March 16, 2026

Toronto Private Mortgages for Over-100% LTV Homeowners: Options When You Owe More Than Your House Is Worth

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Imagine buying a Toronto condo in 2022 at the peak of the market — and discovering in 2026 that your property is now worth $80,000 less than your remaining mortgage balance. You can’t sell without bringing a cheque to the closing table. Your bank won’t refinance. And renewal is coming fast. This is the reality for a growing number of Toronto homeowners, and understanding Toronto Private Mortgages for Over-100% LTV Homeowners is the first step toward finding a way out.

This guide explains how negative equity develops, what private lenders will — and won’t — do for underwater borrowers, and the step-by-step workout strategies that can help you avoid power of sale.

Key Takeaways 📌

- Negative equity (LTV over 100%) means your mortgage debt exceeds your home’s current market value — a growing problem in Toronto’s soft condo market in 2026.

- Most private lenders cap LTV at 65–75%, making true over-100% LTV lending extremely rare and expensive [5].

- Private mortgage rates for distressed borrowers can exceed 10% annually, compared to ~6% for traditional lenders [2].

- Workout strategies — loan modifications, capital injections, and joint ventures — are often more practical than layering new debt.

- Proactive action before default is critical; Ontario’s power-of-sale process moves quickly once a lender accelerates [3].

How Negative Equity Develops in Toronto’s Soft Market

When home values fall after purchase, your loan-to-value (LTV) ratio rises. If your outstanding mortgage is $650,000 but your home appraises at $580,000, your LTV is approximately 112% — meaning you owe more than the property is worth [4]. This is called negative equity, and it creates a trap: you can’t sell without cash to cover the shortfall, and most lenders won’t refinance a property with no equity cushion.

In 2026, this scenario is playing out across Toronto — particularly in the downtown condo segment. Small investors who purchased pre-construction units at 2021–2022 prices are now seeing assignment sales close at roughly $100,000 below original purchase prices. Meanwhile, the CMHC’s February 2026 analysis of the mortgage renewal wave flagged Ontario and Toronto as especially vulnerable, with arrears rates expected to rise moderately as borrowers face payment shock at renewal.

💬 “Many would-be sellers are now in negative equity positions and simply can’t afford to discharge their mortgages.” — Toronto market commentators, March 2026

Rising consumer insolvencies are amplifying the problem. Investors and owner-occupiers alike are being squeezed by higher carrying costs, softer rents, and a market that hasn’t bounced back as quickly as many hoped. If you’re in this position, understanding your options — including what private mortgage options exist in Ontario — is essential before making any decisions.

The LTV Math: A Simple Example

| Scenario | Mortgage Balance | Home Value | LTV Ratio | Equity Position |

|---|---|---|---|---|

| Healthy | $500,000 | $700,000 | 71% | +$200,000 |

| Break-even | $600,000 | $600,000 | 100% | $0 |

| Underwater | $650,000 | $580,000 | 112% | -$70,000 |

Once you cross the 100% threshold, conventional refinancing becomes essentially impossible, and even private lenders get very cautious [4].

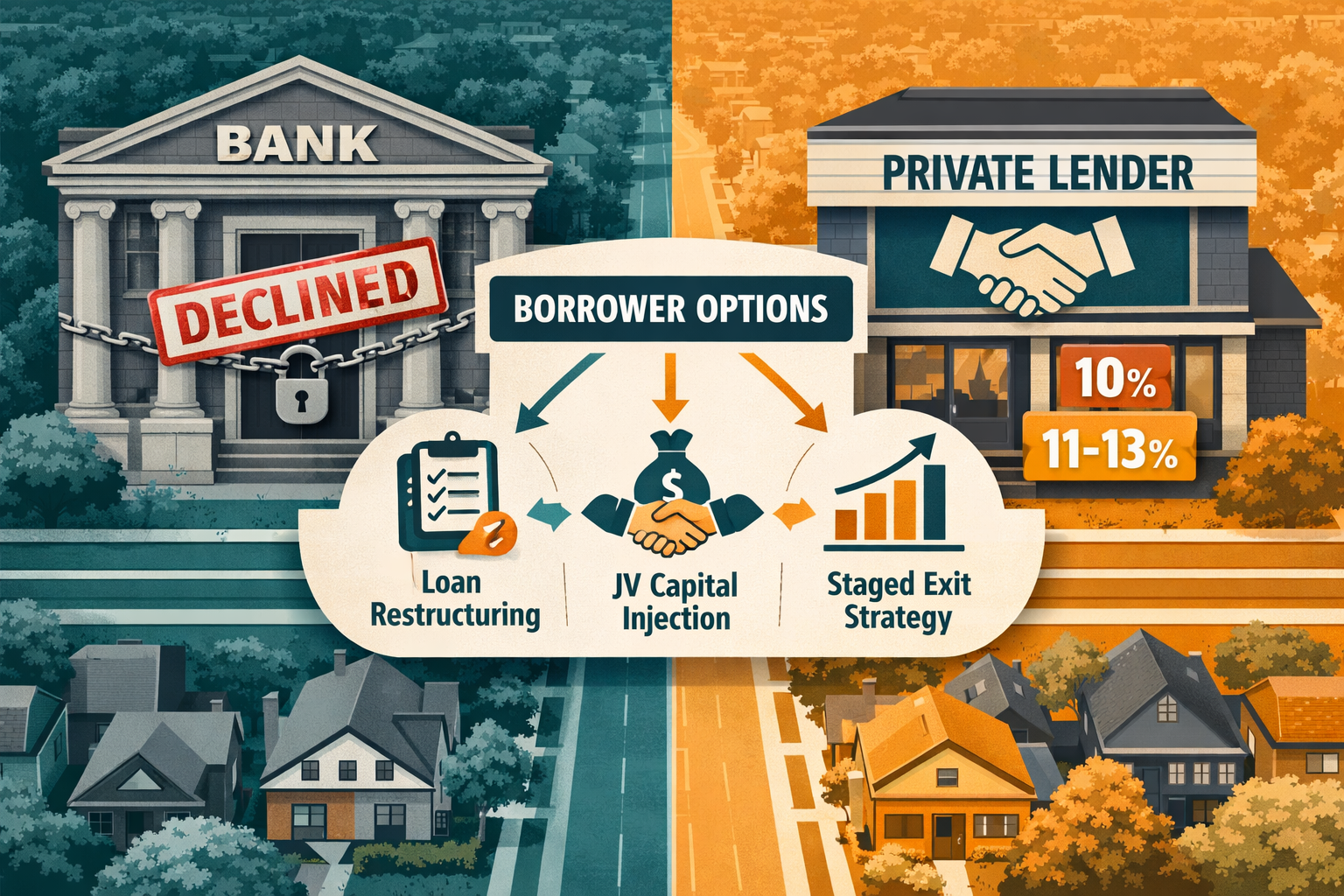

Toronto Private Mortgages for Over-100% LTV Homeowners: What Private Lenders Will (and Won’t) Do

This is where many homeowners get a rude surprise. The idea that private lenders will lend regardless of equity is a myth. Ontario’s private lending market — including mortgage investment corporations (MICs), individual investors, and specialty lenders — operates on strict risk parameters.

The Hard Truth About Private LTV Caps

Private lending law specialists note that prudent Ontario private lenders typically cap first-mortgage LTV at 65–75% and combined first-plus-second mortgage exposure at 80–85% [5]. This “security cushion” protects investors. A homeowner already at 112% LTV on their primary mortgage cannot simply layer a second mortgage on top — there is no collateral value left to secure it [5].

Most Toronto-area private lenders advertising residential products explicitly cap residential LTVs at around 75% on both first and second mortgages [7]. That said, a few niche scenarios exist where private capital may still flow:

✅ When private lenders MAY still engage:

- The property has other assets (a second property, investment portfolio) that can cross-collateralize the loan

- A co-signer or guarantor with strong assets and income is added to the deal

- The borrower can inject external capital (savings, family gift, RRSP withdrawal) to reduce the LTV below 80% before funding

- A joint venture partner buys into the property, effectively reducing the lender’s exposure

- The underwater position is temporary and provable — e.g., a condo closing delayed by construction, with a clear resale or rental exit

❌ When private lenders will almost certainly decline:

- Pure over-100% LTV with no additional collateral

- No verifiable income or exit strategy

- Active power-of-sale proceedings already underway

- Multiple missed payments with no cure plan

💡 Key insight: Private mortgage rates for high-risk files can go well over 10% annually [2]. Under Canada’s 2025 criminal interest rate reforms, the maximum APR is now capped at 35% (down from 60%) [2] — but even at 10–13%, carrying costs on a distressed loan can accelerate financial deterioration.

Ontario’s Financial Services Regulatory Authority (FSRA) has made private mortgage supervision a top priority in its 2025–2026 plan. Brokers arranging private deals for stressed borrowers must now document suitability, disclose total borrowing costs, and explain the exit strategy in detail. This is good news for consumers — it means a reputable broker won’t simply put you into an expensive private loan without ensuring it genuinely helps your situation.

For context on how B-lender mortgage rates in Toronto compare to private options, it’s worth exploring whether a B-lender solution exists before going the private route.

Step-by-Step Workout Strategies for Underwater Toronto Homeowners

If private lending isn’t a clean solution for over-100% LTV situations, what actually works? The answer usually involves a combination of strategies rather than a single product. Here are the most practical paths forward, ranked from least to most disruptive.

Step 1: Contact Your Existing Lender Immediately 📞

Before exploring any external financing, call your current lender. Many banks and credit unions offer loan modification programs that can:

- Capitalize arrears (add missed payments to the principal)

- Extend the amortization period to reduce monthly payments

- Temporarily defer payments during financial hardship

This approach doesn’t increase your LTV further and avoids the high cost of private financing. Ontario’s power-of-sale process gives borrowers a redemption period to cure default — but only if you act before the lender accelerates the full loan balance [3][9]. Proactive contact is everything.

Step 2: Explore Mortgage Restructuring with a Broker

A licensed mortgage broker can assess whether any restructuring options exist — including all about mortgage refinancing strategies that might apply even in partial-equity situations. In some cases, a blended rate refinance or a partial payout arrangement can stabilize payments without requiring full equity.

It’s also worth reviewing your current mortgage terms carefully. Breaking your mortgage early may trigger penalties — understanding how mortgage penalties work before making any moves can save thousands.

Step 3: Inject External Capital to Restore Equity 💰

This is often the most direct path to unlocking private or B-lender financing. If you can reduce your LTV to below 80% by injecting:

- Personal savings or investments

- A family gift or loan

- RRSP withdrawals (with tax planning)

- A private loan secured against other assets

…then conventional private lending becomes available again. Even getting from 112% LTV to 85% LTV opens up a much wider range of lender options.

Step 4: Consider a Joint Venture (JV) Partner

A JV arrangement involves bringing in a capital partner — often a family member, friend, or private investor — who contributes funds in exchange for a share of future appreciation. This isn’t a mortgage product; it’s an equity arrangement. It reduces the lender’s risk exposure and can bridge the gap until the market recovers.

This strategy works best when the property has strong long-term fundamentals — a freehold home in a desirable Toronto neighbourhood, for example, rather than a downtown micro-condo.

Step 5: Staged Exit — Sell When You Can, Not When You Must 🏠

Sometimes the most rational option is to plan a controlled sale rather than wait for a forced power-of-sale. A staged exit might involve:

- Renting out the property (or a suite) to cover carrying costs while you save toward the shortfall

- Adding a legal secondary suite to boost rental income and property value

- Setting a 12–24 month timeline to either recover equity or exit with minimal loss

This approach preserves your credit score and avoids the long-term damage of power of sale. Speaking of credit — if your score has already taken hits, reviewing how to improve your credit score in Canada can help you rebuild eligibility for better financing options down the road.

Step 6: If All Else Fails — Negotiate Power of Sale Terms

If power of sale becomes unavoidable, Ontario law still gives borrowers rights. The lender must follow a specific process, and homeowners retain the right to redeem the property by paying the full amount owing [9]. In some cases, negotiating a voluntary sale (rather than a lender-driven power of sale) can result in better net proceeds and less credit damage [3][6].

Conclusion: Don’t Wait — Act Before Options Disappear

Toronto Private Mortgages for Over-100% LTV Homeowners is not a simple product you can shop for online. It’s a complex situation that requires honest assessment, professional guidance, and a realistic plan. The good news: there are more options than most underwater homeowners realize — but those options shrink rapidly once default proceedings begin.

✅ Actionable Next Steps

- Calculate your current LTV using a recent appraisal or comparable sales — not your purchase price.

- Contact your lender today if you’re struggling with payments; ask specifically about hardship programs and loan modifications.

- Consult a licensed mortgage broker who specializes in distressed situations and understands private loan lenders in Ontario.

- Explore capital injection options — even a partial equity restoration dramatically improves your financing choices.

- Build a written exit strategy with a clear 12–24 month timeline before approaching any private lender.

The 2026 Toronto market is challenging, but underwater homeowners who act proactively — rather than waiting for a rescue product that may not exist — have the best chance of navigating through to the other side.

References

[1] Private Mortgage Lenders Ontario – https://wowa.ca/private-mortgage-lenders-ontario [2] Private Lenders Ontario – https://alpinecredits.ca/alpine-blog/private-lenders-ontario/ [3] Power Of Sale In Ontario What Homeowners Need To Know – https://www.lendtoday.ca/2024/12/power-of-sale-in-ontario-what-homeowners-need-to-know/ [4] Loan To Value – https://rates.ca/guides/mortgage/loan-to-value [5] Private Lending In Ontario – https://pacificlegal.ca/private-lending-in-ontario/ [6] How The Ontario Real Estate Market Affects Power Of Sale Rates 2025 – https://powerofsalesontario.ca/blog/how-the-ontario-real-estate-market-affects-power-of-sale-rates-2025/ [7] lendworth.ca – https://www.lendworth.ca [9] Understanding The Mortgage Default Power Of Sale Process In Ontario – https://www.sukhlaw.ca/understanding-the-mortgage-default-power-of-sale-process-in-ontario/