March 21, 2026

OSFI CAR 2026 Rules: How New Capital Requirements Are Driving Toronto Borrowers to Private Mortgages

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

A quiet regulatory shift took effect on January 1, 2026 — and it is already reshaping who gets a mortgage in Toronto. The OSFI CAR 2026 Rules: How New Capital Requirements Are Driving Toronto Borrowers to Private Mortgages story is not just about red tape. It is about real landlords, real investors, and real families who suddenly find themselves locked out of bank financing — and turning to private lenders to fill the gap.

Key Takeaways 📌

- OSFI’s CAR 2026 Guideline, effective January 1, 2026, bans banks from counting the same rental income twice when qualifying borrowers for multiple investment properties [1].

- This “double-counting prohibition” reduces investor borrowing power by an estimated 23% for multi-property portfolios.

- Private and alternative lenders now hold an estimated 8–12% of Canada’s mortgage market — roughly double their share from five years ago [2].

- In Ontario, private mortgages represent 15.8% of all mortgages by count, driven by tightened bank rules and renewal stress [6].

- Toronto borrowers facing bank rejections have a growing range of private mortgage options — but they come with higher rates and fees that require careful planning.

What Are the OSFI CAR 2026 Rules? A Plain-Language Breakdown

The Office of the Superintendent of Financial Institutions (OSFI) published the final Capital Adequacy Requirements (CAR) Guideline on August 14, 2025, with full implementation beginning January 1, 2026 [1]. The guideline followed a 60-day public consultation held between February 20 and April 22, 2025 [1].

At its core, the CAR 2026 framework forces federally regulated banks and lenders to hold more capital against riskier loans. This makes lending more expensive for banks — and by extension, harder for certain borrowers to qualify.

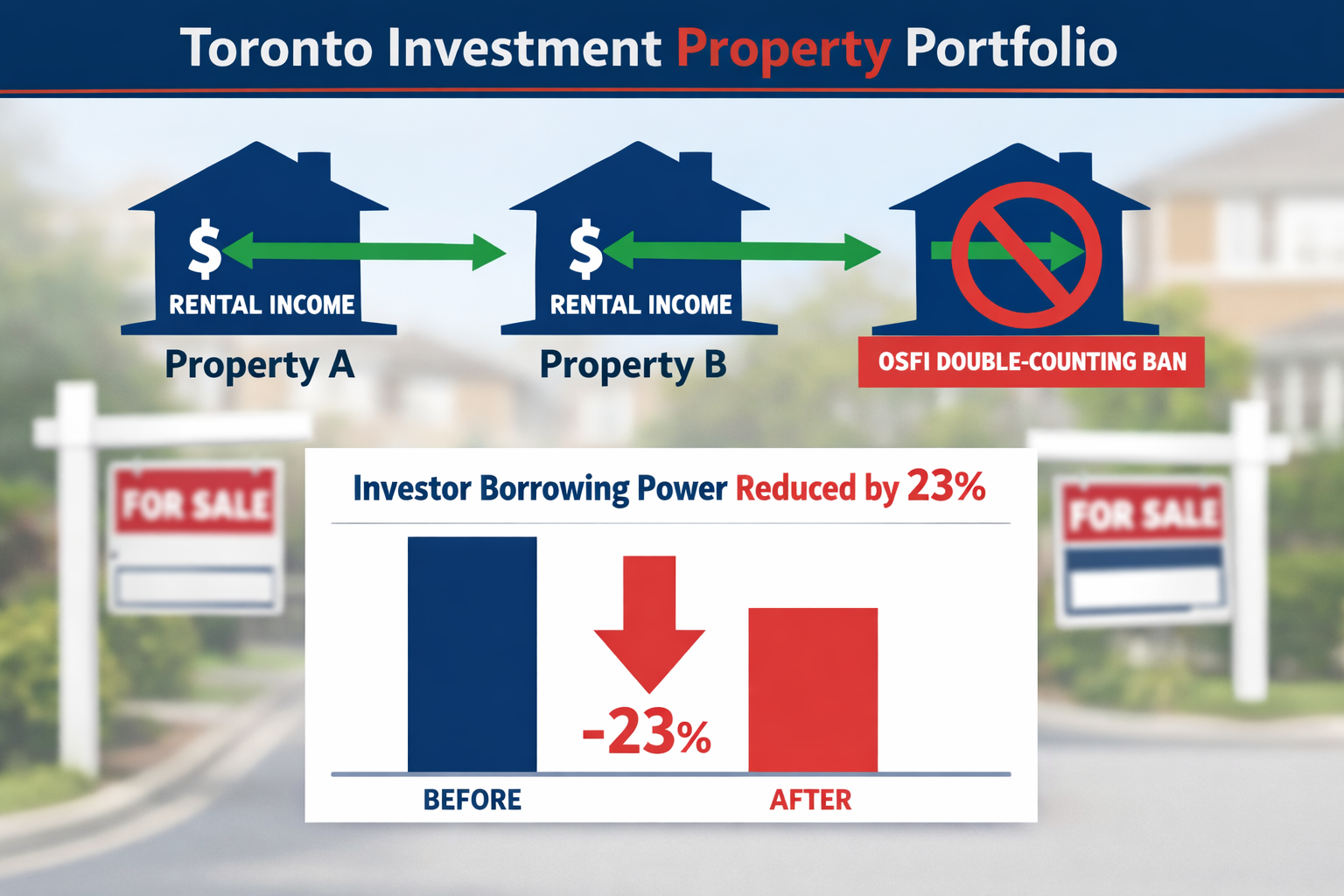

The Double-Counting Ban: The Rule That Changes Everything

The most impactful change for Toronto real estate investors is the prohibition on rental income double-counting.

OSFI’s Director of Capital and Liquidity Standards explained the logic clearly in September 2025:

“The goal is to ensure that income that’s used for one mortgage is not, then again, used a second time for another one.”

Here is how it works in practice:

| Scenario | Before CAR 2026 | After CAR 2026 |

|---|---|---|

| Property A rent ($2,000/mo) used for Property B mortgage | ✅ Allowed | ✅ Still allowed |

| Same $2,000 used again for Property C mortgage | ✅ Allowed | ❌ Prohibited |

| Portfolio of 3+ properties | Full rental income stacked | Income capped at first use |

This single rule effectively ends the classic strategy of gradually building a rental portfolio by recycling income from existing properties to qualify for the next one [6].

💡 Important nuance: OSFI has clarified that this change does not alter Guideline B-20 requirements. Banks can still use rental income for qualification — they simply cannot recycle the same income stream across multiple mortgage applications [1].

How the New Capital Requirements Are Shrinking Investor Borrowing Power in the GTA

The math is sobering for GTA landlords. Industry analysis confirms that the double-counting prohibition reduces effective borrowing power for multi-property investors by approximately 23% when building a portfolio beyond two properties [6].

Consider the Greater Toronto Area context:

- The benchmark home price in February 2026 was $938,800, down 7.9% year-over-year

- The average sold price sits at $1,008,968

- The market holds 5.0 months of supply — firmly in buyer’s territory

Lower prices might seem like good news for investors. But if bank qualification rules shrink buying power by nearly a quarter, the math still does not work for many would-be landlords.

The Renewal Wave Makes It Worse ⚠️

The CAR 2026 changes land at the worst possible moment. As of March 2026, Canada’s mortgage renewal wave has entered its peak cycle, with 1.15 million homeowners facing renewal decisions. Approximately one-third of all Canadian mortgage holders are expected to see payment increases by the end of 2026.

Borrowers who took out 5-year fixed mortgages are facing average payment increases of around 20% compared to late 2024 rates. Meanwhile, OSFI kept the Domestic Stability Buffer at a record 3.5% in December 2025 — freezing roughly $60 billion in bank capital just as $300 billion in mortgages prepare to reset at higher rates [2].

For context on how fixed and variable rates are playing out in this environment, see this breakdown of fixed vs. variable rates for Toronto first-time buyers and refinancers in 2026.

Rather than reject renewal applications outright, some major Canadian banks have quietly extended amortization periods to 35+ years to manage payment shock. This avoids default but significantly increases long-term interest costs. For a deeper look at how longer terms work, the guide to 30-year mortgages in Canada is worth reviewing.

Why Toronto Borrowers Are Turning to Private Mortgages

The combination of stricter capital rules, income qualification limits, and renewal payment shock is pushing a growing segment of Toronto borrowers toward private and alternative lenders — and the numbers prove it.

Private and alternative lenders now represent an estimated 8–12% of Canada’s mortgage market, roughly double their share from five years ago [2]. In Ontario specifically, private mortgages represent 15.8% of the mortgage market by count [6].

Real estate professionals are calling 2026 a “quiet shift that could redefine Canadian real estate financing” — a structural market change, not a temporary blip [6].

Who Is Turning to Private Mortgages? 🏠

The borrowers most affected by OSFI CAR 2026 rules include:

- Multi-property investors whose rental income is now capped under the double-counting ban

- Self-employed borrowers with strong assets but complex income documentation (see mortgages for self-employed borrowers)

- Renewal-stressed homeowners who no longer qualify at their bank under new stress test parameters

- Borrowers with recent credit events such as those getting a mortgage after bankruptcy

As Lendworth Capital summarizes the shift: “Private mortgages are not a last resort — they are a workable option for borrowers whose assets outpace what banks are willing to acknowledge.” [6]

What to Expect From a Private Mortgage in 2026

Private mortgages offer speed and flexibility — but they come at a cost. Here is a realistic comparison:

| Feature | Bank Mortgage | Private Mortgage |

|---|---|---|

| Interest Rate | 5.5–6.5% | 8–14% |

| Approval Speed | 2–4 weeks | 3–7 business days |

| Income Verification | Strict (T4, NOA) | Flexible (asset-based) |

| Rental Income Rules | OSFI CAR 2026 limits apply | Lender-specific |

| Typical Term | 1–5 years | 6–24 months |

| Ideal Use | Long-term financing | Bridge, transition, portfolio building |

For a full overview of the options available in Ontario, the guide to private mortgage options in Ontario covers the landscape in detail.

Navigating the OSFI CAR 2026 Rules: Practical Steps for Toronto Borrowers

Understanding the rules is the first step. Acting on them strategically is what separates borrowers who adapt from those who stall.

Step 1: Know Your Qualification Ceiling

Map out exactly how many properties you own and which rental income streams have already been used in prior mortgage qualifications. Under CAR 2026, each dollar of rental income can only be counted once across your portfolio applications [1][2].

Step 2: Work With a Mortgage Broker — Not Just Your Bank

Banks are bound by OSFI’s capital rules. Mortgage brokers have access to private lenders, credit unions, and MICs (Mortgage Investment Corporations) that operate under different regulatory frameworks. The difference in outcomes can be significant — see why working with a mortgage broker vs. a bank matters more than ever in 2026.

Step 3: Use Private Mortgages as a Bridge, Not a Forever Solution

The smart play for most investors is to use a private mortgage as a 12–24 month bridge while restructuring their portfolio or improving their qualification profile. Then refinance back to an institutional lender at lower rates.

For investors considering restructuring, Second Mortgages vs. Refinancing is a useful comparison to review before deciding.

Step 4: Factor In All Costs

Private mortgages carry higher rates and lender fees, broker fees, and legal costs. Before committing, use a full cost analysis. The guide to understanding closing costs in Toronto helps borrowers avoid sticker shock at the closing table.

Step 5: Pre-Qualify Before You Make Offers

In a market where qualification rules have shifted mid-game, qualifying for a mortgage before buying property is no longer optional — it is essential.

Conclusion: Adapt or Get Left Behind

The OSFI CAR 2026 Rules: How New Capital Requirements Are Driving Toronto Borrowers to Private Mortgages is not a temporary inconvenience. It reflects a deliberate regulatory decision to make the Canadian banking system more resilient — even if that means making it harder for everyday investors to build wealth through real estate [1][8].

For Toronto borrowers, the path forward requires strategy, flexibility, and the right professional guidance.

Actionable next steps:

- ✅ Audit your rental income — identify which income streams have already been used in bank qualifications

- ✅ Consult a licensed mortgage broker who has access to private and alternative lenders

- ✅ Explore private mortgage options as a bridge strategy, not a permanent solution

- ✅ Model the full cost of private financing, including fees and higher rates

- ✅ Stay informed — OSFI’s regulatory environment continues to evolve, and 2026 is just the beginning

The rules have changed. The borrowers who understand the new landscape — and move quickly — will be the ones who keep building in Toronto’s market.

References

[1] Capital Adequacy Requirements Car Guideline 2026 – https://www.osfi-bsif.gc.ca/en/guidance/guidance-library/capital-adequacy-requirements-car-guideline-2026

[2] Private Lending In Canada 2026 What Mortgage Brokers Need To Know About Osfis New Rules – https://www.keycap.ca/blog/private-lending-in-canada-2026-what-mortgage-brokers-need-to-know-about-osfis-new-rules

[3] Backgrounder Final Minimum Capital Test Mct Guideline 2026 – https://www.osfi-bsif.gc.ca/en/news/backgrounder-final-minimum-capital-test-mct-guideline-2026

[4] Unveiling Osfis Proposed New Capital Requirements Impact On Mortgage Lenders And Insurers – https://www.nesto.ca/renewal-refinancing/unveiling-osfis-proposed-new-capital-requirements-impact-on-mortgage-lenders-and-insurers/

[5] 2026 Car Nfp Chap2 En – https://www.osfi-bsif.gc.ca/sites/default/files/documents/2026-car-nfp-chap2-en.pdf

[6] Why Toronto Homeowners Are Ditching Banks For Private Mortgages In 2026 Real Stories And Stats – https://everythingmortgages.ca/blog/why-toronto-homeowners-are-ditching-banks-for-private-mortgages-in-2026-real-stories-and-stats/

[8] Osfi Launches Public Consultation On Capital Adequacy Rules – https://www.canadianmortgagetrends.com/2025/02/osfi-launches-public-consultation-on-capital-adequacy-rules/

[9] Capital Adequacy Requirements Guideline 2026 Letter – https://www.osfi-bsif.gc.ca/en/guidance/guidance-library/capital-adequacy-requirements-guideline-2026-letter

[10] 2026 Car Nfp Chap5 En – https://www.osfi-bsif.gc.ca/sites/default/files/documents/2026-car-nfp-chap5-en.pdf