March 10, 2026

BoC Rate Hold at 2.25% Through 2026: How Self-Employed Toronto Entrepreneurs Can Lock Sub-3.5% Variable Rates Now

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

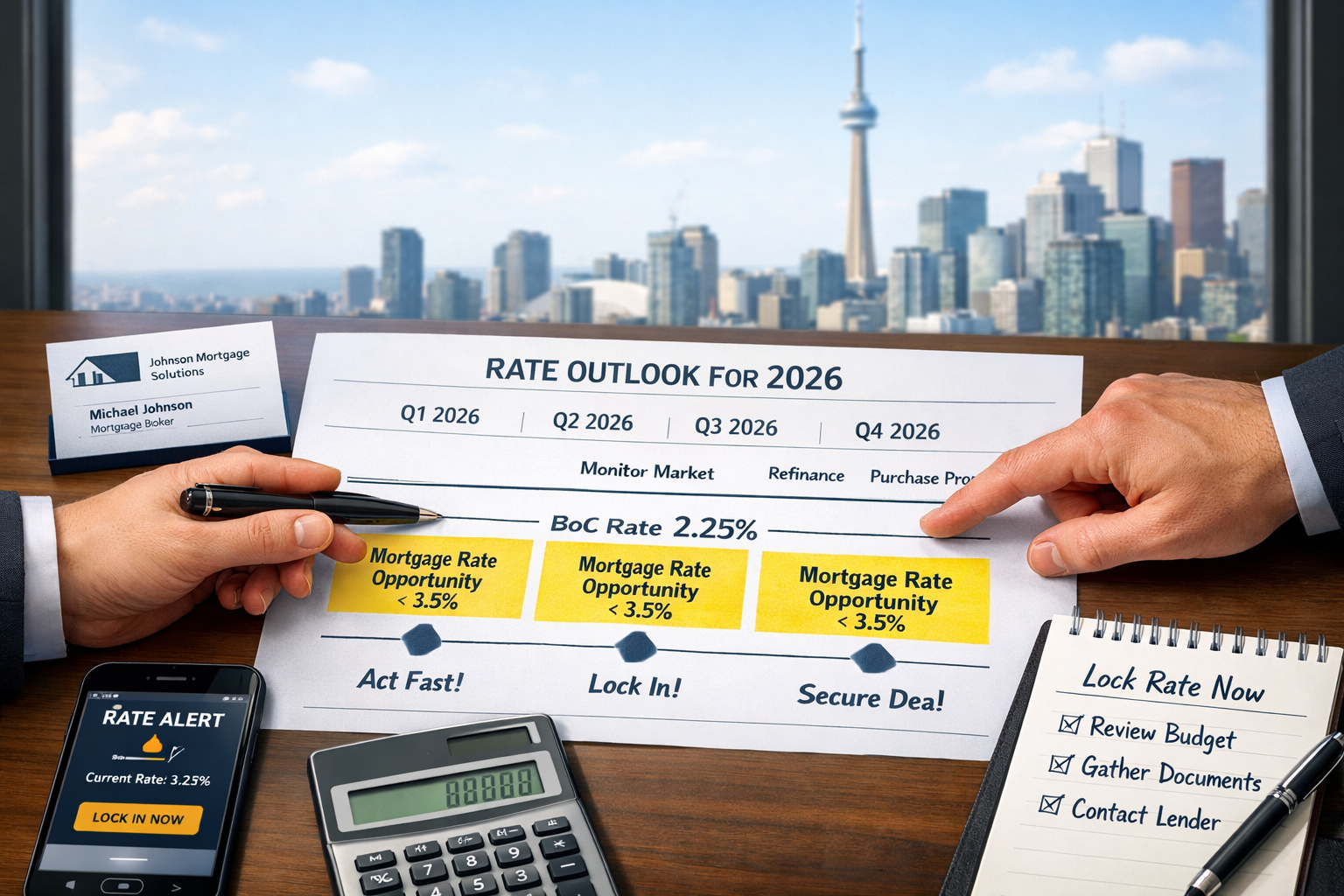

The Bank of Canada has signaled a new era of monetary policy stability that self-employed Toronto entrepreneurs cannot afford to ignore. With the overnight policy rate held steady at 2.25% since December 2025, and analysts forecasting this rate to remain unchanged throughout 2026, a unique window of opportunity has opened for business owners to secure exceptionally competitive variable mortgage rates below 3.5%[1].

For self-employed professionals—from IT consultants and contractors to doctors and creative entrepreneurs—this stable rate environment presents both opportunity and challenge. While prime rate stability at 4.45% creates predictable borrowing costs, traditional lenders continue to impose strict qualification hurdles that can lock out even successful business owners. Understanding how to navigate the BoC rate hold at 2.25% through 2026 and leverage alternative lending solutions can mean the difference between securing a sub-3.5% variable rate or settling for significantly higher costs.

Key Takeaways

✅ Rate Stability Confirmed: The Bank of Canada maintained its 2.25% policy rate in January 2026, with the next decision scheduled for March 18, 2026, and analysts expecting no changes throughout the year[1][2]

✅ Sub-3.5% Rates Are Achievable: Self-employed borrowers can access variable rates between 3.25% and 3.45% through B-lenders and alternative mortgage solutions despite stricter A-lender qualification requirements

✅ Documentation Is Key: Bank statement mortgages, stated income programs, and alternative income verification methods enable entrepreneurs to qualify without traditional T1 Generals or Notice of Assessments

✅ Timing Matters: With inflation at 2.4% and core measures declining, locking competitive rates now protects against potential rate increases if economic conditions shift unexpectedly[1]

✅ Broker Expertise Essential: Mortgage brokers specializing in self-employed clients can navigate B-lender networks and negotiate rate discounts unavailable through direct lender applications

Understanding the BoC Rate Hold at 2.25% Through 2026

The Bank of Canada’s decision to maintain its overnight policy rate at 2.25% represents a significant shift from the aggressive rate-cutting cycle that dominated 2024 and early 2025. On January 28, 2026, Governor Tiff Macklem and the Governing Council announced the rate would remain unchanged, citing inflation levels that have stabilized near the 2% target while acknowledging ongoing economic uncertainties[1].

What the Current Rate Environment Means

The current 2.25% policy rate translates to a prime rate of 4.45% at most Canadian financial institutions. This creates a foundation for variable mortgage rates that can range from prime minus 0.95% (3.50%) to prime minus 1.20% (3.25%) for well-qualified borrowers. For self-employed entrepreneurs, understanding this relationship is crucial when evaluating mortgage offers.

December 2025 inflation data showed consumer price index (CPI) growth at 2.4%, slightly above the Bank’s 2% target but within the acceptable 1-3% control range. More importantly, core inflation measures—which exclude volatile food and energy prices—have declined from 3% in October 2025 to approximately 2.5% in December[1]. This downward trend in core inflation supports the case for continued rate stability.

Economic Factors Supporting Rate Stability

Several key economic indicators suggest the BoC rate hold at 2.25% through 2026 is the most probable scenario:

Unemployment remains elevated: Despite recent employment gains, Canada’s jobless rate sits at 6.8%, with few businesses planning to hire in the near term[1]. This labor market slack reduces wage pressure and inflation risk.

Modest growth projections: The Bank of Canada forecasts economic growth of just 1.1% in 2026, as the country adjusts to slower population growth and ongoing US trade policy uncertainty[1]. This subdued growth outlook doesn’t warrant stimulative rate cuts.

Trade policy uncertainty: Tariff threats and the upcoming review of the Canada-US-Mexico Agreement create significant policy uncertainty that could warrant monetary adjustments in either direction[3]. The Bank is maintaining flexibility to respond to developments.

According to analyst forecasts, the March 18, 2026 rate decision—the first scheduled announcement of the year—will almost certainly maintain the 2.25% rate[2][3]. Subsequent decisions in April, June, July, September, October, and December 2026 are also expected to hold steady unless significant economic shocks emerge.

Why Self-Employed Borrowers Should Act Now

For Toronto entrepreneurs, this stable rate environment creates a strategic opportunity that may not last indefinitely. While further rate cuts are possible in the second half of 2026 if core inflation continues declining and economic weakness becomes more apparent[3], several factors make immediate action advisable:

Qualification standards remain tight: Lenders are maintaining conservative underwriting standards despite rate stability, and any economic deterioration could trigger even stricter requirements

B-lender capacity is finite: Alternative lenders offering competitive rates to self-employed borrowers have limited capital allocation, and popular programs can close to new applications

Real estate market timing: Toronto’s housing market shows signs of recovery, and delaying mortgage approval could mean missing attractive property opportunities

Rate protection: Locking a sub-3.5% variable rate now provides downside protection if unexpected inflation spikes force the BoC to reverse course

Understanding current self-employed mortgage rates in Toronto helps entrepreneurs benchmark available options against the broader rate environment.

How Self-Employed Toronto Entrepreneurs Can Access Sub-3.5% Variable Rates

While the BoC rate hold at 2.25% through 2026 creates a favorable foundation for low mortgage rates, self-employed borrowers face unique qualification challenges that prevent many from accessing the best rates advertised by traditional A-lenders. However, strategic approaches through B-lenders, alternative documentation programs, and specialized mortgage brokers can unlock variable rates between 3.25% and 3.45%—well below the 3.5% threshold.

The Self-Employed Qualification Challenge

Traditional A-lenders (major banks and credit unions) typically require self-employed borrowers to provide:

- Two years of complete tax returns (T1 Generals and Notice of Assessments)

- Two years of business financial statements (for incorporated businesses)

- Consistent or increasing income demonstrated across both years

- Debt service ratios calculated using net income after business expenses

This creates a significant problem: many successful entrepreneurs legitimately write off substantial business expenses to minimize tax liability, which dramatically reduces the “income” lenders use for qualification calculations. A consultant earning $150,000 in gross revenue might show only $65,000 in net income after legitimate deductions—insufficient to qualify for the mortgage needed to purchase a Toronto property.

B-Lender Solutions for Sub-3.5% Rates

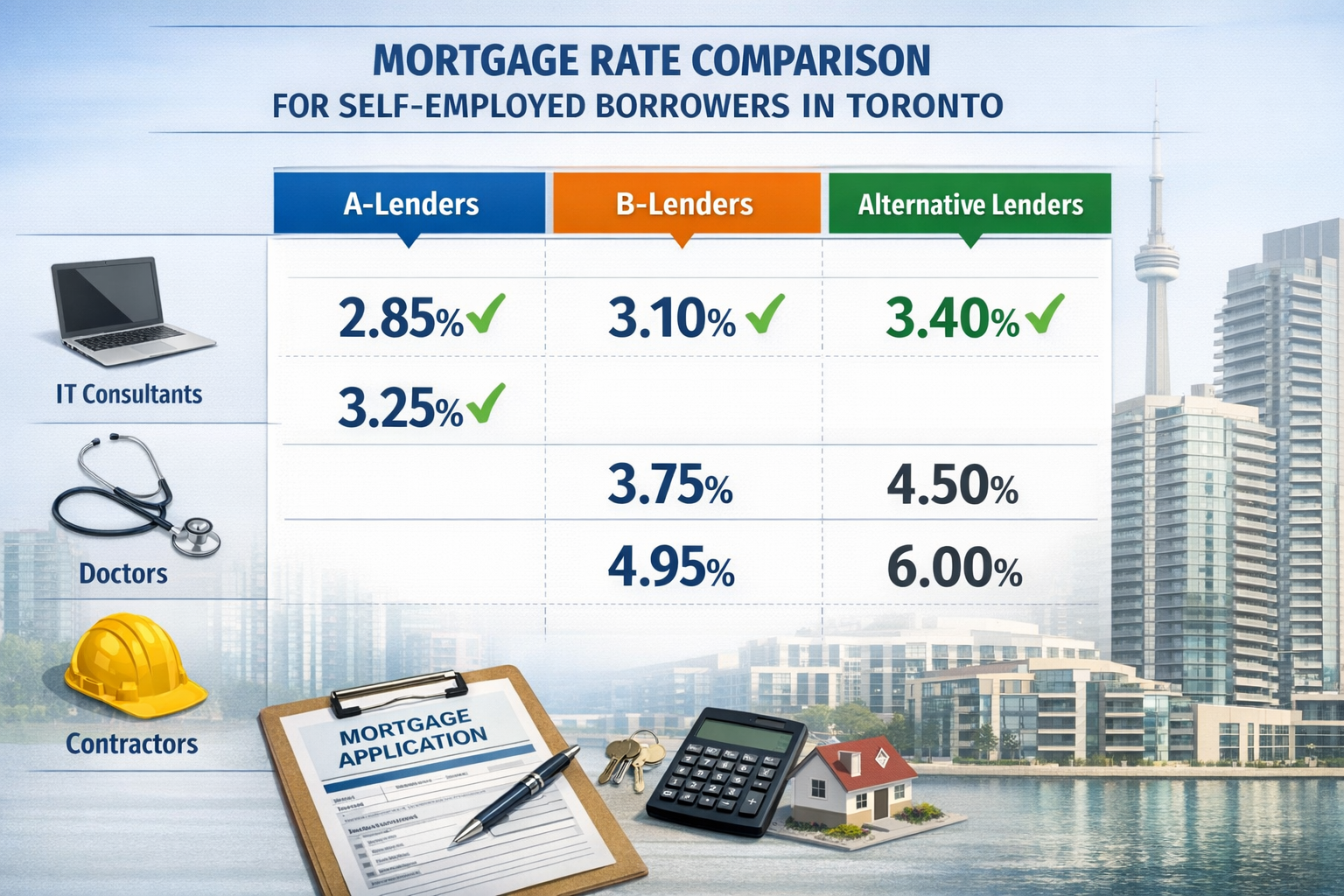

B-lenders—also called alternative or non-prime lenders—fill this critical gap by offering more flexible qualification criteria while maintaining competitive rates. In the current stable rate environment, top-tier B-lenders are offering variable rates as low as 3.25% to 3.45% to self-employed borrowers who meet specific criteria:

| Lender Type | Variable Rate Range | Income Verification | Credit Score Required | Down Payment |

|---|---|---|---|---|

| A-Lenders | 3.50% – 3.75% | Full tax documentation | 680+ | 20%+ |

| B-Lenders | 3.25% – 3.65% | Bank statements or stated income | 600+ | 20%+ |

| Alternative Lenders | 3.45% – 3.95% | Self-declared income | 550+ | 25%+ |

The key advantage of bank statement mortgages for self-employed borrowers is that lenders analyze gross deposits rather than net income after deductions. This approach recognizes the true earning capacity of business owners.

Alternative Income Verification Methods

Several documentation strategies enable self-employed Toronto entrepreneurs to qualify for sub-3.5% variable rates:

📊 Bank Statement Programs: Lenders review 12-24 months of business bank statements and calculate average monthly deposits. They typically apply a conservative percentage (65-75%) to account for business expenses, but this still results in higher qualifying income than tax returns show.

📝 Stated Income Mortgages: For borrowers with strong credit (typically 680+) and substantial down payments (35%+), some lenders accept a signed declaration of income without extensive documentation. Rates range from 3.45% to 3.75% depending on the loan-to-value ratio.

💼 Industry-Specific Programs: Certain professions receive preferential treatment. Self-employed doctors, dentists, and other medical professionals can access specialized programs through innovative mortgage solutions for self-employed Canadians that recognize professional designation as a proxy for income stability.

📈 Asset-Based Qualification: Entrepreneurs with significant investment portfolios, business assets, or real estate holdings can leverage these assets to support income claims and secure better rates.

Broker Strategies to Maximize Rate Discounts

Working with a mortgage broker who specializes in self-employed clients provides several advantages in securing rates below 3.5%:

Lender Network Access: Brokers maintain relationships with 20-40 lenders, including B-lenders and private institutions that don’t accept direct applications from consumers. This access is essential for rate shopping.

Rate Negotiation: Experienced brokers can negotiate rate discounts of 0.10% to 0.25% by leveraging volume relationships with lenders or by structuring applications to meet specific lender promotions.

Application Optimization: Brokers understand exactly how each lender calculates income for self-employed borrowers and can structure documentation to maximize qualifying income while maintaining accuracy.

Timing Strategies: Brokers monitor lender rate changes (which can occur weekly) and can time application submissions to capture the best available rates before increases.

For entrepreneurs comparing options, reviewing current best self-employed mortgage rates in Toronto provides insight into the fixed versus variable decision in the context of the BoC rate hold.

Qualification Requirements for Sub-3.5% Rates

To access the most competitive variable rates below 3.5%, self-employed Toronto entrepreneurs should aim to meet these benchmarks:

✅ Credit score of 650+ (680+ for best rates)

✅ Down payment of 20%+ (35%+ for stated income programs)

✅ Business operating for 2+ years (some lenders accept 1 year)

✅ Gross revenue supporting debt service ratios under 42% TDS

✅ Clean credit history with no recent delinquencies or collections

✅ Stable or growing business revenue demonstrated through bank statements

Borrowers who fall slightly short of these criteria can still access rates in the 3.5% to 3.95% range through more flexible alternative lenders, which remains competitive compared to historical averages.

Strategic Considerations for Locking Rates in 2026

Understanding the BoC rate hold at 2.25% through 2026 is only the first step—self-employed Toronto entrepreneurs must also make strategic decisions about when to lock rates, variable versus fixed options, and how to position themselves for optimal approval.

Variable vs. Fixed in a Stable Rate Environment

The current rate stability creates an interesting decision point for borrowers. With the policy rate expected to remain at 2.25% throughout 2026, variable rates offer several advantages:

Lower starting rates: Variable rates currently sit 0.40% to 0.80% below comparable 5-year fixed rates, translating to significant monthly savings on Toronto’s high property values.

Flexibility: Variable rate mortgages typically offer lower penalties for early repayment or refinancing, which matters for entrepreneurs whose business circumstances may change.

Potential for further decreases: If core inflation continues declining and economic weakness emerges in late 2026, the BoC could resume rate cuts, providing additional savings[3].

However, fixed rates provide payment certainty and protection against unexpected rate increases if inflation resurges or US trade policy creates economic instability. For a comprehensive analysis, see our guide on 5-year fixed vs. variable options for self-employed borrowers.

Timing Your Rate Lock

Several factors should influence when self-employed entrepreneurs lock their mortgage rates:

📅 Seasonal Rate Patterns: Lenders often offer promotional rates during slower periods (typically January-February and September-October) to stimulate volume. Spring and early summer tend to see rate increases as demand peaks.

📊 Economic Data Releases: Major inflation reports and employment data can trigger rate adjustments. Monitoring the Bank of Canada’s schedule for key economic releases helps time applications strategically.

🏠 Property Purchase Timeline: For active home shoppers, securing a rate hold (typically 90-120 days) before finding a property ensures rate protection during the search process.

💡 Lender Capacity: B-lenders and alternative lenders have finite capital to deploy. When popular programs approach capacity limits, they increase rates or tighten qualification criteria. Early application can capture better terms.

Maximizing Qualification Strength

Self-employed borrowers can take specific actions to improve their qualification profile and access the lowest available rates:

1. Optimize Business Structure: Incorporated businesses have more flexibility in income verification. Working with an accountant to structure compensation (salary vs. dividends vs. retained earnings) can improve mortgage qualification without increasing tax burden.

2. Build Strong Bank Statement History: Maintaining consistent deposit patterns and avoiding large irregular transactions creates cleaner documentation for lenders reviewing bank statements.

3. Reduce Personal Debt: Paying down credit cards, lines of credit, and other consumer debt improves debt service ratios and can unlock better rate tiers.

4. Increase Down Payment: Moving from 20% to 25% or 35% down payment opens access to better lender programs and lower rates. Entrepreneurs with business savings or investment portfolios should consider allocating more capital to down payment.

5. Address Credit Issues Proactively: Resolving collections, paying down high-utilization credit accounts, and correcting credit report errors before applying can improve credit scores by 20-40 points in 60-90 days.

For detailed strategies, review The Ultimate Guide to Securing a Mortgage for Self-Employed Canadians.

Understanding Rate Hold Agreements

When working with a broker to secure a sub-3.5% variable rate, understanding rate hold agreements is essential:

- Standard hold period: 90-120 days from application approval

- Rate guarantee: If rates decrease during the hold period, borrowers receive the lower rate; if rates increase, the original rate is honored

- Extension options: Some lenders offer 30-day extensions if property closing is delayed

- Application requirements: Rate holds typically require complete application submission with all supporting documentation

Preparing for Potential Rate Changes

While the BoC rate hold at 2.25% through 2026 is the consensus forecast, self-employed borrowers should prepare for alternative scenarios:

If rates decrease: Variable rate holders benefit automatically as prime rate adjusts downward. Fixed rate holders may consider refinancing if the savings justify penalty costs.

If rates increase: Variable rate holders face higher payments but can typically convert to fixed rates (at current market rates) without penalty. Maintaining financial cushion for potential payment increases is prudent.

If economic shock occurs: Major disruptions (trade war escalation, financial crisis, etc.) could prompt emergency rate adjustments in either direction. Maintaining strong business cash flow and personal savings provides resilience.

Entrepreneurs concerned about rate volatility should explore mortgage refinancing and switching options to understand their flexibility.

Tax Planning Considerations

Self-employed borrowers should coordinate mortgage planning with tax strategy:

📋 Income Reporting Balance: While minimizing taxable income reduces tax liability, it also reduces mortgage qualification capacity. Finding the optimal balance requires coordination between mortgage broker and accountant.

🏡 Mortgage Interest Deductibility: Entrepreneurs using home equity to fund business operations may be able to deduct mortgage interest as a business expense, effectively reducing the true cost of borrowing.

💰 RRSP Strategies: First-time homebuyers can leverage the Home Buyers’ Plan to withdraw up to $35,000 from RRSPs for down payment, improving qualification ratios.

Working with professionals who understand both tax optimization for self-employed Canadians and mortgage qualification creates synergies that maximize both tax efficiency and borrowing capacity.

Actionable Steps to Lock Your Sub-3.5% Variable Rate

For self-employed Toronto entrepreneurs ready to capitalize on the BoC rate hold at 2.25% through 2026 and secure sub-3.5% variable rates, following a structured approach maximizes success probability:

Step 1: Assess Your Current Financial Position (Week 1)

Begin by gathering comprehensive documentation of your financial situation:

- Last 12-24 months of business bank statements (personal and business accounts)

- Most recent tax returns (even if not using for qualification)

- Current credit report from Equifax or TransUnion

- List of all debts with current balances and monthly payments

- Down payment sources with account statements showing funds

Calculate your approximate debt service ratios using gross business revenue rather than net income. This provides a realistic picture of qualification capacity under alternative documentation programs.

Step 2: Connect with a Self-Employed Mortgage Specialist (Week 1-2)

Not all mortgage brokers have equal expertise with self-employed clients. Seek brokers who:

✅ Specialize in self-employed and business-for-self clients

✅ Have established relationships with B-lenders and alternative lenders

✅ Can provide recent examples of sub-3.5% rate approvals for similar clients

✅ Understand your specific industry and income structure

✅ Offer comprehensive pre-qualification analysis before formal application

During initial consultation, discuss your business structure, income documentation options, and rate expectations. A qualified broker should provide honest assessment of achievable rates based on your profile.

Step 3: Optimize Your Application Profile (Week 2-4)

Based on broker feedback, take targeted actions to strengthen your application:

For Credit Score Improvement:

- Pay down credit card balances below 30% of limits

- Resolve any outstanding collections or judgments

- Avoid new credit applications during the mortgage process

- Correct any errors on credit reports

For Income Documentation:

- Organize bank statements chronologically with clear labeling

- Prepare explanations for any irregular large deposits or withdrawals

- Gather contracts or invoices demonstrating ongoing business activity

- Obtain accountant letter confirming business operation and revenue if helpful

For Down Payment:

- Consolidate funds into clearly traceable accounts

- Prepare gift letters if receiving family assistance

- Document source of funds for any recent large deposits

- Consider increasing down payment if close to a better rate tier

Step 4: Submit Formal Application and Secure Rate Hold (Week 4-5)

Once your profile is optimized, submit complete application to capture current rates:

- Complete all lender forms accurately and thoroughly

- Provide all requested documentation in organized, clearly labeled format

- Respond promptly to any lender questions or requests for additional information

- Secure rate hold agreement in writing with clear expiration date

Most B-lenders and alternative lenders provide conditional approval within 2-5 business days for well-documented applications. This approval locks your rate for the hold period.

Step 5: Property Search and Purchase (Week 5-16)

With rate hold secured, focus on finding the right Toronto property:

- Work with experienced real estate agent familiar with Toronto neighborhoods

- Get pre-approval documentation to strengthen purchase offers

- Understand financing conditions and timeline requirements in offers

- Communicate with broker about any property-specific issues (condo status, property type, etc.)

For guidance on navigating Toronto’s 2026 real estate market, explore resources on buying in Toronto’s current market conditions.

Step 6: Final Approval and Closing (Week 16-18)

Once you have an accepted offer:

- Submit property details to lender for final approval

- Arrange property appraisal (if required by lender)

- Obtain home insurance with lender listed as mortgagee

- Review final mortgage commitment to confirm rate and terms

- Coordinate with lawyer for closing documentation

- Arrange down payment transfer according to lawyer’s instructions

Ongoing Rate Monitoring Strategy

Even after securing your mortgage, continue monitoring the rate environment:

📊 Track BoC Announcements: Watch for policy rate decisions on the scheduled dates throughout 2026 (March 18, April 16, June 4, July 16, September 10, October 29, December 10)[2].

📈 Monitor Your Variable Rate: Understand how your rate adjusts relative to prime and track monthly payment amounts.

🔄 Review Refinancing Opportunities: If rates drop significantly or your business income increases substantially, refinancing to better terms may make sense.

💡 Maintain Broker Relationship: Stay in contact with your mortgage broker for market updates and refinancing opportunities.

For entrepreneurs exploring refinancing strategies, mortgage refinancing advantages for self-employed borrowers provides comprehensive guidance.

Common Mistakes to Avoid

Self-employed borrowers should be aware of these frequent errors that can derail applications or result in higher rates:

❌ Waiting until after finding a property to explore financing options

❌ Applying to multiple lenders simultaneously (creates duplicate credit inquiries and confusion)

❌ Making major financial changes during the application process

❌ Providing incomplete or disorganized documentation

❌ Failing to disclose all income sources or debts

❌ Accepting the first rate quoted without shopping alternatives

❌ Focusing solely on rate while ignoring terms, penalties, and features

Resources for Self-Employed Borrowers

Additional resources to support your mortgage journey:

- Industry-specific guides: Specialized resources for IT consultants, contractors, and doctors

- Income verification options: Comprehensive overview of alternative income verification methods

- Rate forecasts: Expert analysis on whether mortgage rates will drop further

- Current rates: Real-time updates on best self-employed mortgage rates in Toronto

Conclusion

The BoC rate hold at 2.25% through 2026 creates a unique opportunity for self-employed Toronto entrepreneurs to secure exceptionally competitive variable mortgage rates below 3.5%. While traditional A-lenders maintain strict qualification requirements that exclude many successful business owners, strategic use of B-lenders, alternative documentation programs, and specialized mortgage brokers unlocks access to rates between 3.25% and 3.45%—providing substantial savings over the life of a mortgage.

The key to success lies in understanding that self-employed borrowers have different paths to qualification than traditional employees. Bank statement mortgages, stated income programs, and asset-based qualification methods recognize the true earning capacity of entrepreneurs rather than artificially deflated net income figures designed for tax efficiency.

With the Bank of Canada expected to maintain its overnight rate at 2.25% throughout 2026[1][2][3], and prime rate stabilized at 4.45%, the current environment offers predictability and opportunity. However, B-lender capacity is finite, qualification standards can tighten quickly if economic conditions deteriorate, and the best rate programs may not remain available indefinitely.

Take action now by connecting with a mortgage broker who specializes in self-employed clients, optimizing your documentation and credit profile, and securing a rate hold that protects you during your property search. The combination of stable monetary policy, competitive alternative lending options, and strategic application preparation positions Toronto entrepreneurs to achieve homeownership goals with financing costs that support long-term financial success.

Whether you’re a first-time buyer, looking to upgrade, or seeking to refinance existing debt, the current rate environment favors informed, prepared borrowers who understand how to navigate the self-employed mortgage landscape. The opportunity to lock sub-3.5% variable rates won’t last forever—position yourself to capitalize on it while conditions remain favorable.

References

[1] Fad Press Release 2026 01 28 – https://www.bankofcanada.ca/2026/01/fad-press-release-2026-01-28/

[2] Bank Canada Publishes 2026 Schedule Policy Interest Rate Announcements Other Major Publications – https://www.bankofcanada.ca/2025/08/bank-canada-publishes-2026-schedule-policy-interest-rate-announcements-other-major-publications/

[3] Bank Of Canads First Rate Decision Of 2026 – https://taifujudo.ca/bank-of-canads-first-rate-decision-of-2026/

[4] Interest Rate – https://tradingeconomics.com/canada/interest-rate