March 10, 2026

CMHC Rule Changes Explained: What Canadian Homebuyers Need to Know in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Last updated: March 10, 2026

🏠 Key Takeaways

- The maximum insured mortgage limit rose to $1.5 million (from $1 million), effective December 15, 2024, opening up more of the Canadian housing market to insured buyers. [1]

- 30-year amortizations are now available to all buyers of newly constructed homes, not just first-time buyers, reducing monthly payments. [1]

- The minimum down payment structure is 5% on the first $500,000 and 10% on the portion above $500,000, up to the $1.5 million cap. [1]

- The minimum credit score for CMHC insurance remains at 600, and debt service ratios allow up to 39% GDS and 44% TDS. [1]

- Multi-unit property investors face new premium structures, lease holdback rules, and stricter environmental compliance requirements as of mid-to-late 2025. [7]

- Mortgage arrears are rising in Toronto and Vancouver, with pandemic-era buyers facing the most pressure at renewal. [9]

- Over 1.5 million households have already renewed at higher rates, with another 1 million expected to renew soon. [9]

- First-time buyers can stack the CMHC changes with programs like the FHSA and Home Buyers’ Plan for maximum purchasing power.

Quick Answer

The biggest CMHC rule changes affecting Canadian homebuyers in 2026 center on three shifts: a higher insured mortgage cap ($1.5 million), expanded 30-year amortizations for new builds, and a revised down payment structure. Together, these changes make insured mortgages accessible to more buyers in expensive markets. Investors in multi-unit properties face a separate, more complex set of changes involving new premiums and compliance rules.

What Is CMHC Mortgage Insurance and Why Do the Rules Matter?

CMHC (Canada Mortgage and Housing Corporation) mortgage insurance is required when a homebuyer puts down less than 20% of a property’s purchase price. Without it, most lenders won’t approve a high-ratio mortgage. The rules CMHC sets determine who qualifies, how much they can borrow, and what they pay in premiums.

When CMHC updates its rules, the ripple effects touch every buyer, lender, and real estate market in Canada. That’s why understanding CMHC rule changes explained: what Canadian homebuyers need to know in 2026 is essential before making any purchase decision.

Key terms to know:

- High-ratio mortgage: A mortgage where the down payment is less than 20% of the purchase price.

- Insured mortgage: A mortgage backed by CMHC (or a private insurer like Sagen or Canada Guaranty).

- Amortization period: The total length of time to repay the mortgage in full.

- GDS ratio: Gross Debt Service — the share of gross income going to housing costs.

- TDS ratio: Total Debt Service — the share of gross income going to all debt payments.

For a deeper look at why mortgage loan insurance exists and how it protects both lenders and borrowers, see Why Should We Have Mortgage Loan Insurance?

How Has the Maximum Insured Mortgage Limit Changed?

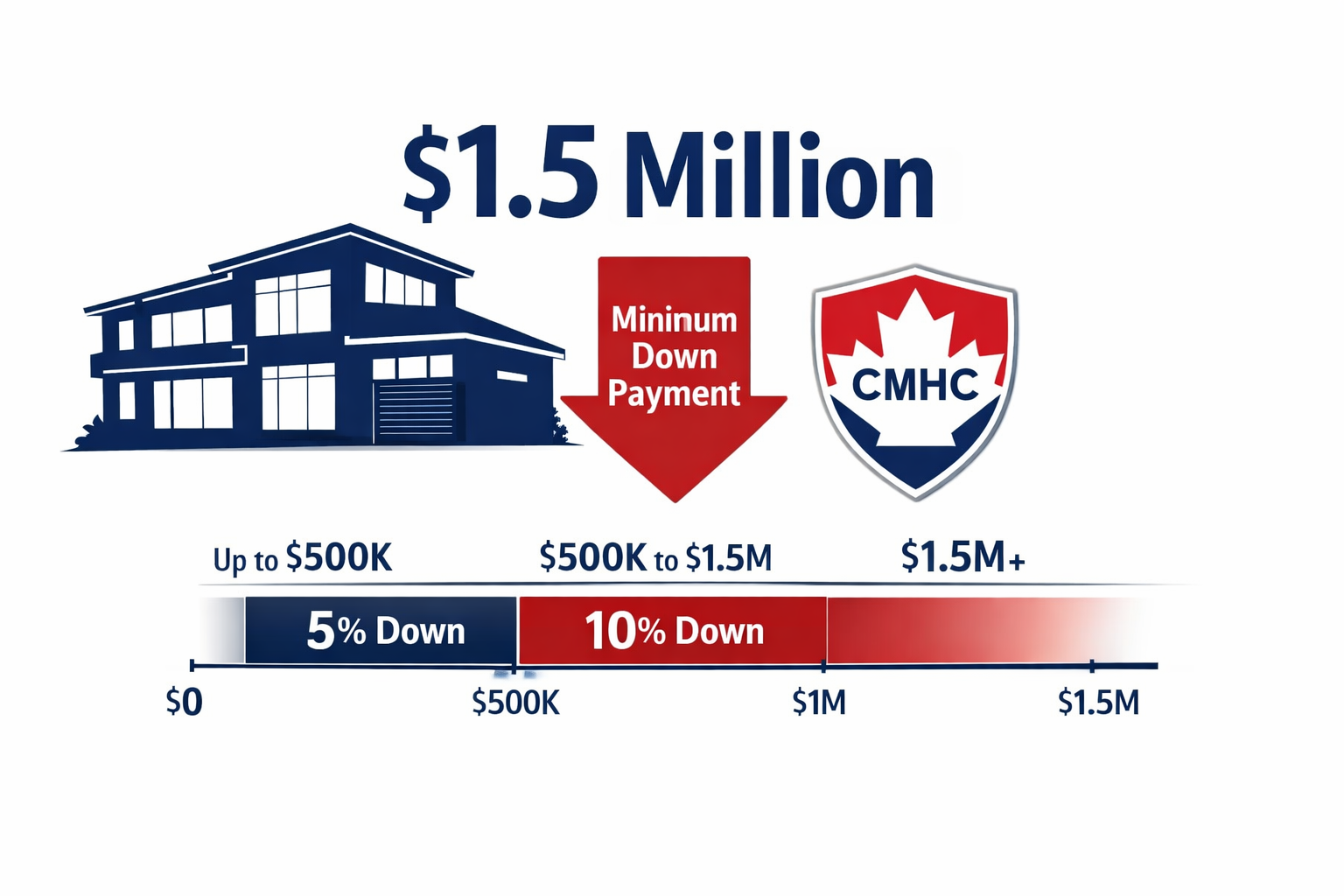

The insured mortgage cap increased from $1 million to $1.5 million, effective December 15, 2024. This is the single most impactful change for buyers in high-cost cities like Toronto and Vancouver.

Previously, any home priced above $1 million required a full 20% down payment — no exceptions. That locked many buyers out of detached homes and larger condos in major urban centres. Now, buyers can purchase properties up to $1.5 million with as little as the minimum required down payment. [1]

What this means in practice:

| Purchase Price | Previous Rule | New Rule (2026) |

|---|---|---|

| Up to $500,000 | 5% down | 5% down |

| $500,001 – $999,999 | 5–10% (tiered) | 5–10% (tiered) |

| $1,000,000 – $1,499,999 | 20% required | Insured (tiered down payment) |

| $1,500,001+ | 20% required | 20% required |

Example: A buyer purchasing a $1.2 million home now needs a minimum down payment of $95,000 (5% on the first $500K = $25,000, plus 10% on the remaining $700K = $70,000). Under the old rules, they would have needed $240,000 (20%).

💡 Choose this if: You’re buying in a major Canadian city where average detached home prices sit between $1 million and $1.5 million, and you don’t have 20% saved.

What Is the New Down Payment Structure for 2026?

The minimum down payment follows a two-tier structure: 5% on the first $500,000 of the purchase price, and 10% on any amount between $500,001 and $1.5 million. [1]

This structure has been in place since 2016 for the lower tiers but now extends up to the new $1.5 million cap. It’s designed to balance accessibility with risk management — buyers purchasing more expensive homes must demonstrate more skin in the game on the upper portion.

Down payment calculator example:

- $600,000 home: 5% × $500,000 = $25,000 + 10% × $100,000 = $10,000 → Total: $35,000

- $900,000 home: 5% × $500,000 = $25,000 + 10% × $400,000 = $40,000 → Total: $65,000

- $1,300,000 home: 5% × $500,000 = $25,000 + 10% × $800,000 = $80,000 → Total: $105,000

Common mistake: Many buyers assume they need 10% on the entire purchase price once the price exceeds $500,000. Only the portion above $500,000 is subject to the 10% requirement.

To maximize your down payment savings, consider pairing this with the First Home Savings Account (FHSA) and the Home Buyers’ Plan through your RRSP.

How Do 30-Year Amortizations Work Under the New Rules?

As of August 1, 2024, all buyers of newly constructed homes can access 30-year amortizations on insured mortgages, regardless of whether they’re first-time buyers. [1] Previously, the maximum amortization for insured mortgages was 25 years.

A longer amortization lowers the monthly payment but increases total interest paid over the life of the mortgage. For buyers in expensive markets, the lower monthly payment can be the difference between qualifying and not qualifying.

25-year vs. 30-year amortization comparison (estimated, $700,000 mortgage at 5.5% interest):

| Amortization | Monthly Payment (est.) | Total Interest Paid (est.) |

|---|---|---|

| 25 years | ~$4,270 | ~$581,000 |

| 30 years | ~$3,970 | ~$729,000 |

Note: These figures are illustrative estimates based on standard amortization calculations. Actual payments depend on your specific rate, lender, and terms.

Who benefits most: Buyers of new builds in high-cost markets who need lower monthly payments to pass the mortgage stress test.

Edge case: The 30-year amortization applies only to insured mortgages on new construction. Resale homes with less than 20% down are still limited to 25-year amortizations unless the buyer qualifies for an uninsured mortgage (20%+ down), where lenders may offer up to 30 years at their discretion.

What Are the Credit Score and Debt Ratio Requirements?

The minimum credit score for CMHC-insured mortgages is 600. The maximum GDS ratio is 39% and the maximum TDS ratio is 44%. [1] These thresholds haven’t changed recently, but they’re worth knowing clearly.

The credit score was reduced from 680 to 600 back in 2021, which expanded access for borrowers with limited credit history or past financial challenges. A score of 600 is the floor — most lenders prefer scores above 650 or 680 for the best rates.

What the debt service ratios mean:

- GDS (39%): Your monthly housing costs (mortgage principal and interest, property taxes, heating, and 50% of condo fees) cannot exceed 39% of your gross monthly income.

- TDS (44%): All of the above, plus all other debt payments (car loans, credit cards, student loans), cannot exceed 44% of your gross monthly income.

Choose a longer amortization if: Your TDS ratio is close to 44% and a lower monthly payment would bring you under the threshold to qualify.

For buyers with non-traditional income, such as self-employed Canadians, qualifying under these ratios can be more complex. See Getting a Mortgage in Canada with a New Job and the Ultimate Guide to Securing a Mortgage for Self-Employed Canadians for more detail.

What Changed for Multi-Unit Property Buyers and Investors?

Investors and developers financing multi-unit residential properties through CMHC face a significantly restructured set of rules introduced in mid-to-late 2025. These changes affect premium pricing, lease holdbacks, and environmental compliance — and they carry real financial consequences if overlooked. [7]

Key changes for multi-unit properties:

New premium pricing grid (July 14, 2025): CMHC introduced a simplified premium structure for multi-unit properties, with rates varying by loan-to-value (LTV) ratio and building type. MLI Select loans — which target affordability, accessibility, and energy efficiency — can receive premium discounts of up to 30%. [7]

Lease holdback requirements (November 2025): New rules require phased funding tied to performance metrics for multi-unit projects. Investors need to plan their cash flow around these staged disbursements rather than receiving full funding upfront. [3]

Environmental compliance (tightened in 2025): Properties cannot receive loan disbursements until environmental remediation is 100% confirmed. No progress remediation is permitted during active construction phases for multi-unit projects. [4] This is a significant change for developers working on brownfield or previously industrial sites.

Rent increase restrictions (February 26, 2026): Landlords can no longer increase rents above the Consumer Price Index (CPI) rate when existing tenants vacate, closing a practice where landlords would charge maximum allowable rents on turnover. [4]

Common mistake for investors: Underestimating the cash flow impact of lease holdbacks and environmental compliance delays. Both can extend timelines and increase carrying costs significantly.

How Is the Mortgage Renewal Wave Affecting Canadian Homebuyers?

Mortgage arrears are rising in Canada’s largest markets, and the renewal wave is putting real financial pressure on borrowers who bought during the pandemic era. This is one of the most important market conditions shaping CMHC’s approach in 2026. [9]

According to CMHC data, Toronto’s mortgage arrears rate has more than quadrupled from post-pandemic lows, with continued increases projected through 2026. Vancouver shows a more moderate but steady rise. [9]

Who is most at risk:

- Buyers who purchased between 2020 and 2024 at peak prices and historically low rates

- Borrowers now renewing into rates that are 2–3 percentage points higher than their original rate

- Households with high TDS ratios who relied on low payments to qualify

Over 1.5 million Canadian households have already renewed at higher rates. Another 1 million are expected to renew in the coming year, with many choosing longer amortizations to manage the payment increase. [9]

📌 Pull quote: “Pandemic-era buyers face the steepest renewal shock — many locked in at rates below 2% and are now renewing closer to 5% or higher.”

For buyers thinking about refinancing to manage renewal pressure, the 2026 rate forecasts and refinancing strategies article offers a useful breakdown.

CMHC Rule Changes Explained: What Canadian Homebuyers Need to Know in 2026 — Practical Checklist

Before applying for an insured mortgage in 2026, work through this checklist:

- Confirm your purchase price falls at or below $1.5 million to qualify for CMHC insurance

- Calculate your minimum down payment using the 5%/10% tiered structure

- Check your credit score — minimum 600 required, but 650+ improves your rate options

- Calculate your GDS and TDS ratios before applying — stay under 39% and 44% respectively

- Determine if your target home is a new build — if so, you may qualify for a 30-year amortization

- Maximize savings vehicles — contribute to your FHSA and consider the Home Buyers’ Plan

- Gather your mortgage documents — see the Mortgage Document Checklist for a full list

- Get pre-approved before making an offer — the importance of qualifying before buying cannot be overstated

- If investing in multi-unit properties, review the new premium grid, holdback rules, and environmental requirements with a broker

Frequently Asked Questions

Q: Does the $1.5 million insured mortgage limit apply to all buyers or just first-time buyers? A: It applies to all buyers, not just first-time buyers. Any eligible homebuyer purchasing a property priced up to $1.5 million can use CMHC-insured financing with less than 20% down. [1]

Q: Can I use a 30-year amortization on a resale home with less than 20% down? A: No. The 30-year amortization for insured mortgages applies only to newly constructed homes. Resale purchases with less than 20% down are still limited to a 25-year amortization. [1]

Q: What credit score do I need for CMHC mortgage insurance? A: The minimum is 600. However, many lenders prefer 650 or higher to offer competitive rates. A score below 600 will disqualify you from CMHC-insured financing. [1]

Q: Do the new CMHC rules help with affordability in Toronto and Vancouver? A: They improve access — more buyers can now purchase homes priced between $1 million and $1.5 million with less than 20% down. But they don’t reduce prices. Buyers still need to pass the stress test and meet income requirements. [1]

Q: What is the CMHC mortgage insurance premium? A: Premiums are calculated as a percentage of the insured mortgage amount, ranging from 0.60% (for a 65–80% LTV) to 4.00% (for a 95% LTV, meaning a 5% down payment). The premium is added to your mortgage balance. [1]

Q: Are the new multi-unit CMHC rules retroactive? A: No. The new premium grid, lease holdback rules, and environmental compliance requirements apply to new applications submitted after the relevant effective dates. Existing insured loans are not retroactively affected. [7]

Q: What is the MLI Select program? A: MLI Select is a CMHC program for multi-unit residential properties that offers premium discounts of up to 30% for projects meeting affordability, accessibility, and energy efficiency targets. [7]

Q: Can I combine the new CMHC rules with the First Home Savings Account (FHSA)? A: Yes. FHSA contributions can be used toward your down payment, and using the FHSA alongside the revised CMHC rules can significantly increase your purchasing power as a first-time buyer.

Q: What happens if I can’t pass the stress test even with a 30-year amortization? A: A longer amortization lowers your monthly payment, which can help you pass the stress test. If you still can’t qualify, options include a larger down payment, a co-borrower, or exploring private mortgage options in Ontario.

Q: Are mortgage arrears a sign that CMHC rules will tighten again? A: Rising arrears are a signal that CMHC monitors closely. While no new tightening has been announced for 2026, borrowers should expect CMHC to continue adjusting rules based on market stress indicators. [9]

Conclusion: What to Do Next

The CMHC rule changes explained throughout this guide represent the most significant shift in Canadian mortgage policy in years. For homebuyers in 2026, the core takeaways are clear: the $1.5 million insured cap opens doors in expensive markets, 30-year amortizations on new builds reduce monthly payments, and the tiered down payment structure makes the math more manageable for mid-range purchases.

Actionable next steps:

- Run your numbers using the down payment tiers and debt service ratio limits before you start shopping.

- Open or maximize your FHSA if you haven’t already — it’s one of the most tax-efficient ways to build a down payment.

- Get pre-approved with a licensed mortgage broker who understands the 2026 rule landscape.

- If you’re a multi-unit investor, review the new premium grid and holdback requirements with a commercial mortgage specialist before committing to a project.

- If you’re approaching renewal, explore refinancing options now rather than waiting — the renewal wave is real, and preparation matters.

For a broader view of where the Canadian housing market is heading, see the 2025 Canadian Housing Market Outlook and the latest on how Canadian fixed mortgage rates are responding to external pressures.

The rules have changed. The opportunity is there. The buyers who act with clear information will be the ones who benefit most.

References

[1] CMHC Mortgage Rules – https://wowa.ca/cmhc-mortgage-rules

[2] CMHC Is Making Important Changes To Multi Unit Mortgage Insurance Here Is What You Need To Know – https://www.firstnational.ca/commercial/resources-insights/article/cmhc-is-making-important-changes-to-multi-unit-mortgage-insurance-here-is-what-you-need-to-know

[3] Watch (Lease Holdback Requirements) – https://www.youtube.com/watch?v=zBsfc7hs5ro

[4] Watch (Environmental Compliance and Rent Restrictions) – https://www.youtube.com/watch?v=sLso4AyiVdw

[7] Article Sept5 25 – https://www.reic.ca/article-sept5-25.html

[9] Mortgage Renewal Wave Strains Some Regions Borrowers – https://www.cmhc-schl.gc.ca/observer/2026/mortgage-renewal-wave-strains-some-regions-borrowers

Tags: CMHC rule changes, mortgage insurance Canada, insured mortgage 2026, down payment rules, 30-year amortization, first-time homebuyers Canada, mortgage stress test, CMHC premiums, Canadian housing market, multi-unit mortgage rules, mortgage renewal Canada, FHSA home buying