February 22, 2026

Why GTA Renters Are Switching to Ownership in 2026: Cost Comparison and Transition Roadmap

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The Greater Toronto Area housing market has entered a unique phase in 2026. With inventory levels reaching 5.8 months and strong rental demand continuing to push monthly costs upward, many renters are now pulling out their calculators to run the numbers. The question on everyone’s mind: Is it finally time to switch from renting to owning?

Understanding why GTA renters are switching to ownership in 2026 requires looking beyond simple monthly payment comparisons. The current buyer’s market, combined with stabilizing mortgage rates and persistent rental price pressures, has created a window of opportunity that savvy renters are beginning to recognize. This comprehensive guide explores the cost comparison and transition roadmap that can help renters make this important financial decision.

Key Takeaways

✅ Rental costs continue climbing while the GTA housing market offers increased inventory and buyer negotiating power in 2026

✅ Break-even analysis shows many renters can recover ownership costs within 5-7 years, building equity instead of paying landlords

✅ First-time buyers represent 45% of intending purchasers in 2026, with new tools and programs making the transition more accessible

✅ Strategic timing matters: Current market conditions favor prepared buyers who understand closing costs, down payment options, and mortgage pre-approval

✅ The transition roadmap involves specific steps from financial assessment to keys in hand, typically taking 6-12 months for committed renters

Understanding the 2026 GTA Housing Market Landscape

Current Market Conditions Favoring Buyers

The GTA housing market has shifted dramatically from the seller-dominated environment of previous years. In 2026, inventory levels have reached 5.8 months, giving buyers significantly more negotiating power and time to make informed decisions. This represents a substantial change from the frenzied bidding wars that characterized earlier periods.

Average home prices in the GTA are expected to stabilize between $1 million and $1.03 million throughout 2026, with some softness anticipated in the first half of the year. This price stability, combined with increased selection, creates an environment where renters can transition to ownership without the fear of immediate price escalation or being forced into rushed decisions.

The Toronto Regional Real Estate Board forecasts approximately 60,000 to 70,000 transactions for 2026, mirroring 2025 levels. While this represents steady rather than explosive activity, it indicates a mature market where quality properties remain available for serious buyers.

Why Rental Demand Remains Strong

Despite favorable buying conditions, rental demand in the GTA continues to surge. Immigration patterns, newcomers establishing themselves before purchasing, and economic uncertainty all contribute to sustained pressure on rental inventory. This demand translates directly into rising rental costs that are pushing many long-term renters to reconsider their housing strategy.

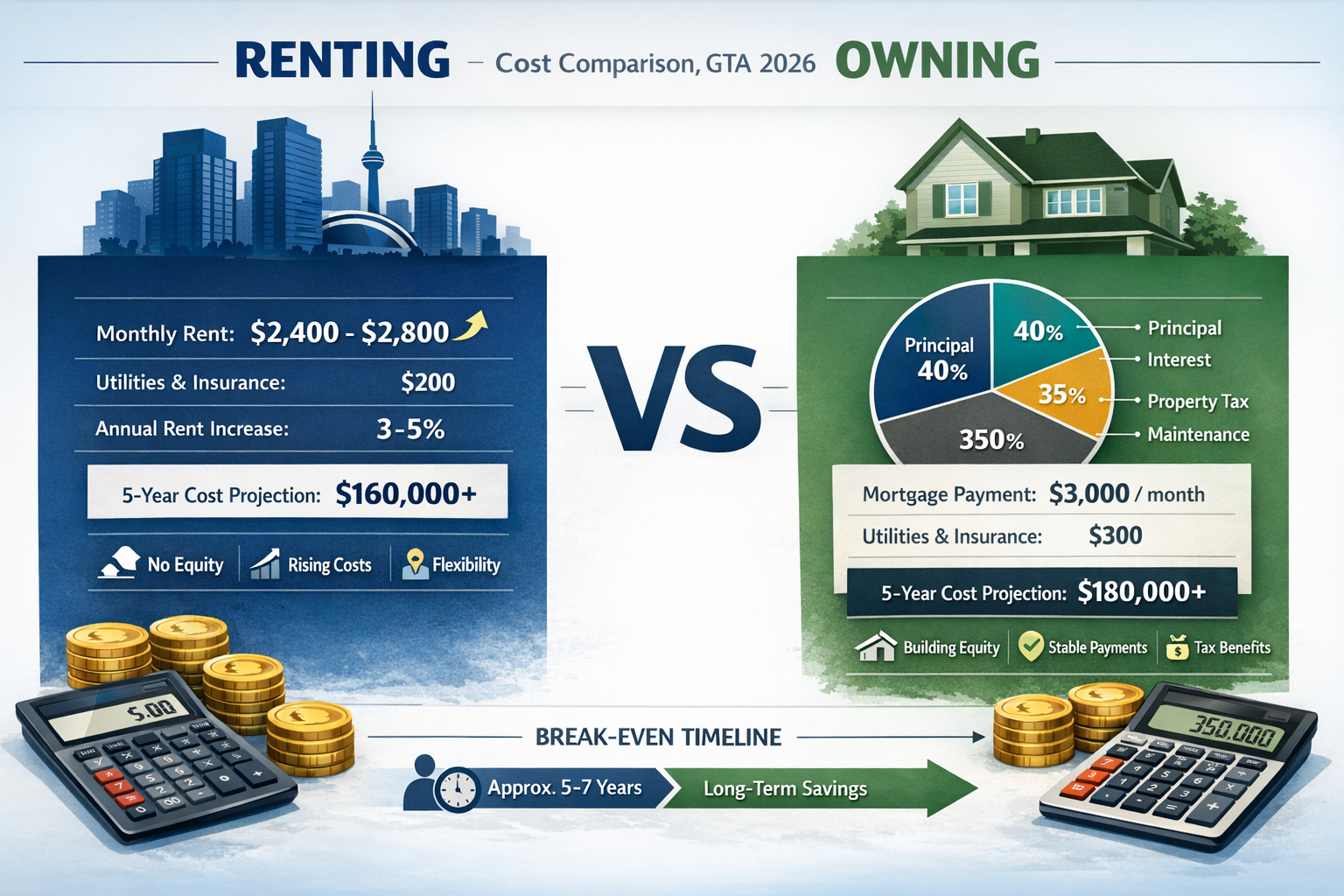

Monthly rental rates for one-bedroom units in Toronto proper now average $2,400 to $2,800, while two-bedroom units command $3,200 to $3,800 depending on location and amenities. These figures represent significant portions of household income, often exceeding the recommended 30% threshold for housing costs.

The rental market’s strength paradoxically creates the motivation for renters to explore ownership. When monthly rent approaches or exceeds potential mortgage payments, the equation shifts from “Can I afford to buy?” to “Can I afford NOT to buy?”

The Real Cost Comparison: Renting vs. Owning in 2026

Breaking Down Monthly Rental Costs

To understand why GTA renters are switching to ownership in 2026, examining the true cost of renting provides essential context. Monthly rent represents only the most visible expense. Renters also face:

- Annual rent increases averaging 2-5% in rent-controlled units, potentially higher in newer buildings

- Utility costs not included in base rent (hydro, internet, sometimes heat)

- Renter’s insurance typically $25-50 monthly

- Parking fees ranging from $100-300 monthly in many buildings

- Storage locker fees adding another $50-150 monthly

- Pet fees where applicable, often $25-75 per pet monthly

A renter paying $2,600 monthly for a one-bedroom condo might actually spend $3,100-3,400 when all associated costs are included. Over five years, assuming modest 3% annual increases, this renter will pay approximately $195,000 with zero equity accumulation.

Understanding True Ownership Costs

Homeownership involves different cost structures that many renters underestimate or misunderstand. For a $600,000 condo purchase (representing an entry-level property in many GTA areas), the monthly costs break down as follows:

Mortgage Payment Components:

- Principal and interest (20% down, 5.5% rate, 25-year amortization): ~$2,750

- Property taxes: ~$300

- Condo fees: ~$450

- Home insurance: ~$100

- Maintenance reserve: ~$150

Total monthly: ~$3,750

However, this comparison requires deeper analysis. Unlike rent, a portion of the mortgage payment builds equity. In the example above, approximately $1,500-1,800 monthly goes toward principal reduction in the early years, representing forced savings that increase net worth.

Additionally, homeowners benefit from:

- Property appreciation (historically 3-5% annually in GTA)

- Mortgage interest deductibility for investment properties

- Renovation value additions that increase property worth

- Fixed housing costs (principal and interest remain constant with fixed-rate mortgages)

For those exploring their options, understanding closing costs in Toronto provides crucial insight into the upfront investment required beyond the down payment.

The Five-Year Cost Projection

Creating a realistic five-year projection reveals why many renters are making the switch:

| Year | Renter Total Paid | Owner Total Paid | Owner Equity Built | Owner Net Cost |

|---|---|---|---|---|

| 1 | $39,000 | $45,000 | $21,600 | $23,400 |

| 2 | $79,170 | $90,000 | $44,800 | $45,200 |

| 3 | $120,565 | $135,000 | $69,700 | $65,300 |

| 4 | $163,282 | $180,000 | $96,400 | $83,600 |

| 5 | $207,420 | $225,000 | $125,000 | $100,000 |

Assumptions: 3% annual rent increases, 4% property appreciation, consistent mortgage payments

By year five, the renter has spent $207,420 with nothing to show for it, while the homeowner has spent $225,000 but accumulated $125,000 in equity (principal paydown plus appreciation), resulting in a net cost of just $100,000. The homeowner is effectively $107,420 ahead financially.

This analysis doesn’t even account for the psychological benefits of ownership, the ability to customize living space, or the forced savings discipline that mortgage payments provide.

Break-Even Point Analysis

The critical question for renters considering the switch: When do you break even?

For most GTA properties in 2026, the break-even point—where ownership costs equal rental costs when factoring in equity building—occurs between 5 to 7 years. This timeline depends on several variables:

- Down payment size (larger down payments reduce monthly costs and accelerate break-even)

- Property appreciation rates (GTA historically averages 3-5% annually)

- Rental cost inflation (currently 3-5% annually)

- Mortgage interest rates (2026 rates ranging from 4.5-6.5%)

- Transaction costs (realtor fees, land transfer taxes if selling early)

Renters planning to stay in the GTA for at least 5-7 years typically benefit financially from ownership. Those with shorter timelines may find renting more cost-effective due to transaction costs and the time required for appreciation to offset initial expenses.

Understanding important mortgage features to consider helps renters evaluate whether their situation aligns with successful homeownership.

Why GTA Renters Are Switching to Ownership in 2026: The Driving Factors

Economic Factors Creating Opportunity

Several economic conditions have converged in 2026 to make the transition from renting to owning more attractive:

💰 Stabilizing Mortgage Rates

After the volatility of 2022-2024, mortgage rates have found a more predictable range in 2026. Five-year fixed rates hover between 4.9% and 6.5%, while variable rates offer competitive alternatives for risk-tolerant buyers. This stability allows renters to plan with greater confidence.

🏘️ Increased Housing Inventory

The 5.8 months of inventory represents a significant shift toward buyer-friendly conditions. Renters transitioning to ownership benefit from:

- More time to conduct thorough property inspections

- Reduced pressure to waive conditions

- Greater negotiating leverage on price and terms

- Ability to be selective about location and features

📊 Price Stabilization

Unlike the rapid appreciation of previous years, 2026 prices are expected to remain relatively flat in the first half before potential modest increases in the second half. This creates a “soft landing” environment where buyers aren’t racing against escalating prices, reducing FOMO (fear of missing out) as a decision driver.

🏦 Improved Lending Options

Mortgage lenders in 2026 have expanded programs targeting first-time buyers and renters making the transition. Options include:

- Extended amortizations for insured mortgages (30 years for first-time buyers)

- Lower down payment requirements for qualifying properties

- Alternative documentation for self-employed individuals

- Flexible debt service ratio calculations

For self-employed renters, qualifying for mortgages without T4 slips has become significantly more accessible in 2026.

Psychological and Lifestyle Factors

Beyond pure economics, several non-financial factors motivate renters to pursue ownership:

🔑 Control and Stability

Homeownership provides freedom from:

- Landlord restrictions on renovations, pets, or guests

- Uncertainty about lease renewals

- Potential forced moves due to property sales

- Limitations on personalizing living space

👨👩👧👦 Family Planning

Many renters reach life stages where ownership aligns with family goals:

- Starting or expanding families requiring more space

- Desire for outdoor areas and child-friendly neighborhoods

- Need for home offices in hybrid work environments

- Proximity to specific school districts

💪 Wealth Building Mindset

The realization that rent payments build landlord wealth rather than personal equity creates powerful motivation. Renters increasingly view homeownership as:

- Forced savings through mortgage principal reduction

- Inflation hedge as property values typically rise with inflation

- Retirement planning tool (mortgage-free living in later years)

- Intergenerational wealth transfer opportunity

🌱 Community Connection

Ownership often correlates with deeper community engagement:

- Greater investment in neighborhood improvement

- Longer-term relationships with neighbors

- Participation in local governance and planning

- Sense of permanence and belonging

These factors combine with favorable economic conditions to create the momentum behind why GTA renters are switching to ownership in 2026.

The Complete Transition Roadmap: From Renter to Homeowner

Step 1: Financial Assessment and Preparation (Months 1-3)

The journey from renting to owning begins with honest financial evaluation. This critical phase determines readiness and identifies areas requiring improvement.

📋 Credit Score Review

Obtain credit reports from both Equifax and TransUnion (free annually). Lenders typically require minimum scores of:

- 680+ for best rates with A-lenders

- 600-679 for alternative lender options

- Below 600 may require credit repair before proceeding

Address any errors immediately and implement strategies to improve your credit score if needed. Simple improvements like paying down credit card balances below 30% utilization can boost scores within 2-3 months.

💵 Down Payment Calculation

Determine realistic down payment targets:

- Minimum 5% for properties under $500,000

- 5% on first $500,000 + 10% on remainder for properties $500,000-$999,999

- Minimum 20% for properties $1 million+

For a $600,000 property, the minimum down payment would be $40,000 (5% of $500,000 = $25,000, plus 10% of $100,000 = $10,000, plus closing costs of approximately $5,000-8,000).

🏦 Savings Strategy Development

Create an accelerated savings plan using:

- First Home Savings Account (FHSA): Contribute up to $8,000 annually (lifetime maximum $40,000) with tax deductions

- RRSP Home Buyers’ Plan: Withdraw up to $35,000 tax-free for down payment

- TFSA: Tax-free growth for additional savings

- Automated transfers: Set up automatic deposits each payday

Many successful buyers combine all three accounts to maximize down payment potential. Learn more about RRSP and the Home Buyers Plan to optimize this strategy.

📊 Budget Restructuring

Analyze current spending to identify savings opportunities:

- Track all expenses for 30 days

- Eliminate or reduce discretionary spending

- Consider temporary lifestyle adjustments (dining out, subscriptions, entertainment)

- Redirect current rent increases into savings

Setting up a dedicated “down payment account” creates psychological commitment and tracks progress visibly.

Step 2: Mortgage Pre-Approval (Months 3-4)

Securing mortgage pre-approval before house hunting provides crucial advantages and prevents disappointment.

🎯 Why Pre-Approval Matters

The benefits of pre-approval include:

- Knowing your budget with certainty

- Strengthening offers in competitive situations

- Locking in rates for 90-120 days

- Identifying issues early with time to resolve them

- Demonstrating seriousness to sellers and realtors

📄 Documentation Requirements

Gather necessary documents before meeting with mortgage professionals:

- Employment verification: Recent pay stubs (2-3 months), employment letter

- Income proof: T4s, NOAs (Notice of Assessment) for past 2 years

- Asset verification: Bank statements showing down payment funds (90-day history)

- Identification: Government-issued photo ID, proof of residency

- Credit authorization: Permission for lender to pull credit report

Self-employed individuals require additional documentation. Review the complete guide to documentation requirements for self-employed mortgage approval for specific needs.

🔍 Choosing the Right Mortgage Professional

Work with experienced mortgage brokers who:

- Access multiple lenders (not just one bank)

- Understand first-time buyer programs

- Explain options clearly without pressure

- Provide rate comparisons and feature analysis

- Offer ongoing support through closing

Mortgage brokers typically cost nothing to buyers (lenders pay their fees) while providing access to better rates and terms than going directly to banks.

💡 Understanding Mortgage Options

Pre-approval discussions should cover:

- Fixed vs. variable rates: Stability versus potential savings

- Amortization periods: 25 vs. 30 years (first-time buyers)

- Payment frequency: Monthly, bi-weekly, accelerated options

- Prepayment privileges: Ability to pay down principal faster

- Portability features: Transferring mortgage if moving

For detailed comparisons, explore the mortgage rate guide covering fixed and variable options.

Step 3: House Hunting Strategy (Months 4-8)

With pre-approval secured, the exciting phase of property search begins. Strategic approach prevents emotional decisions and costly mistakes.

🏘️ Defining Must-Haves vs. Nice-to-Haves

Create prioritized lists:

Must-Haves:

- Location/commute requirements

- Minimum bedrooms/bathrooms

- Essential amenities (parking, laundry)

- Budget ceiling

- Property type (condo, townhouse, detached)

Nice-to-Haves:

- Upgraded finishes

- Additional space

- Specific views or features

- Proximity to specific amenities

- Outdoor space

This framework prevents “feature creep” that pushes budgets beyond comfortable limits.

🔎 Working with Real Estate Agents

Select buyer’s agents who:

- Specialize in your target neighborhoods

- Understand first-time buyer needs

- Provide honest assessments (not just positive spin)

- Have strong negotiation skills

- Offer market data and comparative analysis

Buyer’s agents are typically paid by sellers (through commission splits), making their services free to buyers while providing valuable expertise.

📍 Neighborhood Research

Evaluate areas beyond individual properties:

- Future development plans: Check municipal planning documents

- Transit accessibility: Current and planned infrastructure

- School ratings: Even for non-parents (affects resale)

- Crime statistics: Police service data

- Walkability scores: Access to services and amenities

- Property tax rates: Vary significantly across GTA municipalities

Spend time in neighborhoods at different times (weekdays, weekends, evenings) to get authentic feel.

🏠 Property Evaluation Criteria

Assess each property systematically:

- Building/property age and condition

- Recent renovations and quality

- Condo reserve fund health (for condos)

- Special assessments history

- Utility costs (request from seller)

- Resale potential (even if planning long-term stay)

For condos specifically, review status certificates carefully, examining reserve fund adequacy, pending litigation, and special assessment risks.

Step 4: Making Offers and Negotiation (Months 8-10)

Finding the right property triggers the critical offer and negotiation phase where preparation pays dividends.

📝 Offer Components

Competitive offers include:

- Purchase price: Based on comparables and market analysis

- Deposit amount: Typically 5% of purchase price

- Conditions: Financing, inspection, status certificate review

- Closing date: Flexibility can strengthen offers

- Inclusions/exclusions: Appliances, fixtures, chattels

- Irrevocable period: Time seller has to respond

In the 2026 buyer’s market, including reasonable conditions (especially inspection) is standard practice and protects buyers from costly surprises.

🔧 Home Inspection Importance

Professional home inspections (costing $400-600) identify:

- Structural issues

- Electrical and plumbing problems

- Roof condition and remaining lifespan

- HVAC system functionality

- Moisture, mold, or pest issues

- Code violations

Inspection reports provide negotiating leverage for price reductions or seller repairs. Never waive inspection conditions to save a few hundred dollars—it risks tens of thousands in hidden repairs.

💬 Negotiation Strategies

Effective negotiation in 2026’s market includes:

- Starting below asking (typically 5-10% in balanced markets)

- Using comparable sales data to justify offers

- Identifying seller motivations (quick close, specific dates, etc.)

- Remaining emotionally detached (don’t fall in love before owning)

- Being prepared to walk away (other opportunities exist)

Your realtor and mortgage broker form a team providing market intelligence and strategic advice throughout negotiations.

Step 5: Closing Process (Months 10-12)

Accepted offers trigger the closing process—a complex series of legal and financial steps culminating in ownership.

⚖️ Legal Representation

Hire real estate lawyers who:

- Conduct title searches ensuring clear ownership

- Review and explain all closing documents

- Calculate and arrange payment of land transfer taxes

- Register the property in your name

- Facilitate mortgage funding

- Provide title insurance

Legal fees typically range $1,500-2,500 including disbursements. Understanding legal fees for buying a house in Toronto helps budget accurately.

💰 Closing Costs Breakdown

Beyond down payment, budget for:

- Land transfer tax: Provincial (0.5-2% of purchase price) plus Toronto municipal (matching amounts for Toronto properties)

- Legal fees: $1,500-2,500

- Home inspection: $400-600

- Appraisal fee: $300-500 (if required by lender)

- Title insurance: $250-400

- Property tax adjustment: Prorated portion

- Condo fee adjustment: Prorated portion

- Utility connection fees: $100-300

- Moving costs: $500-2,000

First-time buyers receive land transfer tax rebates up to $4,000 (provincial) and $4,475 (Toronto municipal), significantly reducing closing costs.

Total closing costs typically represent 1.5-4% of purchase price. For a $600,000 property, budget $9,000-24,000 depending on first-time buyer status and specific circumstances.

🔑 Final Steps Before Possession

The final week before closing involves:

- Final walkthrough: Verify property condition matches offer

- Utility setup: Arrange hydro, gas, water, internet transfers

- Insurance activation: Home insurance must be active at closing

- Moving arrangements: Book movers or rental trucks

- Address changes: Notify employers, banks, government agencies

- Fund transfer: Ensure down payment and closing costs available

On closing day, lawyers exchange funds and documents. Once registered, you receive keys and officially become a homeowner! 🎉

Step 6: Post-Purchase Optimization

Homeownership begins at closing, but smart financial management continues.

🏡 Immediate Priorities

First 30 days:

- Change locks: Previous owners may have distributed keys

- Document property condition: Photos/videos for insurance purposes

- Create maintenance schedule: Regular upkeep prevents costly repairs

- Establish emergency fund: Target 1-3% of property value annually for repairs

- Review mortgage terms: Understand prepayment options and payment dates

📈 Long-Term Wealth Building

Maximize homeownership benefits through:

- Accelerated payments: Bi-weekly or weekly reduces amortization significantly

- Lump sum prepayments: Apply bonuses, tax refunds, or windfalls to principal

- Strategic renovations: Focus on value-adding improvements

- Regular maintenance: Prevents small issues becoming expensive problems

- Refinancing opportunities: Monitor rates for potential savings

Understanding home equity and how to use it opens future opportunities for investment, renovations, or debt consolidation.

🔄 Annual Financial Review

Each year, assess:

- Property value changes (online estimates, comparative sales)

- Mortgage balance reduction

- Potential refinancing benefits

- Maintenance and improvement needs

- Property tax assessment accuracy

- Insurance coverage adequacy

This discipline ensures homeownership remains a wealth-building tool rather than a financial burden.

Common Challenges and Solutions for Transitioning Renters

Challenge 1: Insufficient Down Payment

The Problem: Many renters struggle to accumulate the minimum 5-20% down payment plus closing costs.

Solutions:

- Extended timeline: Delay purchase 6-12 months for additional savings

- Gift from family: Parents or relatives can gift down payment funds (requires gift letter)

- Shared equity programs: Government or private programs providing down payment assistance

- Lower-priced properties: Consider condos or emerging neighborhoods

- Co-ownership: Purchase with partner, family member, or trusted friend

The First Home Savings Account provides tax advantages that accelerate down payment accumulation significantly.

Challenge 2: Credit Score Issues

The Problem: Past financial difficulties, limited credit history, or errors create qualification barriers.

Solutions:

- Credit repair timeline: Address issues 6-12 months before applying

- Secured credit cards: Build history with guaranteed approval products

- Become authorized user: Piggyback on family member’s good credit

- Dispute errors: Challenge inaccurate negative items

- Alternative lenders: B-lenders accept lower scores (higher rates)

Consistent on-time payments for 6-12 months can improve scores by 50-100 points, opening access to better mortgage terms.

Challenge 3: Employment Instability

The Problem: Recent job changes, contract work, or self-employment complicate income verification.

Solutions:

- Wait for stability: Lenders prefer 2+ years employment history

- Alternative documentation: Bank statement programs for self-employed

- Co-signer support: Employed family member strengthens application

- Larger down payment: 20%+ reduces lender risk and requirements

- Specialized brokers: Work with professionals experienced in non-traditional income

Self-employed individuals can explore bank statement loans as viable alternatives to traditional income verification.

Challenge 4: High Debt Levels

The Problem: Student loans, car payments, or credit card balances reduce borrowing capacity.

Solutions:

- Debt consolidation: Combine high-interest debts into lower-rate loans

- Aggressive paydown: Focus on eliminating debts before applying

- Debt service ratio optimization: Pay off small balances completely

- Income increase: Side hustles or raises improve debt-to-income ratios

- Co-borrower addition: Partner’s income offsets debt impact

Lenders calculate Total Debt Service (TDS) ratios—keeping all debt payments below 44% of gross income maximizes approval chances.

Challenge 5: Market Timing Anxiety

The Problem: Fear of buying at the “wrong time” or before potential price drops creates paralysis.

Solutions:

- Long-term perspective: 7+ year ownership horizons smooth short-term volatility

- Opportunity cost calculation: Compare continued rent payments to potential price changes

- Dollar-cost averaging mindset: Perfect timing is impossible; good timing is sufficient

- Focus on fundamentals: Buy properties you can afford in areas you want to live

- Professional guidance: Leverage realtor and mortgage broker market expertise

Historical GTA data shows that time in market beats timing the market—owners who purchased at market peaks still build substantial equity over 10+ years.

Financial Tools and Resources for GTA Renters

Online Calculators and Planning Tools

Rent vs. Buy Calculators: Input current rent, potential purchase price, down payment, and rates to compare long-term costs. Many banks and financial sites offer these tools free.

Mortgage Affordability Calculators: Determine maximum purchase price based on income, debts, and down payment. Conservative estimates prevent overextension.

Amortization Calculators: Visualize how different payment frequencies and prepayments reduce mortgage terms and interest costs.

Closing Cost Estimators: Calculate total funds needed beyond down payment, preventing last-minute surprises.

Government Programs and Incentives

First-Time Home Buyer Incentive: Shared equity mortgage with government (5-10% of purchase price), reducing monthly payments. Repayment required when selling or after 25 years.

Home Buyers’ Plan (HBP): Withdraw up to $35,000 from RRSPs tax-free for down payment. Repayment over 15 years required.

First Home Savings Account (FHSA): Contribute up to $8,000 annually (lifetime $40,000) with tax deductions. Withdrawals for first home purchase are tax-free.

Land Transfer Tax Rebates: First-time buyers receive up to $4,000 provincial rebate and $4,475 Toronto municipal rebate (for Toronto properties).

GST/HST New Housing Rebate: Partial rebate on new construction purchases under $450,000.

Professional Services

Mortgage Brokers: Access multiple lenders, provide rate comparisons, guide through application process. Services typically free to buyers.

Real Estate Agents: Market expertise, property access, negotiation skills, transaction management. Paid by sellers through commission splits.

Real Estate Lawyers: Legal protection, title searches, document review, closing coordination. Fees typically $1,500-2,500.

Home Inspectors: Property condition assessment, defect identification, maintenance recommendations. Fees typically $400-600.

Financial Planners: Holistic financial advice, budget optimization, long-term wealth strategies. Fees vary by service model.

Educational Resources

Workshops and Seminars: Many lenders, real estate boards, and community organizations offer free first-time buyer education sessions.

Online Courses: Comprehensive homebuying education covering all aspects of the transition process.

Government Resources: CMHC (Canada Mortgage and Housing Corporation) provides extensive free educational materials.

Real Estate Boards: TRREB (Toronto Regional Real Estate Board) publishes market reports, statistics, and buyer guides.

The Psychological Transition: From Renter to Owner Mindset

Shifting Financial Perspectives

The transition from renting to owning requires fundamental mindset changes:

From Short-Term to Long-Term Thinking: Renters often focus on monthly costs, while owners must consider 5-10 year horizons. This shift enables better financial decisions and reduces anxiety about short-term market fluctuations.

From Flexibility to Commitment: Renting offers mobility; ownership requires commitment to location and property. Successful owners embrace this stability as an asset rather than viewing it as limitation.

From Consumer to Investor: Rent is pure expense; mortgage payments are partially investment. This reframing transforms housing costs from necessary evil to wealth-building tool.

From Passive to Active Management: Landlords handle maintenance; owners must proactively manage property upkeep. This responsibility, while initially daunting, provides control and long-term cost savings.

Overcoming Common Fears

Fear of Market Downturns: Historical GTA data shows consistent long-term appreciation despite periodic corrections. Focusing on fundamentals (location, property condition, personal affordability) provides confidence regardless of short-term market movements.

Fear of Maintenance Costs: Building emergency funds (1-3% of property value annually) and conducting preventive maintenance minimizes surprise expenses. Many feared repairs prove less expensive than anticipated.

Fear of Being “House Poor”: Careful budgeting and conservative purchase prices prevent overextension. Buying below maximum approval amount provides financial cushion for unexpected expenses or income changes.

Fear of Making Wrong Choice: Perfect properties don’t exist. Successful owners recognize that good decisions beat perfect decisions—properties can be improved, but waiting indefinitely guarantees continued rent payments with zero equity building.

Building Owner Confidence

Education: Knowledge reduces anxiety. Understanding mortgage terms, market dynamics, and maintenance requirements transforms uncertainty into manageable challenges.

Professional Support: Assembling a team (mortgage broker, realtor, lawyer, inspector) provides expertise and guidance throughout the process.

Community Connection: Joining homeowner groups, online forums, or neighborhood associations provides peer support and practical advice.

Celebrating Milestones: Acknowledging progress (pre-approval, offer acceptance, closing, first year anniversary) reinforces positive decision-making and builds confidence.

Looking Ahead: The Future of GTA Homeownership

Market Predictions for Late 2026 and Beyond

Economic forecasters anticipate several trends affecting GTA homeownership:

Gradual Price Appreciation: Following first-half 2026 softness, modest price increases (2-4% annually) are expected as confidence returns and inventory normalizes.

Interest Rate Stabilization: Mortgage rates likely remain in the 4.5-6.5% range through 2027, providing predictability for planning.

Continued First-Time Buyer Focus: Government policies and lender programs increasingly target first-time buyers, improving accessibility.

Rental Market Pressure: Immigration and population growth sustain rental demand, keeping upward pressure on rents and motivating ownership transitions.

Technology Integration: Digital mortgage applications, virtual property tours, and online closing processes continue streamlining the buying experience.

Emerging Opportunities

Pre-Construction Condos: Developers offering incentives and flexible payment structures to attract buyers in slower market conditions.

Emerging Neighborhoods: Areas with planned transit expansion or development offer value opportunities for patient buyers.

Multigenerational Housing: Growing interest in properties accommodating extended families, creating niche market opportunities.

Energy-Efficient Properties: Green building features increasingly valued, offering long-term utility savings and higher resale values.

Alternative Ownership Models: Co-ownership, shared equity, and rent-to-own programs expanding access for non-traditional buyers.

Positioning for Success

Renters considering the switch to ownership in 2026 and beyond should:

✅ Start planning early: 12-18 month preparation timelines yield best results

✅ Build financial foundation: Focus on credit, savings, and debt management

✅ Stay informed: Monitor market conditions and policy changes

✅ Seek professional guidance: Leverage expert knowledge and experience

✅ Maintain flexibility: Be prepared to adjust timelines or targets based on circumstances

✅ Think long-term: Focus on 7-10 year horizons rather than short-term market timing

The transition from renting to owning represents one of life’s most significant financial decisions. With proper preparation, realistic expectations, and professional support, GTA renters can successfully navigate this journey in 2026’s favorable market conditions.

Conclusion: Taking the First Step Toward Homeownership

Understanding why GTA renters are switching to ownership in 2026 reveals a compelling combination of economic opportunity and personal financial strategy. The current market conditions—characterized by increased inventory, stabilizing prices, and sustained rental cost pressures—create a unique window for prepared renters to make the transition.

The cost comparison clearly demonstrates that while ownership involves higher upfront costs and monthly payments, the equity building and long-term wealth accumulation significantly outweigh continued rent payments over 5-7 year periods. For renters planning to remain in the GTA long-term, ownership increasingly represents the financially prudent choice.

The transition roadmap outlined in this guide provides a clear, actionable path from initial financial assessment through closing and beyond. While the journey requires commitment, discipline, and patience, thousands of GTA renters successfully navigate this process annually, building wealth and securing housing stability for themselves and their families.

Your Next Steps

If you’re ready to explore the transition from renting to ownership:

- Assess your financial readiness using the criteria outlined in Step 1 of the roadmap

- Connect with a mortgage professional to understand your borrowing capacity and options

- Create a realistic timeline based on your current situation and goals

- Begin implementing the savings strategies that align with your circumstances

- Educate yourself continuously about the GTA market and homeownership requirements

If you’re not quite ready but want to position yourself for future success:

- Focus on credit improvement and debt reduction over the next 6-12 months

- Maximize your savings through FHSA, RRSP, and TFSA contributions

- Research neighborhoods and property types to refine your preferences

- Build your professional team by interviewing mortgage brokers and realtors

- Set specific milestones with target dates for achieving readiness

The decision to switch from renting to ownership is deeply personal and depends on individual circumstances, goals, and risk tolerance. However, for many GTA renters in 2026, the combination of favorable market conditions, improved mortgage accessibility, and the long-term financial benefits of ownership make this an opportune time to seriously evaluate the transition.

Remember that homeownership is a journey, not a destination. The path from renter to owner may take 6-18 months of preparation, but the financial security, wealth building, and personal satisfaction that result make the effort worthwhile for those ready to take the leap.

Ready to start your journey from renting to owning? Connect with experienced mortgage professionals who can provide personalized guidance based on your unique situation. The first conversation costs nothing but could be the catalyst that transforms your housing future and builds lasting wealth for you and your family.