March 14, 2026

Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Securing a mortgage as a self-employed professional in Toronto can feel like navigating a maze blindfolded. While traditional employees simply present their T4 slips and move forward, entrepreneurs face a more complex journey—especially when business income fluctuates from year to year. The reality is stark: Toronto’s median household income sits at approximately $98,000 annually, yet qualifying for an average mortgage requires between $162,000-$190,000 depending on down payment and rates[1]. This gap of nearly $95,000 creates a significant barrier for self-employed individuals.

However, there’s a powerful strategy that many self-employed borrowers overlook: income averaging. Understanding Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates can transform your mortgage application from a rejection into an approval. Lenders increasingly use two-year income averaging to assess self-employed applicants, but success depends on how you position your fluctuating income without aggressive tax planning that could backfire.

Key Takeaways

✅ Two-year income averaging is the standard method lenders use to evaluate self-employed mortgage applicants, smoothing out revenue fluctuations to determine qualifying income

💰 Strategic income documentation can maximize your borrowing power—understanding which income sources lenders count and how they calculate averages is crucial

📊 Multiple qualification pathways exist beyond traditional tax returns, including 6-month bank deposit history for those with inconsistent annual filings

🏠 Proper preparation with the right documents and timing can increase approval odds by 40-60% compared to unprepared applications

🎯 Working with specialized mortgage professionals who understand self-employed income structures dramatically improves your chances of securing favorable terms

Understanding How Lenders Calculate Income for Self-Employed Borrowers

When it comes to Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates, the foundation lies in understanding exactly how lenders evaluate your income. Unlike salaried employees who present a straightforward annual salary, self-employed individuals require a more nuanced assessment.

The Two-Year Income Standard

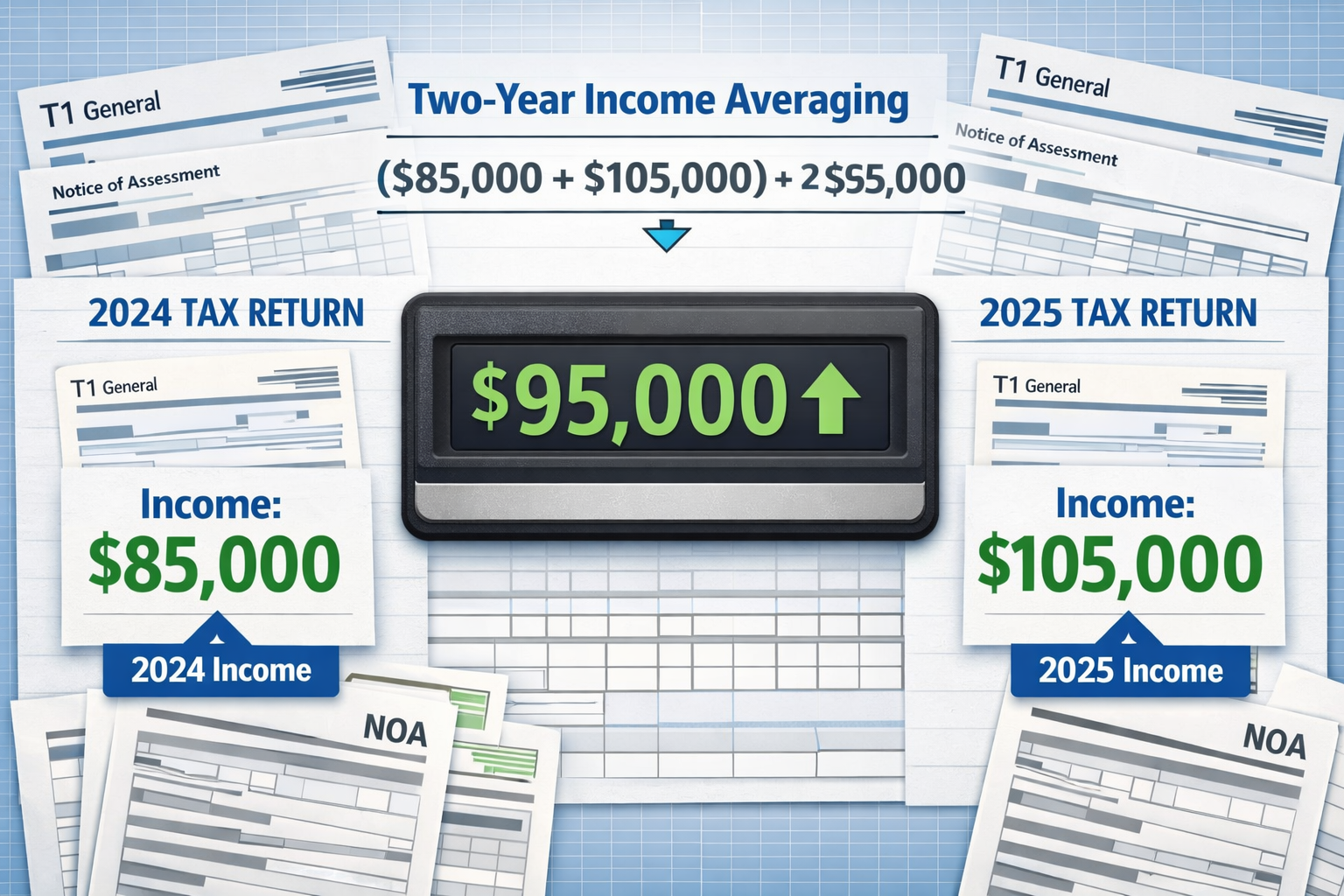

The most common approach lenders use is two-year income averaging. This method requires sole proprietors to provide at least 2 years of income confirmation from T1 tax returns and Notices of Assessment (NOAs)[2]. For incorporated individuals, the requirement extends to 2 years of T1s plus business financial statements[2].

Here’s how the calculation typically works:

Example Income Averaging Calculation:

- Year 1 (2024): Net business income of $85,000

- Year 2 (2025): Net business income of $105,000

- Average qualifying income: $95,000

This averaging approach benefits borrowers whose income has increased over time, as it smooths out the lower-earning year while still reflecting current earning capacity.

Personal vs. Business Income Assessment

Lenders evaluate both personal taxable income (what the business pays you) and total business income/revenue to understand your complete financial picture[3]. This dual assessment helps lenders gauge your ability to make consistent mortgage payments.

For incorporated business owners, lenders may consider:

- Salary drawn from the corporation

- Dividends received

- Retained earnings (in some cases)

- Business net income before personal compensation

Debt-to-Income Ratio Requirements

Regardless of how your income is calculated, lenders typically target a Total Debt Service (TDS) ratio of 32-42%[3]. This means your mortgage payment, property taxes, heating costs, and other debt obligations should not exceed 42% of your qualifying income.

Using our $95,000 averaged income example:

- Maximum monthly debt payments: $3,325 (at 42% TDS)

- If you have $500 in other debts, your maximum mortgage payment: $2,825

This calculation determines your maximum borrowing capacity and explains why accurate income documentation is so critical for self-employed borrowers seeking Toronto mortgages.

For more comprehensive guidance on navigating self-employed mortgage applications, explore our Ultimate Guide to Securing a Mortgage for Self-Employed Canadians.

Essential Documentation Requirements for Income Averaging Success

Mastering Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates requires meticulous documentation. The difference between approval and rejection often comes down to having the right paperwork prepared in advance.

Core Documentation Package

Self-employed borrowers must typically provide a comprehensive documentation package that includes[3]:

Tax Documentation:

- 📄 T1 General tax returns for the past 2 years (minimum)

- 📄 Notices of Assessment (NOAs) from the Canada Revenue Agency for corresponding years

- 📄 T2 corporate tax returns (if incorporated) for the past 2 years

- 📄 Business financial statements including profit and loss statements

Business Verification:

- 🏢 Business license or registration documents

- 🏢 Articles of incorporation (for incorporated businesses)

- 🏢 GST/HST registration (if applicable)

- 🏢 Professional liability insurance (for certain professions)

Income Verification:

- 💵 Bank deposit slips showing regular business income

- 💵 Customer invoices demonstrating ongoing revenue

- 💵 Business bank statements for 6-12 months

- 💵 Accounts receivable documentation

Asset and Liability Documentation:

- 💰 Personal bank statements (3-6 months)

- 💰 Investment account statements

- 💰 Credit report authorization

- 💰 List of current debts and obligations

Alternative Documentation for Fluctuating Income

For self-employed individuals experiencing significant income fluctuations, there’s good news: sole proprietors without verifiable taxed income can qualify with a minimum of 6 months of business deposit history[2]. This alternative pathway offers flexibility for those with inconsistent annual tax filings or rapidly growing businesses.

This approach is particularly valuable for:

- New business owners who haven’t filed 2 years of returns yet

- Entrepreneurs who reinvest heavily in business growth

- Contractors with seasonal income patterns

- Freelancers with variable project-based revenue

Maximizing Your Income Documentation

To optimize your income averaging results, consider these strategic approaches:

Timing Your Application:

- Apply after filing taxes for your strongest income year

- Ensure NOAs are received before starting the mortgage process

- Consider waiting if next year’s income will significantly improve your average

Income Presentation:

- Highlight consistent revenue streams separately from one-time projects

- Document recurring clients or contracts

- Provide context for income fluctuations (seasonal business, major contract completion)

Professional Support:

- Work with an accountant who understands mortgage qualification

- Consult with a mortgage broker experienced in self-employed applications

- Prepare explanatory letters for unusual income patterns

For those navigating the complexities of self-employed income documentation, our guide on Innovative Mortgage Solutions for Self-Employed Canadians provides additional strategies and options.

Strategic Approaches to Maximize Approval Odds with Fluctuating Revenue

Understanding Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates means knowing which strategic approach best fits your unique financial situation. Not all self-employed borrowers should follow the same path.

Three Primary Qualification Pathways

1. Traditional Income Verification (Prime Lending)

This pathway offers the best rates and terms but requires the most stringent documentation:

- ✅ Requirements: 2+ years of T1s and NOAs showing consistent income

- ✅ Borrowing capacity: Up to 95% of home value with mortgage default insurance or 80% without insurance[2]

- ✅ Interest rates: Prime rates (currently 4-5% range in 2026)

- ✅ Best for: Established businesses with stable, documented income

2. Alternative Income Documentation (B-Lenders)

This middle ground offers flexibility while maintaining reasonable rates:

- 📊 Requirements: 6 months of bank deposit history, business license, credit score 600+

- 📊 Borrowing capacity: Typically up to 80% of home value

- 📊 Interest rates: Slightly higher (5-7% range)

- 📊 Best for: Growing businesses with strong cash flow but lower taxable income

3. Stated Income Programs (Private Lending)

This pathway prioritizes assets and equity over income documentation:

- 🔐 Requirements: Larger down payment (20-35%), strong credit, significant assets

- 🔐 Borrowing capacity: Typically 65-80% of home value

- 🔐 Interest rates: Higher (7-10% range plus fees)

- 🔐 Best for: High-net-worth individuals, complex income structures, short-term solutions

Optimizing Your Income Average Without Aggressive Tax Planning

Many self-employed individuals face a dilemma: minimizing taxes versus maximizing mortgage qualification. Here’s how to balance both objectives:

Strategic Income Timing:

- Consider taking higher personal income in the 1-2 years before applying for a mortgage

- Balance salary vs. dividend payments to optimize both tax efficiency and qualifying income

- Document retained earnings that demonstrate business stability

Business Structure Considerations:

- Incorporated individuals should evaluate whether accessing subprime mortgages (7-10% rates) might be more cost-effective than paying income taxes on gross declared income necessary to qualify for prime rates[2]

- Calculate the total cost difference between higher taxes for prime lending vs. higher interest for alternative lending

- Consider the long-term implications of each approach

Income Enhancement Strategies:

- Document all income sources lenders will consider (rental income, investment income, part-time employment)

- Ensure consistent monthly deposits rather than irregular large payments

- Maintain clean separation between personal and business finances

Leveraging CMHC Self-Employed Programs

The Canada Mortgage and Housing Corporation (CMHC) offers Self-Employed mortgage loan insurance with flexible income and employment requirements at no extra cost[4]. This program can be particularly valuable for self-employed borrowers who meet traditional down payment requirements but face income documentation challenges.

Key advantages include:

- Access to insured mortgage rates (typically lower)

- Acceptance of alternative income verification methods

- No premium surcharge for self-employed status

- Ability to qualify with down payments as low as 5%

Understanding Lender-Specific Policies

Not all lenders treat self-employed income equally. Some important distinctions:

- Mortgage amount caps: Some lenders cap self-employed mortgages at $500,000 and up, while others make discretionary decisions with no stated upper limits[3]

- Income calculation methods: Different lenders may weight salary, dividends, and business income differently

- Industry preferences: Certain lenders favor specific professions or business types

- Relationship lending: Some institutions offer preferential treatment to long-standing business banking clients

Working with a mortgage broker who understands these lender-specific nuances can significantly improve your approval odds. Our article on Mortgages for Self-Employed Borrowers explores these differences in greater detail.

Common Mistakes to Avoid When Applying with Fluctuating Income

Even with a solid understanding of Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates, many self-employed borrowers make critical errors that derail their applications.

Top Application Mistakes

1. Writing Off Too Many Expenses

While tax minimization is smart business practice, excessive write-offs can devastate your mortgage application. Lenders base qualification on net income after expenses, not gross revenue.

❌ Mistake: Writing off $80,000 in expenses on $120,000 revenue, leaving only $40,000 qualifying income

✅ Better approach: Balance tax savings with mortgage qualification needs in the 1-2 years before applying

2. Inconsistent Income Patterns

Large fluctuations without clear explanation raise red flags for lenders.

❌ Mistake: $150,000 income in Year 1, $45,000 in Year 2 (average: $97,500, but concerning trend)

✅ Better approach: Provide context explaining the fluctuation (major contract completion, business expansion costs, etc.)

3. Poor Record Keeping

Missing documentation can delay or derail your application entirely.

❌ Mistake: Unable to provide complete bank statements, missing invoices, disorganized records

✅ Better approach: Maintain organized financial records year-round, not just when applying

4. Applying Too Soon

Rushing the application before establishing adequate income history is a common error.

❌ Mistake: Applying after just one year of self-employment

✅ Better approach: Wait until you have at least 2 years of filed returns with NOAs (unless using alternative documentation)

5. Ignoring Credit Score Impact

Self-employed borrowers face higher scrutiny, making credit scores even more critical.

❌ Mistake: Applying with credit score below 650

✅ Better approach: Improve credit to 680+ before applying for best rates and approval odds

For comprehensive guidance on avoiding application pitfalls, review our article on Common Mistakes to Avoid When Applying for a Mortgage in Canada.

Timing Your Application Strategically

The timing of your mortgage application can significantly impact your approval odds:

Optimal Application Windows:

- 📅 After tax season: Once you’ve received NOAs for your most recent tax year

- 📅 Following strong income years: When your 2-year average reflects improved earnings

- 📅 Before major business changes: Prior to restructuring, expansion, or other transitions that might complicate income verification

- 📅 During rate-favorable periods: When mortgage rates are declining or stable

Situations to Delay Application:

- ⏸️ Recent business incorporation or structure change

- ⏸️ Significant income decline in most recent year

- ⏸️ Outstanding tax issues or unfiled returns

- ⏸️ Recent credit issues or high debt loads

Working with Specialized Professionals

Perhaps the most critical success factor is partnering with professionals who understand self-employed mortgage qualification:

Mortgage Broker Benefits:

- Access to multiple lenders with varying self-employed policies

- Experience positioning fluctuating income favorably

- Knowledge of alternative lending options

- Ability to match your situation with the right lender

Accountant Collaboration:

- Strategic tax planning that considers future mortgage needs

- Proper income documentation and presentation

- Business structure optimization

- Income timing strategies

For self-employed professionals in Toronto, working with specialists who understand both the local market and self-employed challenges is invaluable. Learn more about how to work with a mortgage broker in Toronto to maximize your approval chances.

Actionable Steps to Improve Your Mortgage Qualification Today

Now that you understand Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates, it’s time to take concrete action. Here’s your step-by-step roadmap to mortgage approval success.

Immediate Actions (Next 30 Days)

Week 1-2: Assessment and Organization

- Gather your documentation: Collect the past 2-3 years of T1s, NOAs, business financial statements, and bank statements

- Calculate your current income average: Determine what lenders will see based on your recent tax returns

- Review your credit report: Obtain a free credit report and identify any issues requiring attention

- Estimate your borrowing capacity: Use your averaged income and the 32-42% TDS ratio to calculate your maximum mortgage amount

Week 3-4: Professional Consultation

- Connect with a mortgage broker: Schedule consultations with 2-3 brokers specializing in self-employed mortgages

- Consult your accountant: Discuss your mortgage timeline and income optimization strategies

- Get pre-qualified: Obtain informal pre-qualification to understand your current standing

- Identify gaps: Determine what documentation or improvements are needed before formal application

Short-Term Strategies (3-6 Months)

Income Optimization:

- 💼 Adjust your income draw to improve your 2-year average if possible

- 💼 Document all income sources consistently (maintain regular deposit patterns)

- 💼 Prepare explanatory letters for any income fluctuations

- 💼 Consider accelerating income or deferring expenses strategically

Credit Improvement:

- 📈 Pay down credit card balances below 30% utilization

- 📈 Make all payments on time (set up automatic payments)

- 📈 Avoid opening new credit accounts

- 📈 Dispute any errors on your credit report

Documentation Preparation:

- 📋 Organize all financial documents in clearly labeled folders

- 📋 Create a business overview document explaining your income model

- 📋 Compile client contracts or recurring revenue documentation

- 📋 Prepare business licenses and incorporation documents

Medium-Term Planning (6-12 Months)

Financial Positioning:

- 🎯 Build your down payment to at least 20% to avoid insurance premiums

- 🎯 Reduce debt-to-income ratio by paying down existing debts

- 🎯 Establish 3-6 months of reserves (lenders view this favorably)

- 🎯 Maintain consistent business banking patterns

Business Structure Optimization:

- 🏢 Consider whether incorporation or sole proprietorship better serves your mortgage goals

- 🏢 Evaluate salary vs. dividend mix for optimal tax and qualification balance

- 🏢 Ensure business financial statements are professionally prepared

- 🏢 Document business stability (client retention, recurring contracts)

Market Research:

- 🏘️ Research Toronto neighborhoods within your budget

- 🏘️ Monitor mortgage rate trends and lock in when favorable

- 🏘️ Understand property tax and maintenance costs in target areas

- 🏘️ Calculate total homeownership costs including insurance and utilities

For additional insights on maximizing your self-employed mortgage approval, explore our resources on Tax Smarts and Maximizing Benefits for the Self-Employed in Canada.

Long-Term Success Strategies

Ongoing Financial Management:

- Maintain clean separation between personal and business finances

- Keep detailed records of all income and expenses year-round

- File taxes on time every year without exception

- Build relationships with lenders through business banking

Renewal and Refinancing Preparation:

- Remember that mortgage renewals require re-qualification

- Plan income strategies for renewal years (typically every 5 years)

- Monitor your income trends and address declining patterns early

- Consider renewal options well before your term expires

Building Lender Relationships:

- Establish business banking relationships with potential mortgage lenders

- Maintain good standing with all financial institutions

- Consider consolidating banking to demonstrate financial stability

- Communicate proactively about business changes or challenges

Conclusion

Mastering Income Averaging for Self-Employed Toronto Mortgage Qualification: Maximizing Approval Odds When Business Revenue Fluctuates is entirely achievable with the right knowledge and preparation. While self-employed borrowers face additional scrutiny compared to traditional employees, understanding how lenders calculate income averages and what documentation they require puts you in control of the process.

The key insights to remember:

🔑 Two-year income averaging is the standard qualification method, smoothing revenue fluctuations to determine your borrowing capacity

🔑 Multiple qualification pathways exist beyond traditional documentation, including alternative lenders and stated income programs for those with complex situations

🔑 Strategic preparation with proper documentation, timing, and professional guidance can dramatically improve approval odds

🔑 Balance is essential between tax minimization and mortgage qualification—plan ahead to optimize both objectives

As Toronto’s housing market continues to evolve in 2026, self-employed professionals who understand these income averaging principles position themselves for success. The gap between median household income and mortgage qualification requirements remains significant, but with proper planning and expert guidance, homeownership is within reach.

Your Next Steps:

- Assess your current position using the frameworks outlined in this article

- Gather your documentation and calculate your 2-year income average

- Connect with specialized professionals who understand self-employed mortgage qualification

- Develop a timeline that aligns your business income planning with your homeownership goals

- Take action today to improve your qualification profile for tomorrow’s opportunities

The journey to mortgage approval as a self-employed borrower requires more preparation than traditional employment, but the reward—homeownership in one of Canada’s most dynamic cities—makes the effort worthwhile. With income averaging strategies, proper documentation, and expert guidance, your fluctuating business revenue becomes a manageable challenge rather than an insurmountable obstacle.

Ready to take the next step? Connect with mortgage professionals who specialize in self-employed applications and start building your path to Toronto homeownership today.

References

[1] Watch – https://www.youtube.com/watch?v=ly-w0bTlAwg

[2] Self Employed Mortgage Options Qualifications In Canada – https://www.nesto.ca/mortgage-basics/self-employed-mortgage-options-qualifications-in-canada/

[3] Self Employed – https://rates.ca/guides/mortgage/self-employed

[4] Self Employed – https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/self-employed