March 17, 2026

Variable Private Mortgages at 8.99%: Toronto Borrowers’ Guide to Capitalizing on BoC 2.25% Stability in March 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s mortgage market is shifting fast. With the Bank of Canada holding its policy rate at 2.25% for the third straight time in March 2026, a growing number of borrowers are bypassing traditional banks entirely — and turning to variable private mortgages at 8.99% instead [2]. That might sound expensive at first glance. But for buyers who can’t pass a stress test, self-employed professionals, or homeowners facing urgent renewals, this guide to Variable Private Mortgages at 8.99%: Toronto Borrowers’ Guide to Capitalizing on BoC 2.25% Stability in March 2026 explains exactly why this option is surging — and how to use it strategically.

Key Takeaways 🔑

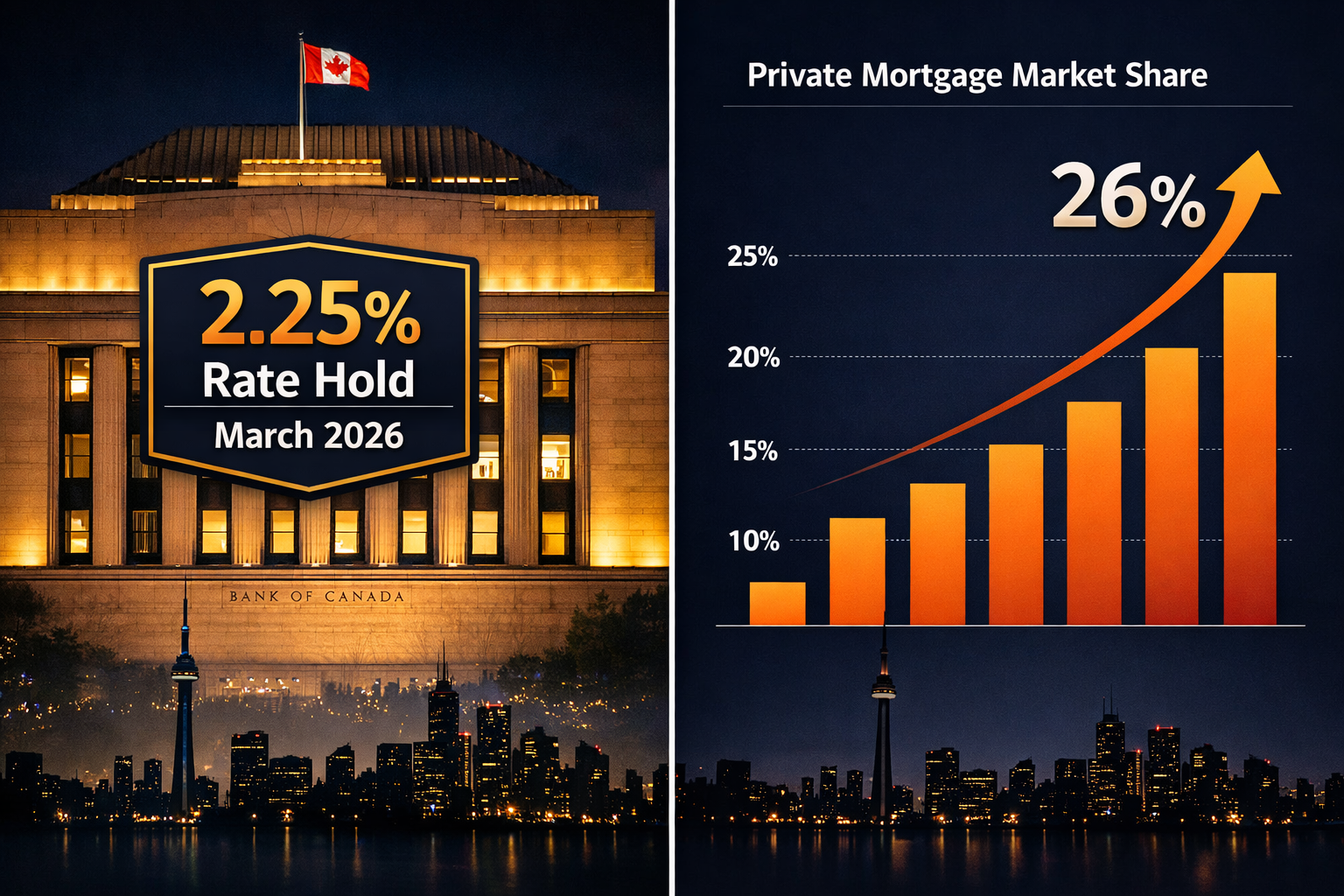

- The Bank of Canada held its overnight rate at 2.25% on March 8, 2026, keeping Canada’s prime rate stable at 4.45% [2][10]

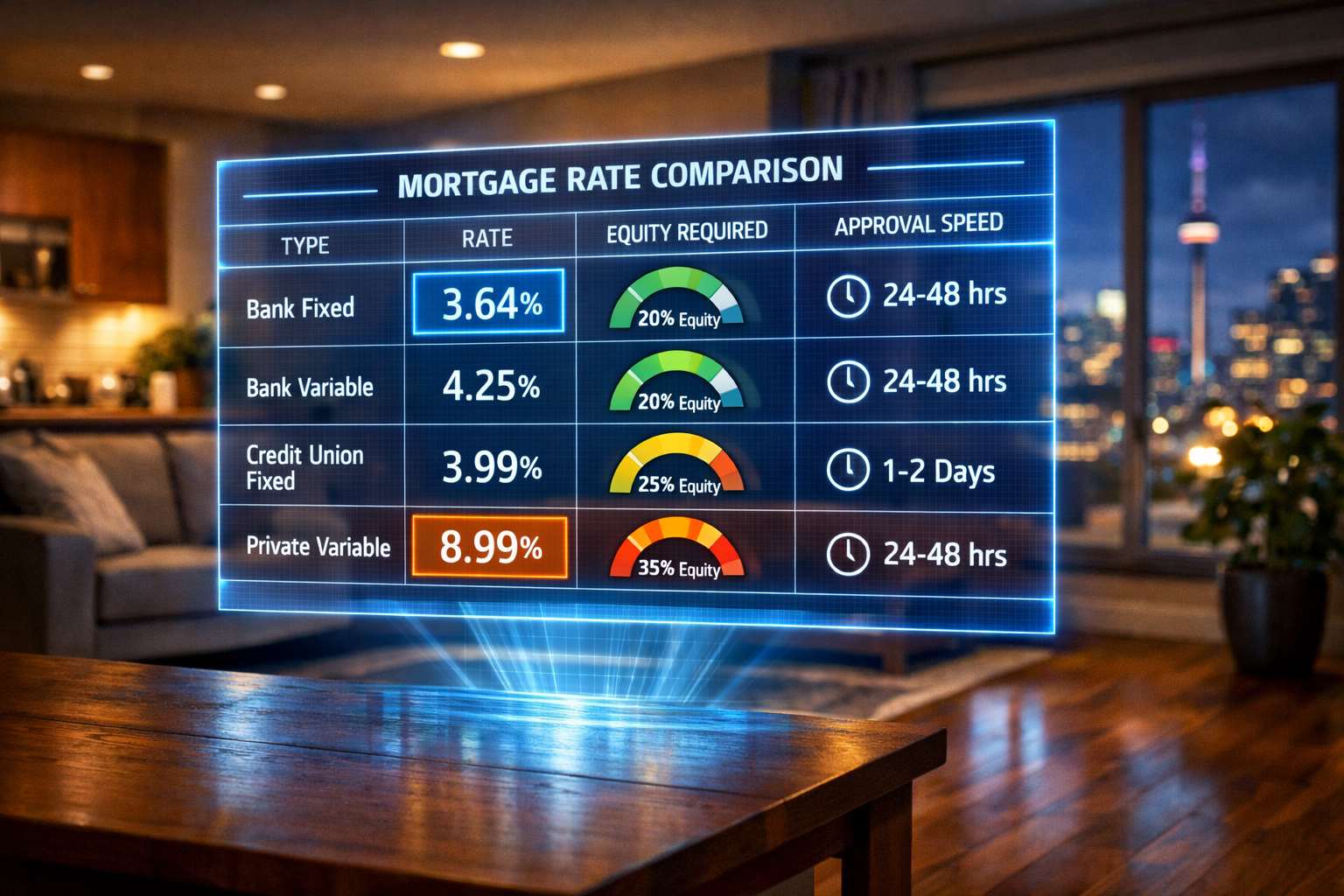

- Private variable mortgage rates of 8.99% are available from multiple Ontario lenders, sitting in the mid-range of private lending options [1]

- Private lenders approve based on property equity and exit strategy — not income verification or stress tests

- Variable private mortgages are a short-term bridge tool, not a long-term solution — a clear exit plan is essential

- Rate stability in 2026 makes this an ideal window to enter, stabilize finances, and refinance into a conventional product

Why Variable Private Mortgages Are Surging in Toronto’s 2026 Market

Variable private mortgages now represent approximately 26% of Toronto’s alternative lending market share — a figure that has climbed steadily since the BoC began cutting rates in 2025. The reason? Rate stability creates a predictable cost environment for short-term borrowers who need speed and flexibility over rock-bottom pricing.

The BoC Hold: What It Means for Private Borrowers

On March 8, 2026, the Bank of Canada confirmed its policy rate would remain at 2.25% — the third consecutive hold following seven consecutive cuts throughout 2025 [5]. Canada’s prime rate sits at 4.45%, with TD Bank’s prime slightly higher at 4.60% [10]. For variable private mortgage holders, this is welcome news: rate stability means monthly payment predictability, even at the higher 8.99% rate tier.

💬 “Variable mortgage rates remain the lowest-priced borrowing option [in conventional lending], but borrowers should have the risk tolerance and room in their budget to absorb future increases.” — Penelope Graham, Mortgage Expert [8]

RBC Economics forecasts the overnight rate will stay at 2.25% through all of 2026, with a gradual rise to 3.25% only by end of 2027 [5]. For private borrowers planning a 12–18 month bridge, this window is as stable as it gets.

Who Is Actually Using 8.99% Variable Private Mortgages?

Private lenders like Squire and Altawest are quoting 8.99% as of early March 2026, representing the mid-range of Ontario’s private lending spectrum [1]. Rates range from as low as 5.94% (Altrua Financial) to as high as 9.99% (Corwin Capital, Hosper Mortgage, CMI) [1]. The 8.99% tier typically serves:

| Borrower Type | Why They Choose Private |

|---|---|

| Self-employed professionals | Non-traditional income, no NOA verification required |

| Borrowers with bruised credit | Equity-based approval bypasses credit score thresholds |

| Homeowners facing urgent renewal | Banks too slow; private lenders approve in 24–48 hours |

| Recent immigrants or new-to-Canada | Limited Canadian credit history |

| Investors with multiple properties | Debt-service ratios too high for bank approval |

For self-employed Torontonians especially, securing a mortgage without traditional income documentation is a known challenge — and private lending fills that gap directly.

If credit challenges are the barrier, understanding how to get a mortgage with bad credit in Ontario is a critical first step before approaching any lender.

Understanding the 8.99% Rate: Costs, Comparisons, and Qualification Paths

How 8.99% Compares to Conventional Options

The gap between private and conventional rates is real — but context matters. In March 2026, the best fixed mortgage rates sit at 3.64%–3.69%, while five-year variable rates from banks are as low as 3.35% [8]. The spread between fixed and variable conventional options is only about 30 basis points, translating to roughly $90/month on a $700,000 mortgage.

The spread between a 3.35% conventional variable and an 8.99% private variable is significantly larger — approximately $2,100–$2,400/month more on a $700,000 mortgage. This premium reflects what borrowers are actually paying for:

- ✅ Speed: Approvals in 24–48 hours, even when banks say no

- ✅ Flexibility: No stress test, no income proof requirements

- ✅ Access: Equity-first underwriting opens doors for non-qualifying borrowers

- ✅ Bridge potential: A structured path back to conventional financing

For a deeper look at how fixed and variable options stack up in conventional lending, the comprehensive guide to fixed vs. variable rates provides useful context before making any decision.

How Private Lenders Qualify Toronto Borrowers

Unlike banks, private lenders focus on three core factors:

- The property — location, condition, and marketability in Toronto’s market

- The equity — typically requiring 20–35% equity or down payment

- The exit plan — a credible 12–24 month strategy to refinance or sell

CMHC’s Deputy Chief Economist Tania Bourassa-Ochoa has noted that “elevated financial stress for mortgage holders in Toronto and Vancouver” is real, but that “most Canadians have been resilient in facing significantly higher interest rates at renewal.” This resilience is partly driven by borrowers using private mortgages as a bridge to buy time.

For borrowers who’ve navigated financial difficulties, getting approved for a mortgage after bankruptcy is also possible through the private lending channel.

Variable vs. Fixed Within Private Lending

Even within the private lending space, the fixed vs. variable choice matters. A variable private mortgage at 8.99% offers:

- Potential rate decreases if the BoC cuts again (unlikely in 2026, but possible in 2027)

- Typically lower prepayment penalties, making early exit cheaper

- Greater flexibility to refinance into conventional products mid-term

However, borrowers should understand how trigger rates work in variable mortgages — the point at which rising rates could require a lump-sum payment or payment increase. In a stable rate environment like March 2026, this risk is low but not zero.

Toronto Borrowers’ Strategic Playbook: Capitalizing on BoC 2.25% Stability

Building Your Exit Strategy Before You Enter

The single most important rule of private mortgage borrowing: know your exit before you sign. A variable private mortgage at 8.99% is a tool, not a destination. The BoC’s current stability gives borrowers a predictable 12–18 month window to:

- Repair credit — Pay down debts, resolve collections, and build a stronger credit profile. See 5 tips to rapidly improve your credit score for a practical roadmap.

- Document income — Self-employed borrowers should use this period to file updated tax returns and build a two-year income history.

- Build equity — Rising Toronto property values can push loan-to-value ratios into conventional territory within 12–24 months.

- Refinance into conventional — Once qualifying criteria are met, transition to a bank or monoline lender at significantly lower rates. Explore how 2026 rate forecasts could make refinancing a smart move.

Practical Steps for Toronto Borrowers in March 2026

Step 1: Assess your equity position Most private lenders require a minimum of 20–25% equity. In Toronto, where average detached home prices remain elevated, many homeowners already meet this threshold.

Step 2: Work with a licensed mortgage broker Private lender networks are not easily navigated alone. A broker with access to multiple private lenders can compare the full spectrum — from 5.94% to 9.99% — and match borrowers to the right product. Understanding the difference between a mortgage broker and a bank is essential before starting this process.

Step 3: Understand all-in costs Private mortgages carry lender fees (typically 1–3% of the loan amount) and broker fees on top of the interest rate. Factor in closing costs and land transfer taxes when calculating total borrowing costs for a purchase.

Step 4: Set a hard refinance date Build a 12-month calendar with specific milestones: credit score targets, income documentation deadlines, and a target conventional rate to refinance into.

Is 8.99% Worth It? A Realistic Assessment

| Scenario | Private Mortgage Suitable? |

|---|---|

| Facing mortgage renewal with bruised credit | ✅ Yes — bridge to credit repair |

| Self-employed with 2+ years of filed returns | ⚠️ Maybe — explore bank alternatives first |

| Need approval in under 48 hours | ✅ Yes — speed is the primary value |

| Long-term homeowner with no exit plan | ❌ No — cost too high without clear strategy |

| First-time buyer with strong credit | ❌ No — qualify conventionally instead |

Conclusion: Make the BoC’s Stability Work for You

The Bank of Canada’s decision to hold at 2.25% in March 2026 has created a rare window of predictability in an otherwise uncertain economic landscape [2]. For Toronto borrowers who can’t access conventional financing today, variable private mortgages at 8.99% represent a legitimate — if expensive — bridge to homeownership or financial stability.

The key is treating this as a strategic short-term tool with a clear exit plan, not a permanent solution. The stable rate environment means costs are predictable. The 24–48 hour approval timelines mean opportunity isn’t missed. And the equity-first underwriting means more Torontonians qualify than they might expect.

Actionable Next Steps ✅

- Get a free broker consultation to compare private lenders across Ontario’s full rate spectrum

- Check your equity position — calculate your current loan-to-value ratio

- Start your credit repair plan today — even small improvements open better rate tiers

- Set a 12-month refinance goal — map the specific milestones needed to qualify conventionally

- Review all-in costs including lender fees, broker fees, and closing costs before committing

The window is open. The rate is stable. The strategy is clear. Toronto borrowers who move deliberately — with a plan — can use today’s private lending market as the bridge to tomorrow’s conventional mortgage.

References

[1] Private Mortgage Lenders Ontario – https://altrua.ca/private-mortgage-lenders-ontario/ [2] BoC Rate Decision March 2026 – https://dutec.net/boc-rate-decision-march-2026/ [3] Toronto Ontario – https://myperch.io/mortgage-rates-canada/toronto-ontario/ [4] 3 Year Variable Mortgage Rates – https://citadelmortgages.ca/3-year-variable-mortgage-rates/ [5] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast [6] Best Mortgage Rates Ontario – https://altrua.ca/best-mortgage-rates-ontario/ [7] 3 Year – https://www.nesto.ca/mortgage-rates/variable/3-year/ [8] Bank Of Canada Interest Rate March 2026 – https://dailyhive.com/vancouver/bank-of-canada-interest-rate-march-2026 [9] Mortgage Rates Toronto – https://citadelmortgages.ca/mortgage-rates-toronto/ [10] Prime Rates Canada – https://wowa.ca/banks/prime-rates-canada