March 9, 2026

Variable Private Mortgages in Toronto: Why They’re Gaining Traction Amid 2026 Rate Stability

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

As variable rates claim roughly 26% of Toronto’s mortgage market share in early 2026, a quiet shift is underway — and private lenders are at the center of it. Variable Private Mortgages in Toronto: Why They’re Gaining Traction Amid 2026 Rate Stability is no longer just a niche conversation. It’s a mainstream financial strategy for borrowers who want savings, flexibility, and access to funding that traditional banks simply won’t provide.

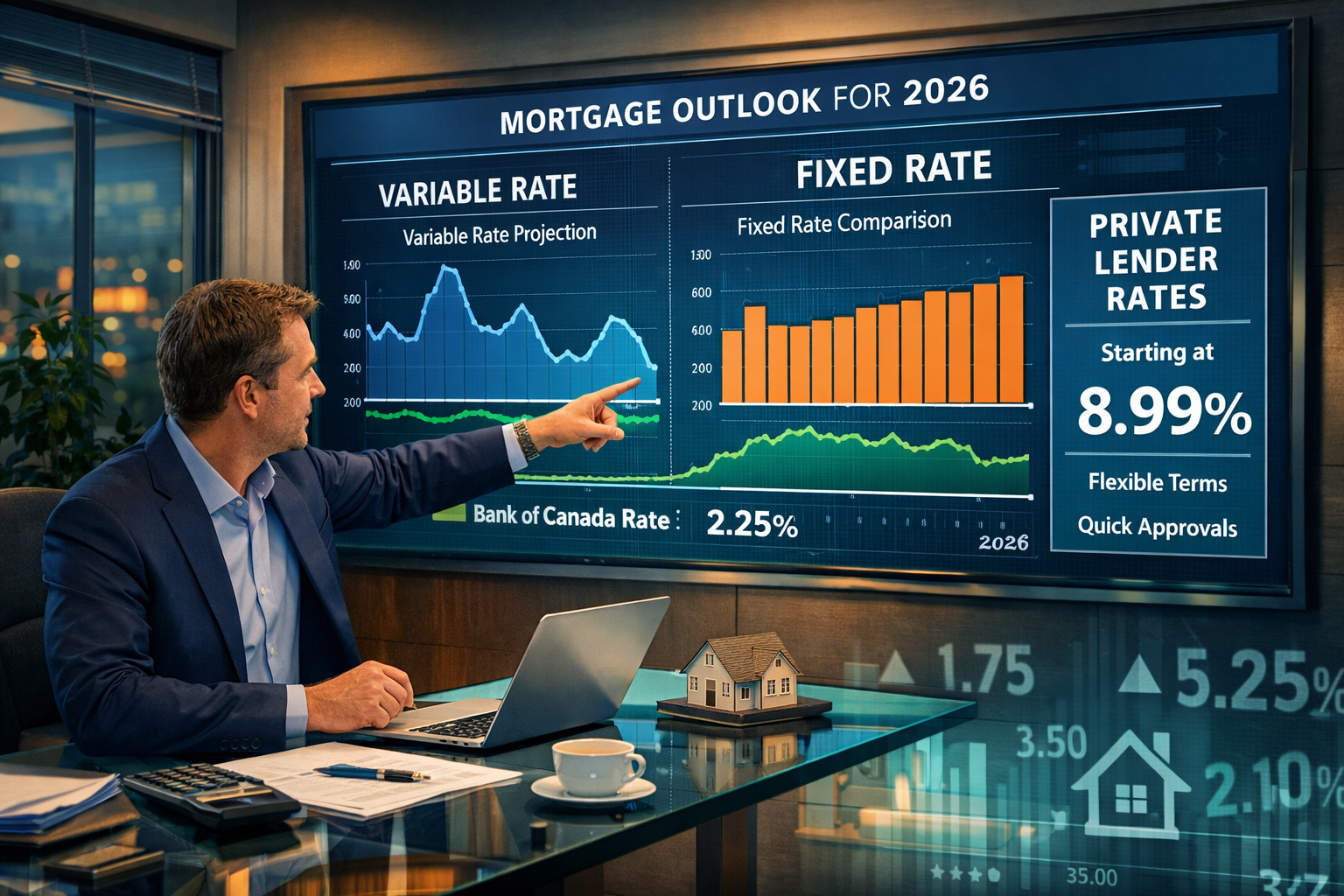

With the Bank of Canada holding its policy rate at 2.25% and the prime rate sitting at 4.45%, the conditions for variable-rate products — including private mortgage options — have rarely looked this favorable [9]. Whether a borrower is self-employed, carrying bruised credit, or navigating a tricky renewal, private variable mortgages are becoming a serious tool in the Toronto market.

Key Takeaways 📌

- The Bank of Canada held its rate at 2.25% in January 2026, creating a stable environment for variable mortgage products [9]

- Variable private mortgages in Toronto are seeing renewed demand, with professionals calling 2026 a “rare opportunity” for variable-rate borrowers [1]

- Private variable rates start around 8.99% for high-equity Toronto cases, while bank variable rates sit between 3.35%–3.65% [1]

- Fixed 5-year rates (best at 3.64%) cost approximately $5,628 more annually than comparable variable options [1]

- Private lending is projected to grow to ~20% of Ontario mortgages, driven by renewals and tightening bank criteria

Understanding the 2026 Rate Landscape for Toronto Borrowers

To understand why Variable Private Mortgages in Toronto: Why They’re Gaining Traction Amid 2026 Rate Stability matters right now, it helps to look at the macro picture.

Bank of Canada’s Steady Hand 🏦

On January 28, 2026, the Bank of Canada officially held its overnight rate at 2.25%, keeping the prime rate at 4.45% [9]. Analysts at Nesto forecast no easing moves in 2026, with bond markets potentially pricing in hikes by year-end [3][4]. True North Mortgage’s March 2026 outlook similarly holds the BoC steady at 2.25%, acknowledging inflation and trade risks from U.S. tariffs but maintaining a stable variable-rate environment [7].

This is a significant shift from the volatility of 2022–2024. For borrowers who were burned by rapid rate hikes, the current plateau feels like a breath of fresh air. Mortgage experts are calling it a “renaissance” for variable rates after years of fixed-rate dominance [1][10].

💬 “2026 represents a rare opportunity for variable-rate borrowers in Toronto — minimal spread, BoC stability, and convertibility options make it hard to ignore.” — Mortgage Experts, EverythingMortgages.ca [1]

The Toronto Housing Market Context 🏘️

The GTA housing market stabilized in February 2026, with benchmark prices settling at $938,800 — down 7.9% year-over-year [2]. This buyer-friendly environment rewards borrowers who can move quickly and flexibly. Variable private mortgages, with their faster approval timelines and looser qualification criteria, are well-suited to capitalize on deals in a cooling market.

For a deeper look at how rate forecasts are shaping borrower decisions, see this analysis on how 2026 mortgage rate forecasts impact self-employed homebuyers.

Variable vs. Fixed: What the Numbers Actually Say

The debate between fixed and variable mortgages is never just philosophical — it comes down to dollars and cents.

The Cost Comparison 💰

| Mortgage Type | Best Rate (March 2026) | Annual Cost Difference |

|---|---|---|

| 5-Year Fixed | 3.64% | Baseline |

| Variable (Bank) | 3.34%–3.35% | Save ~$5,628/year [1] |

| Variable (Private) | 8.99%+ (high-equity) | Higher, but accessible |

For borrowers who qualify at traditional banks, the math strongly favors variable rates right now. The spread between fixed and variable is narrow enough that even modest rate stability delivers meaningful savings [1].

For those who don’t qualify at banks — due to self-employment income, credit challenges, or non-standard property types — private variable mortgages offer a pathway that didn’t exist at this scale just a few years ago.

To understand the mechanics of how these rate types work, the comprehensive guide to fixed vs. variable rates is an excellent starting point. It’s also worth understanding trigger rates in variable mortgages before committing to a variable product.

Why Fixed Rates Aren’t Always the Safe Choice

Many borrowers assume fixed rates are “safer.” But in a stable rate environment, that safety comes at a premium. Locking into a 3.64% fixed rate while variable options hover at 3.34%–3.35% means paying for certainty that may not be necessary [1]. The mortgage rate guide covering fixed and variable options breaks down when each product makes sense.

Why Variable Private Mortgages in Toronto Are Gaining Traction Amid 2026 Rate Stability

The growth of private lending isn’t just about borrowers with bad credit. That narrative is outdated. Experts Ryan MacNeil and Neal Andreino, speaking on the Canadian Private Lenders Podcast in February 2026, predicted that private lending could grow to ~20% of Ontario mortgages, driven primarily by renewals and market volatility — not just credit issues.

Who Is Turning to Private Variable Mortgages? 👥

1. Renewal Shock Borrowers Thousands of Toronto homeowners are hitting mortgage renewals in 2026 after locking in at ultra-low pandemic-era rates. Banks are tightening their renewal criteria, pushing many borrowers toward private options. The impact of 2026 mortgage renewals on first-time buyers and refinancers explores this challenge in depth.

2. Self-Employed Professionals Freelancers, contractors, and business owners often can’t satisfy traditional income verification requirements. Private lenders use equity-based underwriting, making variable private mortgages accessible where banks say no. Learn more in the ultimate guide to securing a mortgage for self-employed Canadians.

3. Credit-Challenged Borrowers Those recovering from a consumer proposal or past credit events can use private variable mortgages as a bridge strategy — accessing funds now while rebuilding creditworthiness for a bank mortgage later. Understanding getting a mortgage after a consumer proposal is critical for this group.

4. Real Estate Investors Investors moving quickly in Toronto’s buyer’s market need fast approvals. Private variable mortgages can close in days, not weeks.

The FSRA Factor 🔍

The Financial Services Regulatory Authority of Ontario (FSRA) has made private mortgages a top supervision priority in its 2025–2026 plan, acknowledging their growing role post-2024. While delinquency rates ticked up to 0.20% in 2024, FSRA’s stance is one of heightened oversight — not restriction. This regulatory attention actually signals legitimacy and growing market importance.

Borrowers considering private options should also review the landscape of private loan lenders in Ontario and understand how banks compare to alternative private lenders.

Key Benefits of Variable Private Mortgages in 2026 ✅

- Faster approvals — ideal for competitive Toronto deals

- Flexible qualification — equity-focused, not income-focused

- Rate environment alignment — stable BoC rate reduces payment shock risk

- Convertibility options — many private products allow switching to fixed if rates move

- Bridge-to-bank strategy — use private now, qualify for bank rates later

The Risks to Know ⚠️

Variable private mortgages are not without downsides:

- Higher rates — private rates start at 8.99% vs. 3.35% at banks [1]

- Shorter terms — typically 1-year terms require renewal planning

- Lender fees — arrangement and broker fees add to the total cost

- Rate movement risk — if BoC raises rates late 2026, variable payments increase [4]

How to Approach Variable Private Mortgages Strategically in 2026

Given the current environment, here’s a practical framework for Toronto borrowers:

Step 1: Assess Your Qualification Gap

Determine why traditional banks are declining or limiting your options. Is it income documentation, credit score, or property type? This defines whether a private variable mortgage is a short-term bridge or a longer-term solution.

Step 2: Compare Total Cost of Borrowing

Don’t just look at the interest rate. Factor in lender fees, broker fees, and renewal costs. A private variable mortgage at 8.99% with a clear 12-month exit plan may cost less overall than a missed opportunity in Toronto’s buyer’s market [2].

Step 3: Prioritize Convertibility

Experts at EverythingMortgages.ca specifically recommend choosing private variable products with convertibility clauses — the ability to lock into a fixed rate if economic conditions shift [1]. With bond markets potentially pricing in hikes by year-end [4], this optionality has real value.

Step 4: Plan the Exit Strategy

Private mortgages work best as part of a plan. Whether the goal is rebuilding credit, documenting income, or waiting for a property refinance, having a 12–24 month roadmap to conventional lending is essential.

Conclusion: Is a Variable Private Mortgage Right for You in 2026?

The story of Variable Private Mortgages in Toronto: Why They’re Gaining Traction Amid 2026 Rate Stability is ultimately a story about access, strategy, and timing. The Bank of Canada’s steady hand at 2.25% has created a window where variable-rate products carry less risk than they have in years [9]. Private lenders are filling a real gap for borrowers the traditional system is leaving behind.

For the right borrower — someone with equity, a clear exit plan, and a need for fast or flexible financing — a variable private mortgage in Toronto in 2026 isn’t a last resort. It’s a calculated move.

Actionable Next Steps 🚀

- Get a mortgage assessment from a licensed broker who specializes in private lending

- Review your credit and income documentation to understand your qualification gap

- Compare total borrowing costs — not just the rate — across private and bank options

- Ask specifically about convertibility clauses in any variable private product

- Set a 12-month review date to assess refinancing into conventional lending

- Explore current rates at Everything Mortgages rates page to benchmark your options

The market won’t stay this stable forever. Borrowers who act with clarity and a solid plan in 2026 are positioning themselves well — regardless of what rates do next.

References

[1] Fixed Vs Variable Rates For Toronto First Time Buyers Refinancing In 2026 Which Saves More – https://everythingmortgages.ca/blog/fixed-vs-variable-rates-for-toronto-first-time-buyers-refinancing-in-2026-which-saves-more/ [2] Toronto Housing Market – https://wowa.ca/toronto-housing-market [3] Bank Of Canada Interest Rate Schedule – https://www.nesto.ca/mortgage-basics/bank-of-canada-interest-rate-schedule/ [4] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/ [7] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast [9] Fad Press Release 2026 01 28 – https://www.bankofcanada.ca/2026/01/fad-press-release-2026-01-28/ [10] Gta Mortgage Trends Variable Rates Gain Traction In 2026 – https://www.realestategtatoday.ca/index.php/2026/03/02/gta-mortgage-trends-variable-rates-gain-traction-in-2026/