February 7, 2026

Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

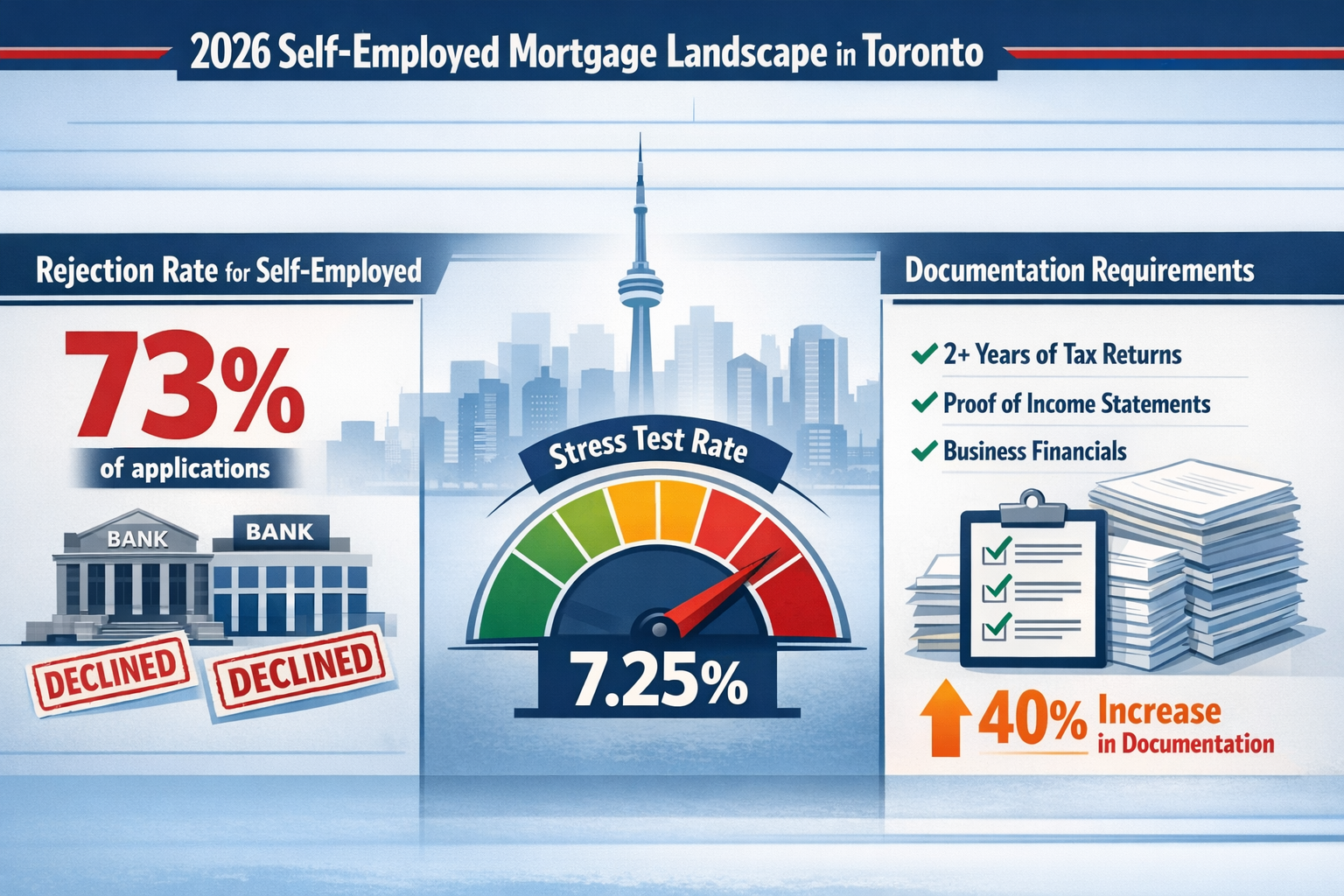

Imagine opening your mortgage renewal letter and discovering your monthly payment could jump by 20% or more. For self-employed Toronto homeowners facing renewal in 2026, this scenario isn’t just possible—it’s increasingly common. With approximately 33% of Canadian mortgage holders approaching renewal this year and major banks now rejecting 73% of self-employed applications that would have sailed through in 2024, understanding Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know has never been more critical[3].

The mortgage landscape has transformed dramatically. Self-employed borrowers who secured favourable rates years ago are now confronting a perfect storm: stricter lending criteria, elevated stress test requirements, and significantly higher documentation demands. The rules have changed, and those unprepared risk facing declined renewals, substantially higher rates, or being forced into alternative lending channels with premium pricing.

This comprehensive guide breaks down everything Toronto’s self-employed community needs to navigate the 2026 renewal process successfully. Whether you’re a contractor, consultant, physician, or business owner, the strategies outlined here will help you secure the best possible terms in today’s challenging environment.

Key Takeaways

✅ Major banks now reject 73% of self-employed mortgage applications that would have been approved in 2024, requiring 40% more documentation than previous years[3]

✅ Payment increases of 15-20% are expected for most five-year fixed-rate mortgages renewing in 2026, with self-employed borrowers facing additional rate premiums of 0.50-1.25%[1][3]

✅ Strategic tax planning 24 months before renewal can dramatically improve approval odds by reducing business write-offs and demonstrating stronger income[3]

✅ Alternative lending pathways including Alt-A and B-lender programs offer viable options when traditional banks decline, though at higher rates[3]

✅ Early preparation is essential—starting the renewal process 120-180 days before maturity provides maximum negotiating leverage and alternative options

Understanding the 2026 Self-Employed Mortgage Landscape

The mortgage environment for self-employed borrowers has undergone seismic shifts entering 2026. What worked just two years ago no longer applies, and Toronto’s entrepreneurial community must adapt quickly to secure favourable renewal terms.

The New Reality: Rejection Rates and Tightened Standards

The statistics paint a sobering picture. Major Canadian banks are now rejecting 73% of self-employed mortgage applications that would have received approval in 2024[3]. This dramatic increase reflects fundamental changes in how lenders assess self-employment income and risk.

Several key factors drive this trend:

📊 Elevated Stress Test Requirements: The mortgage stress test rate for self-employed borrowers has climbed to 7.25%, meaning applicants must prove they can afford payments at this qualifying rate even if actual rates are lower[3]. For a $600,000 mortgage, this translates to qualifying at approximately $4,200 monthly instead of the actual payment of around $3,600 at current rates.

📄 Documentation Explosion: Lenders now require 40% more documentation compared to 2024[3]. Where two years of Notice of Assessment (NOA) documents might have sufficed previously, borrowers now face requests for:

- Three years of complete tax returns (T1 Generals)

- Corporate tax returns (T2s) if incorporated

- Year-to-date profit and loss statements

- Business bank statements (6-12 months)

- Contracts or invoices demonstrating ongoing income

- CRA proof of income statements

- Accountant-prepared financial statements

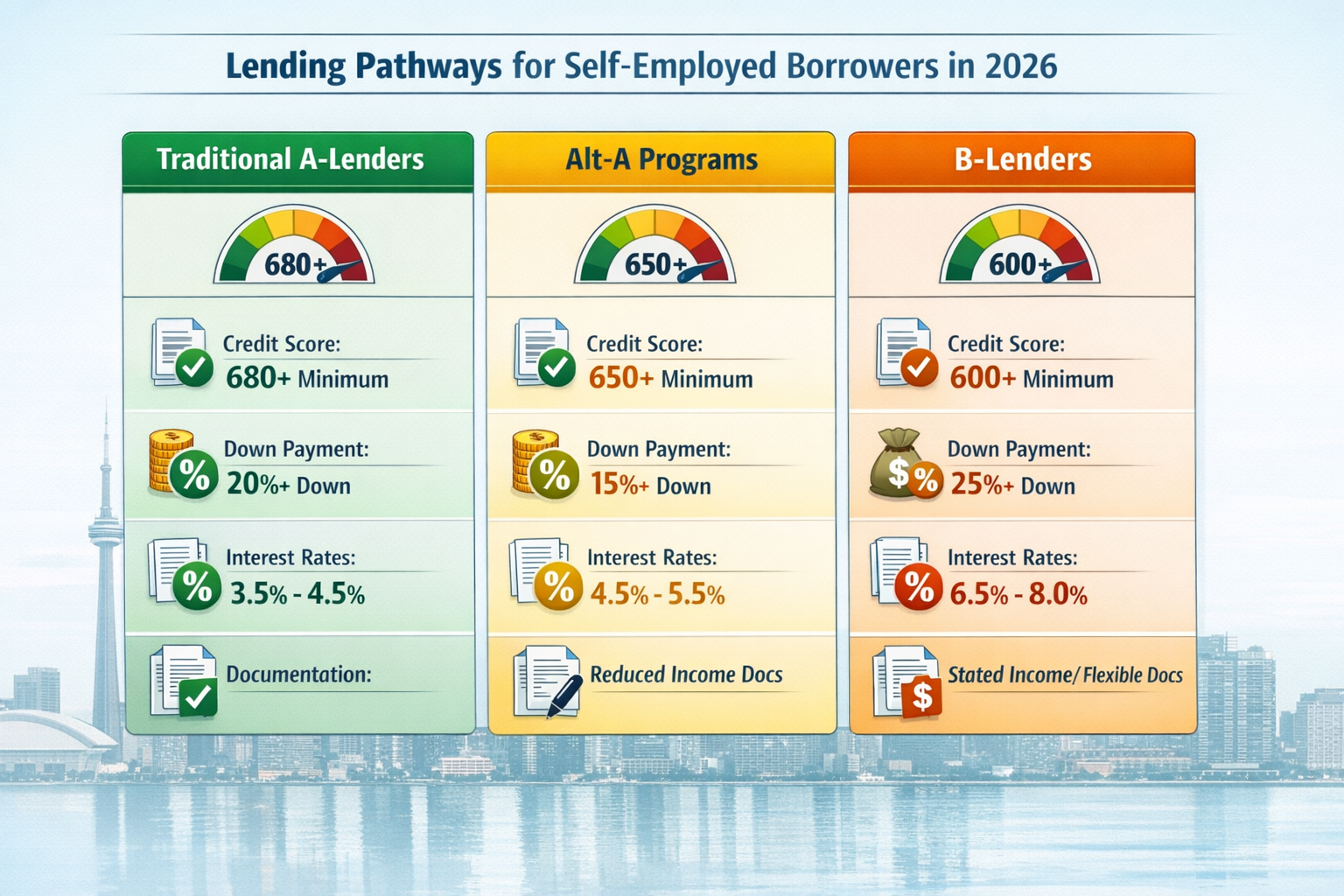

💳 Stricter Credit and Debt Requirements: Credit score minimums have increased across all lending categories. Conventional mortgages now require 680+ (up from 650), Alt-A programs require 650+, and B-lenders accept 600+[3]. Additionally, acceptable debt-to-income ratios have tightened to 42% for self-employed borrowers, down from 45%[3].

Interest Rate Environment and Premium Pricing

The interest rate landscape adds another layer of complexity for those navigating Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know. While conventional mortgage rates have stabilized around 6.75%, self-employed borrowers face additional premiums ranging from 0.50% to 1.25% depending on documentation strength[3].

This means:

- Strong documentation (3+ years, consistent income): 6.75% – 7.25%

- Moderate documentation (2 years, some fluctuation): 7.25% – 7.75%

- Limited documentation or newer businesses: 7.75% – 8.00%+

For context, approximately 60% of mortgage holders renewing in 2026 are expected to see payment increases, with five-year fixed-rate mortgages facing average increases of 15-20% compared to their previous payments[1]. Self-employed borrowers often experience the higher end of this range due to rate premiums.

The Toronto Factor: Local Market Considerations

Toronto’s unique real estate dynamics add specific challenges for self-employed renewal applicants. The city’s elevated property values mean larger mortgage amounts, which amplifies the impact of rate increases and stricter qualifying criteria.

A self-employed professional renewing a $750,000 mortgage in Toronto faces significantly different challenges than someone renewing $400,000 in a smaller market. The higher loan amount means:

- Greater scrutiny of income documentation

- Higher absolute dollar impact from rate premiums

- Increased sensitivity to debt-to-income calculations

- More significant payment shock from rate increases

Working with a best self-employed mortgage broker in Toronto who understands these local nuances becomes essential for navigating the renewal process successfully.

Preparing for Self-Employed Mortgage Renewals in 2026: Essential Strategies

Success in the 2026 renewal environment requires proactive preparation, ideally beginning 18-24 months before your maturity date. The self-employed borrowers who secure the best terms are those who treat renewal preparation as a strategic business initiative.

Tax Planning: The 24-Month Advantage

Perhaps the single most powerful strategy for improving renewal outcomes is strategic tax planning in the two years preceding your renewal. This approach requires balancing tax efficiency with mortgage qualification strength.

Reduce Business Write-Offs Strategically

While maximizing business deductions makes sense from a tax perspective, it works against mortgage qualification. Lenders assess your income based on what you report to the Canada Revenue Agency, not your actual cash flow.

Consider this example:

| Scenario | Gross Business Income | Business Expenses | Net Income (Line 150) | Mortgage Qualifying Income |

|---|---|---|---|---|

| Maximum Write-Offs | $180,000 | $95,000 | $85,000 | $85,000 |

| Strategic Approach | $180,000 | $70,000 | $110,000 | $110,000 |

The strategic approach costs approximately $6,250 in additional taxes (assuming 25% marginal rate on the extra $25,000 income) but increases qualifying income by $25,000 annually. Over two years, this builds a stronger income history while the tax cost ($12,500) is minimal compared to potential savings from better mortgage rates over a five-year term.

💡 Pro Tip: Work with both your accountant and mortgage professional 24 months before renewal to develop a tax strategy that balances immediate tax savings with mortgage qualification strength.

Leverage Corporate Structure (If Applicable)

Self-employed professionals with incorporated businesses have additional flexibility. Consider implementing a T4 salary alongside dividend income. While dividends are tax-efficient, T4 employment income carries more weight with traditional lenders and can strengthen your application significantly[3].

A balanced approach might include:

- $80,000 T4 salary (provides stable, easily verified income)

- $40,000 dividends (maintains tax efficiency)

- Retained earnings in corporation (demonstrates business stability)

This structure provides verifiable employment income while maintaining tax advantages. Learn more about getting a mortgage as a business owner in Canada.

Documentation Excellence: Building Your Renewal Package

In 2026’s environment where lenders require 40% more documentation[3], organizing a comprehensive renewal package months in advance provides significant advantages.

Create Your Master Documentation File

Assemble these documents 120-180 days before your renewal date:

📋 Income Verification:

- Last 3 years of complete tax returns (T1 General)

- All Notices of Assessment (NOAs)

- Corporate tax returns if incorporated (T2s)

- Year-to-date profit & loss statement

- Accountant-prepared financial statements

📋 Business Verification:

- Business registration documents

- GST/HST returns (demonstrates business legitimacy)

- Business bank statements (6-12 months)

- Major contracts or client agreements

- Business licenses or professional certifications

📋 Personal Financial Documents:

- Personal bank statements (3-6 months)

- Investment account statements

- Credit report (pull your own to review first)

- Property tax statements

- Existing mortgage statement

The Declaration Method for Established Businesses

Businesses operating for 3+ years with strong banking history may qualify for a streamlined approach. Some lenders accept signed income declarations with 25% down payment when bank deposits clearly exceed stated income needs[3].

This pathway works best when:

- Your business banking shows consistent deposits exceeding $10,000+ monthly

- You can provide 3+ years of business operation history

- You have 25%+ equity in your property

- Your credit score exceeds 700

This approach bypasses extensive tax return analysis, focusing instead on demonstrated cash flow through business banking activity.

Credit Optimization: Meeting the New Thresholds

With credit score minimums increasing across all lending categories, optimizing your credit profile becomes essential for accessing the best rates and terms.

Target Credit Score Benchmarks for 2026:

🎯 680+ for conventional A-lender mortgages (best rates)

🎯 650+ for Alt-A programs (competitive rates)

🎯 600+ for B-lender programs (higher rates but accessible)

90-Day Credit Improvement Strategies:

- Pay down revolving credit: Reduce credit card balances to below 30% of limits (ideally under 10%)

- Correct errors: Review your credit report and dispute any inaccuracies immediately

- Avoid new credit applications: Each inquiry can temporarily reduce your score

- Maintain perfect payment history: Set up automatic payments to ensure nothing is missed

- Keep old accounts open: Length of credit history matters significantly

Understanding the role of credit scores in the mortgage approval process helps prioritize the most impactful improvements.

Debt-to-Income Optimization

With acceptable debt-to-income ratios tightened to 42% for self-employed borrowers[3], reducing other debts before renewal can dramatically improve your position.

Calculate Your Current Ratio:

<code>Total Monthly Debt Payments ÷ Gross Monthly Income = Debt-to-Income Ratio

</code>Example:

- Mortgage payment: $2,800

- Car payment: $450

- Credit card minimum: $200

- Line of credit: $150

- Total debt payments: $3,600

- Gross monthly income: $9,000

- Debt-to-income ratio: 40% ✅

If your ratio exceeds 42%, consider:

- Paying off smaller debts entirely (car loans, credit cards)

- Consolidating high-interest debt

- Increasing reported income through tax planning

- Requesting credit limit increases (without using them) to improve utilization ratios

Alternative Lending Pathways for Self-Employed Mortgage Renewals in 2026

When traditional A-lenders decline your renewal application or offer unfavourable terms, alternative lending pathways provide viable solutions. Understanding these options is crucial for Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know.

Alt-A Mortgage Programs: The Middle Ground

Alt-A lenders bridge the gap between traditional banks and private lenders, offering reasonable rates for self-employed borrowers who don’t fit conventional criteria but maintain strong financial profiles.

High-Ratio Alt-A Programs

These programs accept down payments as low as 5% and provide competitive rates at Prime + 0.25% to 0.75%[3]. Key features include:

✅ Full NOA documentation required (2+ years of consistent income)

✅ Credit scores 650+ typically required

✅ CMHC or other mortgage insurance for down payments under 20%

✅ Rates currently 7.00% – 7.50% depending on profile strength

✅ Standard amortization up to 25-30 years

This pathway works exceptionally well for self-employed borrowers with:

- Fluctuating income that averages well over two years

- Strong credit but higher debt servicing ratios

- Newer businesses (2-3 years) showing growth trajectory

- Income that’s difficult to verify through traditional means

Stated Income Programs

For established businesses with 25%+ equity, stated income programs offer flexibility:

- Minimum 3 years in business required

- Bank statements demonstrating income flow

- 25%+ down payment or existing equity

- Rates typically 1-2% higher than conventional

- Simplified documentation compared to traditional mortgages

B-Lender Solutions: Accessibility with Premium Pricing

B-lenders specialize in serving borrowers who don’t qualify with traditional institutions. While rates are higher, these lenders provide crucial access when other options aren’t available.

B-Lender Profile:

📊 Credit requirements: 600+ accepted

📊 Income verification: Flexible approaches, may accept alternative documentation

📊 Rates: Typically 8.00% – 10.00% in current environment

📊 Terms: Usually 1-3 years, designed as bridge financing

📊 Equity requirements: Generally 20%+ required

When B-Lenders Make Sense:

- Recent credit challenges (consumer proposal, bankruptcy discharge)

- Insufficient income documentation for A or Alt-A lenders

- Complex income situations (multiple businesses, international income)

- Bridge financing while improving credit or income documentation

- Properties that don’t meet traditional lender criteria

The strategy with B-lenders often involves using a 1-2 year term to improve your financial profile, then refinancing to better terms with A or Alt-A lenders. Learn more about B-lender mortgage rates in Toronto.

Private Mortgage Solutions

Private mortgages represent the most flexible but expensive option, typically used for short-term bridge financing or unique situations.

Private Mortgage Characteristics:

- Rates: 8% – 15%+ depending on risk factors

- Terms: 6 months to 2 years typically

- Qualification: Primarily equity-based (loan-to-value focus)

- Fees: Higher lender and broker fees

- Speed: Fastest approval and funding timelines

Private mortgages work best as temporary solutions while addressing qualification challenges, not as long-term financing strategies.

Switching Lenders vs. Staying Put

One critical decision in the renewal process is whether to stay with your current lender or switch to a competitor. This choice significantly impacts both rates and qualification requirements.

Advantages of Switching:

✅ Access to competitive rates from multiple lenders

✅ Ability to shop for better terms and features

✅ Potential for improved mortgage features (prepayment options, portability)

✅ Leverage in negotiations with current lender

Challenges of Switching for Self-Employed:

❌ Full re-qualification required (complete documentation package)

❌ Subject to current, stricter lending criteria

❌ Potential for appraisal requirements

❌ Legal and administrative costs (though often covered by new lender)

Staying with Current Lender:

When renewing with your existing lender, you typically face simplified qualification. However, this convenience often comes at a cost—renewal rates offered are frequently 0.25% – 0.50% higher than available market rates.

💡 Strategic Approach: Begin by exploring switching options 120-180 days before maturity. Use competitive offers as leverage when negotiating with your current lender. Even if you ultimately stay, this process typically secures better rates than accepting the initial renewal offer.

Explore more about mortgage refinancing and switching lenders at renewal to understand the full advantages for self-employed borrowers.

Industry-Specific Considerations for Toronto Self-Employed Professionals

Different self-employment categories face unique challenges and opportunities in the 2026 renewal landscape. Understanding industry-specific factors helps tailor your approach for maximum success.

Contractors and Trades Professionals

Construction contractors, electricians, plumbers, and other trades professionals often face specific documentation challenges despite strong actual incomes.

Common Challenges:

- Seasonal income fluctuations

- High business expense ratios

- Cash components to income (difficult to document)

- Subcontractor vs. employee classification issues

Optimization Strategies:

📌 Maintain detailed invoicing records showing consistent client relationships

📌 Separate personal and business banking clearly

📌 Consider GST/HST registration (demonstrates business legitimacy)

📌 Document long-term contracts or recurring client relationships

📌 Average income over 2-3 years to smooth seasonal variations

Contractors should review our specialized guide on self-employed mortgages for contractors for detailed strategies.

IT Consultants and Tech Professionals

Technology consultants, software developers, and IT professionals often have strong incomes but face challenges related to contract work and incorporation structures.

Unique Advantages:

✅ Generally higher income levels

✅ Strong credit profiles

✅ Often incorporated (provides structure flexibility)

✅ Verifiable contracts with established companies

Documentation Best Practices:

- Provide copies of major consulting contracts

- Show consistent contract renewals or new client acquisition

- Leverage T4 salary from your corporation

- Demonstrate retained earnings and business stability

- Highlight professional certifications and credentials

Learn more through our IT consultant self-employed mortgage resource.

Medical Professionals and Physicians

Doctors, dentists, and other medical professionals typically enjoy favourable treatment from lenders despite self-employment status, though 2026’s tighter environment affects even this traditionally preferred group.

Lender Advantages:

✅ Recognized professional designation

✅ Stable, predictable income

✅ Lower perceived risk

✅ Often qualify for professional mortgage programs

Specific Considerations:

- Billings vs. net income (some lenders assess gross billings)

- Partnership or group practice structures

- Overhead costs in private practice

- Professional corporation dividend strategies

Medical professionals should consult our specialized self-employed mortgages for doctors guide for profession-specific strategies.

Business Owners with Multiple Income Streams

Entrepreneurs with multiple businesses, rental properties, or diverse income sources face complexity in presenting a clear income picture to lenders.

Documentation Strategy:

- Consolidate income presentation: Create a summary showing all income sources

- Prioritize strongest sources: Lead with most stable, verifiable income

- Explain complementary businesses: Show how multiple ventures reduce overall risk

- Leverage rental income: Investment properties can strengthen applications when properly documented

For those with rental properties, understanding investing in rental properties as a self-employed individual provides valuable insights.

Navigating the Renewal Timeline: Month-by-Month Action Plan

Success in Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know requires following a strategic timeline. Here’s your month-by-month roadmap for optimal results.

180 Days Before Renewal (6 Months Out)

🎯 Primary Objectives: Assessment and initial preparation

Action Items:

✅ Review your current mortgage details: Note your maturity date, current rate, remaining balance, and any prepayment privileges

✅ Pull your credit report: Identify any issues requiring correction

✅ Assess your documentation: Determine what you have and what you need

✅ Calculate current debt ratios: Understand where you stand relative to the 42% threshold

✅ Research current market rates: Establish baseline expectations

✅ Consult with mortgage professional: Get preliminary assessment of your renewal prospects

120 Days Before Renewal (4 Months Out)

🎯 Primary Objectives: Documentation assembly and credit optimization

Action Items:

✅ Assemble complete documentation package: Gather all tax returns, NOAs, bank statements, and business documents

✅ Implement credit improvements: Pay down balances, correct errors, optimize utilization

✅ Meet with accountant: Review income reporting strategy and discuss any year-end planning

✅ Reduce unnecessary debt: Pay off small balances to improve debt ratios

✅ Begin lender shopping: Start exploring options beyond your current lender

90 Days Before Renewal (3 Months Out)

🎯 Primary Objectives: Active lender engagement and rate shopping

Action Items:

✅ Submit applications to 2-3 lenders: Include your current lender and competitors

✅ Obtain rate holds: Lock in current rates while continuing to shop

✅ Compare mortgage features: Look beyond rates to prepayment options, portability, penalties

✅ Request written offers: Get everything in writing for comparison

✅ Negotiate with current lender: Use competitive offers as leverage

60 Days Before Renewal (2 Months Out)

🎯 Primary Objectives: Decision making and commitment

Action Items:

✅ Make final lender selection: Choose based on rate, terms, and overall value

✅ Finalize documentation: Provide any additional requested items promptly

✅ Review commitment letter carefully: Ensure all terms match discussions

✅ Arrange legal review if switching: Ensure smooth transfer process

✅ Confirm all conditions: Verify what’s required before funding

30 Days Before Renewal (1 Month Out)

🎯 Primary Objectives: Final execution and preparation

Action Items:

✅ Complete all outstanding conditions: Submit final documents or information

✅ Arrange payment method: Set up new payment schedule

✅ Review final numbers: Confirm rate, payment amount, and term

✅ Prepare for payment adjustment: Budget for any payment increases

✅ Confirm funding date: Ensure seamless transition

Renewal Date

🎯 Primary Objectives: Smooth transition

Action Items:

✅ Verify new mortgage is in place: Confirm funding completion

✅ Update payment information: Ensure correct bank account is debited

✅ File all documents: Keep complete records of new mortgage terms

✅ Calendar next renewal date: Begin planning for next renewal cycle

✅ Review mortgage features: Understand prepayment options and other benefits

Common Pitfalls to Avoid in Self-Employed Mortgage Renewals

Even well-prepared self-employed borrowers can stumble into costly mistakes during the renewal process. Awareness of these common pitfalls helps you avoid them.

Waiting Until the Last Minute

The Mistake: Starting the renewal process 30 days or less before maturity.

The Consequence: Limited options, reduced negotiating leverage, potential for rushed decisions, and risk of accepting unfavourable terms due to time pressure.

The Solution: Begin renewal preparation 120-180 days before maturity. This timeline provides adequate opportunity to address documentation challenges, improve credit, shop lenders, and negotiate effectively.

Automatically Accepting the Renewal Offer

The Mistake: Signing the renewal letter your lender sends without shopping alternatives.

The Consequence: Renewal rates are typically 0.25% – 0.50% higher than available market rates. On a $600,000 mortgage, this costs approximately $1,500 – $3,000 annually in unnecessary interest.

The Solution: Always shop your renewal, even if you ultimately stay with your current lender. Use competitive offers to negotiate better terms.

Neglecting Tax Planning

The Mistake: Maximizing business deductions in the two years before renewal without considering mortgage implications.

The Consequence: Artificially low reported income that doesn’t reflect actual earning capacity, leading to declined applications or reduced borrowing power.

The Solution: Work with both your accountant and mortgage professional to balance tax efficiency with mortgage qualification strength 24 months before renewal.

Ignoring Credit Score Impact

The Mistake: Making large purchases on credit, applying for new credit cards, or missing payments in the months before renewal.

The Consequence: Reduced credit scores can bump you into higher-rate lending categories or result in declined applications.

The Solution: Treat the 6-12 months before renewal as a “credit freeze” period. Avoid new credit applications, maintain perfect payment history, and optimize existing credit utilization.

Failing to Document Income Properly

The Mistake: Providing incomplete documentation or failing to explain income fluctuations.

The Consequence: Lenders assess your income conservatively, often using the lowest year or heavily discounting variable income.

The Solution: Provide complete documentation proactively with written explanations for any fluctuations. Show trends, growth patterns, and factors supporting income stability.

Overlooking Alternative Lender Options

The Mistake: Assuming if traditional banks decline your application, you’re out of options.

The Consequence: Missing viable Alt-A or B-lender solutions that, while more expensive, prevent forced property sales or emergency refinancing.

The Solution: Work with mortgage professionals who have access to the full lending spectrum, including Alt-A and B-lender programs. Access our self-employed mortgage Q&A resource for comprehensive guidance.

Mixing Business and Personal Finances

The Mistake: Using business accounts for personal expenses or vice versa, creating unclear financial pictures.

The Consequence: Lenders cannot clearly verify income, leading to conservative assessments or declined applications.

The Solution: Maintain completely separate banking for business and personal finances. This clarity dramatically simplifies income verification and strengthens your application.

Frequently Asked Questions About Self-Employed Mortgage Renewals in 2026

How much will my mortgage payment increase at renewal in 2026?

Most five-year fixed-rate mortgages renewing in 2026 face average payment increases of 15-20% compared to their previous payments[1]. Self-employed borrowers often experience the higher end of this range due to rate premiums of 0.50-1.25%[3]. However, approximately half of 2026 renewals may actually see payment declines if they switch to alternative mortgage types or benefit from recent rate decreases[6].

Example calculation:

- Previous payment (2021 rate of 2.5%): $2,800/month

- Renewal payment (2026 rate of 6.75%): $3,360/month

- Increase: $560/month or 20%

Can I switch lenders at renewal if I’m self-employed?

Yes, you can switch lenders at renewal, but be prepared for full re-qualification under 2026’s stricter standards. You’ll need to provide complete documentation and meet the new lender’s criteria, which may be more stringent than when you originally qualified. The advantage is access to competitive rates and better terms, potentially saving thousands over your mortgage term.

What if my lender declines my renewal application?

While uncommon, lenders can decline renewals if your financial situation has deteriorated significantly or if you no longer meet current lending criteria. If this happens:

- Don’t panic: You have options through Alt-A and B-lenders

- Understand why: Get clear explanation of the decline reasons

- Address issues: Improve credit, reduce debt, or strengthen documentation

- Explore alternatives: Work with a mortgage broker to access alternative lenders

- Consider bridge financing: Short-term private financing while improving your profile

How far in advance should I start the renewal process?

Ideal timeline: 120-180 days (4-6 months) before your maturity date. This provides adequate time to:

- Assemble documentation

- Improve credit scores

- Shop multiple lenders

- Negotiate effectively

- Address any unexpected challenges

Starting early is especially critical for self-employed borrowers given the 40% increase in documentation requirements[3].

Do I need an appraisal when renewing my mortgage?

When renewing with your current lender, an appraisal is typically not required. However, if you’re switching lenders or accessing additional equity through refinancing, the new lender will likely require a current appraisal. Budget approximately $300-500 for professional appraisal services in the Toronto area.

Should I choose a fixed or variable rate at renewal?

This decision depends on your risk tolerance, budget flexibility, and market outlook. In 2026’s environment:

Fixed rates provide:

- Payment certainty and budgeting ease

- Protection against potential rate increases

- Peace of mind for risk-averse borrowers

Variable rates offer:

- Typically lower starting rates

- Potential savings if rates decrease

- Greater flexibility with lower penalties

For self-employed borrowers facing payment increases, fixed rates often provide valuable certainty for business planning. Review our comprehensive fixed vs. variable rates guide for detailed analysis.

What documentation do I need for self-employed mortgage renewal in 2026?

Comprehensive documentation requirements include:

Income Verification:

- 3 years of complete tax returns (T1 General)

- All Notices of Assessment (NOAs)

- Corporate tax returns if incorporated (T2s)

- Year-to-date profit & loss statement

- CRA proof of income statements

Business Verification:

- Business registration documents

- Business bank statements (6-12 months)

- Major contracts or agreements

- Professional licenses or certifications

Personal Financial:

- Personal bank statements (3-6 months)

- Current mortgage statement

- Credit report

- Property tax statements

Check our complete mortgage document checklist for comprehensive preparation.

Working with Mortgage Professionals: Maximizing Your Renewal Success

Given the complexity of Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know, partnering with experienced mortgage professionals dramatically improves your outcomes.

The Value of Mortgage Brokers for Self-Employed Borrowers

Mortgage brokers provide several critical advantages:

🏆 Access to Multiple Lenders: Brokers work with dozens of lenders including A-lenders, Alt-A programs, B-lenders, and private sources. This breadth ensures you find the best fit for your specific situation.

🏆 Self-Employment Expertise: Experienced brokers understand how to present self-employed income in the most favourable light, knowing which lenders are most receptive to different business structures and income types.

🏆 Documentation Guidance: Brokers help you assemble documentation strategically, highlighting strengths and addressing potential weaknesses proactively.

🏆 Negotiating Power: Brokers leverage relationships and volume to negotiate better rates and terms than individual borrowers typically access.

🏆 Time Savings: Rather than approaching multiple lenders individually, your broker submits your application to appropriate lenders simultaneously, streamlining the process.

🏆 No Direct Cost: Lenders pay broker commissions, so you access professional expertise without direct fees in most cases.

Questions to Ask Potential Mortgage Professionals

When selecting a mortgage broker or advisor, ask:

“How much experience do you have with self-employed mortgages specifically?” Look for substantial self-employment expertise, not just general mortgage knowledge.

“Which lenders do you work with?” Ensure they have access to Alt-A and B-lender options beyond traditional banks.

“Can you provide references from self-employed clients?” Speak with past clients about their experiences.

“What’s your approach to presenting self-employed income?” Assess their strategic thinking and documentation expertise.

“How do you handle declined applications?” Understand their problem-solving approach and backup options.

“What are your fees, if any?” Clarify any potential costs upfront.

The Renewal Consultation Process

A thorough renewal consultation with a mortgage professional should include:

Initial Assessment (30-45 minutes):

- Review of current mortgage details

- Discussion of income and employment situation

- Credit profile review

- Preliminary qualification assessment

- Overview of current market rates and options

Documentation Review (1-2 weeks):

- Detailed review of your documentation package

- Identification of any gaps or weaknesses

- Strategic recommendations for strengthening application

- Timeline development for submission

Lender Shopping (2-4 weeks):

- Submission to appropriate lenders

- Rate hold securing

- Negotiation with current and new lenders

- Presentation of options with detailed comparison

Decision Support (1 week):

- Analysis of all offers received

- Recommendation based on your priorities

- Review of terms, conditions, and features

- Assistance with final selection

Execution (2-4 weeks):

- Coordination of all documentation

- Management of conditions and requirements

- Liaison with lawyers and lenders

- Confirmation of funding and completion

Conclusion: Taking Control of Your 2026 Mortgage Renewal

The landscape for Self-Employed Mortgage Renewals in 2026: What Toronto Borrowers Need to Know presents significant challenges, but informed preparation transforms these obstacles into manageable steps. While major banks now reject 73% of self-employed applications that would have been approved just two years ago[3], and payment increases of 15-20% are expected for most renewals[1], self-employed borrowers who implement the strategies outlined in this guide can successfully navigate the process and secure favourable terms.

The key differentiators between successful renewals and challenging outcomes come down to:

✅ Early preparation beginning 120-180 days before maturity

✅ Strategic tax planning in the 24 months preceding renewal

✅ Comprehensive documentation addressing the 40% increase in lender requirements

✅ Credit optimization to meet elevated score thresholds

✅ Exploration of alternative lending pathways when traditional banks decline

✅ Professional guidance from experienced mortgage brokers

Your Next Steps

Don’t wait until your renewal date approaches. Take action now:

Immediate Actions (This Week):

- Note your exact renewal date and calculate your 120-day preparation start date

- Pull your credit report to identify any issues requiring attention

- Gather your last three years of tax returns and NOAs

- Calculate your current debt-to-income ratio to understand your starting position

- Research current mortgage rates to establish baseline expectations

Short-Term Actions (Next 30 Days):

- Consult with a mortgage professional experienced in self-employed renewals

- Meet with your accountant to discuss income optimization strategies

- Begin credit improvement initiatives if your score is below optimal thresholds

- Assemble your complete documentation package following the checklist in this guide

- Review your business financial structure to identify strengthening opportunities

Medium-Term Actions (Next 90 Days):

- Implement tax planning strategies to strengthen income documentation

- Pay down debt to improve debt-to-income ratios

- Start lender shopping if you’re within 120 days of renewal

- Obtain rate holds to protect against potential increases

- Negotiate with your current lender using competitive offers

The mortgage renewal process doesn’t need to be stressful or result in unfavourable terms. With proper preparation, strategic planning, and professional guidance, self-employed Toronto borrowers can successfully renew their mortgages in 2026’s challenging environment while securing competitive rates and terms that support their financial goals.

Remember, approximately half of 2026 renewals are expected to see payment declines through strategic approaches[6], proving that informed action produces positive results even in difficult markets. Your self-employment status is a strength demonstrating entrepreneurial success—present it strategically, prepare thoroughly, and partner with experienced professionals to achieve renewal success.

For personalized guidance on your specific situation, explore our comprehensive self-employed mortgage resources or connect with a mortgage professional who understands the unique challenges and opportunities facing Toronto’s self-employed community in 2026.

References

[1] Staff Analytical Note 2025 21 – https://www.bankofcanada.ca/2025/07/staff-analytical-note-2025-21/

[2] Mortgage Renewal – https://www.ratehub.ca/mortgage-renewal

[3] 5 Steps To Navigating 2026s Tightened Self Employed Lending Rules – https://www.kraftmortgages.ca/blog/5-steps-to-navigating-2026s-tightened-self-employed-lending-rules

[4] Watch – https://www.youtube.com/watch?v=2O6zz6aU2XE

[6] F9a87ba8 9962 4265 A2a9 E51303e269ca – https://economics.bmo.com/en/publications/detail/f9a87ba8-9962-4265-a2a9-e51303e269ca/