March 14, 2026

Self-Employed Variable Rate Mortgages in Toronto: Should You Lock in 3.45%-3.95% Before Rates Rise?

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage landscape in Toronto has reached a critical inflection point in 2026. Self-employed borrowers who secured variable rate mortgages are now facing a pivotal decision: should they lock in current rates between 3.45% and 3.95%, or ride out the variable rate wave as economic forecasts hint at potential increases? With the Bank of Canada holding its overnight rate at 2.25% but market analysts predicting upward pressure by year-end, understanding Self-Employed Variable Rate Mortgages in Toronto: Should You Lock in 3.45%-3.95% Before Rates Rise? has never been more important for contractors, consultants, doctors, and other independent professionals navigating Toronto’s competitive real estate market.

The stakes are particularly high for self-employed individuals. Unlike traditional employees with straightforward T4 income verification, self-employed borrowers face stricter qualification requirements and often pay slightly higher rates. This makes timing decisions around rate locks even more critical—a difference of just 0.50% on a $700,000 mortgage can mean thousands of dollars annually.

Key Takeaways

- 💰 Current variable rates for self-employed borrowers in Toronto range from 3.45% to 3.95%, with the lowest rates available through specialized lenders and brokers [1]

- 📈 Rate forecasts suggest the Bank of Canada overnight rate could rise from 2.25% to 2.5% by end of 2026, potentially pushing variable rates to approximately 3.6% [3]

- ⚖️ Self-employed borrowers face unique qualification challenges requiring two years of tax returns and higher documentation standards, making rate decisions more consequential

- 🎯 Locking in now provides payment certainty during a period of economic uncertainty, while staying variable offers potential savings if rate cuts resume

- ⏰ The decision window is narrowing—with the next Bank of Canada rate announcement on March 18, 2026, borrowers have limited time to assess their options [2]

Understanding Self-Employed Variable Rate Mortgages in Toronto’s Current Market

Variable rate mortgages operate differently than their fixed-rate counterparts. Rather than locking in a specific interest rate for the entire mortgage term, variable rates fluctuate based on the lender’s prime rate, which typically moves in tandem with the Bank of Canada’s overnight rate.

For self-employed professionals in Toronto, accessing these variable rates requires meeting more stringent criteria than traditional employees. Most lenders require:

- Two years of Notice of Assessments (NOAs) from the Canada Revenue Agency

- Business financial statements showing consistent or growing income

- Higher credit scores (typically 680+ for A-lenders, though alternative lenders may accept lower scores)

- Larger down payments (often 20% minimum to avoid mortgage insurance complications)

Current Rate Landscape for Self-Employed Borrowers

As of March 2026, the variable rate mortgage market presents the following picture:

| Lender Type | Variable Rate Range | Typical Self-Employed Premium |

|---|---|---|

| Big 6 Banks | 3.95% – 4.90% | +0.20% – 0.50% |

| Credit Unions | 3.65% – 4.25% | +0.15% – 0.35% |

| Monoline Lenders | 3.45% – 3.85% | +0.10% – 0.25% |

| Alternative Lenders | 4.50% – 6.50% | +0.50% – 2.00% |

The lowest advertised 5-year variable rate in Canada currently sits at 3.35% [1], though self-employed borrowers typically face a premium of 0.10% to 0.50% depending on their financial profile and documentation strength.

Major banks like RBC are offering variable rates around 3.95%, while Scotiabank’s rates reach as high as 4.90% [2]. For self-employed professionals with strong financials and comprehensive documentation, working with mortgage brokers who have access to monoline lenders can secure rates in the 3.45% to 3.75% range—a significant savings opportunity.

Why Self-Employed Borrowers Pay More

The premium charged to self-employed borrowers reflects perceived risk factors:

- Income volatility: Business income can fluctuate year-over-year

- Tax optimization strategies: Many self-employed individuals minimize reported income for tax purposes, reducing qualifying income

- Documentation complexity: Verifying self-employed income requires more extensive review

- Default risk perception: Historical data shows slightly higher default rates among self-employed borrowers during economic downturns

However, professionals like self-employed doctors and IT consultants with stable client bases and strong earnings often qualify for rates very close to standard employed rates.

Rate Forecast Analysis: Should You Lock in Self-Employed Variable Rate Mortgages in Toronto Before Rates Rise?

Understanding whether to lock in Self-Employed Variable Rate Mortgages in Toronto: Should You Lock in 3.45%-3.95% Before Rates Rise? requires examining both current conditions and future projections.

Current Bank of Canada Position

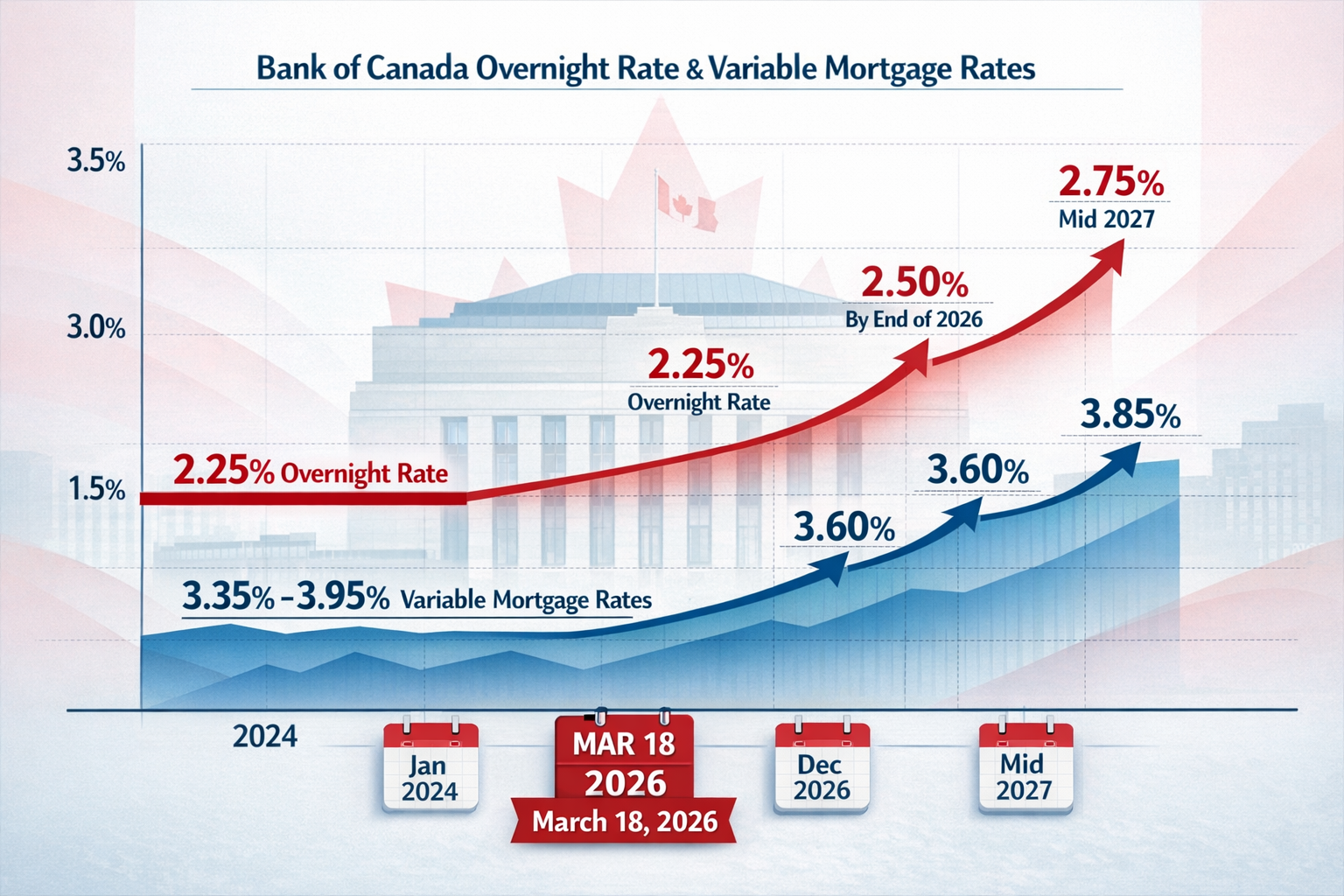

The Bank of Canada has held its overnight rate at 2.25% as of January 28, 2026, with the next policy decision scheduled for March 18, 2026 [2]. This represents a significant decrease from the peak rates of 2023-2024, providing relief to variable rate mortgage holders who weathered the storm of aggressive rate hikes.

However, the rate hold stance signals a shift from the cutting cycle that dominated late 2024 and early 2025. Governor Tiff Macklem has indicated that further cuts are unlikely in the near term as the Bank monitors:

- Inflation stability around the 2% target

- Economic growth indicators

- Employment data

- Global economic conditions and trade tensions

Expert Rate Forecasts Through 2027

Multiple forecasting agencies have published projections for the Bank of Canada overnight rate:

End of 2026 Projections:

- Oxford Economics predicts the BoC rate will remain at 2.25% through the remainder of 2026 [4]

- Bond market pricing suggests a 30% probability of a rate increase to 2.5% by December 2026 [3]

- If rates rise to 2.5%, 5-year variable mortgage rates would likely climb to approximately 3.6% [3]

Mid-2027 Projections:

- Forecasts suggest the BoC overnight rate could reach 2.75% by mid-2027 [3]

- Corresponding 5-year variable rates would rise to approximately 3.85% [3]

- This represents a potential increase of 0.50% from current levels

What This Means for Self-Employed Borrowers

For a self-employed professional with a $700,000 mortgage at a current variable rate of 3.45%, here’s what rate increases could mean:

| Scenario | Interest Rate | Monthly Payment | Annual Cost | 5-Year Total |

|---|---|---|---|---|

| Current Rate | 3.45% | $3,112 | $37,344 | $186,720 |

| End 2026 Forecast | 3.60% | $3,180 | $38,160 | $190,800 |

| Mid 2027 Forecast | 3.85% | $3,289 | $39,468 | $197,340 |

| Worst Case | 4.25% | $3,461 | $41,532 | $207,660 |

Calculations based on 25-year amortization

The difference between locking in at 3.45% today versus facing a 3.85% rate in 2027 amounts to $177 per month or $2,124 annually—a significant consideration for self-employed individuals managing variable business income.

Understanding Payment Shock for Renewals

The Bank of Canada has warned that borrowers renewing mortgages in 2026 face an average payment increase of 20% [6]. For self-employed professionals who may have secured ultra-low rates during the pandemic era (sub-2%), renewal at current rates represents substantial payment shock.

For those exploring options to manage this transition, understanding current self-employed mortgage rates in Toronto provides valuable context for both refinancing and renewal decisions.

Evaluating Your Lock-In Decision: Risk Scenarios and Strategic Considerations

The decision to lock in Self-Employed Variable Rate Mortgages in Toronto: Should You Lock in 3.45%-3.95% Before Rates Rise? isn’t purely mathematical—it requires assessing personal risk tolerance, financial stability, and business outlook.

When Locking In Makes Sense

✅ Consider locking in if you:

- Have variable business income with seasonal fluctuations that make budgeting challenging

- Operate in an uncertain industry where economic downturns could impact revenue

- Value payment certainty over potential savings from rate decreases

- Are close to your maximum debt servicing capacity and can’t absorb payment increases

- Plan to hold the property long-term (5+ years) and want stability

- Are approaching retirement or a major life transition requiring predictable expenses

For example, a self-employed contractor in Toronto’s construction industry might prioritize payment stability during uncertain economic conditions, making a lock-in at 3.65% attractive compared to the risk of rates climbing to 3.85% or higher.

When Staying Variable Makes Sense

✅ Consider staying variable if you:

- Have stable, predictable business income with strong cash reserves

- Can comfortably absorb payment increases of 15-20% without financial stress

- Believe rate cuts may resume if economic conditions deteriorate

- Have a shorter time horizon (planning to sell or refinance within 2-3 years)

- Want to maintain lower penalties for early payoff (variable mortgages typically have 3-month interest penalties vs. IRD calculations for fixed)

- Are financially disciplined and will use savings from lower rates to accelerate principal payments

Self-employed professionals with insurable mortgage rates and strong qualification metrics may have more flexibility to ride out variable rate fluctuations.

The Hybrid Approach: Rate Hold Options

Many lenders offer rate hold periods ranging from 90 to 120 days, allowing borrowers to secure a fixed rate while maintaining their variable mortgage temporarily. This strategy provides:

- Time to monitor the March 18, 2026 Bank of Canada decision

- Flexibility to lock in if rates begin rising

- No commitment if economic conditions shift favorably

For self-employed borrowers, working with experienced mortgage brokers who understand self-employed mortgage rate trends can unlock access to these strategic options.

Calculating Your Break-Even Point

To determine whether locking in makes financial sense, calculate your break-even point:

- Identify the rate differential: Current variable rate vs. available fixed rate

- Calculate monthly payment difference: How much more would you pay with a fixed rate?

- Estimate rate increase timing: When do forecasts suggest variable rates will exceed the fixed rate?

- Factor in penalty costs: What would it cost to break your current mortgage?

Example Calculation:

- Current variable rate: 3.45%

- Available fixed rate: 3.95%

- Monthly payment difference: $175 on a $700,000 mortgage

- Forecasted variable rate in 12 months: 3.60%

In this scenario, you’d pay an extra $2,100 in the first year by locking in at 3.95%. However, if rates rise to 3.85% by mid-2027, you’d start saving money compared to staying variable. The break-even occurs approximately 18-24 months into the term.

Special Considerations for Different Self-Employed Profiles

🏗️ Contractors and Tradespeople: Economic sensitivity makes payment stability valuable. Consider locking in if residential construction activity shows signs of slowing. Review our guide on self-employed mortgages for contractors for qualification strategies.

💻 Tech Consultants and IT Professionals: Often have stable corporate clients and predictable income. May benefit from staying variable if cash flow is strong. Learn more about IT consultant mortgage options.

⚕️ Medical Professionals: Doctors and healthcare practitioners typically have extremely stable income. Can often qualify for the best rates and may benefit from variable rate savings. See our specialized guide for self-employed doctors.

📊 Business Owners and Entrepreneurs: Income volatility varies widely. Those with established businesses (5+ years) may have more flexibility than startups. Consider both business growth projections and personal risk tolerance.

Taking Action: Next Steps for Self-Employed Borrowers in Toronto

Whether you decide to lock in your variable rate or maintain flexibility, taking informed action requires a strategic approach tailored to self-employed circumstances.

Step 1: Assess Your Current Mortgage Terms

Review your existing mortgage agreement to understand:

- Current variable rate and lender: Who holds your mortgage and what rate are you paying?

- Remaining term length: How much time is left before renewal?

- Prepayment privileges: Can you make lump sum payments or increase monthly payments?

- Conversion options: Does your lender allow penalty-free conversion to fixed rates?

- Penalty calculations: What would it cost to break your mortgage early?

Many variable rate mortgages include conversion clauses allowing borrowers to switch to fixed rates without penalties—a valuable feature if you decide to lock in.

Step 2: Update Your Financial Documentation

Self-employed borrowers need current documentation ready for any mortgage changes:

- ✅ Most recent two years of Notice of Assessments (NOAs)

- ✅ Current year business financial statements (if available)

- ✅ Six months of business bank statements

- ✅ Credit report (check for errors that could impact rates)

- ✅ Proof of down payment or equity (if refinancing)

Having documentation organized accelerates the approval process and may help secure better rates. For those with less than traditional documentation, explore alternative documentation options.

Step 3: Compare Multiple Lender Options

Don’t limit yourself to your current lender. Self-employed borrowers should compare:

A-Lenders (Big Banks and Credit Unions):

- Best rates for borrowers with strong documentation

- Strictest qualification requirements

- Current range: 3.45% – 4.25% for well-qualified self-employed

B-Lenders (Alternative Lenders):

- More flexible income verification

- Slightly higher rates but easier approval

- Explore B-lender mortgage rates in Toronto

Monoline Lenders:

- Competitive rates without branch overhead

- Available exclusively through mortgage brokers

- Often offer the best rates for self-employed borrowers

Specialized Programs:

- Bank statement loan programs for those with limited tax documentation

- DSCR loans for real estate investors

Step 4: Consult with a Specialized Mortgage Broker

Working with a mortgage broker experienced in self-employed mortgages provides significant advantages:

- Access to 30+ lenders including those not available to consumers directly

- Understanding of self-employed documentation requirements and optimization strategies

- Rate negotiation leverage based on volume and lender relationships

- Guidance on timing for rate locks and conversions

- No cost to borrowers (brokers are compensated by lenders)

A skilled broker can often secure rates 0.20% to 0.50% lower than borrowers obtain independently—potentially saving thousands over the mortgage term.

Step 5: Monitor Economic Indicators

Stay informed about factors influencing rate decisions:

- Bank of Canada announcements: Next decision March 18, 2026 [2]

- Inflation reports: Monthly CPI data from Statistics Canada

- Employment figures: Job market strength influences rate policy

- Global economic conditions: International factors affect Canadian rates

Understanding how 2026 mortgage rate forecasts impact self-employed homebuyers helps contextualize your decision within broader economic trends.

Step 6: Create Multiple Scenarios

Develop a financial plan for different rate environments:

Conservative Scenario (Rates Rise to 4.25%):

- Calculate maximum monthly payment

- Identify budget cuts if needed

- Build emergency fund to cover 6 months of payments

Moderate Scenario (Rates Rise to 3.85%):

- Plan for modest payment increases

- Maintain current savings rate

- Continue business growth investments

Optimistic Scenario (Rates Hold or Decrease):

- Use savings to accelerate principal payments

- Build investment portfolio

- Consider property upgrades or additional real estate

Step 7: Make Your Decision with Confidence

After gathering information and consulting professionals, trust your analysis. Remember:

- There’s no perfect decision—only the right decision for your circumstances

- You can adjust later—most mortgages allow refinancing at renewal

- Payment certainty has value—even if you pay slightly more, peace of mind matters

- Business success matters most—mortgage decisions should support, not hinder, business growth

Conclusion

The question of Self-Employed Variable Rate Mortgages in Toronto: Should You Lock in 3.45%-3.95% Before Rates Rise? doesn’t have a one-size-fits-all answer. With the Bank of Canada holding rates at 2.25% through early 2026 but forecasts suggesting potential increases to 2.5% by year-end and 2.75% by mid-2027, self-employed borrowers face a genuine decision window.

For those with variable business income, limited cash reserves, or low risk tolerance, locking in current rates between 3.45% and 3.95% provides valuable payment certainty during uncertain economic times. The potential cost of waiting—an additional 0.40% to 0.50% on your mortgage rate—could translate to thousands of dollars annually on Toronto’s typical mortgage balances.

Conversely, self-employed professionals with stable income, strong financial cushions, and confidence in their business outlook may benefit from maintaining variable rate flexibility. The savings from staying at current rates, combined with lower prepayment penalties, could outweigh the risks of modest rate increases.

Key action items for self-employed borrowers in Toronto:

- 📋 Gather your financial documentation and assess your current mortgage terms

- 📊 Calculate your break-even point comparing lock-in costs versus rate increase scenarios

- 🤝 Consult with a mortgage broker specializing in self-employed mortgages

- ⏰ Monitor the March 18, 2026 Bank of Canada decision for directional signals

- 💰 Compare rates from multiple lenders including monolines and alternative lenders

- ✅ Make your decision based on your unique business situation and risk tolerance

The mortgage market in 2026 offers opportunities for strategic self-employed borrowers who act decisively with proper guidance. Whether you choose to lock in current favorable rates or maintain variable rate flexibility, ensure your decision aligns with both your business trajectory and personal financial goals.

Don’t navigate this critical decision alone. Connect with mortgage professionals who understand the unique challenges and opportunities facing self-employed borrowers in Toronto’s dynamic real estate market. The right mortgage strategy today can save you thousands tomorrow while providing the financial stability to focus on what matters most—growing your business and building wealth.

References

[1] Variable – https://www.ratehub.ca/best-mortgage-rates/5-year/variable

[2] Variable Mortgage Rates – https://www.nerdwallet.com/ca/p/best/mortgages/variable-mortgage-rates

[3] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[4] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast

[5] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/

[6] Staff Analytical Note 2025 21 – https://www.bankofcanada.ca/2025/07/staff-analytical-note-2025-21/