March 18, 2026

Self-Employed Toronto Mortgage Affordability in 2026: Can You Qualify at $670K Average Home Prices?

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s housing market in 2026 presents both challenges and opportunities for self-employed professionals. With average home prices hovering around $670,000 and mortgage rates stabilizing near 4.2%, the question on every entrepreneur’s mind is: can you actually qualify for financing when your income doesn’t come from a traditional T4? Understanding Self-Employed Toronto Mortgage Affordability in 2026: Can You Qualify at $670K Average Home Prices? requires navigating complex income verification rules, debt service ratios, and lender requirements that differ significantly from traditional employment scenarios.

The good news? Self-employed borrowers have more options than ever before, from traditional A-lenders to alternative stated-income programs. The challenge lies in understanding which path suits your financial situation and how to position yourself for approval in Toronto’s competitive real estate market.

Key Takeaways

✅ Two-year minimum: Most traditional lenders require at least 2 years of self-employment history with consistent or growing income[1][3][4]

📊 Documentation is critical: Expect to provide 2-3 years of Notices of Assessment (NOAs), T1 General forms, business financial statements, and recent bank statements[3][4]

💰 Down payment flexibility: With proven income, qualify with as little as 5% down; stated-income programs require minimum 10% down[1][4]

🏦 Alternative pathways exist: If you can’t prove traditional income through tax documents, stated-income mortgages offer viable solutions with higher down payments[4]

🎯 Debt ratios matter most: Your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios determine borrowing power more than income alone

Understanding Self-Employed Mortgage Qualification Requirements in Toronto

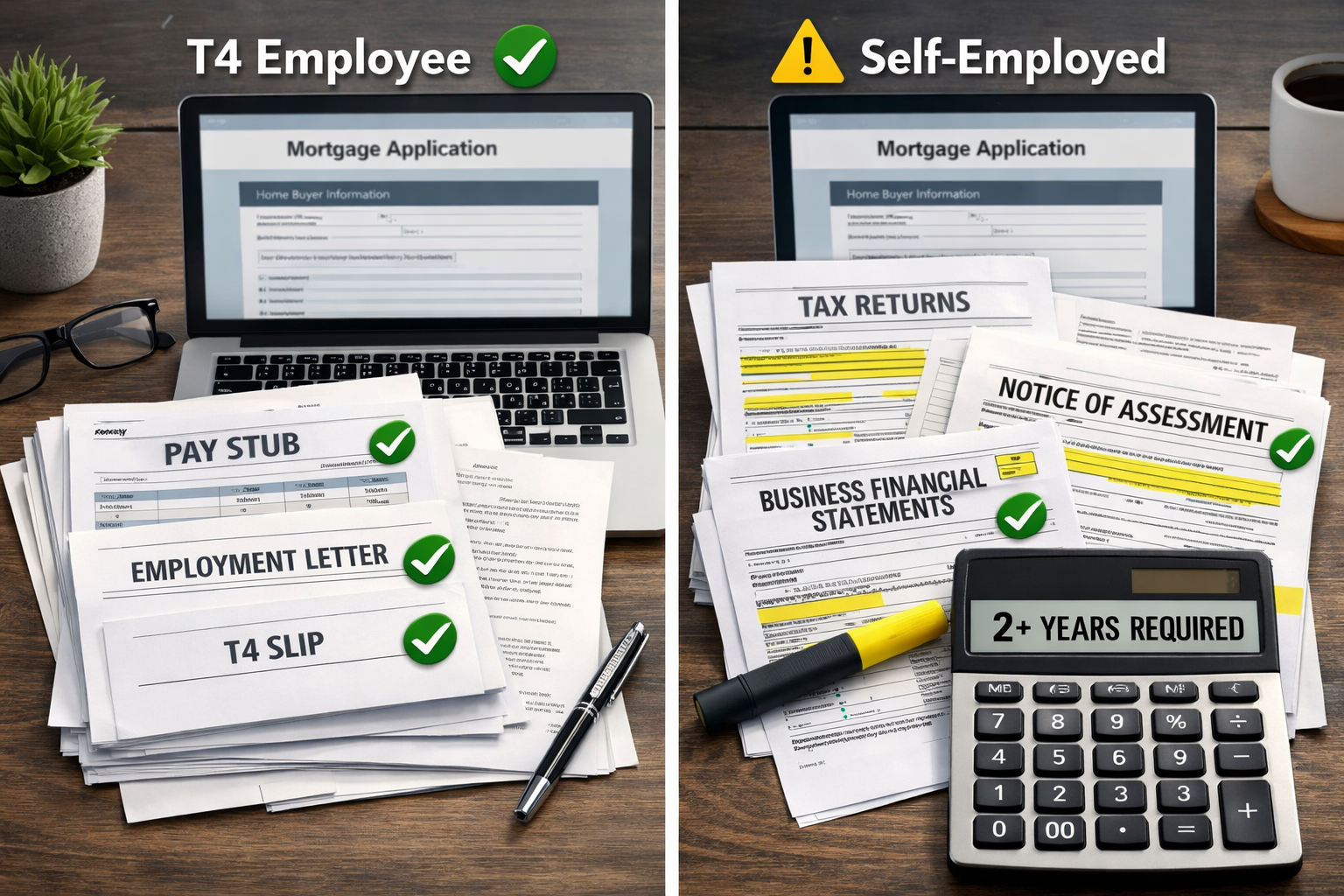

The path to homeownership for self-employed individuals in Toronto differs substantially from traditional employees. While salaried workers can simply provide recent pay stubs, self-employed borrowers face more rigorous scrutiny of their financial history.

The Two-Year Rule and Income Verification

Traditional lenders require a minimum of 2 years of self-employment history before considering your mortgage application[1][2][3]. This isn’t arbitrary—lenders want to see consistent income patterns and business stability. Some lenders may even request 3 years of documentation to establish a reliable income average[3].

The income verification process for obtaining a mortgage when you’re self-employed typically requires:

- Notices of Assessment (NOA) from the Canada Revenue Agency for the past 2-3 years[3][4]

- T1 General tax returns showing your personal income declarations[3][4]

- Business financial statements including profit and loss statements and balance sheets[3][4]

- 3 months of personal and business bank statements demonstrating cash flow[3][4]

- Articles of incorporation or business registration documents[3]

- Credit report with minimum score of 600 (though 680+ is preferred)[1]

How Lenders Calculate Your Income

Unlike traditional employees whose income calculation is straightforward, self-employed income requires careful analysis. Lenders typically use a two-year average of your net business income, which can work for or against you depending on your business trajectory[3][6].

Here’s the critical distinction: lenders look at your net income after business expenses and write-offs. While tax deductions benefit you at tax time, they reduce your qualifying income for mortgage purposes. This creates a common dilemma for self-employed borrowers—maximizing tax efficiency versus maximizing borrowing power.

For professionals like lawyers, accountants, or consultants, specialized programs exist. Self-employed lawyers, for instance, may have access to professional practice loans with more favorable terms.

Self-Employed Toronto Mortgage Affordability: Breaking Down the $670K Home Purchase

With Toronto’s average home price at $670,000 in 2026, understanding your borrowing capacity and down payment requirements becomes essential for planning your purchase.

Down Payment Options and Loan-to-Value Ratios

Your down payment significantly impacts both your mortgage approval odds and your monthly costs. Here’s how the numbers break down for a $670K Toronto home:

| Down Payment | Amount Required | Mortgage Amount | LTV Ratio | Insurance Required |

|---|---|---|---|---|

| 5% | $33,500 | $636,500 | 95% | Yes (CMHC/Sagen) |

| 10% | $67,000 | $603,000 | 90% | Yes (Sagen/Canada Guaranty) |

| 20% | $134,000 | $536,000 | 80% | No |

| 25% | $167,500 | $502,500 | 75% | No |

With proven income through traditional documentation, self-employed borrowers can access insured mortgages with as little as 5% down, borrowing up to 95% of the home’s value[1][5]. This requires mortgage default insurance from CMHC, Sagen, or Canada Guaranty, which protects the lender if you default.

Without traditional income proof, stated-income mortgage programs require a minimum 10% down payment and can provide up to 90% financing through certain insurers (Sagen and Canada Guaranty, but not CMHC)[1][4]. These programs verify income through alternative methods like bank statements showing consistent deposits.

For conventional mortgages without insurance, you’ll need 20% down and can borrow up to 80% of the property value[1][5].

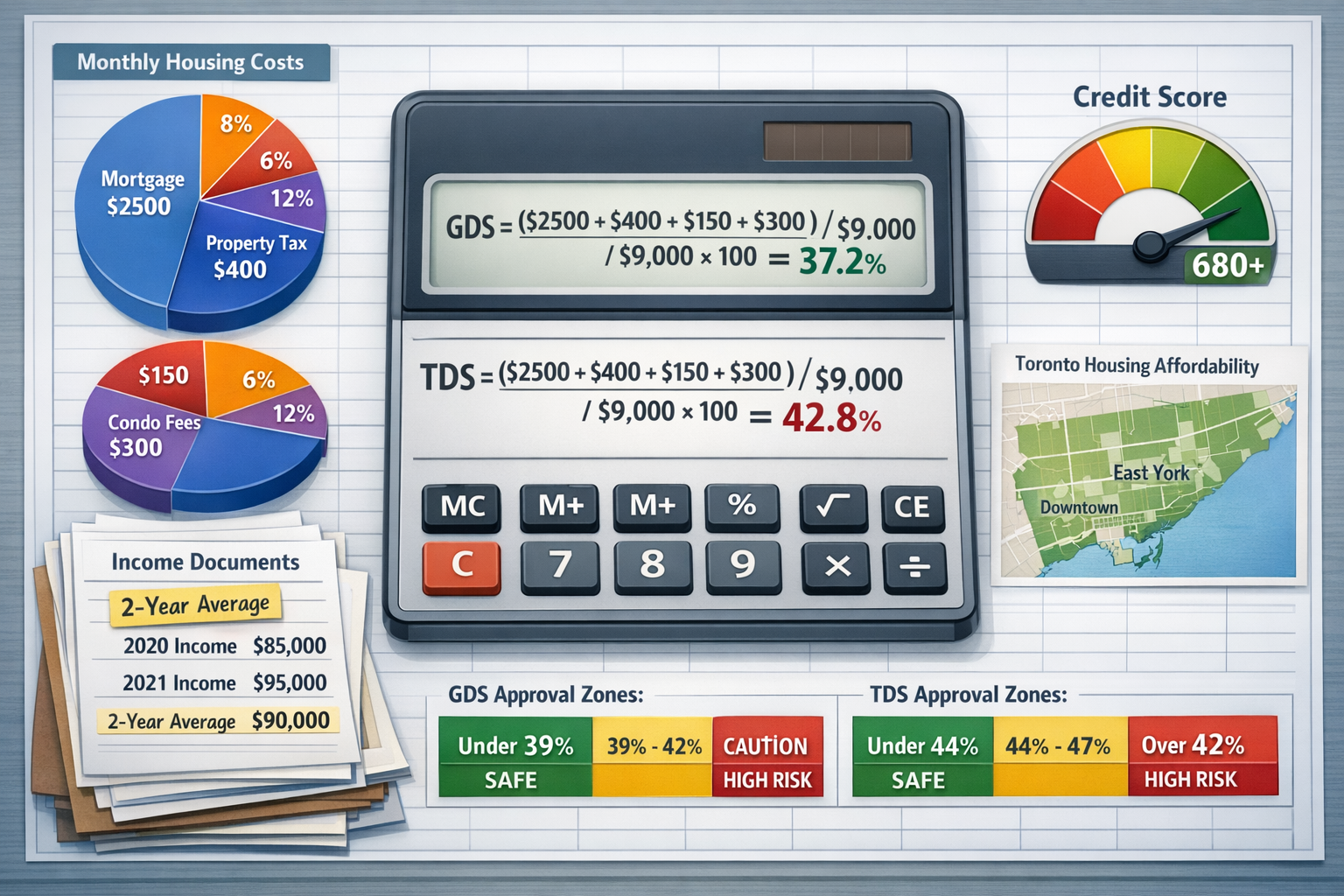

Calculating Your Debt Service Ratios

The most critical factor in determining Self-Employed Toronto Mortgage Affordability in 2026: Can You Qualify at $670K Average Home Prices? is your debt service ratios. These percentages tell lenders whether you can comfortably afford the mortgage payments alongside your other obligations.

Gross Debt Service (GDS) Ratio measures housing costs as a percentage of your gross monthly income:

GDS = (Mortgage Payment + Property Taxes + Heating + 50% of Condo Fees) ÷ Gross Monthly Income

Most lenders require GDS below 39%[6].

Total Debt Service (TDS) Ratio includes all debt obligations:

TDS = (Housing Costs + Credit Cards + Car Loans + Other Debts) ÷ Gross Monthly Income

Maximum TDS typically cannot exceed 44%[6].

Real-World Example: $670K Toronto Home

Let’s examine a practical scenario for a self-employed borrower purchasing a $670K home in Toronto:

Scenario Details:

- Home price: $670,000

- Down payment: $134,000 (20%)

- Mortgage amount: $536,000

- Interest rate: 4.2%

- Amortization: 25 years

- Monthly mortgage payment: ~$2,900

Additional monthly costs:

- Property taxes: $350

- Heating: $100

- Condo fees: $400

- Total housing costs: $3,750/month

To qualify with 39% GDS ratio: Required gross monthly income = $3,750 ÷ 0.39 = $9,615 Annual income required: $115,380

If you have additional debts (car loan $400/month, credit cards $200/month), your TDS calculation becomes: ($3,750 + $400 + $200) ÷ gross income ≤ 44% Required gross monthly income = $4,350 ÷ 0.44 = $9,886 Annual income required: $118,632

For self-employed borrowers in Toronto who can qualify without T4 slips, these calculations remain the same—only the income verification method differs.

Alternative Mortgage Solutions for Self-Employed Toronto Buyers

Not every self-employed professional fits the traditional lending mold. Whether you’ve been in business for less than two years, have significant tax write-offs that reduce your qualifying income, or have irregular income patterns, alternative solutions exist.

Stated-Income Mortgage Programs

Stated-income mortgages allow you to declare your income without providing traditional tax documentation[4]. Instead, lenders verify your income through:

- Bank statement analysis: Consistent deposits demonstrating regular business income

- Contracts or invoices: Showing ongoing client relationships and revenue

- Business bank accounts: Proving operational cash flow

- Credit history: Strong credit score (typically 680+) demonstrating financial responsibility

These programs typically require:

- Minimum 10% down payment (up to 90% LTV with mortgage insurance)[1][4]

- Minimum credit score of 600 (though 680+ improves approval odds)[1]

- Higher interest rates compared to traditional mortgages (typically 0.25-0.75% premium)

For entrepreneurs with less than 1 year’s accounts, stated-income programs may be the only viable option initially.

B-Lender and Private Mortgage Options

When traditional A-lenders decline your application, B-lenders and private lenders offer more flexible qualification criteria:

B-Lenders:

- Accept credit scores as low as 600[1]

- More flexible income verification

- Interest rates typically 1-2% higher than A-lenders

- Maximum 80% LTV for conventional mortgages

- Ideal for self-employed with good credit but complex income

Private Lenders:

- Focus primarily on property equity rather than income

- Accept lower credit scores and unusual income situations

- Interest rates typically 6-12%

- Shorter terms (6-24 months)

- Best used as bridge financing while you improve qualifications

Checking current self-employed mortgage rates in Toronto helps you understand the rate differential between lending tiers.

Lender-Specific Programs and Limits

Different lenders have varying appetite for self-employed mortgages. National Bank, for instance, caps self-employed mortgages at $1,500,000 overall, with lower limits in certain Toronto metropolitan areas (as low as $750,000 in some regions)[2].

Major banks like RBC offer dedicated self-employed mortgage programs with competitive rates for qualified borrowers who meet their documentation requirements[5]. Understanding these lender-specific nuances is where working with a knowledgeable mortgage broker in Toronto provides significant value—they know which lenders are most favorable for your specific situation.

The Importance of Pre-Qualification

Before house hunting in Toronto’s competitive market, qualifying for a mortgage before buying property gives you critical advantages:

✅ Know your exact budget based on actual lender approval, not estimates ✅ Strengthen your offer with pre-approval in hand ✅ Identify documentation gaps early and address them ✅ Compare multiple lenders to find the best rates and terms ✅ Avoid disappointment of falling in love with homes you can’t finance

Strategies to Maximize Your Self-Employed Mortgage Approval Odds

Successfully navigating Self-Employed Toronto Mortgage Affordability in 2026: Can You Qualify at $670K Average Home Prices? requires strategic planning beyond simply meeting minimum requirements.

Optimize Your Tax Strategy

The tension between tax efficiency and mortgage qualification requires careful balance:

12-18 months before applying:

- Reduce aggressive write-offs to show higher net income

- Document all income sources clearly on tax returns

- Maintain clean separation between personal and business expenses

- Consider incorporating if operating as sole proprietor (may provide advantages)

Consult both your accountant and mortgage professional to develop a coordinated strategy that optimizes both tax position and borrowing capacity.

Build Strong Credit and Reduce Debt

Your credit score significantly impacts both approval odds and interest rates:

- Maintain credit score above 680 for best rates and terms[1]

- Pay down credit cards to below 30% utilization

- Avoid new credit applications in the 6 months before mortgage application

- Correct any credit report errors well in advance

- Establish credit history if you’re new to Canada or have thin credit files

Reducing existing debts improves your TDS ratio, increasing your borrowing capacity for the $670K home purchase.

Increase Your Down Payment

While 5% down is technically possible with proven income, larger down payments provide multiple advantages:

💪 Lower monthly payments and total interest costs 💪 Avoid mortgage insurance premiums with 20%+ down 💪 Stronger approval odds with more equity at stake 💪 Better interest rates from lenders 💪 Greater flexibility in lender selection

For first-time buyers entering Toronto’s market, maximizing down payment through savings, gifts from family, or programs like the First Home Savings Account can make the difference between approval and denial.

Maintain Impeccable Financial Records

Organization is critical for self-employed mortgage applicants:

📁 Keep digital and physical copies of all financial documents 📁 Maintain separate business and personal bank accounts 📁 Track income and expenses meticulously throughout the year 📁 Prepare financial statements quarterly, not just at tax time 📁 Document major deposits or unusual transactions with explanations

When lenders request documentation, being able to provide it immediately demonstrates professionalism and financial competence.

Consider Co-Borrowers or Guarantors

If your income alone doesn’t qualify for the $670K purchase, adding a co-borrower or guarantor can strengthen your application:

- Spouse or partner: Combines both incomes and credit profiles

- Family member: Can co-sign to add their income to qualification

- Business partner: If purchasing investment property together

Understand that co-borrowers share full responsibility for the mortgage, while guarantors are liable only if you default.

Work With Specialized Mortgage Professionals

The complexity of self-employed mortgages makes professional guidance invaluable. Mortgage brokers who specialize in self-employed financing:

🎯 Know which lenders are most favorable for your situation 🎯 Understand documentation requirements and how to present your application 🎯 Can access multiple lenders simultaneously, including B-lenders 🎯 Save you time by pre-screening your application before submission 🎯 Negotiate rates and terms on your behalf

Freelancers and independent professionals particularly benefit from specialized mortgage guidance given their unique income structures.

Conclusion

Self-Employed Toronto Mortgage Affordability in 2026: Can You Qualify at $670K Average Home Prices? The answer is a resounding yes—with proper preparation, documentation, and strategy. While self-employed borrowers face additional scrutiny compared to traditional employees, multiple pathways exist to homeownership at Toronto’s current price points.

The key factors determining your success include:

✅ Minimum 2 years of self-employment history with consistent or growing income ✅ Comprehensive documentation including NOAs, tax returns, and financial statements ✅ Debt service ratios within acceptable limits (39% GDS, 44% TDS) ✅ Adequate down payment ranging from 5-20% depending on your documentation ✅ Strong credit profile with scores above 680 for optimal terms ✅ Strategic tax planning that balances write-offs with qualifying income

For those who don’t fit traditional lending criteria, stated-income programs, B-lenders, and private financing options provide viable alternatives, albeit at higher costs.

Next Steps for Self-Employed Toronto Home Buyers

Ready to pursue homeownership in Toronto’s $670K market? Take these actionable steps:

- Review your financial documentation and identify any gaps

- Calculate your debt service ratios to understand your borrowing capacity

- Check your credit score and address any issues

- Consult with a mortgage professional who specializes in self-employed financing

- Get pre-qualified before beginning your home search

- Consider your down payment options and savings strategies

- Explore different neighborhoods within your budget range

The Toronto housing market in 2026 presents opportunities for prepared self-employed buyers. With mortgage rates stabilizing and lenders offering more flexible programs than ever before, now may be an excellent time to transition from renting to ownership—provided you approach the process with clear understanding of requirements and realistic expectations about your qualifications.

Don’t let self-employment status discourage you from pursuing homeownership. With the right preparation and professional guidance, that $670K Toronto home is within reach.

References

[1] Self Employed Mortgage Options Qualifications In Canada – https://www.nesto.ca/mortgage-basics/self-employed-mortgage-options-qualifications-in-canada/

[2] Self Employed – https://www.nbc.ca/personal/mortgages/self-employed.html

[3] Self Employed Mortgage – https://www.ratehub.ca/self-employed-mortgage

[4] Self Employed Mortgage Requirements – https://www.frankmortgage.com/blog/self-employed-mortgage-requirements

[5] Self Employed Mortgage – https://www.rbcroyalbank.com/mortgages/self-employed-mortgage.html

[6] Self Employed Heres How Qualifying For A Mortgage Works – https://www.mortgagenb.ca/first-time-home-buyers/self-employed-heres-how-qualifying-for-a-mortgage-works/