March 16, 2026

FSRA-Covered vs Unregulated Private Lenders in Toronto: How to Vet Safe Funding When You’re Under Pressure

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

;

Toronto’s private lending market has exploded — and so has the risk. When a deal is closing fast, a bank says no, or a mortgage renewal deadline looms, the pressure to sign quickly can override common sense. That’s exactly when unscrupulous lenders strike. Understanding FSRA-Covered vs Unregulated Private Lenders in Toronto: How to Vet Safe Funding When You’re Under Pressure is not just a compliance exercise — it’s financial self-defense.

Key Takeaways 📌

- FSRA-licensed mortgage brokers and lenders must follow strict conduct rules; unregulated private lenders operate with almost no oversight.

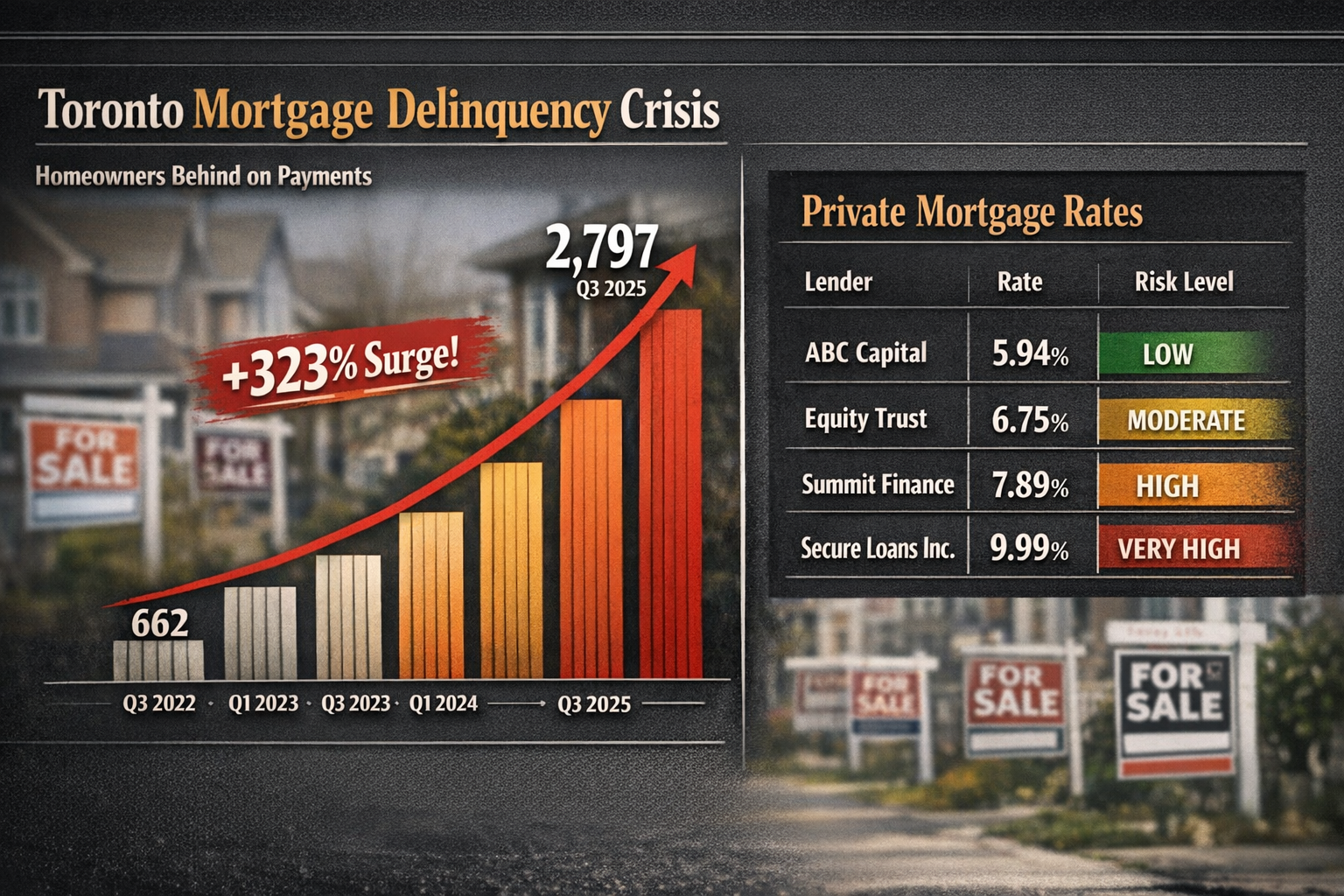

- Toronto mortgage arrears quadrupled between Q3 2022 and Q3 2025, making borrower vetting more critical than ever.

- Private mortgage rates in Ontario currently range from 5.94% to 9.99% — a massive spread driven by lender type and borrower risk profile [7].

- FSRA’s 2025–2026 supervision plan flags private mortgages as a key risk area, with 65% of brokerages showing documentation failures [10].

- A simple due-diligence checklist can protect borrowers from predatory deals even when time is short.

Why Toronto’s Private Lending Market Demands Extra Caution

The private lending landscape in Ontario has grown dramatically. The total value of private lending jumped 72% from $13 billion in 2019 to over $22 billion in 2021 [2]. In Toronto, nearly 1 in 11 mortgages originated from a private lender as recently as 2018, up from a 4.9% market share in 2016 to 6.7% by 2018 [2].

That growth has not come without consequences. Toronto mortgage arrears quadrupled from 662 homeowners in Q3 2022 to 2,797 by Q3 2025 — a 323% increase in just three years [4]. Marina Walsh, MBA Vice President of Industry Analysis, attributes rising delinquencies to a “softer labour market, other personal debt obligations, and increases in taxes, homeowners’ insurance and other fees that exacerbate already stretched affordability.” Private mortgage borrowers face amplified vulnerability because their payment obligations are already higher.

The Bank of Canada’s March 2026 Financial Stability Assessment reinforced this concern, warning that “weakness in private credit could spill back to the regulated sector” — signalling that regulatory attention on private lenders will only intensify.

💬 “Private mortgages should be viewed as a bridge, not a destination — with refinancing planned from day one.” — Manzeel Patel, Award-Winning Mortgage Broker, Everything Mortgages [4]

For borrowers navigating these waters, understanding B-lender mortgage rates in Toronto is a smart first step before jumping to private options entirely.

FSRA-Covered vs Unregulated Private Lenders: What’s Actually Different?

The FSRA Framework: What Protection Looks Like

The Financial Services Regulatory Authority of Ontario (FSRA) governs mortgage brokers, agents, and lenders under the Mortgage Brokerages, Lenders and Administrators Act, 2006 (MBLAA). FSRA-covered participants must:

| Requirement | FSRA-Licensed | Unregulated |

|---|---|---|

| License verification | ✅ Public registry | ❌ None |

| Suitability assessment | ✅ Mandatory | ❌ Optional |

| Disclosure of fees | ✅ Required | ❌ Varies |

| Complaint process | ✅ Formal pathway | ❌ Civil court only |

| Conduct standards | ✅ Enforced | ❌ None |

FSRA issued a critical warning in early 2026: mortgage brokers must renew their licenses by March 31, 2026, with business disruption threatened for non-compliance [10]. This enforcement action signals heightened regulatory scrutiny across the brokerage sector.

FSRA’s 2025–2026 Supervision Plan has designated private mortgages as a key area of supervisory focus, citing rising delinquency rates and increasing financial pressure on vulnerable borrowers. Alarmingly, approximately 65% of brokerages engaged in private lending had missing, incomplete, or inconsistent suitability assessments — a 9% increase from the previous examination cycle [10].

The Unregulated Side: Where the Risks Hide

Unregulated private lenders — sometimes called “hard money lenders” or informal private investors — operate outside FSRA’s reach. They may include:

- Individual investors lending personal capital

- Loosely structured syndicates or joint ventures

- Foreign capital operators with no Canadian registration

- Online platforms that match borrowers with anonymous funders

These lenders are not inherently fraudulent, but the absence of oversight creates fertile ground for predatory terms, hidden fees, and aggressive default enforcement. The Homebuyers Privacy Protection Act, which took effect March 4, 2026, now restricts how lenders can use mortgage-related inquiry data in prescreen programs without express consumer authorization [3] — but unregulated operators may simply ignore this rule.

Current private mortgage rates in Ontario range from 5.94% (Altrua Financial) to 9.99% (Corwin Capital), with institutional lenders like MFC and Westborough sitting at 6.69% [7]. That 4.05 percentage point spread within the private market alone tells a powerful story: who you borrow from matters enormously.

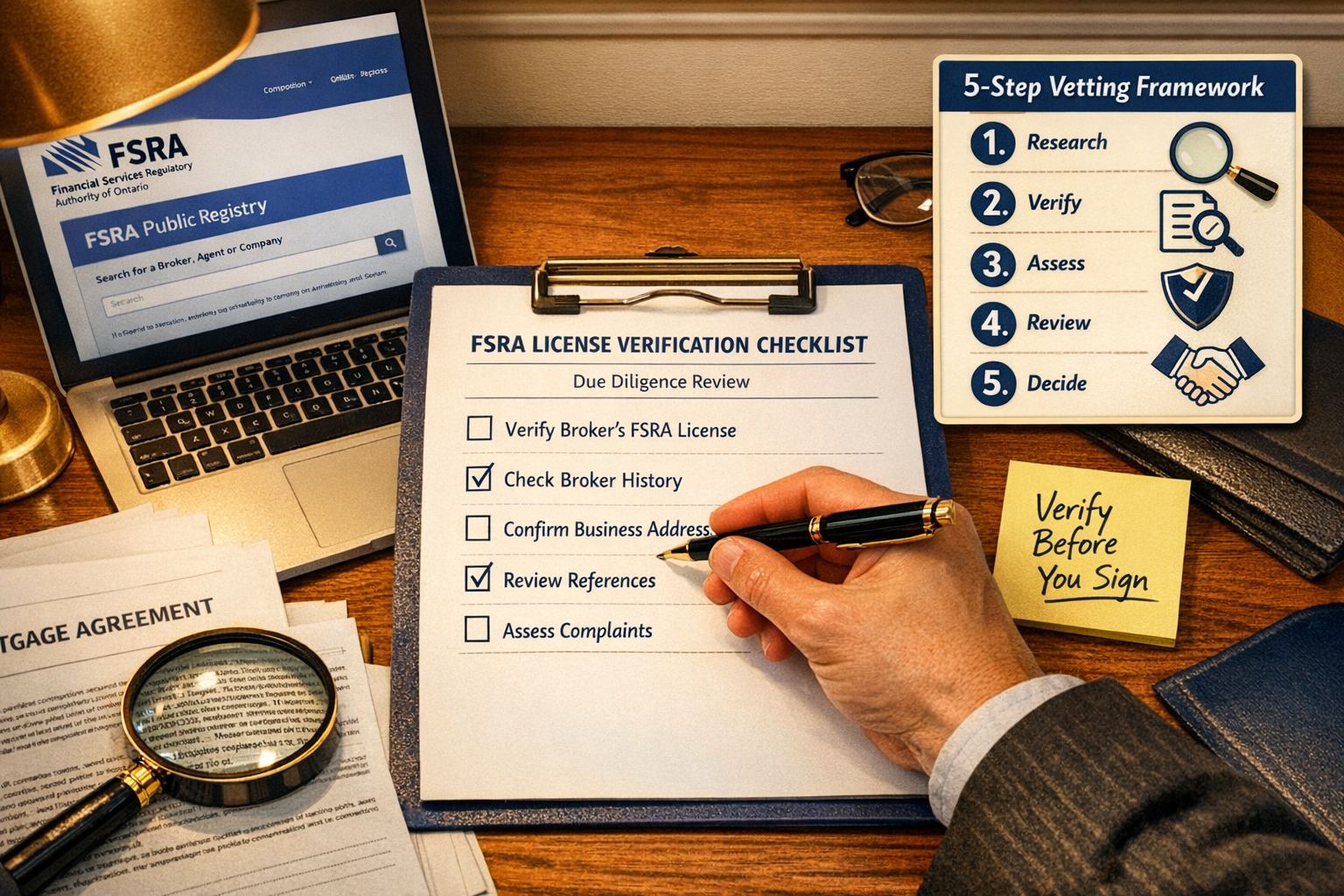

How to Vet Safe Funding When You’re Under Pressure: A Practical Checklist

When time is short, a structured checklist prevents costly mistakes. Here is a 5-step due-diligence framework for Toronto borrowers evaluating any private lender.

✅ Step 1: Verify the FSRA License

Search the FSRA public registry at fsrao.ca before any conversation goes further. Confirm:

- The brokerage or lender holds a valid, current licence

- The individual broker or agent is listed under that brokerage

- No disciplinary actions or conditions are attached to the licence

⚠️ Red flag: Any lender who discourages you from checking their licence status.

✅ Step 2: Demand a Suitability Assessment in Writing

FSRA-licensed brokers are required to document why a private mortgage is suitable for your situation. If a broker skips this step — or rushes past it — that is a serious warning sign, especially given that 65% of brokerages already fail this requirement [10].

For self-employed borrowers especially, a proper suitability review should reference your income documentation and long-term refinancing pathway. See documentation requirements for self-employed mortgage approval in Toronto for what a thorough review should include.

✅ Step 3: Get Full Fee Disclosure Before Signing

Private mortgages carry costs beyond the interest rate:

- Lender fees: 1–3% of the loan amount

- Broker fees: 1–2% (must be disclosed under MBLAA)

- Legal fees: Both lender’s and borrower’s counsel

- Renewal/extension fees: Often 1–2% per term

Ask for a complete cost of borrowing statement in writing. Unregulated lenders frequently bury fees in complex term sheets.

✅ Step 4: Understand the Exit Strategy Before You Enter

Private mortgages are typically 6–12 month bridge instruments. Before signing, confirm:

- What are the refinancing conditions at term end?

- Does the lender have renewal discretion (can they refuse to renew)?

- Is there a prepayment penalty, and how is it calculated?

Reviewing 2026 mortgage rate forecasts can help borrowers time their exit to a conventional mortgage strategically. The Bank of Canada held its benchmark rate at 2.25% through March 2026, with Scotiabank forecasting a potential rise to 2.75% by year-end [1] — a relatively stable environment for planning a refinance.

✅ Step 5: Run an Independent Legal Review

Never use the lender’s recommended lawyer exclusively. Retain independent legal counsel to review:

- Mortgage commitment letter terms

- Default and enforcement clauses

- Power of sale triggers

This is especially important given Canada’s expanding AML framework in real estate and lending [5], which places additional obligations on professionals involved in private transactions.

Safer Alternatives Worth Exploring First

Before committing to a private deal, Toronto borrowers should exhaust regulated alternatives:

- B-lenders and credit unions — More flexible than major banks, still FSRA/OSFI supervised

- Mortgage Investment Corporations (MICs) — Regulated under the Income Tax Act, often more transparent than informal private lenders

- Refinancing existing equity — Explore home equity and how to use it as a lower-cost bridge

- CMHC-insured products — Note that CMHC’s February 2026 MLI Select overhaul raised ground-up construction insurance premiums from 4–5% to approximately 7% [1], so factor updated costs into any new construction plan

For those navigating the self-employed borrower landscape, innovative mortgage solutions for self-employed Canadians outlines several regulated pathways that may eliminate the need for private lending entirely.

Also worth reviewing: common mistakes to avoid when applying for a mortgage — many borrowers turn to private lenders unnecessarily because of application errors that a qualified broker could have resolved.

Conclusion: Pressure Is Not an Excuse to Skip Due Diligence

The urgency of a closing deadline or a bank rejection can feel overwhelming — but that pressure is precisely the moment when careful vetting matters most. Understanding FSRA-Covered vs Unregulated Private Lenders in Toronto: How to Vet Safe Funding When You’re Under Pressure is the difference between a strategic bridge loan and a financial trap.

Actionable next steps for Toronto borrowers:

- 🔍 Search the FSRA registry before any lender conversation

- 📋 Demand written suitability documentation from your broker

- 💰 Request a full cost-of-borrowing statement including all fees

- 🚪 Plan your exit strategy before you sign — know your refinancing pathway

- ⚖️ Hire independent legal counsel to review all private mortgage documents

- 🤝 Consult a licensed mortgage broker who can access both regulated and private markets on your behalf

Toronto’s private lending market will continue to grow — and so will the risks for unprepared borrowers. Regulatory oversight is tightening, delinquency rates are climbing, and the cost of choosing the wrong lender has never been higher. Slow down, verify credentials, and always have a plan to get out before you get in.

References

[1] Private Lenders Ontario – https://alpinecredits.ca/alpine-blog/private-lenders-ontario/ [2] Watch – https://www.youtube.com/watch?v=fhmdbl83A-c [3] Mark Your Calendars 2026 Compliance Dates For Consumer And Small Business Financial Services – https://www.huschblackwell.com/newsandinsights/mark-your-calendars-2026-compliance-dates-for-consumer-and-small-business-financial-services [4] Toronto Private Mortgages For Newcomer Investors Navigating 2026 Cmhc Restrictions And Equity Pathways – https://everythingmortgages.ca/blog/toronto-private-mortgages-for-newcomer-investors-navigating-2026-cmhc-restrictions-and-equity-pathways/ [5] Navigating Canada S Expanding Aml Framework In Real Estate And Lending – https://www.blakes.com/insights/navigating-canada-s-expanding-aml-framework-in-real-estate-and-lending/ [7] Private Mortgage Lenders Ontario – https://altrua.ca/private-mortgage-lenders-ontario/ [10] Legislative Review Mortgage Brokerages Lenders And Administrators Act 2006 – https://www.ontario.ca/page/legislative-review-mortgage-brokerages-lenders-and-administrators-act-2006