March 12, 2026

Self-Employed Mortgage Delinquency Risks in Toronto 2026: Warning Signs and Prevention Strategies

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s mortgage landscape in 2026 has reached a critical inflection point. Mortgage arrears have surged 322% since Q3 2022, with 2,797 homeowners now in arrears—the highest level seen in over 12 years.[1] For self-employed professionals navigating this crisis, the risks are even more pronounced. Income volatility, alternative documentation challenges, and the looming June 2026 renewal wave create a perfect storm that threatens financial stability for contractors, freelancers, and business owners across the Greater Toronto Area.

Understanding Self-Employed Mortgage Delinquency Risks in Toronto 2026: Warning Signs and Prevention Strategies isn’t just about avoiding default—it’s about proactively protecting the homeownership dreams that self-employed Canadians have worked so hard to achieve. With over 1 million mortgages renewing from historic 2021 lows of 1.77% to current rates around 3.84%, and analysts projecting that 30% of June 2026 renewers could miss their first payment[1], the time to act is now.

Key Takeaways

- 🚨 Toronto mortgage arrears quadrupled from 662 homeowners in Q3 2022 to 2,797 by Q3 2025, with self-employed borrowers facing amplified vulnerability due to income documentation challenges

- ⚠️ Three critical warning signs from the Bank of Canada signal imminent default risk: using credit cards for groceries, exceeding 33% credit utilization, and making only minimum payments[4]

- 📅 The 120-180 day window before mortgage renewal is critical for self-employed borrowers to explore alternative documentation options and prevent credit damage

- 💰 Alternative lending solutions including bank statement loans and private mortgages provide emergency bridges, though at higher costs (8-14% vs. 4-5% traditional rates)[1]

- 📊 Income volatility management through strategic documentation and working with specialized brokers significantly improves approval odds during the 2026 renewal crisis

Understanding the Self-Employed Mortgage Delinquency Crisis in Toronto 2026

The mortgage delinquency landscape in Toronto has fundamentally shifted. What began as a gradual increase in arrears has accelerated into a full-blown crisis, with Power of Sale listings surging 543% since 2022.[1] For self-employed borrowers, this crisis presents unique challenges that traditional employees simply don’t face.

The Scale of the Problem

The numbers paint a sobering picture. Toronto’s delinquency rate has climbed to 0.24% by late 2025, representing thousands of households struggling to maintain their mortgage obligations. The Office of the Superintendent of Financial Institutions (OSFI) reports particularly elevated delinquencies in “business for self” investor mortgage portfolios[2], directly highlighting self-employed borrower vulnerability.

The Greater Toronto Area’s weaker labour market compared to other major Canadian cities further compounds the problem, limiting households’ ability to manage rising mortgage payments.[3] For self-employed professionals whose income naturally fluctuates with market conditions, client contracts, and seasonal variations, this environment creates exceptional pressure.

Why Self-Employed Borrowers Face Amplified Risks

Self-employed mortgage holders navigate several unique vulnerability factors:

Income Volatility: Unlike salaried employees with predictable bi-weekly paycheques, self-employed income varies month-to-month. A strong Q4 2025 doesn’t guarantee similar performance in Q1 2026, yet mortgage payments remain constant regardless of revenue fluctuations.

Documentation Challenges: Traditional lenders require T4 slips and employment letters—documents self-employed borrowers simply don’t have. When renewal time arrives and circumstances have changed, proving income becomes significantly more difficult than it was during the original approval.

Tax Optimization Consequences: Many self-employed professionals legitimately minimize taxable income through business deductions. While this strategy reduces tax liability, it also reduces the income shown on tax returns—the primary document traditional lenders use for qualification. This creates a paradox where financially successful business owners appear “income-poor” on paper.

Variable Rate Exposure: Variable rate fixed payment mortgages (VRMFPs) show higher delinquencies[2], and self-employed borrowers who opted for these products during the low-rate environment of 2020-2021 now face payment shock as rates have climbed.

For guidance on navigating these challenges, our Ultimate Guide to Securing a Mortgage for Self-Employed Canadians provides comprehensive strategies tailored to business owners and contractors.

The June 2026 Renewal Wall

The most critical pressure point arrives in June 2026, when a massive wave of mortgages secured at pandemic-era lows come due for renewal. Borrowers who locked in at 1.77% in 2021 now face rates more than double that figure. For a $500,000 mortgage, this translates to hundreds of dollars in additional monthly payments—a manageable increase for stable-income households, but potentially devastating for self-employed borrowers experiencing a slow business quarter.

The lag effect compounds the problem. CMHC forecasts that arrears lag renewals by 6 to 12 months[1], meaning the full impact of 2025 renewals may not appear in delinquency statistics until late 2026. This delayed reaction creates a false sense of security for some borrowers who haven’t yet felt the full weight of their new payment obligations.

Warning Signs Every Self-Employed Borrower Must Recognize

The Bank of Canada has identified three critical warning signs that signal imminent mortgage default risk.[4] For self-employed borrowers in Toronto, recognizing these red flags early can mean the difference between proactive problem-solving and reactive crisis management.

Warning Sign #1: Using Consumer Credit for Essential Expenses

When credit cards become necessary for groceries, utilities, or other basic living expenses, financial stress has crossed from manageable to critical. This pattern indicates that current income no longer covers fundamental household needs, forcing debt accumulation just to maintain day-to-day life.

For self-employed professionals, this often manifests during slow business periods. A contractor might experience a gap between project completions, or a freelancer might face delayed client payments. The temptation to “bridge the gap” with credit cards seems reasonable in the moment, but it signals that cash flow management has broken down.

Action Required: If credit cards are covering essentials, it’s time to immediately review all expenses, contact your mortgage lender about hardship programs, and explore alternative mortgage solutions before the situation deteriorates further.

Warning Sign #2: Credit Utilization Exceeding 33%

Credit utilization—the percentage of available credit being used—becomes dangerous when it crosses the 33% threshold. At this level, credit scores begin declining, future borrowing becomes more expensive, and the debt spiral accelerates.

For example, if total credit card limits equal $30,000, carrying balances above $10,000 signals financial strain. Self-employed borrowers often maintain higher credit lines for business expenses, making it easier to unconsciously drift into dangerous utilization territory.

The Self-Employed Trap: Business expenses charged to personal credit cards can quickly inflate utilization rates, especially when client payments arrive late or project invoicing extends beyond 30 days. What appears as “normal business operations” to the borrower appears as “high credit risk” to lenders.

Action Required: Prioritize paying down credit balances below 30% utilization, separate business and personal expenses, and consider a line of credit for business cash flow management rather than revolving credit cards.

Warning Sign #3: Making Only Minimum Payments

When only minimum payments are manageable, debt is no longer being repaid—it’s being maintained. Minimum payments primarily cover interest charges, leaving principal balances virtually unchanged month after month.

This warning sign is particularly insidious because it feels like responsible behavior. “I’m making my payments on time,” borrowers tell themselves. But minimum payments on a $10,000 credit card balance at 19.99% APR would take over 30 years to repay and cost more than $20,000 in interest.

For self-employed borrowers facing the 2026 renewal crisis, this pattern indicates insufficient cash flow to handle both current debt obligations and the increased mortgage payment that renewal will bring.

Action Required: If only minimum payments are possible, mortgage renewal at traditional rates may not be feasible. This is the moment to explore bank statement loans or consult with a specialized mortgage broker who understands self-employed borrower challenges.

Additional Warning Signs Specific to Self-Employed Borrowers

Beyond the Bank of Canada’s three primary indicators, self-employed professionals should watch for:

- Declining business revenue trends over consecutive quarters

- Increasing reliance on business lines of credit for operating expenses

- Delayed invoicing or payment collection becoming the norm rather than the exception

- Mixing personal and business finances to cover gaps in either area

- Avoiding financial planning or refusing to review mortgage renewal terms

Recognizing these patterns early provides the critical window needed to implement prevention strategies before credit damage occurs.

Prevention Strategies for Self-Employed Mortgage Holders

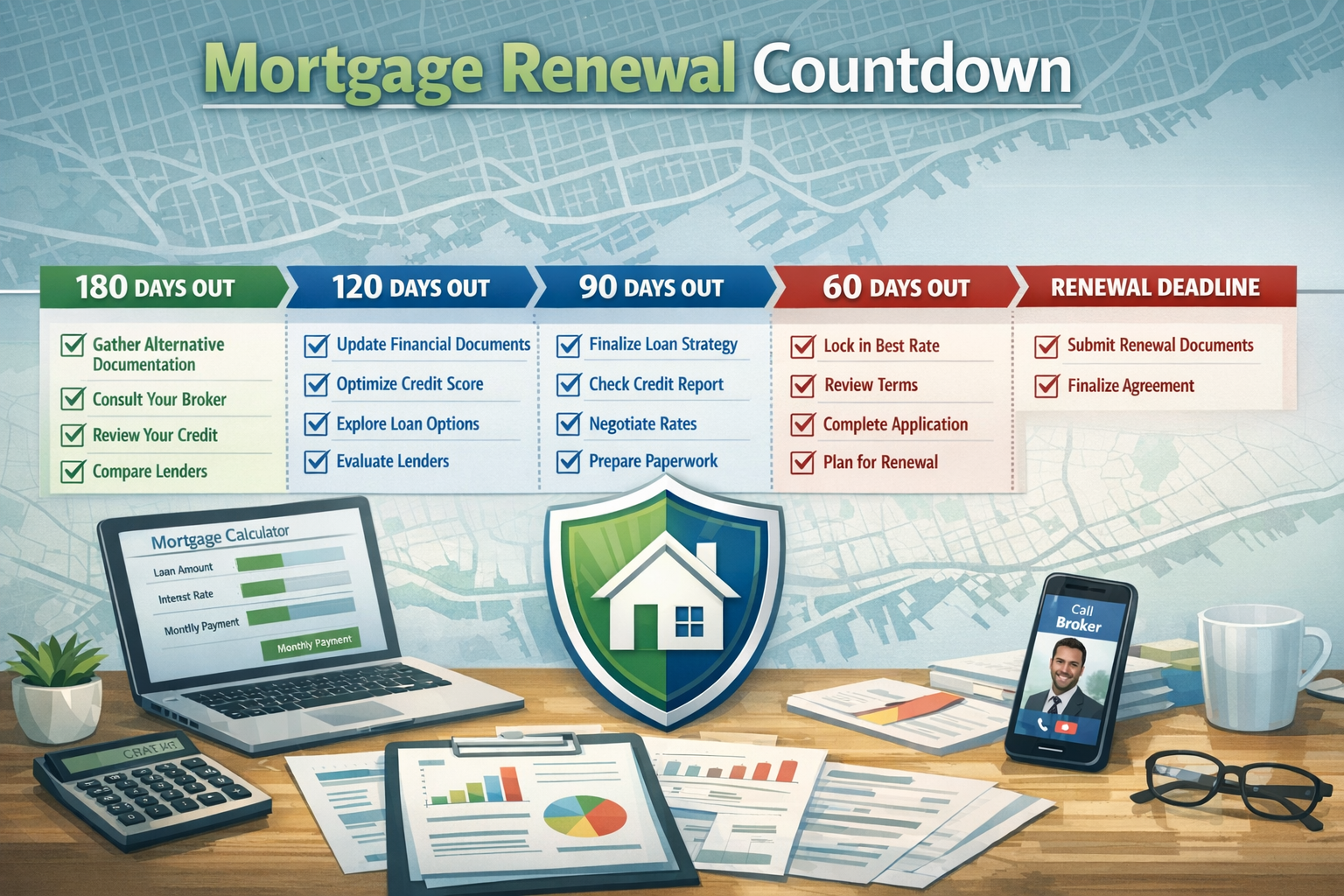

Prevention is exponentially more effective than crisis management. For self-employed borrowers facing the 2026 renewal challenge, implementing these strategies 120-180 days before renewal provides the best opportunity for successful outcomes.

Strategy #1: Start the Renewal Process Early (180 Days Out)

The 120-180 day window before mortgage maturity is critical.[1] After 90 days of arrears, credit reports are impacted and B-lender options close, dramatically limiting available solutions.

Action Steps:

- Mark your calendar six months before renewal date

- Request your current mortgage statement and renewal terms

- Pull your credit report to identify any issues requiring correction

- Begin gathering alternative income documentation

Self-employed borrowers need extra time because documentation requirements are more complex. Unlike traditional employees who can provide a recent pay stub, self-employed professionals must compile business financial statements, bank statements, and tax returns—a process that can take weeks.

Strategy #2: Build Alternative Income Documentation

Traditional lenders want T4s and employment letters. Self-employed borrowers need to build equivalent proof through alternative documentation:

Bank Statement Programs: Many lenders now offer bank statement loans that use 12-24 months of business bank deposits to calculate income. This approach bypasses tax return limitations and reflects actual business cash flow.

Stated Income Programs: Some alternative lenders offer programs where borrowers with strong credit and substantial equity can qualify based on stated income with minimal documentation. These typically require:

- Credit scores above 680

- Loan-to-value ratios below 80%

- Demonstrated industry experience

Contract-Based Income: For contractors with long-term agreements, providing client contracts can demonstrate income stability. Our guide for self-employed contractors details how to leverage contract documentation effectively.

Professional Designation Leverage: Certain professions receive preferential treatment. Self-employed lawyers, doctors, and accountants often qualify for programs with reduced documentation requirements based on professional credentials.

Strategy #3: Optimize Your Financial Profile

Six months before renewal, implement these optimization tactics:

Credit Score Enhancement:

- Pay down credit card balances below 30% utilization

- Ensure all payments are on-time (set up automatic payments)

- Don’t close old credit accounts (credit history length matters)

- Dispute any errors on credit reports immediately

Debt Consolidation: If consumer debt is high, consider debt consolidation strategies before renewal. Consolidating high-interest credit cards into a lower-rate product improves cash flow and debt service ratios.

Income Presentation Strategy: Work with an accountant to present income in the most favorable light. This might involve:

- Adding back legitimate business expenses that don’t affect cash flow (depreciation, vehicle allowances)

- Demonstrating income trends showing growth or stability

- Providing context for any anomalous low-income years

Strategy #4: Explore Refinancing and Switching Options

Don’t assume you must renew with your current lender. Mortgage refinancing and switching at renewal can provide significant advantages for self-employed borrowers.

Benefits of Switching:

- Access to more competitive rates

- Lenders specializing in self-employed borrowers

- Opportunity to consolidate high-interest debt

- Potential to access home equity for business investment

Timing Consideration: Begin shopping for alternative lenders 120-150 days before renewal. This provides adequate time for application, underwriting, and approval without rushing into unfavorable terms.

Strategy #5: Create a Cash Flow Buffer

Income volatility is the defining challenge for self-employed mortgage holders. Creating a dedicated mortgage payment reserve fund provides crucial stability.

Implementation:

- Calculate 6 months of mortgage payments

- Open a separate high-interest savings account

- Contribute systematically during high-income months

- Draw from this reserve during slow periods only for mortgage payments

This buffer transforms unpredictable income into predictable mortgage payments, eliminating the stress of wondering whether this month’s revenue will cover housing costs.

Strategy #6: Consider Alternative Lending Solutions Proactively

If traditional renewal appears unlikely, exploring alternatives before missing payments preserves more options:

B-Lenders: These institutions specialize in borrowers who don’t fit traditional criteria. Rates are typically 0.5-1.5% higher than A-lenders, but qualification is more flexible. Our resource on easier qualification for self-employed borrowers explains this pathway.

Private Mortgages: For borrowers with substantial equity but temporary income challenges, private mortgages charge 8-14% interest rates plus fees.[1] While expensive, they provide a short-term bridge (typically 1-2 years) to stabilize finances before returning to traditional lending.

Credit Unions: Some credit unions offer more flexible underwriting for self-employed members, particularly those with existing banking relationships. Building this relationship before renewal provides another option.

Emergency Solutions When Prevention Wasn’t Enough

Despite best efforts, some self-employed borrowers find themselves facing renewal with insufficient time to implement prevention strategies. When crisis arrives, these emergency solutions can prevent foreclosure.

Private Mortgage Bridge Strategy

Private mortgages serve as emergency bridges for asset-rich but cash-strapped borrowers.[1] While expensive (8-14% interest plus 2-5% in fees), they prevent foreclosure and provide time to rebuild qualification for traditional lending.

Ideal Candidates:

- Substantial home equity (typically 30%+ required)

- Temporary income disruption with clear recovery path

- Strong business fundamentals despite recent poor financial results

- Willingness to pay premium rates for 12-24 months

Cost Example: A $400,000 private mortgage at 10% costs approximately $3,333 monthly in interest alone, compared to $1,333 at 4%. The additional $2,000 monthly cost is significant, but far less expensive than losing the home to foreclosure.

Exit Strategy Required: Private mortgages are not long-term solutions. Borrowers must have a clear plan to return to traditional lending within 1-2 years, whether through improved income documentation, business recovery, or property sale.

Bank Statement Loan Programs

Bank statement loans analyze business deposits over 12-24 months to calculate qualifying income. This approach works well for self-employed borrowers whose tax returns don’t reflect true earning capacity.

Qualification Process:

- Provide 12-24 months of business bank statements

- Lender calculates average monthly deposits

- Applies expense ratio (typically 25-50%) to determine net income

- Underwrites based on calculated income

Advantages:

- Bypasses tax return limitations

- Reflects current business performance

- Faster approval than traditional documentation

- Rates closer to traditional mortgages than private options

Requirements:

- Minimum credit score (typically 600-680)

- Maximum loan-to-value ratio (usually 80-90%)

- Consistent deposit patterns showing business activity

- Reasonable debt service ratios

Hardship Programs and Lender Negotiations

Many traditional lenders offer hardship programs for borrowers experiencing temporary financial difficulties. These programs are underutilized because borrowers don’t know they exist or fear that requesting help will damage their relationship with the lender.

Available Options:

- Payment deferrals: Skipping 1-3 months of payments (interest still accrues)

- Extended amortization: Stretching remaining balance over longer period to reduce payments

- Interest-only periods: Temporarily paying only interest to reduce monthly obligations

- Blended rates: Combining current low rate with new higher rate for gradual adjustment

How to Request: Contact your lender’s retention department (not regular customer service) before missing payments. Explain the situation, demonstrate it’s temporary, and propose a specific solution. Lenders prefer workout arrangements over foreclosure proceedings.

Selling Before Foreclosure

When mortgage payments are truly unsustainable, strategic sale before foreclosure preserves credit and maximizes equity recovery. Power of Sale proceedings damage credit for years and typically result in lower sale prices.

Strategic Sale Advantages:

- Control over timing and pricing

- Preservation of credit score

- Recovery of remaining equity

- Avoidance of legal costs and lender fees

Timing: List the property immediately when it becomes clear renewal won’t work. The Toronto market requires 30-90 days for sale completion, and waiting until foreclosure proceedings begin eliminates this option.

Conclusion: Taking Control of Self-Employed Mortgage Delinquency Risks in Toronto 2026

The mortgage delinquency crisis gripping Toronto in 2026 presents unprecedented challenges for self-employed borrowers, but it doesn’t have to result in foreclosure. With mortgage arrears up 322% and the critical June 2026 renewal wave approaching, the time for action is now—not later.[1]

Self-employed professionals face amplified risks from income volatility and documentation challenges, but these obstacles are surmountable with proper planning and expert guidance. The three warning signs identified by the Bank of Canada—using credit for groceries, exceeding 33% credit utilization, and making only minimum payments—provide clear indicators that intervention is needed.[4]

Your Action Plan Starting Today

If your renewal is 6+ months away:

- Begin gathering alternative income documentation immediately

- Review and optimize your credit profile

- Create a 6-month mortgage payment reserve fund

- Consult with a specialized self-employed mortgage broker

If your renewal is 3-6 months away:

- Contact your current lender about renewal terms today

- Shop alternative lenders who specialize in self-employed borrowers

- Explore bank statement loan programs as backup options

- Pay down consumer debt aggressively to improve debt service ratios

If your renewal is within 90 days:

- Engage a mortgage broker immediately—time is critical

- Prepare alternative documentation packages

- Consider all options including B-lenders and private mortgages

- Request hardship program information from current lender

If you’re already struggling with payments:

- Contact your lender’s retention department before missing payments

- Explore private mortgage bridge solutions if you have substantial equity

- Consult with a mortgage professional about refinancing options

- Consider strategic sale if payments are truly unsustainable

The mortgage landscape has fundamentally changed, but self-employed borrowers who act proactively, recognize warning signs early, and leverage specialized expertise can successfully navigate the 2026 renewal crisis. Your self-employment status is a strength, not a weakness—it simply requires different strategies and documentation approaches.

Don’t wait until crisis becomes catastrophe. The 120-180 day window before renewal is your opportunity to implement prevention strategies that protect your home and financial future. With Toronto’s delinquency rates at historic highs and the renewal wave intensifying, the borrowers who thrive will be those who took action early, sought expert guidance, and refused to let income volatility derail their homeownership dreams.

References

[1] Mortgage Delinquency Crisis In Toronto 2026 When Should Private Mortgages Replace Traditional Renewals – https://everythingmortgages.ca/blog/mortgage-delinquency-crisis-in-toronto-2026-when-should-private-mortgages-replace-traditional-renewals/

[2] Annual Risk Outlook Semi Annual Update Fiscal Year 2025 2026 – https://www.osfi-bsif.gc.ca/en/about-osfi/reports-publications/annual-risk-outlook-semi-annual-update-fiscal-year-2025-2026

[3] Mortgage Renewal Wave Strains Some Regions Borrowers – https://www.cmhc-schl.gc.ca/observer/2026/mortgage-renewal-wave-strains-some-regions-borrowers

[4] Watch – https://www.youtube.com/watch?v=PMEJjgmzh78