February 9, 2026

Will Mortgage Rates Drop Further for Self-Employed in Toronto in 2026? Expert Forecast

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The question on every self-employed professional’s mind in Toronto right now is simple yet critical: Will mortgage rates drop further for self-employed in Toronto in 2026? As we navigate through 2026, the answer is becoming clearer—and it’s not what many hopeful borrowers expected. With the Bank of Canada holding its policy rate steady at 2.25% and bond yields showing limited downside, the era of dramatic rate cuts appears to be over. For self-employed individuals seeking mortgage financing in Toronto, understanding this new reality is essential for making informed decisions about homeownership and refinancing strategies.

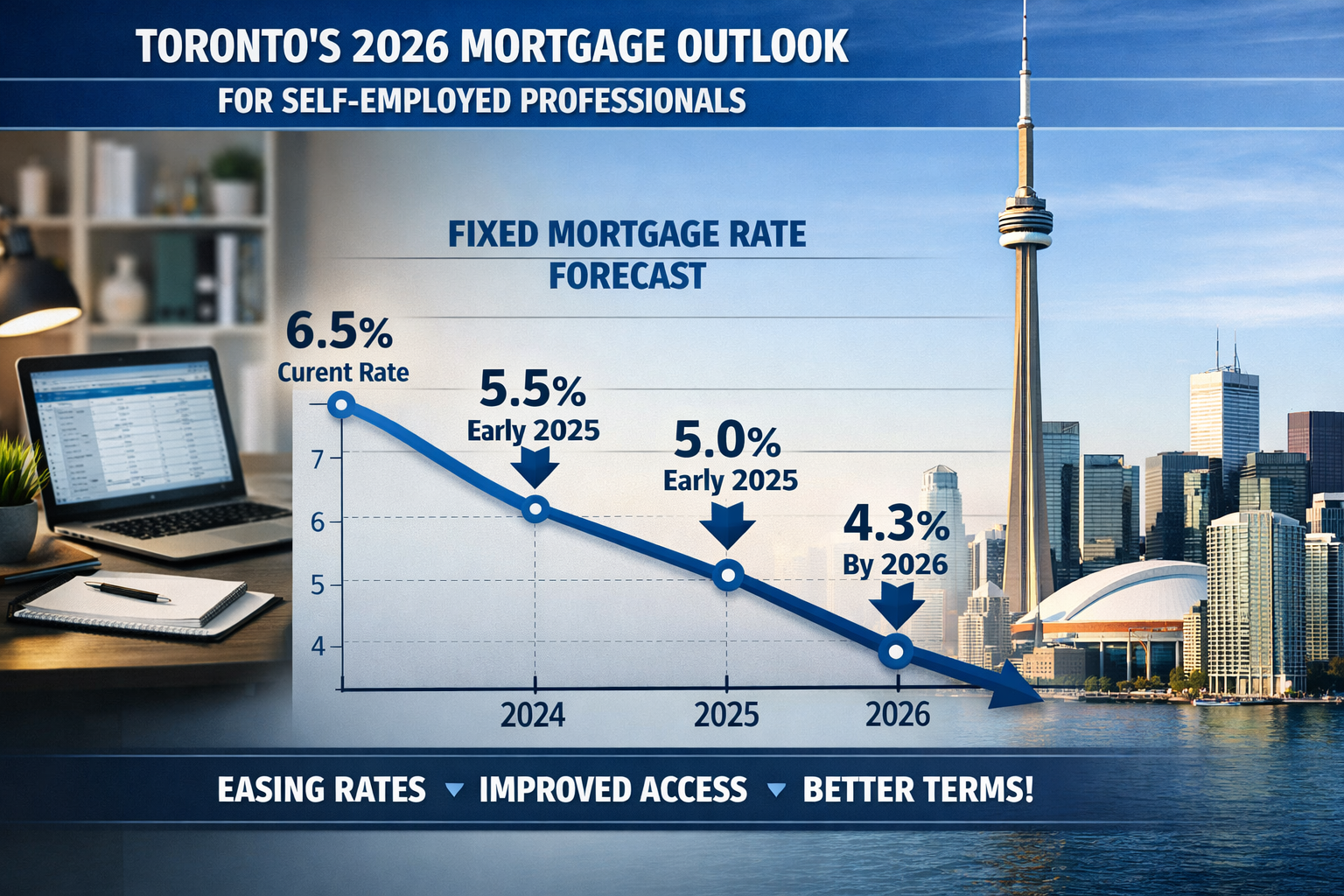

The landscape for self-employed mortgage rates in Toronto in 2026 presents both challenges and opportunities. While fixed rates hover around 3.69% and variable rates remain attractive at approximately 3.35%, the unique documentation requirements and income verification processes for self-employed borrowers add complexity to an already nuanced market. This comprehensive expert forecast will help you navigate what lies ahead.

Key Takeaways

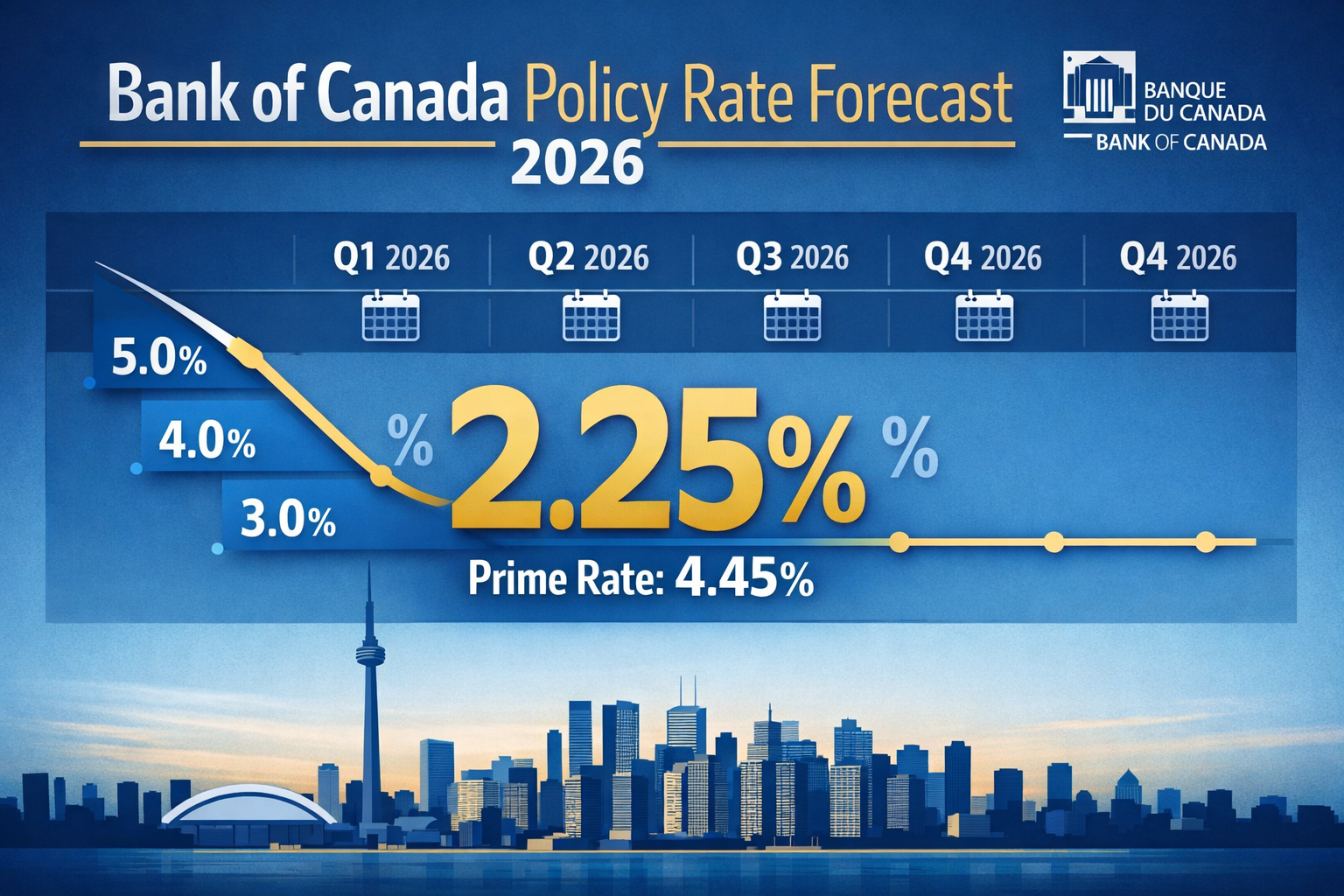

📊 Bank of Canada’s policy rate is expected to remain at 2.25% throughout 2026, with the prime rate holding steady at 4.45%, meaning significant rate drops are unlikely[2][3].

📉 5-year fixed mortgage rates are projected to stay between 4.5% and 5.5% for most of 2026, with limited downside potential due to stable bond yields[6].

💼 Self-employed borrowers face unique challenges in qualifying for mortgages, but current stable rates create a predictable environment for planning.

⚖️ Variable rates around 3.35% remain attractive compared to fixed rates, though the risk-reward profile has shifted with minimal downside and potential upside risk[4].

🏠 Approximately 33% of Canadian mortgage holders will face higher payments by the end of 2026, making strategic planning essential for renewals[2].

Understanding the Bank of Canada’s 2026 Rate Hold and What It Means for Self-Employed Borrowers

The Bank of Canada made a decisive statement at its January 28, 2026 meeting by holding its policy rate at 2.25%, with the corresponding prime rate remaining at 4.45%[3]. This decision signals a fundamental shift in monetary policy from the aggressive cutting cycle that characterized 2024 and 2025 to a period of stability and observation.

For self-employed professionals in Toronto, this rate hold carries significant implications. Unlike the dramatic cuts that brought relief to borrowers over the past two years, markets now expect the policy rate to remain at 2.25% through at least Q3 2026[3]. This stability means that those hoping for substantially lower mortgage rates will likely be disappointed.

What Major Banks Are Forecasting

The consensus among Canada’s major financial institutions is remarkably uniform. Most major Canadian banks predict rates will end 2026 at the same level they began, with only a couple of outliers—National Bank and CIBC—expecting potential increases of 50 basis points to 2.75% by year-end[2]. This near-unanimous forecast suggests that the current rate environment represents a “new normal” rather than a temporary pause.

The projected rate path for 2026 shows remarkable consistency:

| Month/Quarter | Expected BoC Policy Rate | Prime Rate |

|---|---|---|

| January 2026 | 2.25% | 4.45% |

| March 2026 | 2.25% | 4.45% |

| June 2026 | 2.25% | 4.45% |

| September 2026 | 2.25% | 4.45% |

| Q4 2026 | 2.25% – 2.75% | 4.45% – 4.95% |

Why Self-Employed Borrowers Should Pay Attention

For self-employed individuals, this rate stability has a dual impact. On one hand, predictable rates make financial planning easier, allowing for more accurate budgeting and business forecasting. On the other hand, those who delayed mortgage applications hoping for significantly lower rates may have missed the optimal window.

The December 2025 inflation readings showed no immediate pressure for a rate hike[3], which provides some reassurance. However, the Bank of Canada has made it clear that any future rate adjustments will be “gradual and measured, aimed at fine-tuning rather than delivering broad-based relief”[2]. This means borrowing costs are unlikely to return to pre-pandemic lows anytime soon.

For self-employed professionals navigating the mortgage landscape, understanding these macro trends is just the first step. The real challenge lies in how these rates translate into actual mortgage products and qualification criteria—topics we’ll explore in depth throughout this forecast.

Will Mortgage Rates Drop Further for Self-Employed in Toronto in 2026? The Fixed Rate Reality

The short answer to whether mortgage rates will drop further for self-employed borrowers in Toronto in 2026 is: not significantly. Fixed mortgage rates, which are primarily influenced by bond yields rather than the Bank of Canada’s policy rate, have already found their floor for the foreseeable future.

Current Fixed Rate Landscape

5-year fixed mortgage rates are expected to remain stable between 4.5% and 5.5% throughout most of 2026[6]. The most optimistic forecasts suggest rates could hover near 4.5% by year-end[4], but this represents the lower bound rather than a likely scenario for all borrowers.

For self-employed individuals specifically, these rates typically appear at the higher end of the spectrum due to perceived risk factors. Self-employed mortgages for contractors and other independent professionals often face rate premiums of 0.25% to 0.50% compared to traditionally employed borrowers, depending on documentation strength and income stability.

Why Fixed Rates Won’t Drop Much Further

Several factors are keeping fixed rates elevated:

📈 Bond Yield Stability: Government of Canada bond yields, which directly influence fixed mortgage rates, have stabilized and show limited downside potential. The 5-year bond yield has found support around current levels, creating a floor for fixed mortgage rates.

💰 Lender Margin Protection: After years of compressed margins during the rate-cutting cycle, lenders are now protecting their profitability. Even if bond yields decline modestly, banks may not pass the full savings to borrowers.

🎯 Risk Premium Persistence: The economic uncertainty surrounding global trade tensions, particularly potential U.S. tariffs, has kept risk premiums elevated. As discussed in our analysis of how potential U.S. tariffs could impact Canadian mortgage rates, these external factors create upward pressure on rates.

🏦 Funding Cost Realities: Banks’ cost of funds has stabilized at levels that support current mortgage rates. Without significant changes in deposit rates or wholesale funding costs, there’s limited room for rate reductions.

The Self-Employed Premium

For self-employed borrowers in Toronto, the reality is even more nuanced. The ultimate guide to securing a mortgage for self-employed Canadians reveals that documentation quality significantly impacts the rates offered.

Strong documentation (two years of Notice of Assessments, consistent income, minimal write-offs) may qualify for rates near the advertised 4.5% range. However, borrowers with complex income structures or significant business deductions often face rates in the 5.0% to 5.5% range, or may need to consider alternative lending options.

“Fixed rates are unlikely to see substantial further declines in 2026; instead, they are expected to remain near current levels.”[4]

This stability actually presents an opportunity for self-employed borrowers. Rather than waiting for rates that may never materialize, locking in current fixed rates around 3.69% to 4.5% (for well-qualified borrowers) provides certainty and protection against potential future increases.

Strategic Considerations for Fixed Rate Mortgages

Self-employed professionals should consider these factors when evaluating fixed rates:

✅ Income Stability: If your business income fluctuates significantly, a fixed rate provides payment predictability that can help with cash flow management.

✅ Tax Planning Impact: As outlined in tax smarts and maximizing benefits for the self-employed in Canada, the way you structure business deductions affects mortgage qualification. Fixed rates may be more accessible if you’ve minimized write-offs to show higher income.

✅ Term Selection: With rates expected to remain stable, 5-year fixed terms offer good value. Shorter terms may not provide sufficient savings to justify the renewal risk.

✅ Prepayment Flexibility: Ensure your fixed-rate mortgage includes adequate prepayment privileges, as self-employed income can be irregular, and the ability to make lump-sum payments during profitable periods is valuable.

The bottom line: Will mortgage rates drop further for self-employed in Toronto in 2026? For fixed rates, the answer is largely no. Current levels represent the new normal, and borrowers should plan accordingly rather than waiting for significant declines that are unlikely to materialize.

Variable Rates vs. Fixed Rates: What Self-Employed Borrowers Need to Know in 2026

While fixed rates have stabilized, variable rates present a different picture for self-employed borrowers in Toronto. Understanding the dynamics between these two options is crucial for making the right mortgage decision in 2026.

Current Variable Rate Environment

Variable rates are expected to remain broadly stable until mid-2026, with very little movement anticipated if the Bank of Canada remains on hold[4]. Currently, well-qualified borrowers can access variable rates around 3.35%, which represents a significant discount compared to fixed rates hovering around 4.5% or higher.

For self-employed individuals, this spread of approximately 1.15% to 2.15% between variable and fixed rates creates a compelling value proposition—but only for those who can qualify and tolerate the inherent risk.

The Risk-Reward Profile Has Shifted

The traditional calculation for choosing between variable and fixed rates has changed dramatically in 2026. Here’s why:

Limited Downside Potential 🔻

- With the Bank of Canada expected to hold rates at 2.25% throughout most of 2026, further cuts are remote[2]

- Variable rate borrowers cannot expect the same savings that characterized 2024-2025

- The best-case scenario is rate stability, not significant decreases

Asymmetric Upside Risk 🔺

- A resurgence in inflation could force the BoC to consider raising rates again in 2027[4]

- Global economic uncertainties, including trade tensions, create upward pressure

- Variable rate borrowers face the risk of payment increases without the corresponding benefit of potential decreases

Who Should Choose Variable Rates?

Despite the shifted risk profile, variable rates still make sense for certain self-employed borrowers:

✅ Risk-Tolerant Borrowers: Those with stable, growing businesses who can absorb potential payment increases without financial stress.

✅ Short-Term Homeowners: If you plan to sell or refinance within 2-3 years, the immediate savings from variable rates may outweigh the risk.

✅ High-Income Professionals: Self-employed mortgages for doctors and other high-earning professionals who have significant cash reserves can weather rate volatility.

✅ Strategic Refinancers: Those who plan to convert to fixed rates if the BoC signals future increases can benefit from current variable rate savings while maintaining flexibility.

Who Should Choose Fixed Rates?

Fixed rates are more appropriate for:

🏠 Budget-Conscious Borrowers: Self-employed individuals with variable income who need payment certainty for household budgeting.

📊 Conservative Planners: Those who prioritize stability over potential savings, especially given the limited downside for variable rates.

⏰ Long-Term Homeowners: If you plan to stay in your home for 5+ years, locking in current fixed rates provides protection against future uncertainty.

💼 Business Reinvestors: Self-employed professionals who reinvest heavily in their businesses and prefer predictable mortgage costs.

The Mathematics of the Decision

Let’s examine a practical example for a self-employed borrower in Toronto:

Scenario: $600,000 mortgage, 25-year amortization

| Rate Type | Rate | Monthly Payment | Annual Cost | 5-Year Total Cost |

|---|---|---|---|---|

| Variable | 3.35% | $2,965 | $35,580 | $177,900 |

| Fixed | 4.50% | $3,337 | $40,044 | $200,220 |

| Difference | 1.15% | $372 | $4,464 | $22,320 |

Over five years, the variable rate saves $22,320 compared to the fixed rate—if rates remain stable. However, if the BoC raises rates by just 0.50% in 2027, much of this advantage disappears. If rates increase by 1.00% or more, the fixed rate becomes the better choice.

Qualification Differences for Self-Employed Borrowers

An often-overlooked aspect is that qualification requirements differ between variable and fixed rates:

Stress Test Impact: Both variable and fixed rates must pass the mortgage stress test, but the qualifying rate differs. Variable rates use the contract rate plus 2%, while fixed rates use the greater of the contract rate plus 2% or the Bank of Canada’s benchmark rate.

Income Documentation: Some lenders are more flexible with easier qualification for self-employed borrowers on variable rate products, as they’re perceived as less risky for the lender (they can adjust with rate changes).

Alternative Lender Options: If you don’t qualify with A-lenders, B-lender mortgage rates in Toronto may offer variable products with more flexible documentation requirements, though at higher rates.

The Hybrid Approach

Some self-employed borrowers benefit from a split mortgage strategy:

- 50% fixed at current rates (4.5% – 5.5%) for stability

- 50% variable at current rates (~3.35%) for savings potential

This approach provides a balance between payment certainty and cost optimization, which can be particularly valuable for self-employed individuals with fluctuating income.

Expert Recommendation for 2026

Given the current rate environment and forecast, variable rates around 3.35% offer better value than fixed rates for self-employed borrowers who:

- Have strong cash reserves (6+ months of expenses)

- Demonstrate stable or growing business income

- Can absorb potential payment increases of 15-20%

- Plan to monitor rates actively and potentially convert to fixed if the BoC signals increases

However, fixed rates around 4.5% to 5.5% are more appropriate for those who:

- Prioritize payment certainty over potential savings

- Have tight monthly budgets with limited flexibility

- Prefer a “set it and forget it” approach

- Believe inflation risks will materialize in 2027

The key is understanding your personal risk tolerance, business income stability, and financial goals. For personalized guidance on mortgages for self-employed borrowers, consulting with a mortgage professional who understands the unique challenges of self-employment is essential.

Navigating Mortgage Renewals and Refinancing as a Self-Employed Borrower in 2026

One of the most significant challenges facing Canadian mortgage holders in 2026—including many self-employed professionals in Toronto—is the mortgage renewal wave. Understanding how to navigate this landscape is critical for financial success.

The Renewal Crisis: By the Numbers

The statistics paint a sobering picture:

📈 33% of Canadian mortgage holders are expected to face higher monthly mortgage payments by the end of 2026[2]. For self-employed borrowers, this percentage may be even higher due to the timing of when many independent professionals entered the housing market.

🏦 Approximately 75% of borrowers facing payment increases have 5-year fixed-rate mortgages, with average payment increases expected around 20%[2]. This means a borrower currently paying $2,500 monthly could see payments jump to $3,000 or more.

📊 Variable rate renewal outcomes vary dramatically:

- 10% are projected to see payments rise by more than 40%

- Roughly 25% could see payments fall by at least 7%

- The remainder will see modest increases or stability[2]

Unique Challenges for Self-Employed Renewals

Self-employed borrowers face additional hurdles during the renewal process:

Income Verification Requirements: Even at renewal, many lenders now require updated income documentation. If your business income has declined or you’ve increased tax deductions, you may not qualify for the same mortgage amount or rate.

Changed Qualification Rules: Mortgage rules have evolved since you obtained your original mortgage. The stress test and other qualification criteria may now work against you, even with the same lender.

Business Performance Scrutiny: Lenders will examine your most recent two years of tax returns. If 2024 or 2025 showed reduced income compared to when you originally qualified, you may face challenges.

Credit Score Changes: Self-employment can sometimes lead to irregular credit utilization. Ensure your credit score remains strong before renewal time.

Strategic Renewal Planning for Self-Employed Borrowers

Start Early ⏰ Begin the renewal process 120-180 days before your maturity date. This gives you time to:

- Shop multiple lenders for the best rates

- Address any documentation issues

- Improve your financial profile if needed

- Consider alternative lender options if necessary

Optimize Your Income Reporting 💰 Work with your accountant to balance tax optimization with mortgage qualification:

- Consider reducing business deductions in the year before renewal

- Ensure your Notice of Assessment accurately reflects your income capacity

- Prepare detailed financial statements showing business stability

- Document any non-traditional income sources properly

Consider Your Options 🔄

- Traditional Renewal: Accept your current lender’s offer (often not the best rate)

- Rate Negotiation: Use competing offers to negotiate better terms

- Lender Switch: Move to a new lender offering better rates (requires full re-qualification)

- Alternative Lenders: If you don’t qualify with A-lenders, explore B-lenders or private options

- Refinancing: Access equity for business investment or debt consolidation

Refinancing Opportunities in 2026

For self-employed professionals, refinancing can serve multiple strategic purposes beyond just securing a better rate:

Business Investment 💼 Access home equity to fund business expansion, purchase equipment, or increase working capital. With rates around 4.5% to 5.5%, mortgage financing is often cheaper than business loans or lines of credit.

Debt Consolidation 💳 Consolidate high-interest business or personal debt into your mortgage. This can significantly improve cash flow and simplify financial management.

Tax Efficiency 📋 Mortgage interest on funds used for business purposes may be tax-deductible. Consult with a tax professional about the implications.

Cash Reserve Building 🏦 Extract equity to build business cash reserves, providing a buffer against income volatility.

The Rate Lock Dilemma

One critical decision for self-employed borrowers renewing in 2026 is whether to lock in a fixed rate or choose variable:

Case for Locking In Fixed:

- Rates are unlikely to drop significantly further

- Payment certainty helps with business budgeting

- Protection against potential 2027 rate increases

- Peace of mind during economic uncertainty

Case for Variable:

- Immediate savings of 1.15% to 2.15% compared to fixed

- Flexibility to convert to fixed if rates begin rising

- Benefit from any unexpected rate cuts

- Lower initial payments improve cash flow

Alternative Lending Solutions

If you don’t qualify for traditional renewal terms, several options exist:

B-Lenders: These institutions specialize in non-traditional borrowers and may offer:

- More flexible income verification

- Higher debt service ratios

- Consideration of alternative documentation

- Rates typically 0.50% to 2.00% higher than A-lenders

Private Lenders: For challenging situations, private mortgages provide:

- Minimal income verification

- Focus on property equity rather than income

- Faster approval processes

- Higher rates (typically 7% to 12%) but short-term solutions

Credit Unions: Often more flexible than major banks for self-employed borrowers, with competitive rates and personalized service.

Payment Increase Preparation

If you’re facing a significant payment increase at renewal, take these steps:

📊 Calculate the Impact: Use mortgage calculators to determine your new payment based on current rates.

💰 Adjust Your Budget: Start living with the higher payment amount now, saving the difference to build reserves.

🏠 Consider Amortization Extension: If available, extending your amortization can reduce payment shock (though it increases total interest paid).

💼 Increase Business Income: If possible, focus on growing business revenue before renewal to improve qualification.

🔄 Explore Income-Averaging: Some lenders will average income over multiple years if recent years show declines.

The Bottom Line for Renewals

For self-employed borrowers in Toronto facing renewal in 2026, the key is proactive planning. Don’t wait for your lender’s renewal offer—it’s rarely the best available rate. Start exploring options early, optimize your financial profile, and be prepared to demonstrate the strength and stability of your self-employed income.

The mortgage landscape has changed significantly since many borrowers obtained their original mortgages. Understanding these changes and working with professionals who specialize in self-employed mortgages can make the difference between a smooth renewal and a financial challenge.

Expert Strategies for Self-Employed Mortgage Success in Toronto’s 2026 Market

As we’ve established that mortgage rates are unlikely to drop significantly further for self-employed borrowers in Toronto in 2026, the focus shifts to optimization strategies. Success in this environment requires understanding how to position yourself for the best possible rates and terms despite the unique challenges of self-employment.

Maximizing Your Qualification Strength

Documentation Excellence 📄

The foundation of securing favorable mortgage rates as a self-employed borrower is impeccable documentation:

Essential Documents:

- Two years of complete T1 General tax returns

- Two years of Notice of Assessments (NOAs) from CRA

- Business financial statements (if incorporated)

- Year-to-date profit and loss statements

- Corporate tax returns (T2) if applicable

- Business license and registration documents

- Six months of business bank statements

- Personal bank statements showing regular deposits

Pro Tip: Organize these documents in a professional package before approaching lenders. This demonstrates business competence and makes underwriters’ jobs easier, potentially resulting in better rate offers.

Income Reporting Strategy

One of the biggest challenges for self-employed borrowers is the tension between tax optimization (minimizing taxable income) and mortgage qualification (maximizing reported income).

The Two-Year Planning Approach:

Years 1-2 Before Mortgage Application:

- Minimize business deductions

- Report higher taxable income

- Accept higher tax liability as an investment in mortgage qualification

- Document all income sources clearly

After Mortgage Approval:

- Return to optimal tax strategy

- Maximize legitimate business deductions

- Reduce tax burden

This strategic approach can make the difference between qualifying at A-lender rates (4.5% to 5.5%) versus requiring B-lender or private financing (6% to 12%).

Alternative Documentation Programs

Some lenders offer stated income or alternative documentation programs specifically designed for self-employed borrowers:

Bank Statement Programs: Lenders analyze 12-24 months of business bank deposits to determine income rather than relying solely on tax returns. This can benefit borrowers who write off significant business expenses.

Asset-Based Programs: For high-net-worth self-employed individuals, some lenders consider total assets rather than just income when determining qualification.

Industry-Specific Programs: Certain professions (doctors, lawyers, accountants) may qualify for specialized programs with more flexible requirements.

Credit Score Optimization

Your credit score significantly impacts the rates you’ll be offered. For self-employed borrowers, maintaining excellent credit is even more critical:

Target Score: 740+ for best rates Minimum Score: 680 for A-lender consideration Below 680: May require B-lender or alternative solutions

Credit Improvement Strategies:

- ✅ Pay all bills on time (set up automatic payments)

- ✅ Keep credit utilization below 30% (ideally below 10%)

- ✅ Maintain long-standing credit accounts

- ✅ Avoid new credit applications before mortgage shopping

- ✅ Review credit reports for errors and dispute inaccuracies

- ✅ Pay down high-interest debts first

Down Payment Strategies

Larger down payments can offset some of the challenges self-employed borrowers face:

20%+ Down Payment Benefits:

- Avoid mortgage default insurance premiums

- Access to better rates

- Stronger negotiating position with lenders

- Lower debt service ratios

- Reduced perceived risk

Creative Down Payment Sources:

- RRSP Home Buyers’ Plan (up to $35,000 per person)

- Gift from family members (with proper documentation)

- Sale of investments or other properties

- Business retained earnings (with proper documentation)

- Vendor take-back arrangements

Choosing the Right Lender Type

Not all lenders are created equal when it comes to self-employed mortgages:

Big Banks:

- ✅ Competitive rates for well-qualified borrowers

- ✅ Full-service banking relationships

- ❌ Rigid qualification criteria

- ❌ Limited flexibility for complex income situations

Credit Unions:

- ✅ More personalized service

- ✅ Greater flexibility in underwriting

- ✅ Competitive rates

- ❌ May have membership requirements

- ❌ Smaller lending capacity

Monoline Lenders:

- ✅ Highly competitive rates

- ✅ Specialized mortgage focus

- ✅ Flexible programs

- ❌ Mortgage-only (no other banking services)

B-Lenders:

- ✅ Specialize in non-traditional borrowers

- ✅ Flexible income verification

- ✅ Higher approval rates

- ❌ Rates typically 0.50% to 2.00% higher

Private Lenders:

- ✅ Minimal qualification requirements

- ✅ Fast approvals

- ✅ Focus on equity, not income

- ❌ Significantly higher rates (7% to 12%)

- ❌ Shorter terms (typically 1-2 years)

The Mortgage Broker Advantage

For self-employed borrowers, working with a mortgage broker who specializes in self-employed financing offers significant advantages:

Access to Multiple Lenders: Brokers can shop your application to dozens of lenders, finding the best fit for your unique situation.

Expertise in Documentation: Experienced brokers know exactly how to present your income and financial situation to maximize approval odds.

Program Knowledge: Brokers stay current on specialized programs and lenders that cater to self-employed borrowers.

Negotiating Power: Brokers often secure better rates than borrowers can obtain directly.

No Cost to Borrower: Lenders pay broker commissions, so this service is typically free.

Timing Your Application Strategically

Best Times to Apply:

📅 After Tax Season (May-June): Your most recent NOA is available, providing current income verification.

📅 End of Fiscal Year: If you can demonstrate strong year-end results, this strengthens your application.

📅 During Rate Stability: In 2026’s stable rate environment, there’s less urgency, allowing time for proper preparation.

Times to Avoid:

❌ Immediately After Major Business Expenses: Large deductions can reduce qualifying income.

❌ During Business Transitions: Changing business structures or industries creates uncertainty.

❌ Right Before Tax Filing: Wait until you have your NOA to avoid delays.

Building Lender Relationships

Establishing banking relationships before you need a mortgage can pay dividends:

Relationship Banking Strategy:

- Maintain business and personal accounts with your target lender

- Use their business credit products responsibly

- Build a track record of financial responsibility

- Develop rapport with business banking representatives

When mortgage time comes, you’re a known entity rather than a stranger, potentially resulting in more favorable consideration.

Preparing for the Application Process

90 Days Before Application:

- Gather all documentation

- Review and improve credit score

- Reduce outstanding debts

- Avoid large purchases or new credit

60 Days Before:

- Consult with mortgage broker or lender

- Get pre-qualified to understand your budget

- Address any documentation gaps

- Prepare explanations for any credit issues

30 Days Before:

- Finalize documentation package

- Submit formal pre-approval application

- Begin property search with confidence

- Maintain financial stability (no major changes)

The Reality Check: When to Consider Alternatives

Sometimes, despite best efforts, traditional financing isn’t immediately available. Recognize when alternative strategies make sense:

Consider B-Lender or Private Financing If:

- Recent business start (less than 2 years)

- Significant income decline in recent years

- Credit challenges (score below 650)

- Complex income structure

- Need for speed (traditional approval too slow)

Use Alternative Financing as Bridge:

- Secure property now with private or B-lender financing

- Spend 1-2 years improving qualification profile

- Refinance to A-lender rates once qualified

- Total cost may be lower than waiting and facing higher property prices

Looking Beyond 2026: Long-Term Planning

While this forecast focuses on 2026, successful self-employed borrowers think long-term:

5-Year Strategy:

- Build business stability and growth trajectory

- Maintain excellent credit throughout

- Accumulate equity through property appreciation and principal paydown

- Position for favorable renewal terms

- Consider future refinancing opportunities

Business Structure Optimization:

- Consult with accountants about optimal business structure for mortgage qualification

- Balance tax efficiency with lending appeal

- Document business stability through consistent financial reporting

- Build business value that lenders recognize

The bottom line for self-employed mortgage success in Toronto’s 2026 market is preparation and presentation. While rates may not drop significantly further, well-prepared self-employed borrowers can still access competitive financing by understanding lender requirements and positioning themselves strategically.

Conclusion: Taking Action in Toronto’s 2026 Mortgage Market

So, will mortgage rates drop further for self-employed in Toronto in 2026? The expert forecast is clear: significant rate decreases are unlikely. With the Bank of Canada holding its policy rate at 2.25% throughout most of 2026, and 5-year fixed mortgage rates stabilizing between 4.5% and 5.5%, the era of dramatic rate cuts has ended[2][6].

For self-employed professionals in Toronto, this creates both clarity and urgency. Clarity because the rate environment is predictable, allowing for confident financial planning. Urgency because waiting for substantially lower rates may mean missing opportunities in a market where property values could rise faster than rates fall.

Key Insights to Remember

🎯 Fixed rates around 4.5% to 5.5% represent the new normal, with limited downside potential due to stable bond yields.

📊 Variable rates near 3.35% offer immediate savings but come with asymmetric risk—minimal potential for further decreases but real possibility of future increases.

💼 Self-employed borrowers face unique challenges but can access competitive rates through proper documentation, strategic income reporting, and working with specialized lenders.

⏰ 33% of mortgage holders will face payment increases by end of 2026, making proactive renewal planning essential[2].

🏦 Alternative lending options exist for those who don’t qualify with traditional lenders, providing paths to homeownership even with complex income situations.

Your Action Plan for 2026

If You’re Planning to Purchase:

- Get pre-approved now rather than waiting for rates that may never materialize

- Prepare comprehensive documentation showing 2+ years of stable self-employed income

- Consider variable rates if you have strong cash reserves and risk tolerance

- Work with specialists who understand self-employed mortgage qualification

- Optimize your credit score to access the best available rates

If You’re Facing Renewal:

- Start the process 120-180 days early to maximize your options

- Shop multiple lenders rather than accepting your current lender’s offer

- Update your documentation to reflect current income and business stability

- Calculate payment impacts and adjust your budget accordingly

- Consider refinancing if you need to access equity for business or personal purposes

If You’re Currently Shopping:

- Act decisively in the current stable rate environment

- Compare fixed vs. variable based on your specific risk tolerance and financial situation

- Explore all lender types including banks, credit unions, monolines, and B-lenders

- Negotiate aggressively using competing offers to secure better terms

- Lock in rates when you find favorable terms rather than gambling on future decreases

The Bigger Picture

The 2026 mortgage market for self-employed borrowers in Toronto is defined by stability rather than volatility. While this may disappoint those hoping for a return to ultra-low rates, it actually creates a favorable environment for strategic decision-making.

Rates are predictable, allowing you to plan with confidence. Lender competition remains strong, creating opportunities for well-qualified borrowers. Alternative options exist for those with complex situations. And most importantly, homeownership remains achievable for self-employed professionals who prepare properly.

The question isn’t whether rates will drop significantly—they won’t. The question is whether you’ll position yourself to take advantage of the opportunities that exist in the current market.

Final Thoughts

Success in Toronto’s 2026 mortgage market as a self-employed borrower comes down to three principles:

Preparation: Organize your documentation, optimize your financial profile, and present your income in the best possible light.

Education: Understand how rates work, what drives them, and what options exist for your specific situation.

Action: Make informed decisions based on current realities rather than hoping for future changes that may never materialize.

The mortgage landscape has fundamentally changed from the pandemic era. Self-employed borrowers who accept this new reality and adapt their strategies accordingly will find that competitive financing remains accessible—just with different expectations and approaches than in years past.

Whether you choose fixed rates for stability or variable rates for immediate savings, whether you work with A-lenders or explore alternatives, the key is making an informed decision that aligns with your business situation, risk tolerance, and long-term financial goals.

The best mortgage rate is the one you can qualify for, afford comfortably, and that supports your overall financial strategy. In Toronto’s 2026 market, that rate is available now for self-employed borrowers who prepare properly and act strategically.

Don’t wait for rates that may never come. Instead, focus on positioning yourself for success in the market as it exists today. Your homeownership goals are within reach—with the right preparation, guidance, and action.

References

[1] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[2] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/

[3] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast

[4] Mortgage Interest Rate Forecast – https://www.mortgagesandbox.com/mortgage-interest-rate-forecast

[5] Mortgage Rates Forecast 2025 2027 Canada – https://redkeymortgage.ca/blog/mortgage-rates-forecast-2025-2027-canada/

[6] 2026 Mortgage Rate Forecast – https://mortgage.zuzart.ca/2026-mortgage-rate-forecast/

[7] Canada Interest Rate Forecast – https://myperch.io/canada-interest-rate-forecast/

[8] 2026 Mortgage Market – https://www.darrenrobinson.ca/mortgage-blog/2026-mortgage-market/