February 6, 2026

Best Bank Statement Loans for Self-Employed Borrowers in 2026: Top Lenders and Rates

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage landscape for self-employed professionals has transformed dramatically in 2026, with bank statement loans emerging as the go-to solution for entrepreneurs, freelancers, and business owners who struggle with traditional mortgage qualification. As non-QM (non-qualified mortgage) lenders expand their offerings and interest rates stabilize in the 6-6.5% range, more self-employed borrowers are discovering that the Best Bank Statement Loans for Self-Employed Borrowers in 2026: Top Lenders and Rates provide a viable path to homeownership without the burden of complex tax documentation.

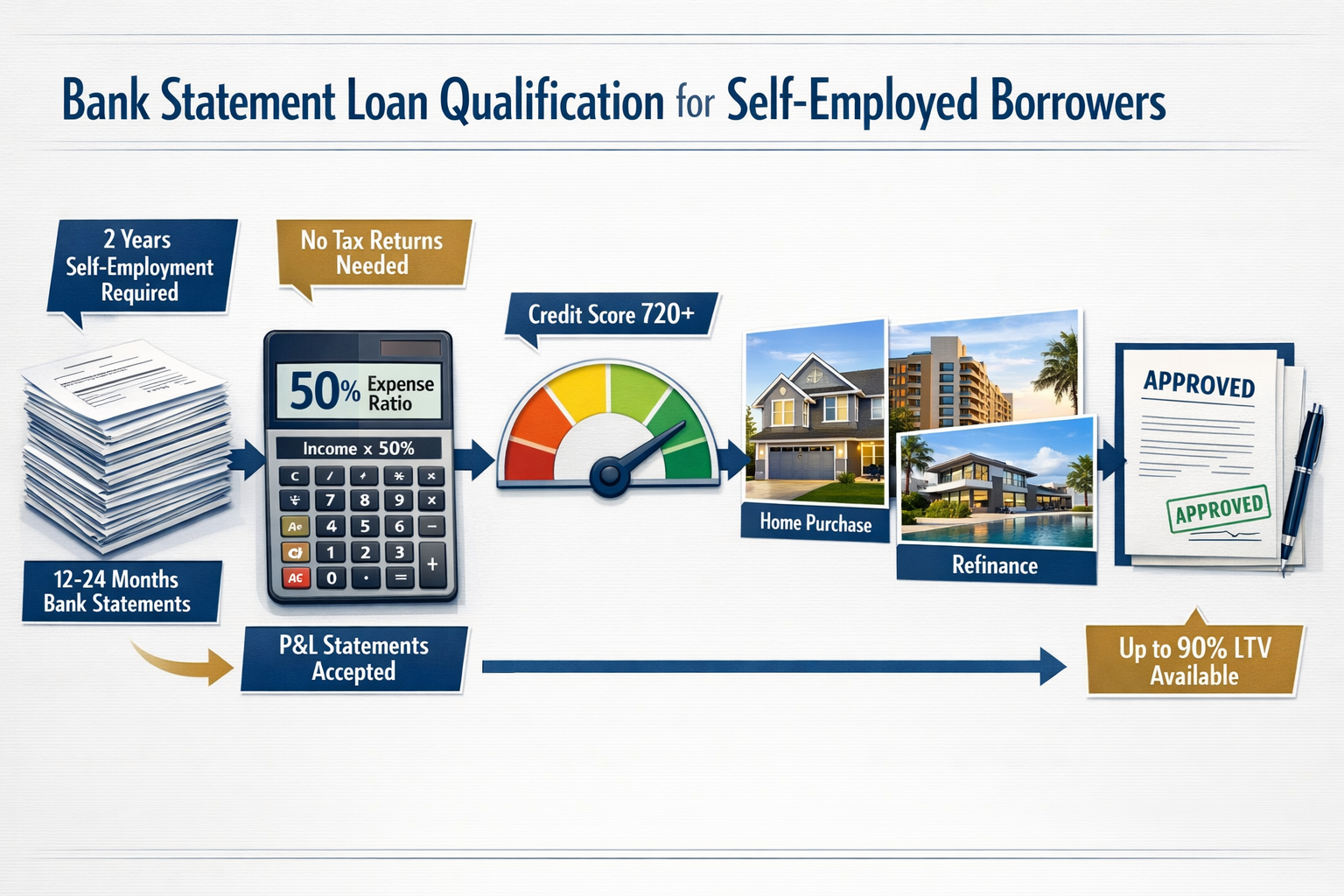

For years, self-employed individuals faced significant barriers when applying for mortgages. Traditional lenders required extensive tax returns, W-2 forms, and proof of consistent income—documents that often didn’t reflect the true earning potential of business owners who maximize deductions to minimize tax liability. In 2026, bank statement loans have surged in popularity as lenders recognize that 12-24 months of bank statements provide a more accurate picture of income for self-employed professionals.

Key Takeaways

- Bank statement loans require only 12-24 months of bank statements instead of tax returns, making them ideal for self-employed borrowers with significant business write-offs

- Interest rates in 2026 range from 6-6.5%, approximately 0.5-3% higher than conventional loans but increasingly competitive as the non-QM market expands

- Top lenders offer loan amounts up to $4 million with down payments as low as 10% and debt-to-income ratios up to 60% for qualified borrowers

- No PMI (Private Mortgage Insurance) is typically required, reducing monthly payment obligations compared to conventional high-LTV loans

- Minimum 2 years of self-employment is standard, though some lenders consider 1+ year with relevant industry experience

Understanding Bank Statement Loans: A Game-Changer for Self-Employed Borrowers

What Are Bank Statement Loans? 💼

Bank statement loans represent a specialized mortgage product designed specifically for self-employed individuals who cannot qualify through traditional income verification methods. Unlike conventional mortgages that rely heavily on tax returns and W-2 forms, these loans use personal or business bank statements as the primary documentation for income verification[2][4].

The fundamental principle is straightforward: lenders analyze deposits into your bank accounts over a 12-24 month period to calculate your average monthly income. This approach recognizes that many successful business owners show lower taxable income on their tax returns due to legitimate business deductions, even though their actual cash flow is substantial.

How Income Calculation Works

Lenders apply specific methodologies to determine qualifying income from bank statements:

Standard Expense Ratio Method: Most lenders use a default 50% expense factor, meaning they assume 50% of deposits represent business expenses and the remaining 50% counts as qualifying income[2]. For example, if your average monthly deposits total $20,000, your qualifying income would be $10,000.

Industry-Specific Adjustments: Some lenders apply higher expense ratios for certain industries. Restaurants and food service businesses might see a 70% expense ratio due to higher operating costs, while professional services might qualify for lower ratios[2].

Low Expense Ratio Programs: Innovative lenders like LendSure offer programs with expense ratios as low as 10%, significantly increasing qualifying income for borrowers with well-documented business operations[1].

Who Benefits Most from Bank Statement Loans?

Bank statement loans serve several categories of self-employed borrowers:

- Business owners who write off substantial expenses to reduce tax liability

- Freelancers and independent contractors with irregular income patterns

- Real estate investors seeking financing for investment properties

- Commission-based professionals with variable monthly earnings

- Entrepreneurs with less than 2 years of tax returns but strong cash flow

For self-employed professionals navigating the mortgage landscape, working with a best self-employed mortgage broker in Toronto can provide valuable guidance through the bank statement loan process.

Best Bank Statement Loans for Self-Employed Borrowers in 2026: Top Lenders Compared

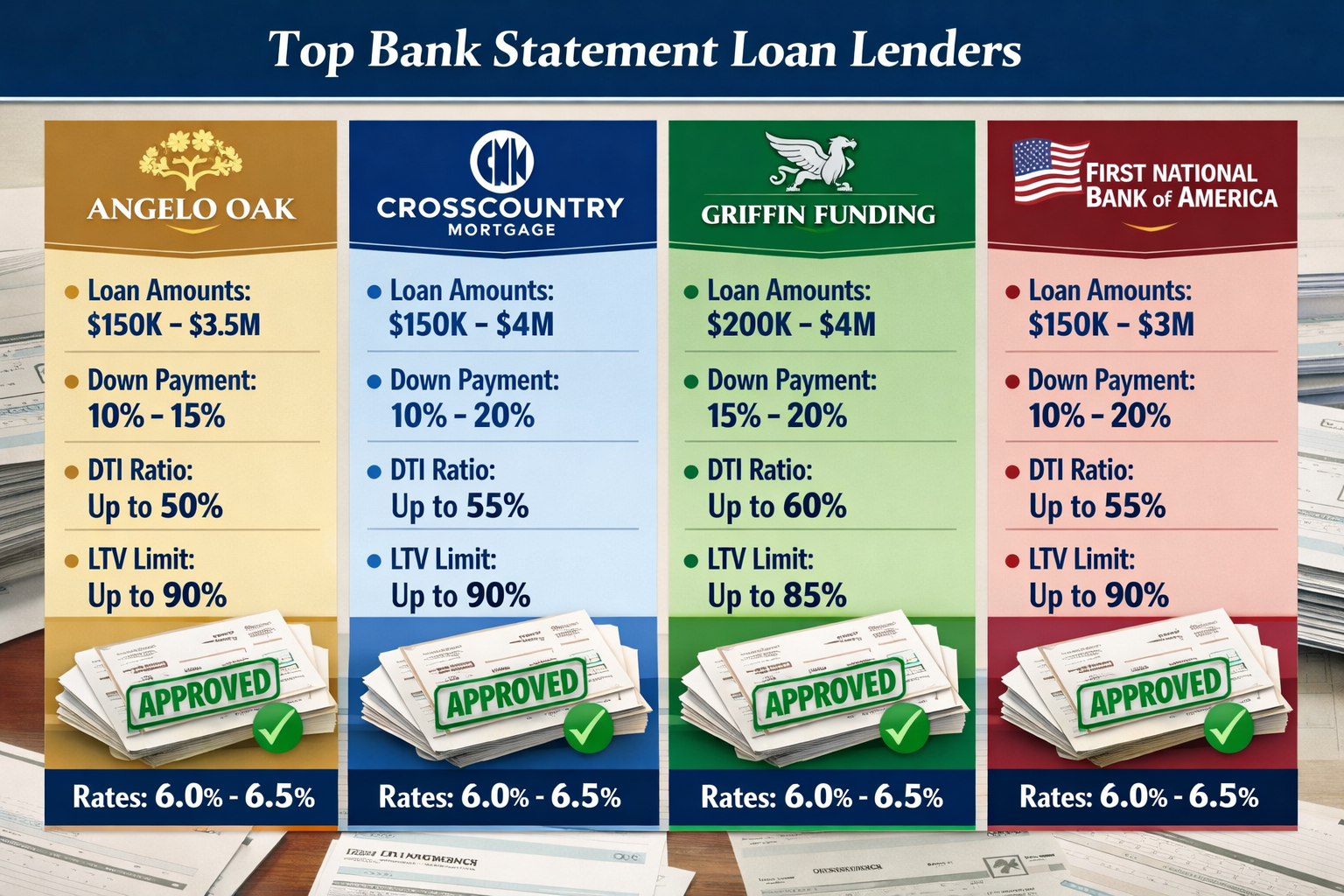

Angelo Oak Mortgage Services ⭐

Angelo Oak stands out as one of the most flexible bank statement loan providers in 2026, offering comprehensive programs tailored to diverse self-employment situations.

Key Features:

- Loan amounts: $150,000 to $4 million[2]

- Down payment: As low as 10% (90% LTV available)

- Business ownership: Borrowers can own as little as 25% of the business[2]

- Income verification: Accepts both personal and business bank statements

- P&L statements: Accepted as alternative documentation[2]

- Expense ratio: Default 50%, with industry-specific adjustments

Unique Advantages:

Angelo Oak’s willingness to work with minority business owners (those owning just 25% of a company) sets them apart from competitors. This flexibility makes them ideal for professionals in partnership arrangements or those with equity stakes in larger enterprises.

The lender also accepts Profit and Loss statements prepared by CPAs or tax professionals, providing an additional pathway for borrowers who maintain detailed financial records but prefer not to submit full tax returns[2].

CrossCountry Mortgage 🏆

CrossCountry Mortgage has built a reputation for accommodating borrowers with higher debt-to-income ratios and offering substantial loan amounts.

Key Features:

- Loan amounts: Up to $3 million[4]

- Down payment: As low as 10%

- DTI ratio: Up to 50% accepted[4]

- Property types: Owner-occupied, second homes, investment properties

- Special programs: Cash-out refinance options available

- PMI: No private mortgage insurance required[4]

Unique Advantages:

CrossCountry’s 50% DTI threshold is particularly valuable for borrowers with existing business debt or those purchasing higher-priced properties. The absence of PMI requirements, even with 10% down payments, can save borrowers hundreds of dollars monthly compared to conventional loans with similar LTV ratios[4].

The lender’s comprehensive property type acceptance makes them an excellent choice for self-employed individuals looking to expand their investment property portfolio.

Griffin Funding (Texas-Based) 🌟

Griffin Funding specializes in serving Texas markets with streamlined underwriting processes designed for busy entrepreneurs.

Key Features:

- Down payment: As low as 10%[6]

- Streamlined underwriting: Faster approval timelines

- Experience consideration: May accept 1+ year self-employment with relevant industry background[6]

- Regional expertise: Deep knowledge of Texas real estate markets

- Flexible documentation: Simplified bank statement review process

Unique Advantages:

Griffin Funding’s willingness to consider borrowers with less than 2 years of self-employment history—provided they have relevant industry experience—opens doors for recently transitioned professionals. For example, an IT consultant who worked in corporate IT for 10 years before launching their own practice might qualify after just 12-15 months of self-employment[6].

First National Bank of America 💪

First National Bank of America operates as a portfolio lender, meaning they hold loans in their own portfolio rather than selling them to secondary markets. This structure allows for exceptional flexibility.

Key Features:

- DTI ratio: Frequently approves ratios of 55-60%[5]

- Portfolio lending: Greater flexibility in underwriting decisions

- Unconventional income: Strong track record with complex income situations

- Write-off friendly: Particularly accommodating for borrowers with substantial deductions

- Relationship banking: Personalized service and decision-making

Unique Advantages:

The 55-60% DTI approval capability is industry-leading, making First National ideal for borrowers who might be rejected elsewhere due to debt ratios. Their portfolio lending model means underwriters have more discretion to consider the complete financial picture rather than adhering to rigid algorithmic requirements[5].

This lender excels with self-employed doctors and other high-income professionals who carry substantial student loan debt or business obligations.

Eligibility Requirements and Qualification Criteria for Bank Statement Loans

Minimum Self-Employment Duration ⏰

Most lenders require at least 2 years of continuous self-employment in the same industry or line of business[6]. This requirement ensures borrowers have established stable business operations and can demonstrate consistent income patterns.

Exceptions and Flexibility:

- Some lenders accept 1 year of self-employment if the borrower has extensive prior experience in the same field

- Industry transitions may require the full 2-year period

- Documented business growth can strengthen applications with shorter histories

Credit Score Requirements 📊

Bank statement loans typically require higher credit scores than conventional mortgages due to the perceived additional risk:

Minimum Scores:

- 620-640: Entry-level qualification with maximum down payment requirements

- 680-700: Access to better rates and more favorable terms

- 720+: Qualifies for maximum LTV ratios (up to 90%) and optimal pricing[1][2]

Borrowers with lower credit scores may still qualify but should expect higher interest rates and larger down payment requirements. Those working to improve their credit should review strategies for rapidly improving credit scores before applying.

Down Payment and LTV Ratios 💰

Bank statement loans offer competitive down payment options:

| Down Payment | Maximum LTV | Typical Credit Score Required |

|---|---|---|

| 10% | 90% | 720+ |

| 15% | 85% | 680-700 |

| 20% | 80% | 640-680 |

| 25%+ | 75% or lower | 620+ |

Important Considerations:

- Higher LTV ratios require stronger credit profiles

- Investment properties typically require larger down payments (20-25%)

- Cash-out refinances may have lower maximum LTV limits

- No PMI is required regardless of down payment amount[4]

Documentation Requirements 📄

While bank statement loans eliminate the need for tax returns, borrowers must still provide:

Essential Documents:

- ✅ 12-24 months of personal or business bank statements

- ✅ Valid government-issued ID

- ✅ Proof of business existence (business license, articles of incorporation)

- ✅ Credit authorization

- ✅ Property information (purchase contract or current mortgage statement)

Optional Documents:

- 📋 Profit and Loss statements (accepted by some lenders)[2]

- 📋 CPA letter verifying self-employment

- 📋 Client contracts or invoices demonstrating ongoing business

- 📋 Business bank account statements (if using personal statements)

Debt-to-Income Ratio Flexibility 📈

One of the most significant advantages of bank statement loans is the flexible DTI requirements:

Standard DTI Limits:

- 43%: Conventional mortgage maximum

- 50%: Common bank statement loan threshold[4]

- 55-60%: Available from specialized portfolio lenders[5]

DTI Calculation Method:

Lenders calculate DTI by dividing total monthly debt obligations by qualifying monthly income:

DTI = (Monthly Debt Payments) ÷ (Qualifying Monthly Income) × 100

For bank statement loans, the qualifying income is determined by applying the expense ratio to average monthly deposits, making it crucial to understand how your specific lender calculates this figure.

Interest Rates and Costs: What to Expect in 2026

Current Rate Environment 📉

The bank statement loan market in 2026 has matured significantly, with rates stabilizing in a competitive range as more lenders enter the non-QM space. Current market conditions show:

2026 Rate Ranges:

- Bank statement loans: 6.0-6.5% for well-qualified borrowers[3]

- Conventional mortgages: 5.5-6.0% (for comparison)

- Premium over conventional: 0.5-3.0 percentage points[3][8]

The rate premium reflects the additional risk lenders assume when using alternative documentation, but this gap has narrowed considerably as bank statement loans have proven to perform well and lenders have refined their underwriting models.

Factors Affecting Your Interest Rate 🎯

Several variables influence the specific rate you’ll receive:

Credit Score Impact:

- 760+: Qualify for lowest available rates

- 720-759: Slightly elevated rates (typically 0.25-0.5% higher)

- 680-719: Moderate rate increases (0.5-1.0% higher)

- 640-679: Higher rates (1.0-2.0% premium)

- Below 640: Maximum rates or potential denial

Loan-to-Value Ratio:

- 80% LTV or lower: Best pricing

- 80-85% LTV: Slight rate increase

- 85-90% LTV: Noticeable rate premium

Property Type:

- Primary residence: Lowest rates

- Second home: Moderate increase (0.25-0.5%)

- Investment property: Higher rates (0.5-1.5% premium)

Loan Amount:

- Jumbo loans (above conforming limits) may carry different pricing

- Very large loans ($2M+) might receive preferential rates from portfolio lenders

Closing Costs and Fees 💵

Bank statement loans typically involve similar closing costs to conventional mortgages, with some variations:

Standard Closing Costs:

- Origination fee: 0.5-1.5% of loan amount

- Appraisal: $500-$800

- Credit report: $50-100

- Title insurance: Varies by location and loan amount

- Attorney fees: $500-$1,500

- Recording fees: $100-500

Unique to Bank Statement Loans:

- Bank statement review fee: Some lenders charge $200-500 for detailed analysis

- CPA verification fee: If P&L statements require third-party verification

- Higher underwriting fees: May be $100-300 more than conventional loans

No PMI Benefit:

A significant cost advantage of bank statement loans is the absence of private mortgage insurance requirements, even with down payments below 20%[4]. For a $400,000 loan with 10% down, this could save $200-300 monthly compared to a conventional loan.

Understanding all costs involved helps borrowers make informed decisions. For comprehensive guidance on what to expect, review our closing cost calculator and guide.

Real Borrower Success Stories: Bank Statement Loans in Action

Case Study 1: Restaurant Owner Secures Dream Home 🍽️

Borrower Profile:

- Occupation: Restaurant owner (3 years in business)

- Tax return income: $45,000 (after substantial deductions)

- Actual bank deposits: $18,000 monthly average

- Credit score: 705

- Property: $550,000 primary residence

Challenge: Traditional lenders denied the application based on tax return income showing only $45,000 annually, insufficient for the desired purchase price.

Solution: Using a bank statement loan with a 70% expense ratio (appropriate for restaurant industry), the lender calculated qualifying income at $5,400 monthly ($18,000 × 30%), or $64,800 annually—a 44% increase over tax return income.

Outcome: Approved for a $440,000 loan (80% LTV) at 6.25% interest rate with a 20% down payment.

Case Study 2: Freelance Consultant Refinances for Better Terms 💻

Borrower Profile:

- Occupation: Marketing consultant (5 years self-employed)

- Bank statement income: $12,500 monthly average

- Credit score: 745

- Property: $425,000 home with existing mortgage

- Goal: Cash-out refinance to fund business expansion

Challenge: Needed to extract $75,000 in equity while maintaining affordable payments, but tax returns showed minimal income due to home office and equipment deductions.

Solution: Applied for a bank statement cash-out refinance using 24 months of business bank statements. With a 50% expense ratio, qualifying income calculated to $6,250 monthly.

Outcome: Approved for a $340,000 cash-out refinance (80% LTV), extracting $75,000 in cash at 6.1% interest rate. Monthly payment increased by only $425 while providing substantial business capital.

Case Study 3: Real Estate Investor Expands Portfolio 🏘️

Borrower Profile:

- Occupation: Real estate investor and property manager

- Properties owned: 4 rental properties

- Bank deposits: $22,000 monthly (including rental income)

- Credit score: 680

- Goal: Purchase 5th investment property

Challenge: Existing debt from four mortgages created a high DTI ratio (52%) that exceeded conventional lending limits.

Solution: Worked with First National Bank of America, which accepts DTI ratios up to 60% for qualified borrowers. Bank statement analysis showed consistent income over 24 months.

Outcome: Approved for a $375,000 investment property loan (75% LTV) at 6.75% interest rate with 25% down payment, despite the 52% DTI ratio.

These success stories demonstrate how bank statement loans create opportunities for self-employed borrowers who would otherwise face rejection from traditional lenders. For professionals in specialized fields, such as those seeking private loan lenders in Ontario, understanding alternative financing options is crucial.

Comparing Bank Statement Loans to Alternative Self-Employed Financing Options

Bank Statement Loans vs. Traditional Mortgages 🔄

| Feature | Bank Statement Loan | Traditional Mortgage |

|---|---|---|

| Income verification | 12-24 months bank statements | Tax returns, W-2s, pay stubs |

| Interest rates | 6.0-6.5% (2026) | 5.5-6.0% (2026) |

| DTI limits | Up to 50-60% | Typically 43% maximum |

| Self-employment duration | 2 years (sometimes 1+) | 2 years minimum |

| PMI requirement | None | Required if LTV > 80% |

| Approval timeline | 2-4 weeks | 3-6 weeks |

| Best for | High write-offs, variable income | Stable documented income |

Bank Statement Loans vs. Stated Income Loans 📝

Stated income loans (also called “no-doc” loans) were popular before the 2008 financial crisis but are now extremely rare and heavily regulated.

Key Differences:

- Documentation: Bank statement loans require substantial documentation (bank statements); stated income loans require minimal proof

- Availability: Bank statement loans widely available; stated income loans nearly extinct

- Risk: Bank statement loans carry moderate risk; stated income loans were considered high-risk

- Rates: Bank statement loans offer competitive rates; stated income loans (when available) carry significant premiums

Bank Statement Loans vs. Asset-Based Mortgages 💎

Asset-based mortgages qualify borrowers based on liquid assets rather than income, making them suitable for retirees or individuals with substantial investment portfolios.

Comparison:

- Qualification method: Bank statement loans use cash flow; asset-based loans use asset depletion calculations

- Best candidates: Bank statement loans suit active business owners; asset-based loans suit asset-rich, income-poor borrowers

- Rate competitiveness: Bank statement loans typically offer better rates

- Flexibility: Bank statement loans better for those with ongoing business income

Bank Statement Loans vs. Portfolio Loans 🏦

Portfolio loans are held by the originating lender rather than sold to secondary markets, allowing for flexible underwriting.

Relationship:

- Many bank statement loans ARE portfolio loans

- Portfolio lending enables the flexible DTI and documentation requirements

- Not all portfolio loans use bank statement methodology

- Portfolio lenders often offer the best terms for complex situations

For borrowers exploring various options, understanding B-lenders and alternative mortgage solutions can provide additional pathways to approval.

How to Apply for a Bank Statement Loan: Step-by-Step Process

Step 1: Assess Your Qualification 🔍

Before applying, evaluate your eligibility:

Self-Assessment Checklist:

- ✅ Have you been self-employed for at least 2 years?

- ✅ Is your credit score above 640 (ideally 680+)?

- ✅ Can you provide 12-24 months of bank statements?

- ✅ Do you have sufficient down payment (10-20%)?

- ✅ Are your bank deposits consistent and verifiable?

- ✅ Can you document your business existence?

Step 2: Organize Your Bank Statements 📊

Preparation Tips:

- Request official bank statements (not screenshots or printouts from online banking)

- Ensure statements show all pages including account numbers and bank logos

- Highlight or note any large unusual deposits that aren’t income (loans, transfers, etc.)

- Separate business and personal deposits if using personal accounts

- Calculate your average monthly deposits over the review period

- Document the source of irregular deposits (tax refunds, gifts, one-time sales)

Red Flags to Address:

- Frequent overdrafts or NSF fees

- Irregular deposit patterns

- Unexplained large deposits

- Negative balances

- Multiple bank account closures

Step 3: Choose the Right Lender 🎯

Based on your specific situation, select a lender that aligns with your needs:

Selection Criteria:

- Loan amount needed: Ensure lender offers your required range

- Property type: Verify lender accepts your property category

- DTI ratio: Choose lenders with appropriate flexibility

- Geographic location: Some lenders focus on specific regions

- Timeline: Consider approval and closing speed requirements

- Rate competitiveness: Compare offers from multiple lenders

Step 4: Submit Your Application 📤

Application Components:

- Complete loan application form

- Bank statements (12-24 months)

- Government-issued identification

- Business documentation (license, articles of incorporation)

- Property information (address, purchase contract, or current loan details)

- Authorization for credit check

- Explanation letters for any unusual circumstances

Step 5: Underwriting and Approval Process ⚖️

Timeline Expectations:

- Initial review: 2-5 business days

- Conditional approval: 7-14 days

- Final approval: 14-21 days

- Closing: 21-30 days from application

Common Conditions:

- Updated bank statements (if process extends beyond statement dates)

- Verification of business existence

- Explanation of specific deposits or withdrawals

- Additional documentation for debt obligations

- Property appraisal completion

- Proof of insurance

- Final verification of employment/business status

Step 6: Closing and Funding 🎉

Once final approval is granted:

Closing Process:

- Review closing disclosure (at least 3 days before closing)

- Conduct final walkthrough (for purchases)

- Attend closing appointment with required identification

- Sign loan documents

- Provide certified funds for down payment and closing costs

- Receive keys (for purchases) or loan proceeds (for refinances)

Working with experienced professionals throughout this process significantly increases success rates. Consider consulting with specialists who understand self-employed mortgage challenges to navigate potential obstacles.

Common Mistakes to Avoid When Applying for Bank Statement Loans

Mistake 1: Mixing Personal and Business Funds Inconsistently 🚫

The Problem: Irregular transfers between personal and business accounts create confusion in income calculation and may trigger additional documentation requests.

The Solution: Maintain clear, consistent patterns for at least 3-6 months before applying. If you must transfer funds, document the purpose and ensure the same deposits aren’t counted twice.

Mistake 2: Making Large Unusual Deposits Before Applying 💸

The Problem: Lenders scrutinize unusual deposits to prevent fraud and ensure income sustainability. Large one-time deposits may be excluded from income calculations or require extensive documentation.

The Solution: Avoid depositing gifts, loans, or one-time windfalls during the bank statement review period. If unavoidable, prepare detailed documentation explaining the source and non-income nature of the deposit.

Mistake 3: Applying with Insufficient Self-Employment History ⏱️

The Problem: Most lenders require 2 years of self-employment. Applying too early results in denial and a hard credit inquiry that may impact your score.

The Solution: Wait until you have at least 24 months of verifiable self-employment, or work with lenders like Griffin Funding that may accept 12-15 months with strong industry experience[6].

Mistake 4: Failing to Explain Income Fluctuations 📉

The Problem: Significant month-to-month variations in deposits raise concerns about income stability, potentially leading to denial or reduced qualifying income.

The Solution: Prepare a written explanation for seasonal businesses or industries with natural income cycles. Provide context showing the pattern is normal and sustainable.

Mistake 5: Overlooking Debt-to-Income Ratio Calculations 🧮

The Problem: Borrowers often underestimate their DTI ratio, leading to disappointment when they don’t qualify for their desired loan amount.

The Solution: Calculate your DTI before applying using the lender’s expense ratio methodology. Include all monthly debt obligations (car loans, student loans, credit cards, etc.) and compare to your qualifying income.

Mistake 6: Choosing the Wrong Property Type 🏠

The Problem: Not all lenders accept all property types. Investment properties, non-warrantable condos, and multi-unit properties may have restrictions.

The Solution: Verify your lender accepts your specific property type before investing time in the application. Some properties may require larger down payments or have different rate structures.

Mistake 7: Neglecting Credit Score Improvement 📈

The Problem: Applying with a borderline credit score (640-680) results in higher rates and less favorable terms.

The Solution: If time permits, spend 3-6 months improving your credit score before applying. Even a 20-40 point increase can significantly impact your rate and monthly payment.

Maximizing Your Chances of Approval: Expert Tips

Optimize Your Bank Statements 💡

3-6 Months Before Applying:

- Maintain consistent deposit patterns

- Avoid overdrafts and NSF fees

- Keep balances positive

- Minimize transfers between accounts

- Document all income sources clearly

Strategic Timing:

- Apply when your average monthly deposits are highest

- Consider waiting if recent months show lower-than-normal income

- Time applications to avoid seasonal low periods for your business

Strengthen Your Application Package 📋

Additional Documentation:

- Include a business overview letter explaining your industry, experience, and income sources

- Provide client contracts or ongoing agreements demonstrating future income

- Submit CPA-prepared P&L statements if available (accepted by some lenders)[2]

- Offer business growth documentation (expanding client base, new contracts, etc.)

Consider Co-Borrowers or Co-Signers 👥

Strategic Partnerships:

- Adding a spouse or partner with W-2 income can strengthen the application

- Co-signers with strong credit can improve terms

- Combined income may allow for higher loan amounts

- Ensure all parties understand their obligations and risks

Work with Specialized Mortgage Professionals 🤝

Benefits of Expert Guidance:

- Lender matching: Professionals know which lenders best suit specific situations

- Application optimization: Experts help present your financial picture most favorably

- Problem solving: Experienced brokers navigate obstacles and find creative solutions

- Rate shopping: Access to multiple lenders ensures competitive pricing

Connecting with knowledgeable professionals who specialize in self-employed financing can make the difference between approval and denial.

Prepare for Higher Interest Rates 💰

Financial Planning:

- Budget for 6-6.5% rates rather than conventional rates

- Calculate payments at slightly higher rates to ensure comfort with worst-case scenarios

- Consider larger down payments to reduce monthly obligations

- Plan for potential refinancing to conventional loans once tax returns show sufficient income

Build Reserves and Assets 🏦

Financial Cushion:

- Maintain 6-12 months of reserves in liquid accounts

- Demonstrate financial stability beyond qualifying income

- Keep business and personal finances healthy

- Avoid large purchases or new debt during the application process

The Future of Bank Statement Loans: Trends and Predictions for 2026 and Beyond

Expanding Lender Participation 📈

The bank statement loan market has grown significantly, with more lenders entering the space as performance data demonstrates these loans perform comparably to traditional mortgages when properly underwritten[7].

2026 Trends:

- Major banks beginning to offer bank statement programs alongside non-QM specialists

- Credit unions developing self-employed lending programs

- Technology platforms streamlining bank statement analysis and approval

- Increased competition driving rates closer to conventional mortgage pricing

Technology Integration and Automation 🤖

Digital Innovations:

- Automated bank statement analysis reducing processing time from weeks to days

- AI-powered income verification improving accuracy and consistency

- Digital document collection simplifying the application process

- Real-time underwriting decisions for well-qualified borrowers

Regulatory Developments 📜

Evolving Standards:

- Standardization of expense ratios across lenders and industries

- Enhanced consumer protections ensuring fair lending practices

- Clearer guidelines for acceptable documentation and verification methods

- Integration with QM standards as regulators recognize alternative documentation validity

Rate Compression 💵

As the market matures and competition increases, the premium over conventional rates continues to narrow:

Rate Evolution:

- 2020: 3-5% premium over conventional rates

- 2023: 2-3% premium over conventional rates

- 2026: 0.5-3% premium over conventional rates[3][8]

- Projected 2028: 0.5-2% premium as market fully matures

Expanded Product Offerings 🎁

New Options:

- Shorter bank statement periods (some lenders testing 6-month programs for exceptional borrowers)

- Hybrid documentation combining bank statements with other alternative income verification

- Specialized programs for specific industries (healthcare, technology, real estate)

- Investment property packages with multiple property financing

Understanding market trends helps borrowers time their applications strategically and anticipate future opportunities for refinancing or additional purchases.

Frequently Asked Questions About Bank Statement Loans

Can I use business bank statements instead of personal bank statements?

Yes, most lenders accept either personal or business bank statements, and some allow a combination of both[2][4]. Business bank statements may be preferable if all business income flows through business accounts, while personal statements work better for sole proprietors who deposit client payments directly to personal accounts.

What if I have multiple bank accounts?

Lenders typically analyze all accounts where business income is deposited. You’ll need to provide statements for each account, and the lender will calculate total average monthly deposits across all accounts while avoiding double-counting transfers between your own accounts.

How do lenders handle seasonal income fluctuations?

Lenders use 12-24 month averages specifically to smooth out seasonal variations. A written explanation of your industry’s seasonal patterns can help underwriters understand that fluctuations are normal and expected. Longer statement periods (24 months vs. 12 months) often benefit seasonal businesses.

Can I get a bank statement loan with recent late payments?

It depends on severity and recency. One or two late payments from 12+ months ago may not disqualify you, especially with strong compensating factors. However, recent late payments (within 6 months) or patterns of delinquency will likely result in denial or require waiting until the credit profile improves.

Are bank statement loans available for investment properties?

Yes, most bank statement loan programs accept investment properties, though they typically require:

- Larger down payments (20-25% minimum)

- Higher interest rates (0.5-1.5% premium over owner-occupied rates)

- Lower maximum LTV ratios (75-80% instead of 90%)

- Stronger credit scores (680-700 minimum)

How long does the approval process take?

Typical timeline: 21-30 days from application to closing, though some lenders offer expedited processing. The bank statement review adds 3-7 days compared to conventional loans, but the overall timeline remains competitive, especially compared to the delays self-employed borrowers often experience with traditional lenders.

Can I refinance from a bank statement loan to a conventional loan later?

Absolutely. Many borrowers use bank statement loans as a bridge solution, then refinance to conventional mortgages once their tax returns show sufficient income for traditional qualification. This strategy can reduce interest rates by 0.5-3% while maintaining the same property and loan amount.

What happens if my bank statements show declining income?

Declining trends raise red flags for underwriters. If your recent months show lower deposits than earlier periods, lenders may:

- Use the lower recent average rather than the full period average

- Request additional documentation explaining the decline

- Require a larger down payment to offset perceived risk

- Deny the application if the trend suggests business instability

Mitigation strategies include waiting until income stabilizes, providing contracts showing upcoming income, or offering larger down payments to strengthen the application.

Conclusion: Taking the Next Steps Toward Homeownership with Bank Statement Loans

The Best Bank Statement Loans for Self-Employed Borrowers in 2026: Top Lenders and Rates represent a powerful tool for entrepreneurs, freelancers, and business owners who have been historically underserved by traditional mortgage lending. With rates stabilizing in the 6-6.5% range and lenders expanding their programs to accommodate diverse self-employment situations, 2026 presents an excellent opportunity for self-employed professionals to achieve their homeownership goals.

Key Success Factors 🎯

To maximize your chances of approval:

- Ensure 2+ years of self-employment with consistent bank statement documentation

- Maintain credit scores of 680+ for optimal rates and terms

- Organize 12-24 months of clean bank statements with consistent deposit patterns

- Prepare 10-20% down payment depending on your credit profile and property type

- Calculate realistic DTI ratios using lender expense ratio methodologies

- Choose the right lender based on your specific situation and needs

Actionable Next Steps 📝

If you’re ready to pursue a bank statement loan:

Immediate Actions (This Week):

- ✅ Request 24 months of bank statements from all accounts with business deposits

- ✅ Check your credit score and review your credit report for errors

- ✅ Calculate your average monthly deposits and estimated qualifying income

- ✅ Determine your target property price and required loan amount

- ✅ Assess your down payment savings and timeline

Short-Term Actions (This Month):

- ✅ Research and contact 2-3 lenders from the top providers discussed

- ✅ Gather business documentation (licenses, incorporation papers, etc.)

- ✅ Prepare explanations for any unusual deposits or income fluctuations

- ✅ Review your debt obligations and calculate your DTI ratio

- ✅ Consult with a mortgage professional specializing in self-employed borrowers

Medium-Term Actions (Next 3-6 Months):

- ✅ Optimize bank statement patterns by maintaining consistent deposits

- ✅ Improve credit score if below 700

- ✅ Increase down payment savings if possible

- ✅ Research properties and neighborhoods

- ✅ Get pre-qualified to understand your buying power

The Competitive Advantage of Acting Now ⚡

2026 market conditions favor self-employed borrowers:

- Rate stability provides predictable planning and budgeting

- Increased lender competition creates favorable terms and pricing

- Mature underwriting standards result in faster, more consistent approvals

- Technology improvements streamline the application and approval process

- Growing acceptance of alternative documentation reduces stigma and improves options

Final Thoughts 💭

Bank statement loans have evolved from niche products to mainstream solutions for the millions of Americans who earn their living through self-employment. The programs offered by Angelo Oak, CrossCountry Mortgage, Griffin Funding, and First National Bank of America demonstrate that lenders recognize the value and stability of self-employed borrowers when evaluated through appropriate income verification methods.

The journey to homeownership as a self-employed individual may require more preparation and documentation than traditional employment, but the Best Bank Statement Loans for Self-Employed Borrowers in 2026: Top Lenders and Rates prove that entrepreneurship and homeownership are not mutually exclusive goals. With proper planning, documentation, and professional guidance, self-employed borrowers can secure competitive financing and achieve their real estate objectives.

Whether you’re purchasing your first home, upgrading to a larger property, refinancing for better terms, or expanding your investment portfolio, bank statement loans provide a viable pathway forward. The key is understanding the requirements, preparing thoroughly, and working with lenders who specialize in serving the self-employed community.

Take the first step today by assessing your qualification, organizing your documentation, and connecting with lenders who understand your unique financial situation. Your entrepreneurial success deserves recognition in the mortgage marketplace—and in 2026, bank statement loans ensure you receive it.

References

[1] Bank Statement Loans Self Employed Borrowers – https://lendsure.com/blog/bank-statement-loans-self-employed-borrowers/

[2] Bank Statement Mortgage Program – https://angeloakms.com/programs/bank-statement-mortgage-program/

[3] Todays Bank Statement Loan Rates In Texas – https://www.texasunitedmortgage.com/todays-bank-statement-loan-rates-in-texas

[4] Bank Statement Loans – https://crosscountrymortgage.com/mortgage/loans/non-qm/bank-statement-loans/

[5] Best Mortgage Lenders For Self Employed Mortgages In 2026 – https://www.lendfriendmtg.com/learning-center/best-mortgage-lenders-for-self-employed-mortgages-in-2026

[6] Bank Statement Loan Texas – https://griffinfunding.com/texas-mortgage-lender/bank-statement-loan-texas/

[7] Bank Statement Loans More Mortgage Options For Self Employed Buyers And Homeowners As Rates Ease – https://www.housingwire.com/articles/bank-statement-loans-more-mortgage-options-for-self-employed-buyers-and-homeowners-as-rates-ease/

[8] Bank Statement Loan – https://www.newamericanfunding.com/loan-types/non-qm-loan/bank-statement-loan/