March 11, 2026

Private Mortgages for Toronto Multi-Family Investors: Capitalizing on 2026 Rental Recovery Trends

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

After years of hyper-compressed vacancies and runaway rents, Toronto’s multi-family rental market is entering a new phase — one that rewards patient, well-financed investors who can move fast. Private Mortgages for Toronto Multi-Family Investors: Capitalizing on 2026 Rental Recovery Trends is no longer just a niche strategy. It is becoming a mainstream playbook for GTA investors who need speed and flexibility that traditional banks simply cannot offer. With asking rents softening, bank lending tightening under new OSFI rules, and 81% of lenders planning to grow originations [9], the window to acquire well-positioned multi-family assets is open — but only for those with the right financing in place.

Key Takeaways 📌

- Toronto asking rents dropped 7.2% year-over-year to $2,504 in January 2026, creating a buyer’s window for strategic acquisitions before the expected 2028–2029 rent rebound.

- New OSFI capital rules effective Q1 2026 make banks more restrictive on rental property mortgages, pushing investors toward private lenders [3].

- Private lending now represents ~20% of Ontario mortgages, up from 8–12% nationally five years ago, driven by timing needs — not credit problems.

- Private mortgages offer 6–12 month bridge solutions that let investors close quickly, renovate, and then refinance into conventional or CMHC-insured products.

- 81% of lenders plan to increase originations in 2026 [9], meaning debt market liquidity is improving — a tailwind for both private and conventional multi-family financing.

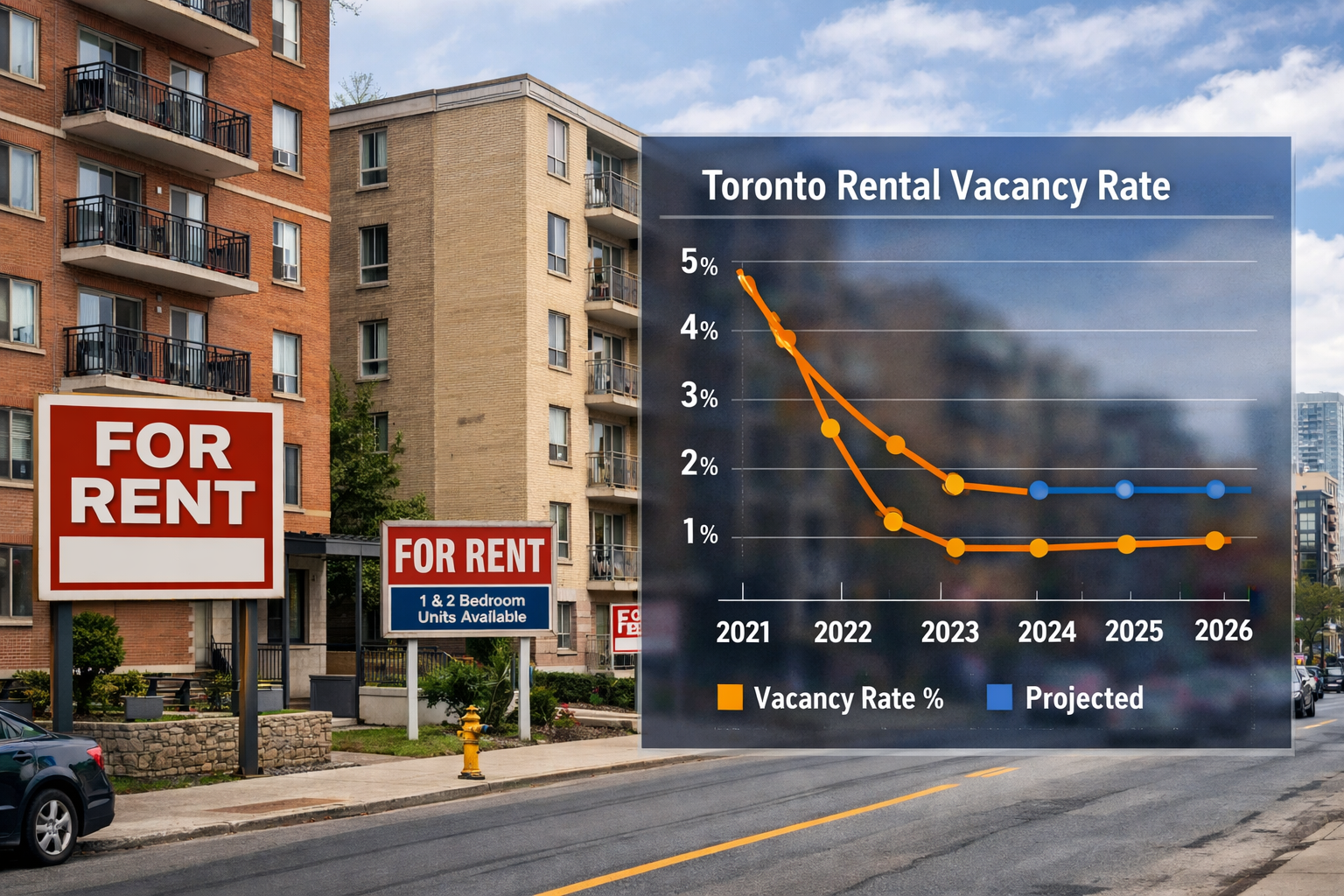

Toronto’s 2026 Rental Market: Softening Now, Surging Later

The headline for Ontario’s rental market in 2026 is balance — a word landlords haven’t heard in years [2]. For the first time in a long time, increased supply and softening demand are converging. The GTA has officially shifted to a tenant’s market, with landlords facing new pressure around retention, turnover costs, and competitive pricing.

The Numbers Behind the Shift

| Market | YoY Rent Change (Jan 2026) | Avg. Asking Rent |

|---|---|---|

| City of Toronto | -7.2% | $2,504 |

| Mississauga | -9.8% | ~$2,300 |

| Brampton | -10.0% | ~$2,100 |

Source: Terry Riddoch Ontario Rental Market Forecast, February 2026

This softening is temporary, not structural. According to John-Bosco Agbasi, Managing Director at Fengate Asset Management, rents may dip further in 2026, but investors who underwrite conservatively now will see outsized rent growth in 2028–2029. The smart money is buying the dip — and using private financing to do it quickly.

💡 Pull Quote: “If you’ve underwritten zero and then two in 2026, you might be several hundred basis points off in the front end. But the good news is in the back end of that model, as you get into ’28, ’29, you’re going to see outsized rent growth.” — John-Bosco Agbasi, Fengate Asset Management

For investors comparing asset classes, a detailed breakdown of investing in condos vs. ADUs in Toronto shows why multi-family residential is gaining ground as a preferred vehicle in 2026’s stabilizing environment.

Why Banks Are Pulling Back — And Private Lenders Are Stepping In

OSFI’s New Rules Change the Game 🏦

Effective Q1 2026, OSFI’s updated Capital Adequacy Requirements (CAR) Guideline introduced stricter income-producing residential real estate (IPRRE) rules. Banks must now hold more capital against rental property mortgages and can no longer “double-count” rental income across multiple properties [3]. The practical result: many experienced multi-family investors with strong portfolios are being declined or offered less favorable terms by their existing bank relationships.

This regulatory shift is one of the primary reasons private lending now represents approximately 20% of Ontario mortgages, compared to just 8–12% nationally five years ago. The market has evolved well beyond serving distressed borrowers. As Ryan MacNeil and Neal Andreino of Keystone Capital Group put it plainly: “Private lending is a timing tool, not a credit issue.”

The Renewal Wave Adds Pressure 🌊

Approximately 1.8 million Canadian mortgages are renewing in the next twelve months, with the absolute peak expected in June 2026 [4]. Many of these are investment properties locked in at pre-2022 rates. When investors face renewal at higher rates while rents are temporarily softer, the math can get tight — and banks applying new OSFI rules may not renew on the same terms. Understanding the impact of rate resets and the mortgage renewal wave is critical for multi-family investors planning their 2026 strategy.

Comparing Financing Options for Multi-Family Investors

| Financing Type | Rate Range | LTV Cap | Best For |

|---|---|---|---|

| CMHC-Insured (MLI) | 3.50%–4.25% | Up to 85% | Stabilized properties, patient timelines |

| Conventional Bank | 4.75%–6.50% | 60%–75% | Strong equity, proven track record |

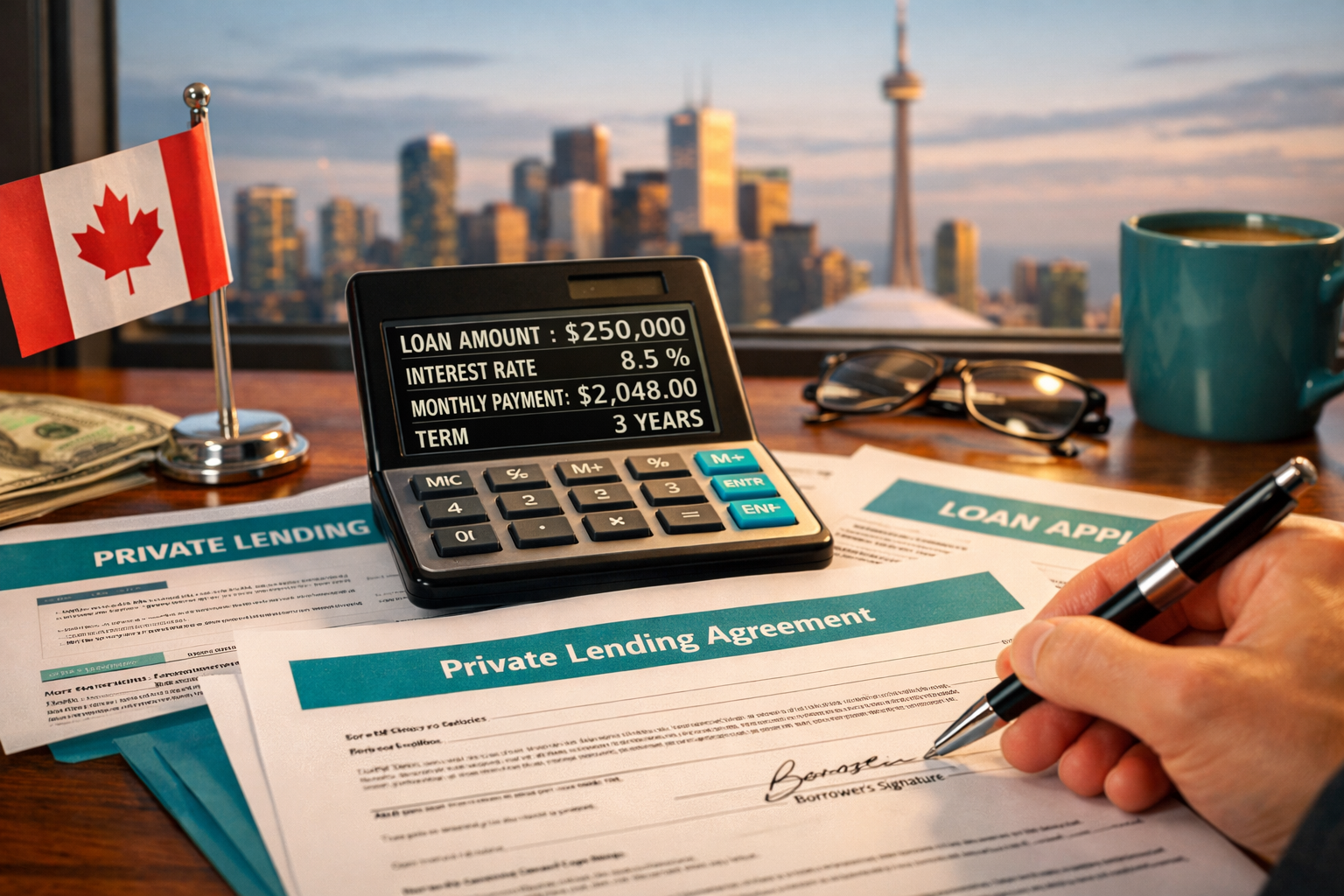

| Private Mortgage | 7.00%–12.00% | Up to 75–80% | Speed, bridge, renovation |

Source: LendCity Multifamily Mortgage Rates Guide, February 2026

While CMHC-insured financing saves roughly $70,000 per year on a $4M loan compared to private rates, it requires stabilized occupancy and a longer approval timeline. Private mortgages fill the gap when speed matters most — and they’re designed to be short-term bridges, not permanent solutions [6].

For investors navigating the difference between bank and alternative lenders, reviewing banks vs. alternative private lenders provides a useful framework for decision-making.

How Private Mortgages Enable Multi-Family Acquisitions in 2026

Private Mortgages for Toronto Multi-Family Investors: Capitalizing on 2026 Rental Recovery Trends works as a strategy precisely because of the timing mismatch between opportunity and traditional financing approval windows.

The Typical Private Mortgage Bridge Strategy

Here’s how a well-structured private mortgage play works in the current GTA market:

- 🔍 Identify an underperforming multi-family property (4–12 units) with below-market rents or deferred maintenance

- ⚡ Close quickly using a private mortgage (often within 5–10 business days vs. 30–60 days for banks)

- 🔨 Renovate and stabilize units to increase rental income and occupancy

- 📋 Refinance into a CMHC-insured or conventional product once the property meets standard lender criteria

- 📈 Hold through the 2027–2029 rent recovery cycle

This model is especially relevant for investors looking to refinance an existing property to create legal basement apartments or garden suites, adding rental units and value before transitioning to long-term financing.

What Private Lenders Actually Look At ✅

Unlike banks, private lenders focus primarily on:

- Property value and equity position (LTV is king)

- Exit strategy clarity — how and when will the borrower refinance?

- Rental income potential of the asset, not just current leases

- Borrower experience in multi-family or real estate generally

This asset-based approach is why investors with complex income structures — including self-employed landlords — often find private lending more accessible. Exploring best private mortgage rates in Ontario helps set realistic expectations on cost before committing to a deal.

Capital Is Shifting Toward Private Mortgages 💰

Canadian investors are actively reallocating capital away from condos — which face oversupply and negative cash flow — and into private mortgages as both a lending investment and a financing tool [7]. With 81% of lenders planning to increase originations in 2026 and most targeting ~10% volume growth over 2025 [9], the private lending ecosystem is well-capitalized and competitive. This benefits borrowers through better rates and more flexible terms than were available even 12 months ago.

Working With a Mortgage Broker Is Non-Negotiable 🤝

Navigating private lenders, OSFI-compliant bank products, and CMHC programs simultaneously requires expertise. Working with a mortgage broker in Toronto gives multi-family investors access to the full lending spectrum — from Schedule A banks to MICs and individual private lenders — without having to shop each relationship independently. A broker also helps structure the deal so the private mortgage exit strategy into conventional financing is viable from day one.

For investors who want to understand the full approval process before committing, reviewing what to expect during the mortgage process and the importance of qualifying for a mortgage before buying property are essential first steps.

Conclusion: Act Now, Refinance Later

The 2026 GTA rental market is offering a rare combination: temporarily softened prices, tightened bank lending, and a confirmed recovery trajectory. For multi-family investors who understand how to use private mortgages as a precision timing tool — not a last resort — this is one of the most compelling entry windows in recent memory.

Actionable Next Steps 🚀

- Audit your current portfolio for properties that could benefit from a private mortgage bridge to fund renovations and increase rental income before the 2028–2029 rent recovery

- Get pre-qualified with a private lender now, before a deal surfaces — speed is the entire value proposition

- Model your exit strategy into CMHC-insured financing from day one to ensure the numbers work at both ends

- Consult a mortgage broker who specializes in multi-family and investment properties to access the full range of private and institutional lenders

- Stay current on OSFI rule changes and Bank of Canada rate movements, as both directly affect the cost and availability of multi-family financing in 2026

The investors who move decisively in 2026 — using private mortgages to bridge the gap between opportunity and bank-ready stabilization — will be best positioned to capture the rental upside that analysts are projecting for 2028 and beyond [2][9].

References

[1] Toronto Private Mortgage Rates 2026 What Homeowners Really Pay And How To Get Approved Fast – https://www.lendworth.ca/blog/lendworth-blog-1/toronto-private-mortgage-rates-2026-what-homeowners-really-pay-and-how-to-get-approved-fast-486

[2] How Will The Canadian Rental Market Enter 2026 – https://valery.ca/blog/how-will-the-canadian-rental-market-enter-2026/

[3] Private Lending In Canada 2026 What Mortgage Brokers Need To Know About OSFI’s New Rules – https://www.keycap.ca/blog/private-lending-in-canada-2026-what-mortgage-brokers-need-to-know-about-osfis-new-rules

[4] Mortgage Delinquency Crisis In Toronto 2026 When Should Private Mortgages Replace Traditional Renewals – https://everythingmortgages.ca/blog/mortgage-delinquency-crisis-in-toronto-2026-when-should-private-mortgages-replace-traditional-renewals/

[6] Private Lending In 2026 Why More Canadians Will Choose Equity Based Financing – https://www.lendworth.ca/blog/lendworth-blog-1/private-lending-in-2026-why-more-canadians-will-choose-equity-based-financing-529

[7] Why Investors Are Choosing Private Mortgages Over Condos In 2026 – https://www.lendworth.ca/blog/lendworth-blog-1/why-investors-are-choosing-private-mortgages-over-condos-in-2026-591

[8] Canada Rent Trends 2026 Forecast Outlook – https://www.tenantpay.com/blogs/canada-rent-trends-2026-forecast-outlook

[9] 2026 Canadian Real Estate Lenders Report – https://www.cbre.ca/-/media/project/cbre/dotcom/americas/canada-emerald/insights/Reports/Lenders-report/2026-canadian-real-estate-lenders-report-e