March 10, 2026

Using Rental Income to Qualify for a Mortgage in Ontario: 2026 Guide

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

n

Last updated: March 10, 2026

Thousands of Ontario homebuyers are sitting on a powerful qualification tool and don’t know it: rental income. Whether it’s a basement apartment, a secondary suite, or a legal duplex, that monthly rent cheque can meaningfully increase your borrowing power — but only if lenders count it the right way. This guide to Using Rental Income to Qualify for a Mortgage in Ontario: 2026 Guide breaks down exactly how lenders treat rental income, what changed under OSFI’s 2026 capital rules, and what steps to take before submitting your application.

Key Takeaways 🏠

- Owner-occupied properties with a self-contained rental suite get the most favourable treatment: lenders may count 50–100% of rental income toward qualification.

- Big banks typically apply a 50% rental income offset; some credit unions and B-lenders may use up to 100% for legal, self-contained suites. [1]

- CMHC-insured mortgages allow 100% of rental income from an owner-occupied suite (up to a duplex), subject to a minimum 680 credit score and 2 years of rental history. [2]

- OSFI’s 2026 CAR Guideline introduced the IPRRE (Income-Producing Real Estate) classification, affecting how banks hold capital — but it does not directly change how borrowers qualify under B-20 guidelines. [3]

- No double-counting: rental income used to qualify for one mortgage cannot be reused to qualify for a second investment property mortgage. [7]

- Separate investment properties (not owner-occupied) face much stricter treatment; many lenders will not count that rental income at all for a new purchase. [1]

- Documentation matters: expect to provide a signed lease, 2 years of T1 tax returns showing rental income, and proof the suite is legal and self-contained.

- A mortgage broker can shop lenders who apply more generous rental income policies, which can make a significant difference in what you qualify for.

Quick Answer

Ontario lenders can use rental income to boost your mortgage qualification, but the rules depend on whether you live in the property. For an owner-occupied home with a legal suite, lenders typically count 50–100% of the rental income. For a separate investment property, most lenders will not count rental income toward a new mortgage application. OSFI’s 2026 rule changes affect bank capital requirements, not borrower qualification directly.

What Is Rental Income Qualification and How Does It Work?

Rental income qualification means a lender adds some or all of your rental earnings to your total qualifying income when calculating how large a mortgage you can carry. The more income a lender recognizes, the higher your gross debt service (GDS) and total debt service (TDS) ratios can support — which translates into a larger mortgage approval.

Two main approaches lenders use:

| Approach | How It Works | Who Uses It |

|---|---|---|

| Rental Offset | Rental income reduces the property’s carrying costs rather than adding to income | Common with investment properties |

| Add-Back to Income | A percentage of rent is added directly to your qualifying income | Common for owner-occupied suites |

For most Ontario borrowers, the add-back method is more powerful. A lender who counts $2,000/month in rental income at 80% is effectively adding $1,600/month to your qualifying income — which can increase your mortgage ceiling by roughly $200,000–$250,000 depending on the rate and amortization.

Quick example: A borrower earns $7,500/month from employment. Their basement suite rents for $2,000/month. If the lender counts 75% of that rent ($1,500), the qualifying income becomes $9,000/month — a 20% boost before any other factors are considered. [5]

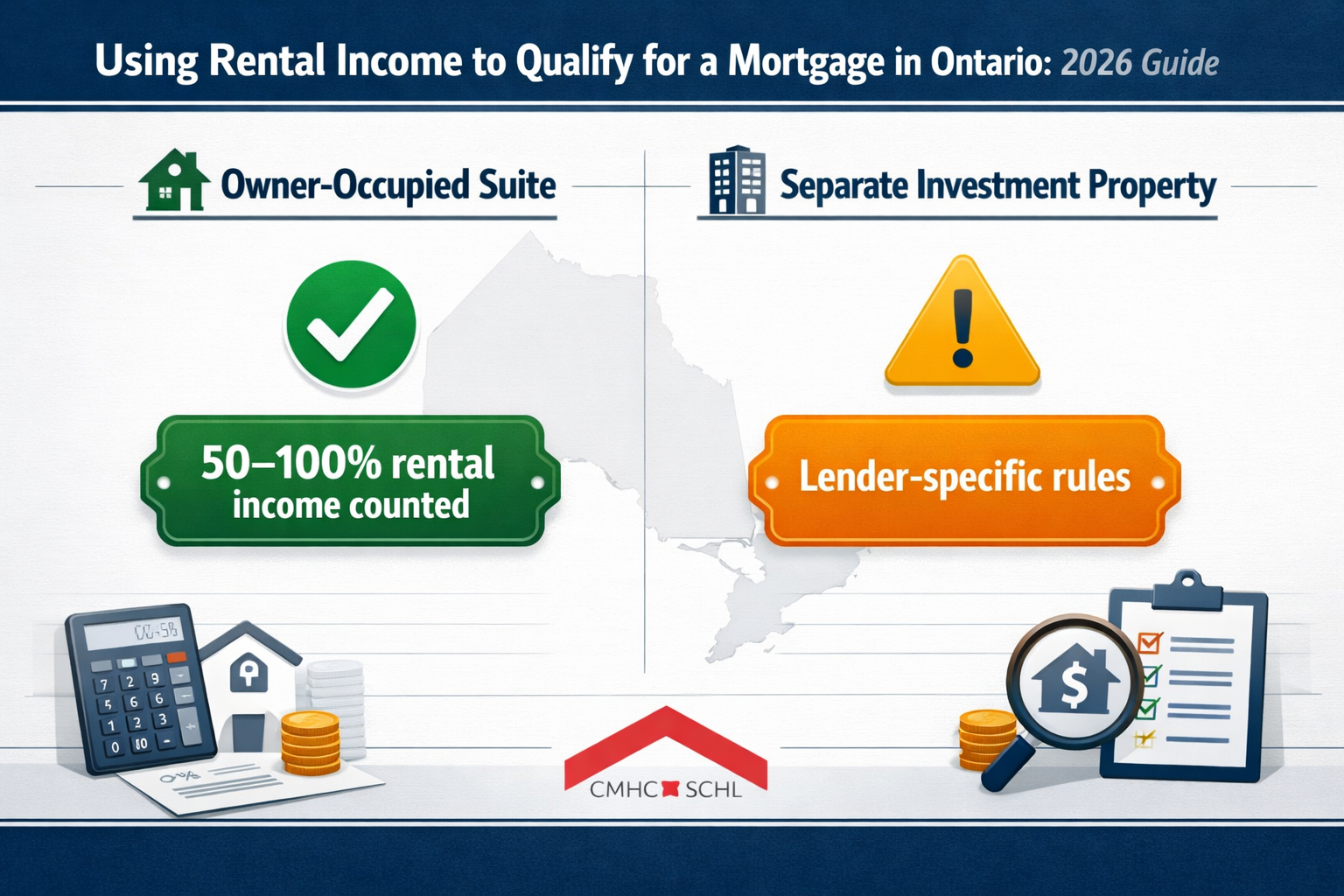

Owner-Occupied vs. Investment Property: The Critical Difference

The single most important factor in using rental income to qualify for a mortgage in Ontario is whether you live in the property. Lenders treat these two scenarios very differently.

Owner-occupied with a rental suite:

- Lenders view this as lower risk because the owner has a personal stake in maintaining the property.

- CMHC allows 100% of rental income from a self-contained suite in an owner-occupied property (maximum 2 units, such as a duplex), provided the owner lives there, has at least 2 years of occupancy/rental history, a minimum 680 credit score, and the suite meets local zoning requirements. [2]

- Conventional lenders (without CMHC insurance) typically use 50% of rental income, though some credit unions and B-lenders may go up to 100% for legal, self-contained suites. [1]

Separate investment property:

- Most lenders will not count rental income from a property you don’t live in when qualifying for a new mortgage. [1]

- The reasoning: rental income from a separate property is considered non-guaranteed. Vacancies, tenant issues, and maintenance costs make it unreliable in lenders’ eyes.

- Some B-lenders and alternative lenders may consider it, but expect stricter terms and higher rates.

Choose the owner-occupied route if: you’re buying a property where you’ll live in one unit and rent the other. This gives you access to the most favourable rental income treatment and potentially CMHC-insured rates.

For more on what to consider before buying a rental property, see this guide on what to consider when buying a rental property investment.

How Do OSFI’s 2026 Rules Affect Rental Income Qualification?

OSFI’s 2026 Capital Adequacy Requirements (CAR) Guideline, effective January 1, 2026, introduced a new classification called IPRRE (Income-Producing Real Estate). This applies when more than 50% of a borrower’s qualifying income comes from the rental income of the property being financed. [3]

What IPRRE means in practice:

- Banks must hold more regulatory capital against IPRRE-classified mortgages.

- This higher capital requirement may lead some lenders to charge slightly higher rates or apply tighter conditions for rental-heavy applications. [8]

- Rental income used to qualify for one mortgage cannot be double-counted for a second property; each property must qualify independently. [7]

What IPRRE does NOT change:

- OSFI confirmed that the 2026 CAR updates affect bank internal capital models, not the B-20 borrower qualification guidelines directly. [3]

- Borrowers can still use rental income for mortgage qualification under the same B-20 framework.

- The rules apply Canada-wide, including Ontario, with no Ontario-specific carve-outs. [3]

Common mistake: Some Ontario investors assumed the 2026 OSFI changes would block them from using rental income entirely. That’s not accurate. The changes make it more expensive for banks to hold these loans, which may filter through to pricing — but qualification itself follows B-20 rules.

If you’re also navigating complex income situations, the guide to getting a mortgage without traditional income covers alternative approaches worth knowing.

What Documentation Do Lenders Require for Rental Income?

Lenders need proof that rental income is real, legal, and stable. Missing even one document can result in the income being excluded entirely.

Standard documentation checklist:

- ✅ Signed lease agreement (current, showing monthly rent amount and tenant name)

- ✅ Last 2 years of T1 General tax returns showing rental income on Schedule L (or equivalent)

- ✅ Notice of Assessment (NOA) for the past 2 years

- ✅ Proof the suite is legal and self-contained (zoning certificate, building permit, or municipal confirmation)

- ✅ Evidence of continuous rental history (bank statements showing rent deposits)

- ✅ Property tax bill and current mortgage statement (if refinancing)

For CMHC-insured applications specifically:

- Rental income must match the current owner’s reported earnings.

- Income must be continuous for at least 2 years, or averaged if it changed during that period. [2]

- Minimum credit score of 680 is required. [2]

Edge case: If the suite is newly built or recently legalized, lenders may use a market rent estimate from an appraiser rather than actual rental history. Not all lenders accept this — confirm with your broker before applying.

For a full list of mortgage application documents, the mortgage document checklist is a practical starting point.

How Much Rental Income Will Lenders Actually Count?

The percentage of rental income a lender counts varies by lender type, property type, and whether the mortgage is insured.

Rental income treatment by lender type:

| Lender Type | Owner-Occupied Suite | Separate Investment Property |

|---|---|---|

| Big 5 Banks (A-lenders) | 50% of gross rent | Often excluded or minimal offset |

| Monoline Lenders | 50–80% of gross rent | Case-by-case basis |

| Credit Unions | Up to 100% for legal suites | Limited; varies by institution |

| B-Lenders | Up to 100% for legal suites | May consider with conditions |

| CMHC-Insured | Up to 100% (owner-occupied duplex) | Not applicable |

[1][6]

Why the 50% rule exists at big banks: Lenders apply a haircut to account for vacancy periods, maintenance costs, and income tax on rental earnings. A 50% factor is a conservative estimate of net rental income after these deductions.

Choosing the right lender matters: A borrower who qualifies for $600,000 at a big bank using 50% of rent might qualify for $750,000+ at a credit union using 80–100%. Working with a mortgage broker lets you compare these options without applying to each lender separately.

Does Rental Income Help with the Mortgage Stress Test?

Yes — and this is where rental income qualification becomes especially valuable. The Canadian mortgage stress test requires borrowers to qualify at the higher of the Bank of Canada’s qualifying rate or their contract rate plus 2%. For more on how stress testing works, see this stress test cheat sheet.

Adding rental income to your qualifying income directly improves your GDS and TDS ratios, which means you can pass the stress test at a higher mortgage amount.

Practical example:

- Borrower A earns $85,000/year (about $7,083/month). No rental income. At current stress test rates, they might qualify for roughly $450,000–$500,000.

- Borrower B earns the same $85,000/year but has a legal basement suite renting for $1,800/month. If the lender counts 50% ($900/month), their effective qualifying income rises to approximately $7,983/month — potentially adding $80,000–$100,000 to their maximum mortgage.

The exact numbers depend on the stress test rate, amortization period, property taxes, and other debts. Always confirm with a broker or lender.

Important constraint: The rental income must be from the property being purchased or refinanced, not from an unrelated property, for most lenders to count it in this way.

What Are the Risks and Downsides of Relying on Rental Income to Qualify?

Using rental income to qualify for a mortgage is legitimate and common — but there are real risks worth understanding before committing.

Key risks:

- Vacancy risk: If the tenant leaves, your qualifying income on paper doesn’t change, but your actual cash flow does. Can you carry the full mortgage payment without the rental income?

- Tenant issues: Eviction in Ontario can take months under the Landlord and Tenant Board process. Budget for potential periods without rent.

- Higher scrutiny from lenders: Applications relying heavily on rental income may face more documentation requests and longer approval timelines.

- IPRRE classification: Under the 2026 OSFI rules, if rental income makes up more than 50% of your qualifying income, the lender must classify the mortgage as IPRRE, which may result in a higher rate. [8]

- Tax implications: Rental income is taxable. Lenders look at gross rental income, but you’ll owe income tax on net rental income, which reduces your actual take-home benefit. For details on the tax side, see this guide to basement rental income tax in Canada.

Self-employed borrowers face an added layer of complexity, since their primary income is already harder to document. If this applies to you, the guide to investing in rental properties as a self-employed individual addresses the overlap directly.

Step-by-Step: How to Use Rental Income to Qualify for a Mortgage in Ontario in 2026

Using rental income to qualify for a mortgage in Ontario in 2026 follows a clear process. Here’s how to approach it:

Step 1: Confirm the suite is legal and self-contained Check with your municipality that the rental unit has a valid building permit, meets zoning requirements, and has a separate entrance. Illegal suites are excluded by all major lenders.

Step 2: Establish a rental history (or get a market rent appraisal) Two years of documented rental income on your tax returns is the gold standard. If the suite is new, ask your mortgage broker about lenders who accept appraised market rent.

Step 3: Gather all documentation Use the checklist above. Have your lease, T1 returns, NOAs, and zoning confirmation ready before approaching any lender.

Step 4: Get pre-approved before shopping Knowing your actual qualification ceiling — with rental income factored in — prevents wasted time and disappointment. See why qualifying for a mortgage before buying matters so much in a competitive market.

Step 5: Compare lenders through a mortgage broker Because rental income treatment varies significantly by lender, a broker who can access A-lenders, B-lenders, and credit unions is far more valuable here than going directly to one bank.

Step 6: Understand the stress test impact Ask your broker to run the numbers with and without rental income so you understand exactly how much the rental income boosts your qualification.

Step 7: Budget conservatively Qualify using the rental income, but budget as if the unit could be vacant for 1–2 months per year. This protects you if a tenant situation changes after closing.

FAQ: Using Rental Income to Qualify for a Mortgage in Ontario

Q: Can I use rental income from an Airbnb to qualify for a mortgage? Short-term rental income (Airbnb, VRBO) is treated with significant skepticism by most lenders. It’s considered highly variable and is generally excluded from qualifying income by A-lenders. Some B-lenders may consider a 2-year average of reported Airbnb income from tax returns.

Q: Do I need a tenant already in place to use rental income? For most lenders, yes — an existing signed lease is required. Some lenders will accept a market rent appraisal from a licensed appraiser for newly constructed suites, but this is lender-specific.

Q: Does rental income help if I’m buying a triplex or fourplex? Yes, but the rules shift. For 3–4 unit properties, lenders typically use a rental offset approach rather than adding income directly. CMHC has specific multi-unit programs for these properties.

Q: Can rental income from a property I already own help me buy a new home? Generally no for conventional lenders — rental income from a separate investment property is usually excluded when qualifying for a new purchase. [1] Some B-lenders may consider it with strong documentation.

Q: What credit score do I need to use rental income under CMHC rules? A minimum credit score of 680 is required for CMHC-insured mortgages that use rental income from an owner-occupied suite. [2]

Q: Will the 2026 OSFI IPRRE rules make it harder for me to qualify? Not directly. OSFI’s IPRRE classification affects how banks hold capital, not how borrowers qualify under B-20 guidelines. However, if rental income exceeds 50% of your qualifying income, lenders may price the mortgage slightly higher to offset their capital costs. [3][8]

Q: Can I use rental income if I’m self-employed? Yes, but documentation requirements are stricter. Lenders want to see both your self-employment income and rental income reported consistently on tax returns for at least 2 years.

Q: What happens if my tenant stops paying rent after I close? The mortgage obligation doesn’t change. This is why budgeting conservatively — assuming some vacancy — is essential when structuring a purchase around rental income.

Q: Is there a maximum rental income percentage lenders will count? CMHC allows up to 100% for owner-occupied duplexes meeting all criteria. [2] Conventional lenders cap it at 50–80% in most cases, though some credit unions go to 100% for legal suites. [1][6]

Q: Do I need to declare the rental income on my taxes for lenders to count it? Yes. Lenders verify rental income against your T1 tax returns and Notice of Assessment. Undeclared rental income cannot be used for qualification and may raise red flags during underwriting.

Conclusion: Actionable Next Steps

Rental income is a legitimate and often underused tool for Ontario mortgage qualification — but only when it’s structured correctly. The rules in 2026 are clear: owner-occupied properties with legal, self-contained suites get the most favourable treatment, CMHC can count up to 100% of that income, and most conventional lenders use 50%. OSFI’s new IPRRE classification adds a layer of complexity for investors whose qualifying income is rental-heavy, but it doesn’t block qualification outright.

Here’s what to do next:

- Confirm your suite’s legal status with your municipality before anything else.

- Pull your last 2 years of T1 returns and check that rental income is properly reported.

- Contact a mortgage broker who works with multiple lender types — the difference between a 50% and 100% rental income count can be worth hundreds of thousands of dollars in qualification.

- Get pre-approved with rental income factored in before making any offers. See the ins and outs of mortgage pre-approval in Ontario for a full walkthrough.

- Budget conservatively: qualify with rental income, but ensure the mortgage is serviceable without it.

Ontario’s housing market in 2026 rewards buyers who understand the full range of tools available to them. Rental income qualification is one of the most powerful — use it wisely.

References

[1] Can You Use Rental Income To Qualify For A Mortgage In Ontario – https://danielleinthecity.ca/can-you-use-rental-income-to-qualify-for-a-mortgage-in-ontario/

[2] Can I Afford To Buy A Home With A Mortgage Helper – https://www.ratehub.ca/blog/can-i-afford-to-buy-a-home-with-a-mortgage-helper/

[3] Osfi Tightens The Rules On Income Producing Real Estate 8819439 – https://andrewleerealty.ca/blog.html/osfi-tightens-the-rules-on-income-producing-real-estate-8819439

[5] Newmortgagerules – https://www.aaronsantos.net/blog/newmortgagerules

[6] Qualify For A Mortgage With Income Suite – https://rates.ca/resources/qualify-for-a-mortgage-with-income-suite

[7] Osfi Rental Property Mortgage Guidelines 2026 – https://valery.ca/blog/osfi-rental-property-mortgage-guidelines-2026/

[8] Osfis Rental Mortgage Changes – https://www.cityplex.ca/news-2/osfis-rental-mortgage-changes

Tags: rental income mortgage Ontario, mortgage qualification 2026, CMHC rental suite, OSFI IPRRE rules, owner-occupied duplex mortgage, B-20 guidelines, mortgage helper Ontario, investment property mortgage, rental income documentation, stress test rental income, Ontario mortgage broker, secondary suite mortgage