March 21, 2026

Self-Employed Toronto Buyers: Qualifying for Sub-3.9% Insured Rates on $1M Homes Under New CMHC Thresholds

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Owning a home in Toronto has long seemed out of reach for many self-employed professionals, but 2026 brings a game-changing opportunity. With CMHC’s increased insured mortgage cap now set at $1.5 million, Self-Employed Toronto buyers can access premium insured rates as low as 3.89-3.91% on properties that were previously excluded from this advantageous financing option. This shift represents the most significant expansion of insured mortgage eligibility in over a decade, opening doors for entrepreneurs, contractors, and independent professionals across the Greater Toronto Area.

For self-employed individuals who have traditionally faced higher scrutiny and steeper rates, understanding how to leverage these new CMHC thresholds is essential. The path to qualifying for sub-3.9% insured rates requires strategic financial planning, proper documentation, and meeting specific credit and down payment requirements. This comprehensive guide reveals exactly how self-employed Toronto buyers can position themselves to secure these competitive rates on homes valued up to $1.5 million.

Key Takeaways

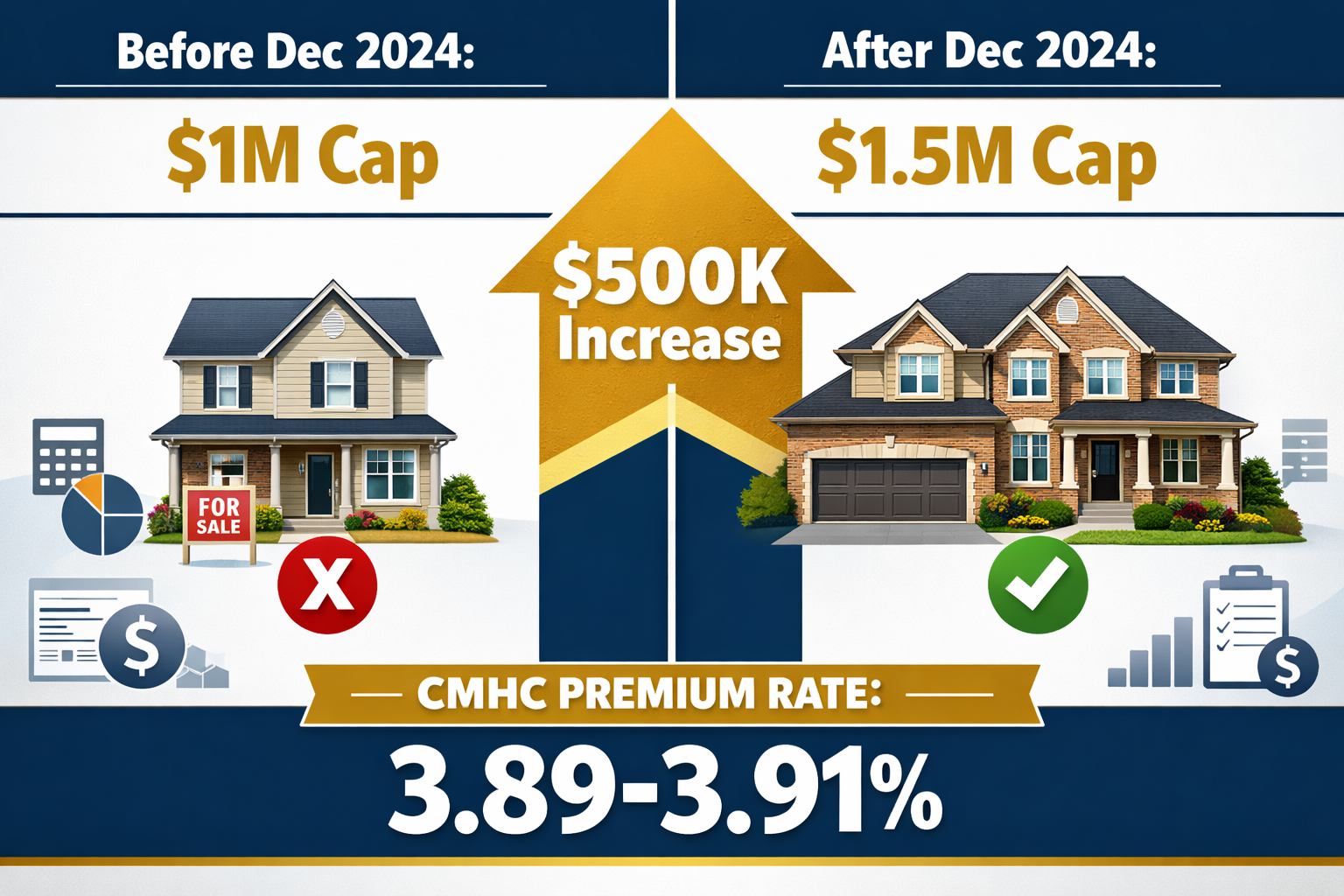

- 🏠 CMHC’s insured mortgage cap increased to $1.5 million as of December 15, 2024, allowing Toronto buyers to access insured rates on higher-value properties[5]

- 💰 Self-employed buyers can secure rates between 3.89-3.91% by qualifying for CMHC insurance with proper documentation including T1 General tax returns and Notices of Assessment

- 📊 Minimum credit score of 620+ is required for CMHC-insured mortgages, with stronger scores (680+) providing better approval odds[4]

- 💵 Down payments of 10-20% offer the best value, with insurance premiums ranging from 2.80% to 3.10% of the mortgage amount[1]

- 📝 Two years of consistent income documentation through T1 returns and NOAs is typically required for self-employed applicants

Understanding the New CMHC Insured Mortgage Thresholds for Toronto Properties

The landscape for self-employed Toronto buyers qualifying for sub-3.9% insured rates transformed dramatically when CMHC raised the maximum property price eligible for insured mortgages from $1 million to $1.5 million. This change, implemented on December 15, 2024, directly addresses the reality of Toronto’s housing market, where the average detached home price regularly exceeds the previous $1 million threshold[5].

What CMHC Insurance Means for Self-Employed Buyers

CMHC mortgage insurance protects lenders when buyers make down payments of less than 20%. This insurance allows lenders to offer significantly lower interest rates—often 0.50% to 1.00% below conventional mortgage rates—because the risk is transferred to the insurer. For self-employed professionals who often face higher rates due to perceived income variability, accessing these insured rates can mean thousands of dollars in annual savings.

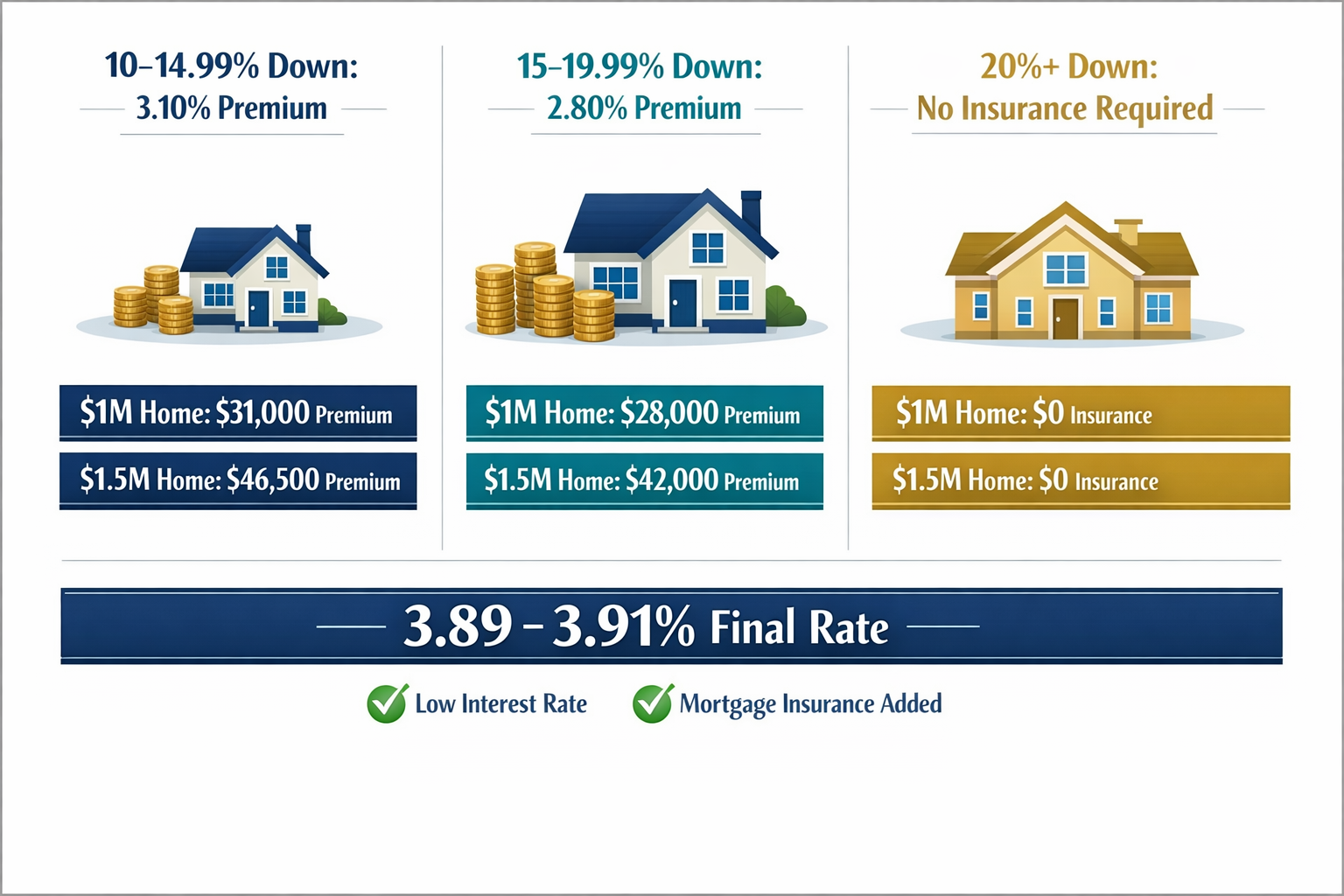

The insurance premium itself is calculated as a percentage of the mortgage amount and varies based on your down payment size:

| Down Payment | Insurance Premium | Example on $1M Mortgage |

|---|---|---|

| 5-9.99% | 4.00% | $40,000 |

| 10-14.99% | 3.10% | $31,000 |

| 15-19.99% | 2.80% | $28,000 |

| 20%+ | 0% (No insurance required) | $0 |

For Mortgages for Self-Employed borrowers, the premium is typically added to the mortgage principal and amortized over the life of the loan, meaning you don’t need to pay it upfront[1].

Toronto Market Context: Why $1.5M Matters

In Toronto’s competitive real estate market, the $1.5 million threshold opens up substantial inventory. Neighborhoods like Riverdale, Roncesvalles, East York, and North York now feature numerous properties that qualify for insured financing. Even some downtown condos and townhouses that previously exceeded the $1 million cap now fall within the insured range.

This expansion is particularly significant for self-employed professionals who have built successful businesses but lack the traditional T4 employment income that lenders prefer. The ability to access insured rates between 3.89% and 3.91% rather than conventional rates of 4.50% or higher can make the difference between qualifying for a home and being priced out of the market entirely.

How Self-Employed Toronto Buyers Can Qualify for Sub-3.9% Insured Rates

Qualifying for CMHC-insured mortgages as a self-employed borrower requires meeting specific criteria that differ from traditional employment verification. The key to accessing sub-3.9% insured rates on $1M homes under new CMHC thresholds lies in understanding and preparing for these requirements well in advance.

Credit Score Requirements: The 620+ Threshold

CMHC requires a minimum credit score of 620 to qualify for insured mortgages[4]. However, self-employed applicants should aim higher for optimal approval chances:

- 620-679: Minimum threshold; may face additional scrutiny

- 680-719: Good range; standard approval process

- 720+: Excellent; strongest approval odds and potential for best rates

For self-employed individuals with credit challenges, focusing on credit improvement strategies is essential. This includes paying all bills on time, reducing credit utilization below 30%, and avoiding new credit applications in the months leading up to your mortgage application.

Income Documentation: T1 General and Notice of Assessment

Unlike salaried employees who can provide recent pay stubs, self-employed Toronto buyers must demonstrate income through tax documentation. Lenders typically require:

Two Years of T1 General Tax Returns: These comprehensive forms show your total income, deductions, and net income. Lenders will average your net income over the two most recent years to determine your qualifying income.

Notices of Assessment (NOA): Issued by the Canada Revenue Agency, NOAs confirm that your tax returns have been filed and assessed. These documents provide third-party verification of your reported income[5].

Business Financial Statements: Some lenders may request additional documentation such as profit and loss statements, especially if you’re incorporated.

The challenge for many self-employed professionals is that they legitimately write off business expenses to minimize tax liability, which also reduces their reported net income. This creates a delicate balance: you need sufficient reported income to qualify for the mortgage amount you need, while also managing your tax obligations strategically.

For those exploring alternative documentation methods, bank statement mortgages for self-employed borrowers may offer additional pathways to qualification.

Down Payment Sweet Spots for Self-Employed Buyers

While CMHC insurance allows down payments as low as 5%, self-employed buyers benefit significantly from larger down payments:

10-15% Down Payment: This range offers a balance between accessibility and lower insurance premiums. At 10-14.99% down, your insurance premium is 3.10% of the mortgage amount[1]. On a $1 million home with 12% down ($120,000), your mortgage would be $880,000 with an insurance premium of $27,280.

15-20% Down Payment: The premium drops to 2.80% in this range, providing meaningful savings. On the same $1 million home with 18% down ($180,000), your mortgage would be $820,000 with an insurance premium of $22,960—saving nearly $4,500 compared to the 10-15% tier[6].

Above 20% Down Payment: You avoid CMHC insurance entirely, but you also lose access to the preferential insured rates. For many self-employed buyers, staying in the 15-19.99% range provides the best overall value.

Debt Service Ratios: Meeting CMHC Standards

CMHC imposes strict debt service ratio requirements that self-employed buyers must meet:

Gross Debt Service (GDS) Ratio: Your housing costs (mortgage principal, interest, property taxes, heating, and 50% of condo fees if applicable) cannot exceed 39% of your gross monthly income[4].

Total Debt Service (TDS) Ratio: Your total debt obligations (housing costs plus all other debts like car loans, credit cards, and lines of credit) cannot exceed 44% of your gross monthly income[4].

For self-employed individuals, these ratios are calculated based on your averaged net income from tax returns, making it crucial to have sufficient reported income over the past two years.

Strategic Steps for Self-Employed Professionals to Secure Insured Financing

Successfully navigating the path to sub-3.9% insured rates on $1M homes requires strategic planning and timing. Self-employed Toronto buyers should follow this comprehensive roadmap to maximize their approval chances.

Step 1: Financial Planning 12-24 Months in Advance

The most successful self-employed mortgage applications begin long before the actual application. Consider these advance strategies:

Balance Tax Write-offs with Income Reporting: Work with your accountant to find the optimal balance between minimizing taxes and maximizing reported income. If you’re planning to purchase within two years, you may want to reduce aggressive expense deductions to show higher net income.

Build Your Down Payment: Aim for 15-20% down to access the best insurance premium rates while still qualifying for insured financing. On a $1 million property, this means saving $150,000-$200,000.

Strengthen Your Credit Profile: Focus on building your credit score above 680. Pay all obligations on time, keep credit utilization low, and avoid opening new credit accounts.

For self-employed professionals just starting out, mortgages for self-employed with less than 1 year’s accounts provides specialized guidance for newer businesses.

Step 2: Gather Comprehensive Documentation

Before approaching lenders, compile a complete documentation package:

✅ Two years of T1 General tax returns (personal)

✅ Two years of Notices of Assessment from CRA

✅ Business financial statements (if incorporated)

✅ Articles of incorporation or business registration

✅ Bank statements showing down payment funds (90 days)

✅ Credit report (obtain your own copy first)

✅ Letter from your accountant confirming business continuity

Having this documentation ready demonstrates professionalism and can significantly speed up the approval process. For specialized professionals, getting a mortgage approved as a self-employed doctor in Ontario offers industry-specific insights.

Step 3: Work with Specialized Mortgage Professionals

Not all lenders have the same appetite for self-employed borrowers. Some major banks maintain rigid requirements, while alternative lenders and credit unions may offer more flexibility. Working with a mortgage broker who specializes in self-employed financing provides several advantages:

- Access to multiple lenders with varying criteria

- Expertise in presenting self-employed income optimally

- Knowledge of which lenders offer the best insured rates

- Ability to navigate complex income situations

Self-employed mortgages for contractors demonstrates how specialized guidance can make the difference between approval and rejection.

Step 4: Consider Timing and Market Conditions

Interest rates fluctuate based on economic conditions and Bank of Canada policy decisions. In 2026, insured mortgage rates have remained competitive, with many lenders offering rates between 3.89% and 3.91% for well-qualified self-employed borrowers[5].

Monitor rate trends and consider getting a rate hold (typically valid for 90-120 days) when rates are favorable. This protects you if rates rise while you’re searching for properties.

Step 5: Understand First-Time Buyer Benefits

If you’re a first-time homebuyer, additional programs can reduce your overall costs:

Home Buyers’ Plan (HBP): Withdraw up to $35,000 from your RRSP tax-free for your down payment. This can be particularly valuable for self-employed individuals who have been contributing to RRSPs for tax planning purposes.

First-Time Home Buyer Incentive: While this program has specific income limits, eligible buyers can access shared-equity mortgages that reduce monthly payments.

Land Transfer Tax Rebates: First-time buyers in Ontario can receive rebates up to $4,000 on provincial land transfer tax, with additional rebates available for Toronto purchases.

For comprehensive guidance on these programs, review the first-time home buyer tax credit in Canada and avoid common first-time home-buyer mistakes.

Maximizing Your Qualification Potential: Advanced Strategies

For self-employed Toronto buyers seeking sub-3.9% insured rates, several advanced strategies can strengthen your application and potentially increase your purchasing power.

Income Averaging and Trending

Lenders typically average your net income over two years, but some will consider income trending if your business shows consistent growth. If your most recent year’s income is significantly higher than the previous year, provide evidence of:

- Growing client contracts or retainer agreements

- Expansion of business operations

- Industry growth trends supporting continued income increases

- Additional revenue streams coming online

A letter from your accountant explaining the growth trajectory can help lenders feel more confident using higher income figures for qualification purposes.

Co-Applicants and Co-Signers

Adding a co-applicant (typically a spouse or partner) with their own income can significantly boost your qualifying power. If your partner has traditional T4 employment, this can offset lender concerns about self-employed income variability.

Alternatively, a co-signer (often a parent) who doesn’t need to be on title can provide additional income support for qualification purposes, though this comes with obligations for the co-signer.

Property Selection Strategy

Not all properties are treated equally by CMHC. To maximize approval odds:

Choose Properties in Strong Markets: Homes in established Toronto neighborhoods with stable property values are viewed more favorably than properties in emerging or volatile areas.

Avoid Non-Standard Properties: Unique properties, homes requiring significant repairs, or properties with unusual features may face additional scrutiny or be declined for insured financing.

Consider Condos Carefully: While condos are eligible for CMHC insurance, ensure the building is CMHC-approved and has sufficient reserve funds. Some lenders have additional requirements for condo purchases.

Leveraging Tax Planning for Future Purchases

If you’re planning to purchase in the next 1-2 years, work closely with your accountant to optimize your tax strategy:

Report Sufficient Income: While minimizing taxes is important, ensure you’re reporting enough net income to qualify for your target mortgage amount. A rough rule of thumb: you’ll need reported annual income of approximately 35-40% of your desired mortgage amount to meet debt service ratios.

Document Business Stability: Maintain consistent business registration, licensing, and professional credentials. Lenders want to see that your self-employment is stable and likely to continue.

Separate Business and Personal Expenses: Clear financial separation demonstrates professional business management and makes income verification easier.

For comprehensive tax strategies, explore tax smarts and maximizing benefits for the self-employed in Canada.

Alternative Documentation Methods

If traditional T1/NOA documentation presents challenges, some lenders offer alternative verification methods:

Bank Statement Programs: Some lenders will qualify you based on 12-24 months of business bank statements rather than tax returns. This can work well if you have strong cash flow but lower reported net income due to legitimate business deductions.

Stated Income Programs: While less common for insured mortgages, some portfolio lenders offer stated income programs for self-employed borrowers with strong credit and larger down payments.

Asset-Based Lending: If you have substantial assets but lower reported income, some lenders will consider your overall financial position rather than focusing solely on income.

For those exploring non-traditional documentation, how self-employed borrowers in Toronto can qualify for mortgages without T4 slips provides detailed alternatives.

Common Pitfalls and How to Avoid Them

Even well-prepared self-employed buyers can encounter obstacles. Avoid these common mistakes:

❌ Insufficient Income Documentation: Failing to report adequate income over two years is the most common reason for self-employed mortgage declines. Plan ahead with your accountant.

❌ Mixing Business and Personal Finances: Commingled accounts make income verification difficult and raise red flags for lenders. Maintain clear separation.

❌ Last-Minute Credit Issues: Applying for new credit, missing payments, or carrying high credit card balances in the months before your mortgage application can derail approval.

❌ Overestimating Qualification Amount: Many self-employed buyers are surprised by how conservatively lenders calculate their qualifying income. Get pre-approved before house hunting to understand your realistic budget.

❌ Ignoring Debt Service Ratios: Even with sufficient income, high existing debts can prevent qualification. Pay down credit cards, lines of credit, and other obligations before applying.

❌ Choosing the Wrong Lender: Not all lenders have the same appetite for self-employed borrowers. Working with specialists who understand self-employed income is crucial.

Conclusion

The expansion of CMHC’s insured mortgage threshold to $1.5 million represents a transformative opportunity for self-employed Toronto buyers seeking sub-3.9% insured rates on $1M homes. By understanding the qualification requirements—including the 620+ credit score threshold, proper T1 General and NOA documentation, and strategic down payment planning—self-employed professionals can access the same advantageous financing that has traditionally been reserved for salaried employees.

Success requires strategic planning 12-24 months in advance, working with specialized mortgage professionals who understand self-employed income verification, and maintaining the delicate balance between tax optimization and demonstrating sufficient income for qualification purposes. With insurance premiums ranging from 2.80% to 3.10% for down payments between 10-20%, the overall cost of accessing these premium rates remains highly competitive[1][6].

Your Next Steps

Ready to pursue sub-3.9% insured rates on your Toronto home purchase? Take these immediate actions:

- Review your last two years of tax returns with your accountant to determine your qualifying income

- Check your credit score and address any issues that could impact approval

- Calculate your target down payment (aim for 15-20% for optimal insurance premiums)

- Connect with a mortgage broker who specializes in self-employed financing

- Get pre-approved before beginning your property search to understand your realistic budget

The Toronto real estate market continues to evolve, and the new CMHC thresholds have leveled the playing field for self-employed professionals. With proper preparation and expert guidance, securing competitive insured financing on properties up to $1.5 million is now within reach for entrepreneurs, contractors, and independent professionals across the Greater Toronto Area.

Don’t let self-employment status stand between you and homeownership. The tools, programs, and competitive rates are available—you just need to know how to access them. Start your planning today to position yourself for success in Toronto’s dynamic housing market.

References

[1] Cmhc Insurance – https://wowa.ca/calculators/cmhc-insurance

[2] Cmhc Mortgage Loan Insurance Cost – https://www.cmhc-schl.gc.ca/consumers/home-buying/mortgage-loan-insurance-for-consumers/cmhc-mortgage-loan-insurance-cost

[3] Cmhc Mortgage Insurance – https://www.ratehub.ca/cmhc-mortgage-insurance

[4] Cmhc Mortgage Rules – https://wowa.ca/cmhc-mortgage-rules

[5] Cmhc Insured Mortgages Changes – https://www.elevatepartners.ca/resources/cmhc-insured-mortgages-changes/

[6] Premium Information For Homeowner And Small Rental Loans – https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/premium-information-for-homeowner-and-small-rental-loans

[7] Cmhc Insurance Ontario – https://www.ratehub.ca/cmhc-insurance-ontario

[8] Cmhc Insurance – https://www.nesto.ca/calculators/cmhc-insurance/