No cost to borrowers: Lenders pay broker commissions, so borrowers receive professional advice without direct fees

✅ Problem-solving for complex situations: For first-time buyers with credit issues, employment changes, or equity challenges, brokers can identify lenders with appropriate risk appetites

For Toronto first-time buyers navigating renewal, working with a mortgage broker can mean the difference between accepting a loyalty-taxed renewal offer and securing competitive terms that save thousands annually.

Avoiding Common Mistakes During 2026 Mortgage Renewals

Mistake #1: Accepting the First Renewal Offer

The single most costly mistake first-time buyers make is passively accepting their lender’s initial renewal offer. These offers typically arrive 30-120 days before the renewal date and are deliberately designed to appear convenient and reasonable—but they rarely represent the lender’s best available rate.

Why initial offers are inflated:

Banks and lenders count on borrower inertia. They know that most customers will accept the first offer for convenience, allowing the lender to maintain higher profit margins. The initial renewal rate often includes a 0.20-0.50% premium above what the lender would offer to a new customer or a borrower who actively negotiates.

The correct approach:

🎯 Start shopping 120 days before renewal: This provides maximum time to compare options and negotiate

🎯 Obtain at least 3-5 competitive quotes: Include quotes from brokers, other banks, and credit unions

🎯 Use competing offers as leverage: Present better offers to your current lender and request a match or beat

🎯 Don’t reveal your bottom line: Negotiate from the competing offers, not from your willingness to pay

First-time buyers who actively negotiate typically secure rates 0.25-0.50% lower than the initial offer, translating to substantial monthly savings.

Mistake #2: Ignoring Qualification Changes

Many Toronto first-time buyers assume that because they qualified for their original mortgage, renewal will be automatic. This assumption can be dangerous, particularly for borrowers whose financial circumstances have changed or who face significantly higher renewal rates.

Qualification factors that may have changed:

📊 Income reduction: Job changes, parental leave, or business income fluctuations

📊 Credit score deterioration: Late payments, increased debt utilization, or collections

📊 Debt accumulation: New car loans, credit card balances, or personal loans that increase debt service ratios

📊 Employment status: Transition to self-employment or contract work, which lenders view as higher risk

The mortgage stress test requires borrowers to qualify at the greater of their contract rate plus 2% or 5.25%, meaning a renewal at 5% requires qualification at 7%. For borrowers whose debt levels have increased since their original purchase, this can create qualification challenges.

Proactive solutions:

✔️ Review qualification early: Work with a mortgage professional to assess qualification 6-12 months before renewal

✔️ Pay down high-interest debt: Reducing credit card balances and car loans improves debt service ratios

✔️ Improve credit score: Address any credit issues well in advance of renewal

✔️ Document income carefully: Self-employed borrowers should work with accountants to optimize income documentation

First-time buyers who discover qualification issues early have time to address them before renewal, avoiding last-minute scrambles or forced acceptance of unfavorable terms. Those who are self-employed should understand specialized qualification requirements.

Mistake #3: Overlooking Penalty Implications for Early Refinancing

Some Toronto first-time buyers consider breaking their current mortgage before the renewal date to access better rates or refinancing opportunities. While this can be strategic in certain scenarios, mortgage penalties can be substantial and must be carefully calculated.

Penalty calculation methods:

For variable-rate mortgages: Penalties are typically three months of interest, which is relatively modest and often worth paying to access significantly better rates or terms.

For fixed-rate mortgages: Penalties are the greater of three months of interest or the Interest Rate Differential (IRD), which can be substantial—sometimes $10,000-$30,000 or more on large Toronto mortgages.

The IRD calculation compares your current rate to the rate the lender can charge for the remaining term. When rates have fallen, IRD penalties are higher; when rates have risen (as in the current environment), IRD penalties are lower.

When breaking early makes sense:

✅ Accessing equity for high-return investments: If refinancing provides capital for investments returning more than the penalty cost

✅ Consolidating very high-interest debt: When credit card or personal loan interest exceeds the annualized penalty cost

✅ Taking advantage of significant rate drops: If rates have fallen substantially and the penalty can be recouped through savings

✅ Avoiding payment shock: For borrowers facing severe financial hardship, early refinancing with amortization extension might justify penalty costs

When to wait for renewal:

⛔ Modest rate differences: If the rate improvement is less than 0.50%, waiting for penalty-free renewal is usually better

⛔ Short time to renewal: Within 6-12 months of renewal, penalties rarely justify early breaking

⛔ Uncertain financial situation: If income or employment is unstable, preserving cash is more important than optimizing rates

Mistake #4: Failing to Understand Product Features Beyond Rate

First-time buyers often focus exclusively on interest rates while overlooking critical mortgage features that affect flexibility and long-term costs. Understanding how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto requires evaluating the complete product package.

Essential features to compare:

Prepayment privileges: The ability to make lump-sum payments (typically 10-20% of original principal annually) and increase regular payments (typically 10-20% annually) without penalty. These features allow borrowers to accelerate paydown when finances improve.

Portability: The option to transfer your mortgage to a new property if you move before the term ends, preserving your rate and avoiding penalties. Particularly valuable in Toronto’s dynamic real estate market.

Assumability: The ability for a buyer to assume your mortgage when you sell, which can be a valuable selling feature if you have a below-market rate.

Conversion options: For variable-rate mortgages, the ability to convert to fixed rates without penalty provides protection against future rate increases.

Payment flexibility: Options to skip payments, make payment holidays, or adjust payment frequency can provide valuable cash flow management tools.

A mortgage with a rate 0.10% higher but superior prepayment privileges may ultimately cost less and provide more flexibility than a bare-bones product with the absolute lowest rate.

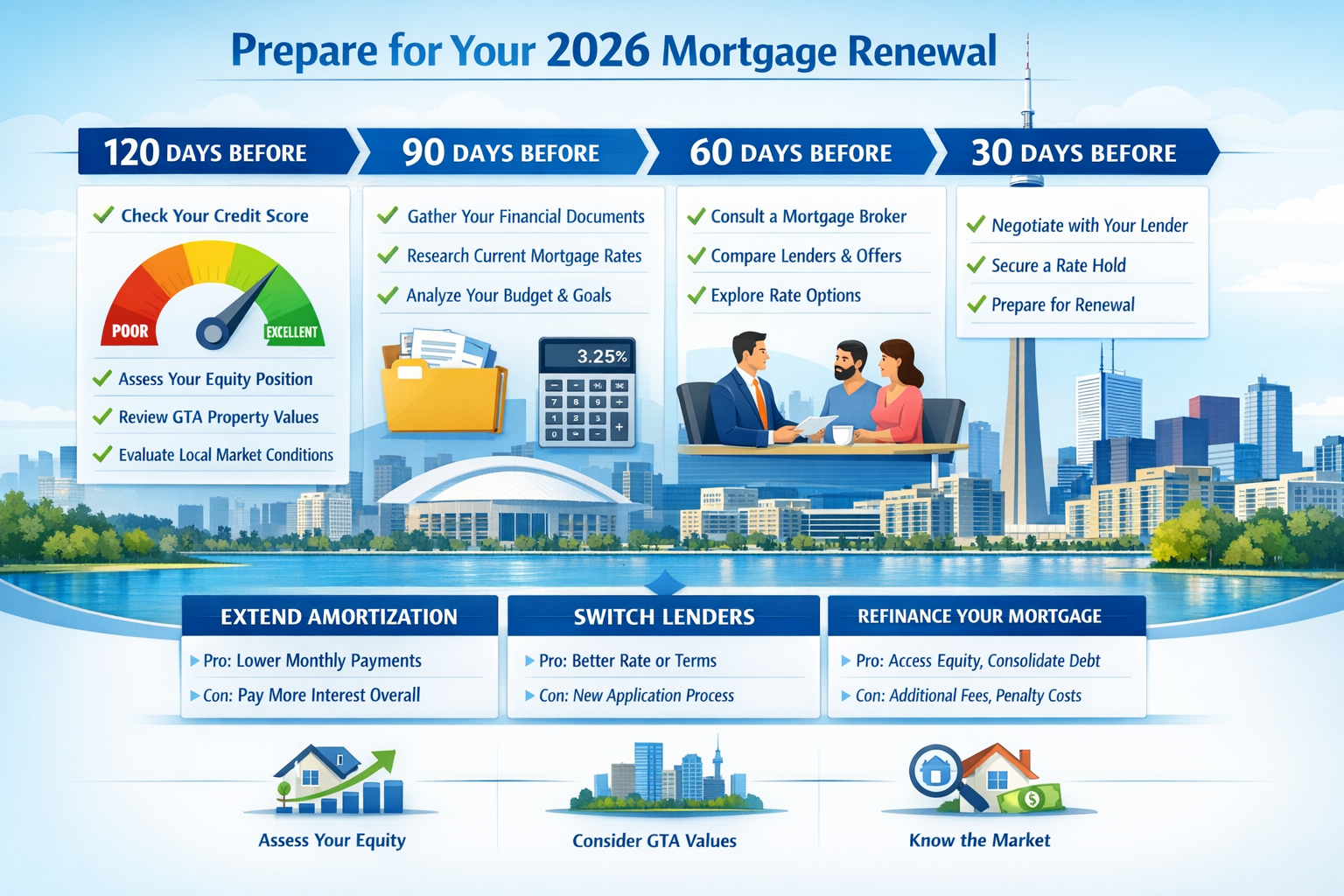

Preparing for Your 2026 Mortgage Renewal: Action Steps

120 Days Before Renewal: Assessment and Research

The optimal time to begin preparing for how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto is 120 days before your renewal date. This timeline provides sufficient time for thorough research, multiple consultations, and strategic decision-making without the pressure of looming deadlines.

Key actions at 120 days:

📋 Review your current mortgage details: Gather your original mortgage documents, note your current rate, remaining amortization, and any special features

📋 Assess your financial situation: Calculate your current debt service ratios, review your credit report, and document any income or employment changes since your original mortgage

📋 Determine your equity position: Obtain a current property valuation (through online tools, recent comparable sales, or professional appraisal) and calculate your loan-to-value ratio

📋 Identify your goals: Decide whether you’re prioritizing lowest payment, fastest paydown, maximum flexibility, or debt consolidation

📋 Research current rates: Review posted rates from major lenders and consult rate comparison websites to understand the current market

📋 Consult a mortgage broker: Schedule an initial consultation to discuss your situation and explore available options

First-time buyers who begin this process early avoid the common trap of accepting their lender’s first offer out of time pressure. Those looking to understand common first-time buyer mistakes can benefit from learning from others’ experiences.

90 Days Before Renewal: Obtaining Competitive Quotes

With 90 days remaining before renewal, the focus shifts to actively obtaining competitive quotes and beginning negotiations.

Quote collection strategy:

🎯 Request quotes from your current lender: Ask for their best renewal offer in writing, including rate, term options, and any special features

🎯 Obtain broker quotes: Work with a mortgage broker to access multiple lender options simultaneously

🎯 Approach credit unions: Credit unions often offer competitive rates and may be more flexible with qualification requirements

🎯 Consider alternative lenders: For borrowers with qualification challenges, alternative lenders may provide solutions, though typically at higher rates

🎯 Compare apples to apples: Ensure all quotes are for the same term length, amortization, and payment frequency for accurate comparison

Documentation to prepare:

- Recent pay stubs or income documentation

- Two years of tax returns (especially for self-employed buyers)

- Current mortgage statement

- Property tax bill

- Recent credit report

- List of all current debts and monthly payments

Having documentation ready accelerates the quote process and ensures lenders can provide accurate, qualified offers rather than estimates.

60 Days Before Renewal: Negotiation and Decision

At 60 days before renewal, Toronto first-time buyers should have multiple competitive quotes in hand and be ready to negotiate final terms.

Negotiation tactics:

💪 Lead with your best competing offer: Present the most competitive rate and terms to your current lender and request they match or beat it

💪 Emphasize your value as a customer: Highlight your payment history, additional products you hold with the lender, and your intention to remain a long-term customer if terms are competitive

💪 Be willing to walk: The most powerful negotiating position is genuine willingness to switch lenders if terms aren’t competitive

💪 Negotiate beyond rate: If the lender won’t match the lowest rate, request enhanced prepayment privileges, reduced fees, or other valuable features

💪 Get everything in writing: Verbal promises mean nothing; ensure all negotiated terms appear in the formal commitment

Decision framework:

When choosing among multiple competitive offers, consider:

- Total cost over the term: Calculate the total interest paid over the full term, not just monthly payments

- Qualification comfort: Ensure you comfortably qualify with room for future financial changes

- Feature alignment: Match mortgage features to your likely needs over the term

- Lender reputation: Consider customer service quality, digital tools, and problem-resolution capabilities

- Future flexibility: Evaluate portability, assumability, and refinancing options

30 Days Before Renewal: Finalization and Documentation

In the final 30 days before renewal, the focus shifts to completing documentation and ensuring a smooth transition.

Final steps:

✅ Complete lender application: If switching lenders, submit all required documentation promptly

✅ Arrange legal services: Switching lenders requires legal work; arrange for a real estate lawyer or notary

✅ Budget for costs: If switching lenders, budget for legal fees ($300-$800), appraisal fees if required ($300-$500), and any discharge fees from your current lender ($200-$350)

✅ Confirm rate hold: Ensure your negotiated rate is held in writing until your renewal date

✅ Review final documents carefully: Before signing, review all terms to ensure they match your negotiated agreement

✅ Set up new payment arrangements: If switching lenders, arrange for automatic payments from your bank account

For first-time buyers who decide to remain with their current lender, the process is simpler—typically just signing the renewal agreement. However, even in this scenario, careful review of all terms is essential to ensure no unfavorable changes have been introduced.

Special Considerations for Toronto First-Time Buyers

Toronto’s Unique Market Dynamics

How 2026 mortgage renewals impact first-time home buyers refinancing in Toronto is shaped by the city’s distinctive real estate characteristics. Understanding these local factors helps buyers make informed renewal decisions.

Greater Toronto Area market factors:

🏙️ Property type diversity: Toronto’s mix of condos, townhouses, and detached homes creates varying equity and appreciation patterns

🏙️ Condo market volatility: Toronto’s condo market has experienced more significant price corrections than detached homes, affecting equity positions differently based on property type

🏙️ Location-specific appreciation: Different Toronto neighborhoods have experienced varying levels of price correction and recovery, making individual property valuations critical

🏙️ Rental income potential: Toronto’s strong rental market provides opportunities for first-time buyers to generate income through legal secondary suites or basement apartments

🏙️ Municipal tax considerations: Toronto’s vacant home tax and other municipal policies affect property ownership costs and rental strategies

First-time buyers should obtain current property valuations specific to their neighborhood and property type rather than relying on city-wide statistics when assessing equity positions for refinancing.

Leveraging First-Time Buyer Programs and Benefits

Even at renewal, Toronto first-time buyers may have access to programs and benefits that can ease the transition or provide refinancing advantages.

Available programs and benefits:

🎁 First Home Savings Account (FHSA): While primarily for initial purchases, understanding FHSA mechanics can help buyers advise friends and family or plan for future property purchases

🎁 Home Buyers’ Plan (HBP) repayment: First-time buyers who used RRSP funds for their down payment must make annual HBP repayments; understanding RRSP and HBP rules helps coordinate these obligations with mortgage payments

🎁 First-Time Home Buyer Tax Credit: Understanding available tax credits can provide modest financial relief during renewal years

🎁 Energy efficiency programs: Toronto and federal programs offering grants for energy-efficient home improvements can be coordinated with refinancing to access equity for qualifying upgrades

Income Documentation for Self-Employed First-Time Buyers

Toronto’s entrepreneurial economy means many first-time buyers are self-employed or have variable income. These borrowers face unique challenges when demonstrating income for renewal qualification.

Self-employed renewal strategies:

📊 Two-year income averaging: Most lenders require two years of tax returns and average income across both years, meaning a strong recent year can offset a weaker previous year

📊 Add-backs and adjustments: Self-employed borrowers can add back certain business expenses (depreciation, home office, vehicle expenses) to increase qualifying income

📊 Alternative documentation: Some lenders accept bank statement programs or other alternative income verification methods for self-employed borrowers

📊 Timing tax planning: Working with accountants to optimize the timing of income recognition and expense deductions around renewal years

Self-employed Toronto first-time buyers should consult with both mortgage professionals and accountants well in advance of renewal to optimize income documentation. Those in specific professions may benefit from understanding specialized programs for doctors or IT consultants.

Looking Beyond 2026: Long-Term Mortgage Strategy

Building Equity Faster Through Prepayments

While managing the immediate challenge of how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto is critical, successful homeowners also develop long-term strategies to build equity and reduce mortgage costs.

Prepayment strategies:

💰 Annual lump-sum payments: Using tax refunds, bonuses, or other windfalls to make annual lump-sum payments within your prepayment privilege limits (typically 10-20% of original principal)

💰 Payment increases: Increasing regular payments by the maximum allowed percentage (typically 10-20% annually) when income grows

💰 Accelerated payment frequencies: Switching from monthly to bi-weekly or weekly payments results in one extra monthly payment per year, reducing amortization by several years

💰 Rounding up payments: Rounding payments up to the nearest $100 or $500 creates automatic prepayments that compound over time

For a $500,000 mortgage at 5% with 25-year amortization, making an additional $5,000 annual lump-sum payment saves approximately $85,000 in interest and reduces the amortization by 7 years.

Planning for Future Renewals

The 2026 renewal is just one point in a long-term mortgage journey. Strategic first-time buyers plan ahead for subsequent renewals to optimize their overall mortgage costs.

Long-term renewal planning:

🔮 Staggered term strategy: Consider mixing term lengths (e.g., splitting the mortgage between a 3-year and 5-year term) to create renewal flexibility and reduce interest rate risk

🔮 Rate environment monitoring: Stay informed about economic trends and interest rate forecasts to time term selections strategically

🔮 Relationship building: Develop relationships with multiple lenders and mortgage professionals to ensure competitive options at each renewal

🔮 Financial discipline: Maintain strong credit, manageable debt levels, and stable income documentation to maximize negotiating power at future renewals

🔮 Equity tracking: Monitor property values and mortgage paydown to understand your equity position and refinancing options

Balancing Mortgage Paydown with Other Financial Goals

Toronto first-time buyers must balance aggressive mortgage paydown with other important financial objectives, including retirement savings, emergency funds, and quality of life.

Balanced financial approach:

⚖️ Emergency fund priority: Maintain 3-6 months of expenses in accessible savings before aggressive mortgage prepayments

⚖️ Employer RRSP matching: Maximize employer-matched retirement contributions before extra mortgage payments (employer matches provide guaranteed returns exceeding mortgage interest savings)

⚖️ TFSA contributions: Tax-free investment growth in TFSAs can provide flexibility and returns that justify moderate mortgage paydown rather than maximum acceleration

⚖️ Quality of life balance: Excessive financial restriction to accelerate mortgage paydown can reduce quality of life and isn’t always optimal

⚖️ Interest rate consideration: When mortgage rates are low (3% or less), investing surplus funds often provides better long-term returns than prepayments; when rates are high (5%+), prepayments provide guaranteed returns exceeding most conservative investments

Understanding how to balance mortgage and retirement savings helps first-time buyers make informed allocation decisions.

Conclusion: Taking Control of Your 2026 Mortgage Renewal

Understanding how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto empowers you to transform a potentially stressful financial event into an opportunity for improved terms, better cash flow, and long-term savings. With 1.15 million Canadians renewing mortgages this year and payment increases averaging 15-20% for fixed-rate holders, the stakes are significant—but so are the opportunities for those who approach renewal strategically.[1][3]

The key insights for Toronto first-time buyers facing 2026 renewals include:

✨ Shop around aggressively to avoid the $1,860 annual loyalty tax paid by borrowers who passively accept their lender’s first offer

✨ Consider amortization extension as a powerful tool to manage payment shock, potentially eliminating increases for half of affected borrowers

✨ Leverage Toronto equity growth through refinancing or HELOCs to consolidate debt, manage cash flow, or fund value-adding improvements

✨ Work with mortgage professionals who can access multiple lenders, negotiate competitive terms, and navigate complex qualification scenarios

✨ Start early (120 days before renewal) to maximize options and avoid time-pressure decisions

Your Next Steps

Don’t wait until your renewal notice arrives to start planning. Take action today:

- Review your current mortgage details and note your renewal date

- Assess your current financial situation including income, debts, and credit score

- Obtain a current property valuation to understand your equity position

- Consult with a mortgage professional to explore your options and develop a renewal strategy

- Create a timeline with specific action items at 120, 90, 60, and 30 days before renewal

- Educate yourself about mortgage products, features, and negotiation strategies

- Build your professional team including mortgage brokers, accountants, and legal advisors

The 2026 mortgage renewal wave represents both a challenge and an opportunity. First-time buyers in Toronto who approach renewal with knowledge, preparation, and professional support can navigate payment increases, optimize their mortgage terms, and build long-term financial security. The difference between passive acceptance and strategic renewal can mean thousands of dollars in annual savings and significantly improved financial flexibility.

Take control of your mortgage renewal today—your future financial self will thank you.

References

[1] Mortgage Renewal 2026 Loyalty Tax – https://tullymortgages.ca/mortgage-renewal-2026-loyalty-tax/

[3] Staff Analytical Note 2025 21 – https://www.bankofcanada.ca/2025/07/staff-analytical-note-2025-21/

[4] Mortgage Renewal Canada – https://www.fairstone.ca/en/learn/finance-101/mortgage-renewal-canada