February 5, 2026

Current Best Self-Employed Mortgage Rates in Toronto: 5-Year Fixed vs Variable in February 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

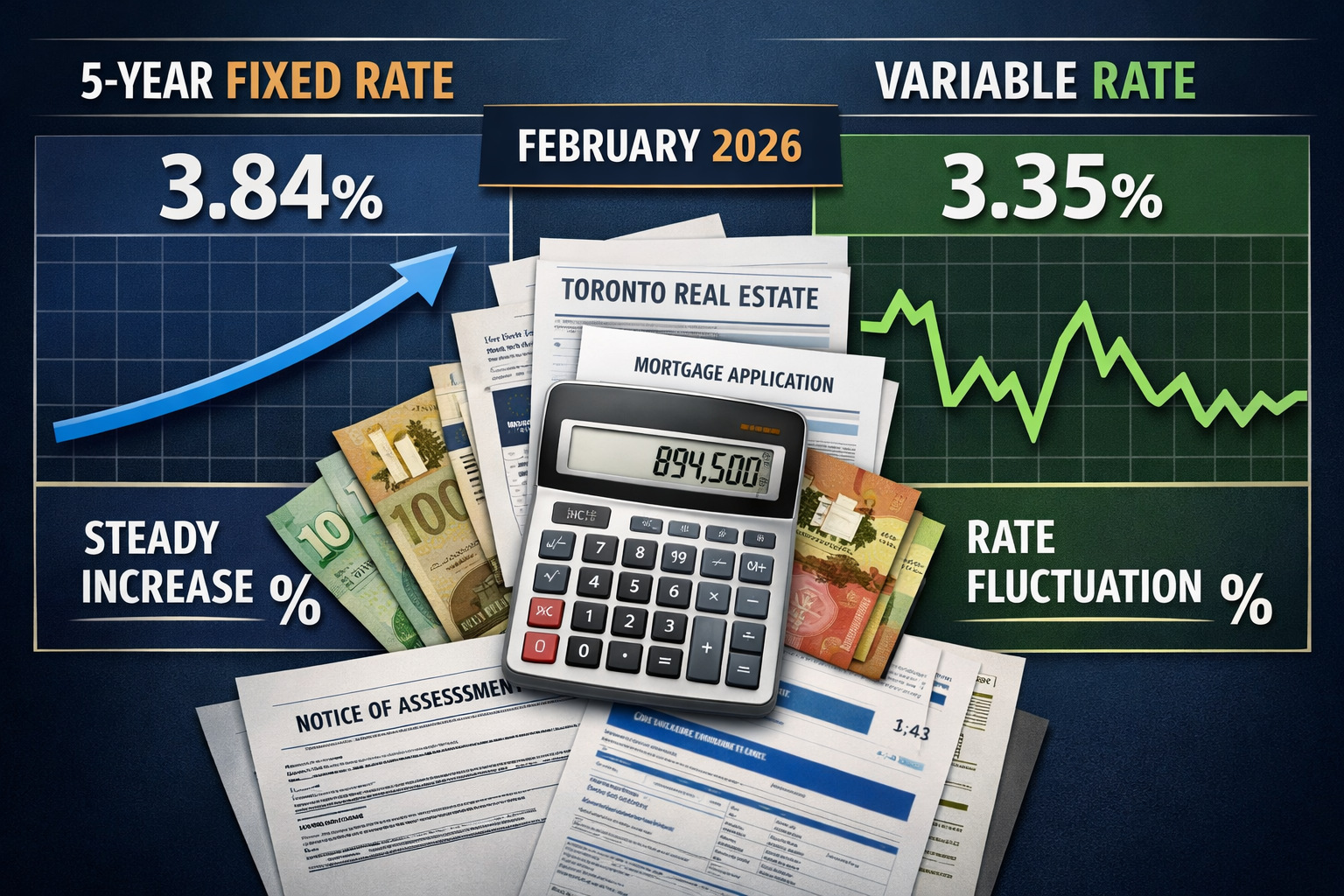

For self-employed professionals, freelancers, and business owners in Toronto, securing a competitive mortgage rate can feel like navigating a maze. Unlike traditional employees with steady T4 income, self-employed borrowers face unique challenges when proving their income to lenders. However, February 2026 brings excellent news: mortgage rates have dropped significantly, with the best 5-year variable rates sitting at 3.35% and fixed rates at 3.84% nationally[4]. Understanding the current best self-employed mortgage rates in Toronto for 5-year fixed versus variable options can save thousands of dollars over the life of your mortgage.

This comprehensive guide breaks down everything Toronto’s self-employed community needs to know about accessing these competitive rates, navigating income verification requirements, and choosing between fixed and variable mortgage products in February 2026.

Key Takeaways

✅ Best rates for self-employed borrowers: 5-year fixed rates range from 3.84% to 3.91%, while variable rates hover around 3.35% to 3.95%, depending on your lender and loan-to-value ratio[1][4]

✅ Income verification is key: Lenders accepting Notice of Assessments (NOAs) and T1 General tax returns offer the most competitive rates for self-employed Torontonians

✅ Fixed vs. variable spread: The difference between fixed and variable rates for self-employed borrowers is minimal in February 2026, at just 0.06 to 0.10 percentage points[1]

✅ Alternative lenders provide flexibility: B-lenders and online mortgage providers often offer easier qualification paths for self-employed borrowers compared to traditional banks

✅ Rate discounts are substantial: The best available rates represent savings of over 1.39 percentage points compared to posted bank rates[10]

Understanding Self-Employed Mortgage Rates in Toronto for February 2026

The mortgage landscape for self-employed borrowers has evolved considerably in recent years. Traditional lenders have become more accommodating, while alternative lending options have expanded dramatically. In February 2026, Toronto’s self-employed professionals have access to rates that rival—and sometimes beat—those available to traditionally employed borrowers.

Current Rate Snapshot

According to the latest data, self-employed borrowers can access 5-year fixed rates starting at 3.89% for 80% loan-to-value (LTV) mortgages, with rates climbing slightly to 3.91% for lower LTV ratios[1]. Meanwhile, variable rates for self-employed applicants sit at approximately 3.95% across all LTV categories[1].

These rates compare favorably to the Bank of Canada’s official posted 5-year conventional mortgage rate of 6.09%[8], demonstrating the significant discounts available through brokers and online lenders. For context, the national average 5-year fixed conventional rate stands at 4.70%[10], meaning self-employed borrowers working with the right lenders can secure rates below the national average.

Why Self-Employed Rates Differ

Self-employed mortgage rates traditionally carried a premium due to perceived higher risk. Lenders viewed fluctuating income and business expenses as red flags. However, in 2026, this gap has narrowed considerably. The difference between rates for self-employed versus traditionally employed borrowers has shrunk to as little as 0.05 to 0.15 percentage points with many A-lenders.

Factors affecting self-employed mortgage rates include:

- Income verification method (traditional NOAs vs. stated income)

- Years in business (typically 2+ years required)

- Credit score (680+ opens the best rates)

- Down payment size (20%+ avoids insurance premiums)

- Business structure (incorporated vs. sole proprietor)

For those seeking guidance on obtaining a mortgage when you’re self-employed, understanding these factors is crucial to securing competitive rates.

Breaking Down the Best 5-Year Fixed vs Variable Rates for Self-Employed Borrowers

Choosing between fixed and variable mortgage rates represents one of the most significant financial decisions for self-employed Toronto homebuyers. In February 2026, the choice is particularly nuanced given the narrow spread between the two options.

5-Year Fixed Rates: Stability and Predictability

Best available 5-year fixed rate nationally: 3.84%[4]

Fixed-rate mortgages lock in your interest rate for the entire term, providing payment certainty regardless of Bank of Canada policy changes. For self-employed borrowers specifically, rates vary by lender category:

| Lender Type | 5-Year Fixed Rate | LTV Requirement | Income Verification |

|---|---|---|---|

| Online/Broker Lenders | 3.84% – 3.89% | 80% | Full NOA documentation |

| Major Banks (Insured) | 4.21% – 4.32% | 95% | Traditional verification |

| Major Banks (Uninsured) | 4.56% – 4.62% | 80% | Traditional verification |

| B-Lenders | 4.89% – 5.25% | 65% – 80% | Flexible documentation |

The 3.89% rate for self-employed borrowers at 80% LTV[1] represents exceptional value, sitting just 0.05 percentage points above the absolute best national rate. This minimal premium reflects lenders’ growing comfort with self-employed income when properly documented.

5-Year Variable Rates: Flexibility and Potential Savings

Best available 5-year variable rate nationally: 3.35%[4]

Variable-rate mortgages fluctuate with the lender’s prime rate, which moves in response to Bank of Canada policy decisions. For self-employed borrowers, variable rates present an interesting opportunity:

- Standard self-employed variable rate: 3.95%[1]

- Best broker/online variable rates: 3.35% – 3.40%[2][4]

- Major bank variable rates: 4.15% – 4.45%

The spread between the best variable rates (3.35%) and self-employed-specific rates (3.95%) highlights the importance of shopping around. Self-employed borrowers who can provide comprehensive income documentation through mortgages for self-employed borrowers programs may qualify for the lowest available rates.

The Fixed vs. Variable Decision Matrix

In February 2026, the decision between fixed and variable carries unique considerations:

Choose Fixed (3.84% – 3.89%) if you:

- 🏠 Prioritize budget certainty for business planning

- 📊 Believe rates will rise over the next 5 years

- 💼 Have irregular income that makes payment predictability valuable

- 🔒 Prefer the peace of mind of knowing your exact payment

Choose Variable (3.35% – 3.95%) if you:

- 📉 Expect Bank of Canada to continue cutting rates

- 💰 Want to maximize potential savings (0.49 – 0.54 percentage points lower)

- 🔄 Value flexibility to convert to fixed later

- 📈 Can absorb potential payment increases

For insights into rate trends, reviewing the variable interest rates landscape helps inform this critical decision.

Income Verification Requirements: How Toronto Self-Employed Borrowers Qualify

The key to accessing the current best self-employed mortgage rates in Toronto for 5-year fixed vs variable options in February 2026 lies in understanding and meeting income verification requirements. Different lenders accept different documentation, and knowing which path you qualify for determines your rate options.

Traditional A-Lender Documentation (Best Rates: 3.84% – 3.95%)

Traditional lenders—including major banks and prime mortgage insurers—offer the best rates but require comprehensive documentation:

Required Documents:

- Two years of Notice of Assessments (NOAs) from Canada Revenue Agency

- Complete T1 General tax returns for the past two years

- Business financial statements (if incorporated)

- Proof of business existence (business license, articles of incorporation)

- Year-to-date income verification (recent bank statements, invoices)

Income Calculation Method: Most A-lenders average your net income plus add-backs (depreciation, CCA, business-use-of-home) over two years. Some lenders use a two-year declining average, giving more weight to recent income.

Example Calculation:

- Year 1 Net Income: $85,000

- Year 2 Net Income: $95,000

- Add-backs (depreciation): $8,000 per year

- Qualifying Income: $93,000 (two-year average)

This traditional approach works well for established self-employed professionals with consistent, well-documented income. Those exploring easier qualification for self-employed borrowers options may find alternative paths more suitable.

Alternative B-Lender Programs (Rates: 4.89% – 5.75%)

B-lenders specialize in serving borrowers who don’t fit traditional lending criteria. They offer greater flexibility in exchange for slightly higher rates:

Flexible Documentation Options:

- ✅ Stated income programs (income declaration with minimal verification)

- ✅ Single-year NOA acceptance (for newer businesses)

- ✅ Business-for-self (BFS) programs requiring only proof of business ownership

- ✅ Bank statement programs (6-12 months of business deposits)

Typical Requirements:

- Minimum 20% down payment (80% LTV)

- Credit score 600+ (650+ for best B-lender rates)

- Proof of business existence (1+ years)

- Reasonable debt service ratios

B-lenders provide crucial access for self-employed borrowers who:

- Have been in business less than 2 years

- Write off significant business expenses, reducing net income

- Have complex corporate structures

- Need faster approval timelines

For more information on alternative lending, explore B-lender mortgage rates in Toronto.

Online Lenders and Mortgage Brokers (Best Rates: 3.35% – 4.25%)

The rise of online mortgage lenders and broker networks has revolutionized access to competitive rates for self-employed borrowers. These platforms often match or beat traditional bank rates while offering:

Advantages:

- 🚀 Streamlined digital applications with faster approvals

- 💻 Automated income verification using CRA data integration

- 🔍 Rate comparison across 30+ lenders simultaneously

- 📱 Transparent pricing with no hidden fees

Documentation Typically Required:

- Authorization to access CRA tax information directly

- Two years of NOAs (pulled electronically)

- Business registration confirmation

- Credit bureau authorization

Many online lenders specialize in self-employed mortgages and have developed sophisticated algorithms to assess income stability beyond simple averaging. This technology-driven approach often results in higher qualifying amounts and better rates than traditional manual underwriting.

Using a best mortgage rates calculator can help compare total costs across different lender types and rate options.

Step-by-Step Comparison: Finding Your Best Rate as a Toronto Freelancer or Business Owner

Navigating the mortgage market as a self-employed Toronto resident requires a strategic approach. Follow this comprehensive roadmap to secure the current best self-employed mortgage rates in Toronto for 5-year fixed vs variable options in February 2026.

Step 1: Assess Your Documentation Readiness

Before approaching lenders, evaluate which qualification path suits your situation:

✅ Full Documentation Path (Access to 3.84% – 3.95% rates):

- 2+ years of filed tax returns with NOAs

- Consistent or growing income trend

- Clean credit history (680+ score)

- Minimal business debt

- 20%+ down payment available

✅ Alternative Documentation Path (Access to 4.89% – 5.50% rates):

- 1-2 years in business

- Significant write-offs reducing net income

- Strong revenue but lower reported income

- 20-35% down payment available

- Good credit (620+ score)

Pro Tip: If you’re between tax years, waiting for your latest NOA could qualify you for significantly better rates if it shows income growth.

Step 2: Calculate Your True Qualifying Income

Self-employed income calculation differs fundamentally from employed income:

Add-Back Items to Include:

- Depreciation and Capital Cost Allowance (CCA)

- Business-use-of-home expenses

- Vehicle expenses (business portion)

- Meals and entertainment (50% add-back)

- Professional development costs

- Home office expenses

Example for Toronto Freelance Designer:

- Reported Net Income (Line 15000): $72,000

- CCA Add-back: $6,000

- Home office expenses: $4,800

- Vehicle expenses: $3,200

- Total Qualifying Income: $86,000

This $14,000 increase in qualifying income could mean the difference between approval and denial, or between a $500,000 and $580,000 purchase price.

Step 3: Compare Lender Categories and Rates

Create a comparison matrix for your specific situation:

| Lender Category | Best Rate | Your Likely Rate | Qualifying Income | Approval Time | Flexibility |

|---|---|---|---|---|---|

| Major Banks | 4.21% – 4.62% | 4.45% | $80,000 | 3-4 weeks | Low |

| Credit Unions | 4.15% – 4.55% | 4.35% | $85,000 | 2-3 weeks | Medium |

| Online Lenders | 3.84% – 4.10% | 3.95% | $86,000 | 1-2 weeks | High |

| Mortgage Brokers | 3.84% – 4.25% | 3.89% | $86,000 | 1-2 weeks | High |

| B-Lenders | 4.89% – 5.50% | 5.15% | $90,000 | 1 week | Very High |

Key Insight: Mortgage brokers access the same lenders as direct applications but can submit to multiple lenders simultaneously, increasing approval odds and rate competitiveness.

Step 4: Understand Total Cost Beyond Rate

The advertised rate tells only part of the story. Calculate true cost including:

Comparison Example: $600,000 Mortgage, 25-Year Amortization

| Rate Type | Rate | Monthly Payment | Total Interest (5 years) | Penalty to Break | Total Cost |

|---|---|---|---|---|---|

| Fixed 3.84% | 3.84% | $3,062 | $111,420 | $18,372 (IRD) | $111,420 |

| Fixed 3.89% | 3.89% | $3,075 | $112,500 | $18,450 (IRD) | $112,500 |

| Variable 3.35% | 3.35% | $2,956 | $100,860 | $3,540 (3 months) | $100,860 |

| Variable 3.95% | 3.95% | $3,083 | $113,940 | $4,625 (3 months) | $113,940 |

Savings with Best Variable vs. Self-Employed Fixed: $11,640 over 5 years ($194/month)

However, if rates increase by just 0.50% over the term, that advantage disappears. Understanding how mortgages work in Toronto helps contextualize these trade-offs.

Step 5: Optimize Your Application Timing

Strategic timing can significantly impact your rate and approval odds:

Best Times to Apply:

- 📅 After filing taxes when you have current-year NOA

- 📅 Early in the year before spring market competition

- 📅 After Bank of Canada announcements when lenders adjust rates

- 📅 Mid-week when underwriters are less backlogged

February 2026 Timing Advantage: Current rates reflect recent Bank of Canada cuts, and lenders are competing aggressively for spring market share. This creates optimal conditions for self-employed borrowers.

Step 6: Work with a Mortgage Broker Specializing in Self-Employed

The complexity of self-employed mortgages makes broker expertise invaluable:

Broker Advantages:

- 🎯 Access to 30+ lenders vs. 1 bank

- 📊 Knowledge of which lenders favor specific business types

- 💼 Pre-underwriting to identify issues before submission

- 🔧 Income presentation strategies to maximize qualifying amount

- ⚡ Faster approvals through established lender relationships

Cost: Most mortgage brokers are paid by lenders, costing borrowers nothing while providing access to better rates than direct bank applications.

Step 7: Lock Your Rate and Prepare for Closing

Once approved, understand rate hold options:

- Rate holds: Typically 90-120 days at no cost

- Rate drops: If rates fall before closing, most lenders honor lower rates

- Conversion options: Variable mortgages can usually convert to fixed anytime

- Portability: Ability to transfer mortgage to new property

Final Documentation for Closing:

- Updated business license

- Recent bank statements (30-60 days)

- Proof of down payment source

- Home insurance quote

- Legal representation confirmation

Strategic Considerations for Self-Employed Toronto Homebuyers in 2026

Beyond simply securing the lowest rate, self-employed borrowers must consider broader strategic factors when choosing between fixed and variable mortgages in Toronto’s dynamic market.

Economic Outlook and Rate Forecasts

Understanding where rates are headed helps inform the fixed vs. variable decision:

Current Economic Indicators (February 2026):

- Bank of Canada policy rate trends suggest continued stability

- Inflation has moderated to target range

- Employment remains strong despite economic uncertainty

- Housing market showing seasonal spring activity

Rate Forecast Considerations: Most economists project rates to remain relatively stable through 2026-2027, with potential for modest decreases if economic growth slows[5][9]. This environment favors variable-rate mortgages for borrowers comfortable with some uncertainty.

However, self-employed borrowers should consider their business cycle sensitivity. If your income fluctuates with economic conditions, the payment certainty of a fixed rate may outweigh potential variable-rate savings.

Tax Planning Integration

Self-employed mortgage decisions should align with tax strategy:

Deductibility Considerations:

- Rental properties: Mortgage interest is tax-deductible

- Home office: Portion may be deductible for incorporated businesses

- Investment properties: Variable rates offer flexibility for refinancing

Income Timing: If you’re planning to incorporate or restructure your business, consider how this affects mortgage qualification. Incorporation can complicate income verification but may increase qualifying income through dividend gross-up calculations.

Renewal Planning for Existing Self-Employed Borrowers

If you’re approaching renewal with an existing mortgage, February 2026 presents exceptional opportunities:

Renewal Rate Comparison:

- Existing rate (from 2021): Likely 2.49% – 3.09% (5-year fixed)

- Current renewal offers: 4.25% – 4.75% (standard bank renewal)

- Best available rates: 3.84% – 3.89% (through shopping around)

Renewal Strategy:

- Request renewal offer 120 days before maturity

- Shop competing rates through broker

- Negotiate with existing lender using competing offers

- Consider switching lenders for better rate (no re-qualification if staying at same balance)

Important: If your income has decreased since original approval, staying with your existing lender avoids re-qualification. However, if income is stable or increased, shopping for the best rate makes financial sense.

Property Type and Location Factors in Toronto

Different Toronto neighborhoods and property types affect lending:

Preferred Property Types (Best Rates):

- ✅ Detached homes in established neighborhoods

- ✅ Semi-detached and townhomes in core areas

- ✅ Condos in buildings with strong reserve funds

- ✅ Properties under $2 million

Properties Requiring Alternative Lending:

- ⚠️ Condos in buildings with special assessments

- ⚠️ Properties over $2 million (require jumbo financing)

- ⚠️ Rural properties or those on large acreage

- ⚠️ Properties requiring immediate renovation

Toronto-Specific Considerations:

- Downtown condos may require 25-30% down with some lenders

- Properties in emerging neighborhoods (Scarborough, Etobicoke) may qualify for better LTV ratios

- Proximity to transit affects property valuation and lending terms

Building Long-Term Lender Relationships

For self-employed borrowers, establishing strong banking relationships provides future benefits:

Relationship Banking Advantages:

- 💳 Better credit card terms for business expenses

- 🏦 Business line of credit at preferential rates

- 📈 Investment services integration

- 🤝 Dedicated relationship manager for future needs

Strategy: Even if you secure your best mortgage rate through a broker and online lender, maintain a business banking relationship with a major bank for complementary services.

Stress Testing and Financial Resilience

Self-employed borrowers must pass the mortgage stress test, currently requiring qualification at the greater of your contract rate plus 2% or 5.25%[8].

Stress Test Example:

- Contract rate: 3.89%

- Stress test rate: 5.89% (contract + 2%)

- $600,000 mortgage qualification requires income to support payments at 5.89%

Building Resilience:

- 🛡️ Maintain 6-12 months emergency fund

- 📊 Diversify income streams where possible

- 💰 Make extra payments when cash flow permits

- 🔄 Review and optimize mortgage annually

Understanding these strategic factors ensures your mortgage choice supports both immediate affordability and long-term financial health.

Conclusion: Securing Your Best Self-Employed Mortgage Rate in Toronto

The current best self-employed mortgage rates in Toronto for 5-year fixed vs variable options in February 2026 represent exceptional value for freelancers, contractors, and business owners. With fixed rates as low as 3.84% to 3.89% and variable rates starting at 3.35%, self-employed borrowers can access financing that rivals or beats rates available to traditionally employed individuals.

The key to unlocking these competitive rates lies in thorough preparation, comprehensive documentation, and strategic lender selection. By understanding how lenders evaluate self-employed income, optimizing your tax returns for mortgage qualification, and working with specialists who understand the nuances of self-employed lending, you can secure financing that supports your homeownership goals.

Your Action Plan

Immediate Steps (This Week):

- ✅ Gather your last two years of NOAs and T1 General tax returns

- ✅ Calculate your qualifying income including add-backs

- ✅ Check your credit score and address any issues

- ✅ Use a mortgage rates calculator to estimate your budget

Short-Term Steps (This Month):

- 📞 Consult with a mortgage broker specializing in self-employed lending

- 📋 Pre-qualify with multiple lender types to compare options

- 🏠 Determine whether fixed or variable aligns with your risk tolerance

- 💼 Organize business documentation and financial statements

Long-Term Strategy:

- 📈 Optimize your tax filing strategy for future mortgage qualification

- 💰 Build down payment savings to access best rates (20%+ down)

- 🔄 Review mortgage options annually as your business grows

- 🎯 Work toward qualifying for A-lender rates if currently using alternatives

Fixed vs. Variable: Making Your Final Decision

For most self-employed Toronto borrowers in February 2026, the choice between fixed and variable depends on three factors:

Choose Fixed (3.84% – 3.89%) if:

- Your business income fluctuates seasonally or cyclically

- You prioritize budget certainty for financial planning

- You believe rates will rise over the next 3-5 years

- The 0.49 percentage point premium is worth peace of mind

Choose Variable (3.35% – 3.95%) if:

- You have stable, predictable self-employed income

- You can absorb potential payment increases

- You believe rates will remain stable or decrease

- You value flexibility and potential savings

Both options offer compelling value at current rates. The “right” choice depends on your unique financial situation, risk tolerance, and business outlook.

The Bottom Line

Self-employed mortgage qualification in Toronto has never been more accessible or affordable. With rates near historic lows and lenders increasingly comfortable with diverse income types, February 2026 presents an ideal window for self-employed professionals to enter or upgrade in the Toronto housing market.

By approaching the process strategically, documenting your income comprehensively, and working with experienced professionals who understand self-employed lending, you can secure competitive financing that supports your homeownership dreams while maintaining the flexibility your business requires.

The mortgage landscape continues to evolve, with new products and lenders entering the market regularly. Staying informed about mortgages for self-employed borrowers and monitoring rate trends ensures you’re positioned to take advantage of opportunities as they arise.

Whether you choose the stability of a 5-year fixed rate at 3.84% or the potential savings of a variable rate at 3.35%, the key is making an informed decision based on comprehensive information, professional guidance, and a clear understanding of your financial goals. Your path to Toronto homeownership as a self-employed professional starts with that first step—and February 2026 offers an exceptional foundation for success.

References

[1] Self Employed – https://rates.ca/guides/mortgage/self-employed

[2] Current Mortgage Rates – https://www.nerdwallet.com/ca/p/best/mortgages/current-mortgage-rates

[4] Best Mortgage Rates – https://www.ratehub.ca/best-mortgage-rates

[5] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[8] Posted Interest Rates Offered By Chartered Banks – https://www.bankofcanada.ca/rates/banking-and-financial-statistics/posted-interest-rates-offered-by-chartered-banks/

[9] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast

[10] 5 Year – https://www.nesto.ca/mortgage-rates/fixed/5-year/