March 22, 2026

Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Self-employed professionals in Toronto face a unique challenge when pursuing homeownership: proving their income to mortgage lenders. While traditional employees simply provide pay stubs and employment letters, entrepreneurs, contractors, and business owners must navigate complex Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026. With stricter debt service ratio requirements—35% for Gross Debt Service (GDS) and 42% for Total Debt Service (TDS)—self-employed borrowers need strategic financial planning and meticulous documentation to qualify for competitive insured rates on properties under $1.5 million.

The Toronto real estate market in 2026 presents both opportunities and obstacles for self-employed homebuyers. Understanding how lenders assess income, which documents carry the most weight, and how to structure finances to meet GDS/TDS thresholds can mean the difference between mortgage approval and rejection. This comprehensive guide explores proven Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026 that help entrepreneurs secure financing on favorable terms.

Key Takeaways

✅ Two-year income history required: Self-employed borrowers must provide at least 2 years of Notices of Assessment (NOAs) and T1 General tax returns to qualify with traditional lenders[1][4]

✅ GDS/TDS ratios are stricter: Self-employed applicants must keep housing costs under 35% of gross income (GDS) and total debt under 42% (TDS) to access insured mortgage rates

✅ Alternative documentation paths exist: Business financial statements, bank statements, and profit/loss reports can supplement or replace traditional tax documents for income verification[3]

✅ Multiple lender options available: A-lenders, B-lenders, and private lenders offer different qualification criteria, with stated-income programs requiring minimum 10% down payment[2][4]

✅ Strategic planning improves approval odds: Properly structuring business income, maintaining clean tax records, and understanding LTV advantages can significantly enhance mortgage applications

Understanding GDS and TDS Ratios for Self-Employed Borrowers

Gross Debt Service (GDS) and Total Debt Service (TDS) ratios form the foundation of mortgage qualification in Canada. These metrics measure how much of a borrower’s gross income goes toward housing costs and total debt obligations.

What Are GDS and TDS Ratios?

The GDS ratio calculates the percentage of gross monthly income needed to cover housing-related expenses, including:

- Mortgage principal and interest payments

- Property taxes

- Heating costs

- 50% of condominium fees (if applicable)

The TDS ratio expands this calculation to include all debt obligations:

- All GDS components listed above

- Credit card payments

- Car loans

- Personal loans

- Lines of credit

- Other debt obligations

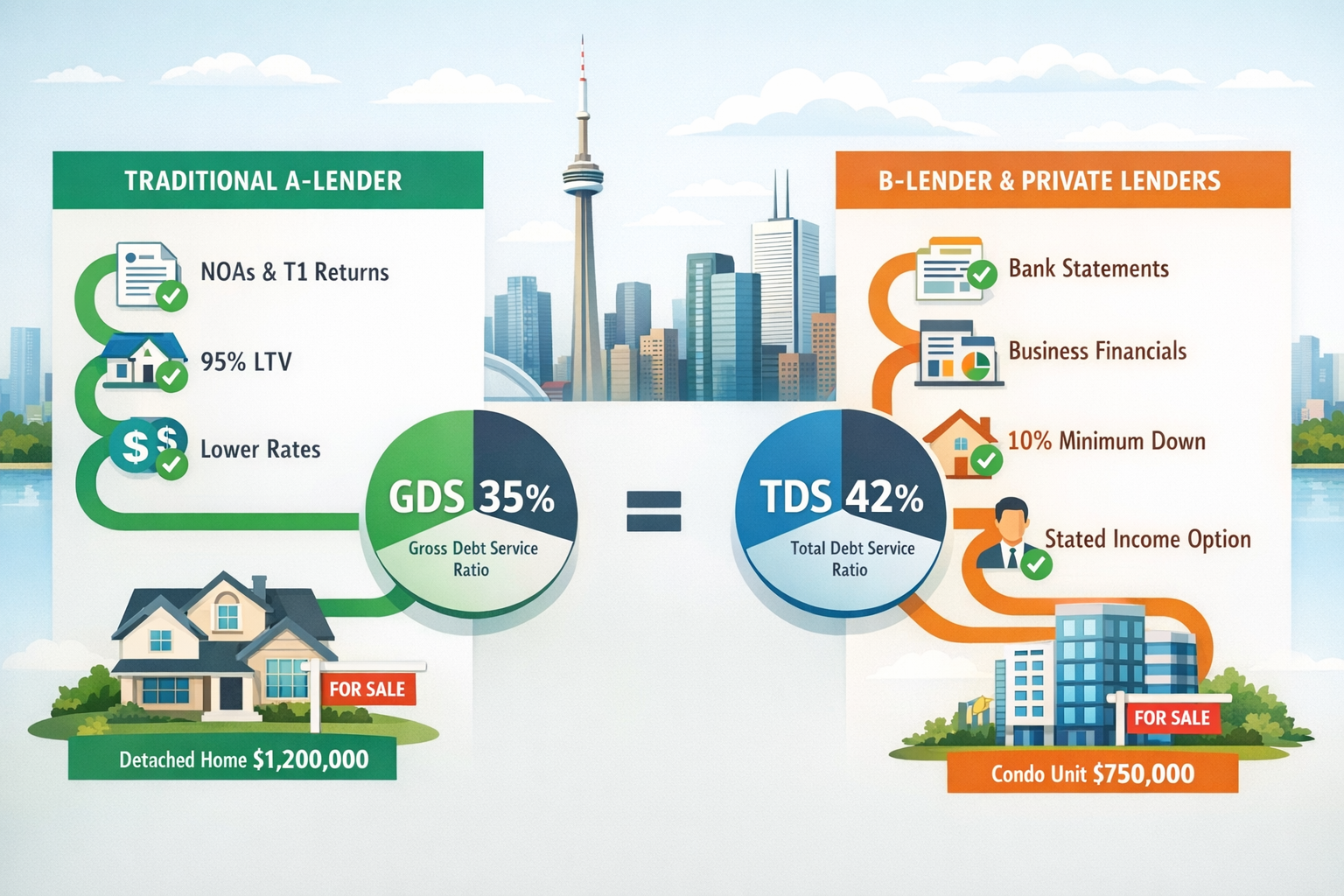

For self-employed borrowers seeking insured mortgages (properties under $1 million with less than 20% down payment), lenders typically require:

📊 GDS ratio: Maximum 35%

📊 TDS ratio: Maximum 42%

These thresholds are often stricter than those applied to traditionally employed borrowers, reflecting lenders’ perception of higher income volatility among self-employed individuals.

Why Self-Employed Borrowers Face Stricter Requirements

Lenders view self-employed income as less predictable than salaried employment. Business revenue fluctuates seasonally, economic conditions affect profitability, and entrepreneurs often write off significant expenses that reduce their taxable income—and consequently, their mortgage-qualifying income.

This perceived risk translates into more rigorous documentation requirements and tighter debt service ratio limits. Self-employed applicants must demonstrate consistent, verifiable income over multiple years to prove their ability to maintain mortgage payments through business cycles.

Working with experienced mortgage brokers who specialize in self-employed applications can help navigate these stricter requirements and identify lenders with more flexible qualification criteria.

Primary Income Verification Strategies for Self-Employed Toronto Mortgages

The cornerstone of Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026 involves understanding which documents lenders prioritize and how to present financial information most effectively.

The Two-Year Income History Requirement

Traditional lenders (A-lenders such as major banks and credit unions) require self-employed borrowers to demonstrate at least 2 years of consistent income through official tax documentation[1][4]. This standard applies across the Canadian mortgage industry and represents the minimum threshold for conventional mortgage approval.

The two-year requirement serves multiple purposes:

- Establishes income consistency: Shows the business generates reliable revenue across different periods

- Reduces lender risk: Longer track record indicates business stability

- Enables income averaging: Allows lenders to calculate qualifying income based on multi-year performance

Some lenders may consider applicants with less than two years of self-employment history if they previously worked in the same field as employees and can demonstrate industry expertise and income continuity.

Notice of Assessment (NOA) as the Gold Standard

The Notice of Assessment (NOA) issued by the Canada Revenue Agency (CRA) represents the most trusted income verification document for self-employed mortgage applicants[2][4]. Lenders prioritize NOAs because they:

✔️ Verify reported income: Confirm the income declared on tax returns

✔️ Check for tax compliance: Reveal any outstanding tax balances or payment issues

✔️ Validate filing accuracy: Ensure tax returns match the mortgage application

✔️ Identify potential liens: Flag unpaid taxes that could result in CRA liens on property

Critical warning: Unpaid taxes shown on NOAs represent a major red flag for lenders. The CRA can place liens on property for outstanding tax debts, which would take priority over the mortgage lender’s security interest. Applicants must resolve all tax arrears before pursuing mortgage approval[2][4].

Lenders typically request NOAs from the past 2-3 years to establish income trends and calculate qualifying income. For comprehensive guidance on documentation requirements, review our ultimate guide to securing mortgages for self-employed Canadians.

T1 General Tax Returns

Alongside NOAs, lenders require complete T1 General tax returns for the same 2-3 year period[1][4]. These returns provide detailed income breakdowns and allow lenders to assess:

- Total income from all sources

- Business expenses and deductions claimed

- Net income after expenses

- Income stability and growth trends

Lenders calculate qualifying income based on the information in T1 returns, often using the line 15000 (total income) or averaging income across multiple years if there’s significant variation.

Supplemental Documentation for Stronger Applications

Beyond NOAs and T1 returns, additional documentation strengthens self-employed mortgage applications by providing a more complete financial picture[1][4][5]:

📄 Bank Statements: 3-6 months of business and personal bank statements demonstrate cash flow, regular deposits, and financial management capabilities.

📄 Business Financial Statements: Balance sheets, income statements, and cash flow statements prepared by accountants provide professional validation of business performance.

📄 Profit and Loss Statements: Detailed P&L reports show revenue, expenses, and net profit over specific periods, helping lenders understand business operations.

📄 Signed Contracts: Future contracts and ongoing agreements demonstrate income continuity and business pipeline, particularly valuable for contractors and consultants.

📄 Corporate Tax Returns: For incorporated businesses, T2 corporate returns supplement personal tax documentation and show business-level income.

📄 Business License and Registration: Proof of legitimate business operation and professional credentials.

This multi-layered documentation approach addresses lender concerns about income verification and demonstrates financial responsibility. Contractors should review our specialized guide on self-employed mortgages for contractors for industry-specific strategies.

Alternative Income Verification Paths: Beyond Traditional Documentation

Not all self-employed borrowers can demonstrate qualifying income through traditional tax returns. Many entrepreneurs legitimately write off significant business expenses that reduce taxable income but don’t reflect actual cash flow or earning capacity. For these situations, Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026 include alternative documentation paths.

Non-Traditional Income Confirmation Programs

Several lenders recognize that personal tax returns don’t always reflect a self-employed borrower’s true earning capacity. These lenders accept business financial statements and bank statements as primary income verification documents[3].

This approach works particularly well for:

- Business owners who reinvest profits back into their companies

- Entrepreneurs with significant legitimate business expenses

- Professionals in growth phases who prioritize business development over personal income

- Contractors with variable project-based income

Under these programs, lenders analyze business-level revenue and cash flow rather than personal taxable income, potentially qualifying borrowers for higher mortgage amounts than traditional documentation would support.

Stated-Income Mortgage Programs

B-lenders and private lenders offer stated-income mortgage programs that require minimal income documentation[2][4]. These programs cater to self-employed borrowers who:

- Have less than 2 years of self-employment history

- Cannot verify income through traditional documentation

- Have complex income structures

- Need faster approval timelines

Stated-income program requirements typically include:

💰 Minimum 10% down payment (some lenders require 15-20%)

💳 Strong credit score (usually 650+, preferably 700+)

📋 Evidence of active business through invoices, contracts, or business registration

🏢 Business legitimacy demonstrated through website, business cards, or professional licenses

Trade-off: Stated-income mortgages carry higher interest rates—typically 0.5% to 2% above prime lending rates—reflecting the increased risk lenders assume without traditional income verification[2][4].

For borrowers considering alternative lending options, our guide to B-lender mortgage rates in Toronto provides current rate comparisons and qualification criteria.

Bank Statement Loan Programs

Bank statement loans represent a middle ground between traditional documentation and stated-income programs. These mortgages use 12-24 months of business bank statements to calculate qualifying income based on deposits rather than tax returns[3].

Lenders typically apply a formula to gross deposits:

- Personal bank statements: Calculate income as 100% of average monthly deposits

- Business bank statements: Calculate income as 50-75% of average monthly deposits (accounting for business expenses)

This approach benefits self-employed borrowers with strong cash flow but lower reported taxable income. For detailed information on this option, see our comprehensive guide to bank statement loans for self-employed borrowers in 2026.

Loan-to-Value (LTV) Advantages with Income Verification

Self-employed borrowers who successfully verify income through traditional documentation access higher loan-to-value ratios and more competitive rates[3]:

With CMHC Insurance: Up to 95% LTV (5% down payment) on properties under $500,000

With Private Insurers (Sagen or Canada Guaranty): Up to 90% LTV (10% down payment)

Conventional Mortgages: Up to 80% LTV (20% down payment) without insurance

Higher LTV ratios reduce the down payment burden and preserve capital for business operations or emergency reserves. However, accessing these ratios requires meeting strict GDS/TDS limits and providing comprehensive income documentation.

Strategic Planning to Overcome GDS/TDS Barriers

Meeting the 35% GDS and 42% TDS thresholds requires strategic financial planning well before applying for a mortgage. These Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026 focus on optimizing financial positioning.

Optimizing Income Reporting

Self-employed borrowers must balance tax efficiency with mortgage qualification. While minimizing taxable income reduces tax liability, it also reduces mortgage-qualifying income.

Strategic income optimization includes:

🎯 Plan ahead: Begin preparing for mortgage applications 2-3 years in advance

🎯 Adjust expense claims: Consider claiming fewer discretionary business expenses in years leading to mortgage applications

🎯 Maximize salary vs. dividends: For incorporated businesses, taking higher salary (rather than dividends) increases qualifying income

🎯 Document add-backs: Work with accountants to identify legitimate business expenses that can be “added back” to income for mortgage purposes

🎯 Maintain consistency: Avoid dramatic income fluctuations that raise lender concerns

For medical professionals navigating these challenges, our guide on getting mortgage approval as a self-employed doctor in Ontario provides profession-specific strategies.

Reducing Debt Obligations Before Applying

Since TDS ratios include all debt obligations, reducing existing debts significantly improves mortgage qualification:

Debt reduction strategies:

- Pay off credit cards: Eliminate high-interest revolving debt

- Consolidate loans: Combine multiple payments into lower monthly obligations

- Pay down car loans: Reduce or eliminate vehicle financing

- Avoid new credit: Don’t take on additional debt in the 6-12 months before applying

- Close unused credit facilities: Reduce available credit that lenders include in calculations

Even reducing monthly debt payments by $200-300 can increase mortgage qualification by $40,000-60,000, depending on rates and amortization.

Choosing the Right Property Price Point

Toronto’s real estate market offers properties across a wide price spectrum. Strategic property selection based on GDS/TDS constraints can make the difference between approval and rejection.

Strategic property considerations:

🏠 Stay under $1.5M: Properties under this threshold qualify for insured mortgages with better rates

🏠 Consider lower property taxes: Suburban Toronto properties often have lower tax rates than downtown

🏠 Factor in condo fees: High condo fees significantly impact GDS calculations (50% of fees count)

🏠 Evaluate heating costs: Older homes with higher utility costs affect GDS ratios

🏠 Plan for maintenance: Budget beyond mortgage payments to avoid future financial stress

For first-time buyers exploring Toronto neighborhoods, our guide to Toronto’s hottest freehold neighborhoods in 2026 identifies value opportunities.

Working with Specialized Mortgage Professionals

Self-employed mortgage applications require expertise beyond standard residential financing. Mortgage brokers specializing in self-employed clients provide critical advantages:

✨ Access to multiple lenders: Brokers work with A-lenders, B-lenders, and private lenders, increasing approval odds

✨ Documentation guidance: Help structure financial documents for maximum impact

✨ Income calculation expertise: Understand how different lenders calculate qualifying income

✨ Alternative program knowledge: Identify stated-income and bank statement options when traditional paths fail

✨ Rate negotiation: Leverage lender relationships to secure competitive rates

Brokers also understand nuances like how different lenders treat specific business expenses, which documentation carries the most weight, and how to position applications for success. Learn more about the benefits in our article on working with a mortgage broker in Toronto.

Timing Applications with Business Cycles

Self-employed income often fluctuates seasonally or follows business cycles. Strategic timing of mortgage applications can significantly impact approval outcomes:

Timing considerations:

📅 Apply after strong income years: Wait until NOAs reflect peak earning periods

📅 Avoid application during business transitions: Don’t apply while changing business models or expanding

📅 Consider tax filing timing: Apply after filing taxes but before year-end to show most recent income

📅 Monitor rate environments: Balance income documentation readiness with current mortgage rate trends

📅 Plan around major expenses: Avoid large business purchases or expansions immediately before applications

Credit Score Optimization

While income verification and GDS/TDS ratios dominate self-employed mortgage discussions, credit scores remain critically important. Strong credit can offset some income documentation challenges and qualify borrowers for better rates.

Credit optimization strategies:

- Maintain credit utilization below 30% of available limits

- Make all payments on time for at least 12 months before applying

- Avoid closing old credit accounts (credit history length matters)

- Correct any errors on credit reports well in advance

- Build diverse credit mix (revolving and installment credit)

For detailed information on how credit scores affect mortgage approval, review our guide on understanding the role of credit scores in the mortgage approval process.

Specialized Programs for Self-Employed Borrowers in 2026

The Canadian mortgage landscape in 2026 includes several programs specifically designed to address the unique challenges self-employed borrowers face.

CMHC Business-for-Self Program

The Canada Mortgage and Housing Corporation (CMHC) offers a Business-for-Self program that provides insured mortgage financing for self-employed borrowers with less restrictive documentation requirements[8].

Program features:

- Accepts borrowers with minimum 2 years of self-employment

- Allows income verification through financial statements

- Provides access to high-ratio financing (up to 95% LTV)

- Requires proof of business operation and income stability

This program represents one of the most accessible options for self-employed borrowers seeking competitive rates with government-backed insurance.

Sagen Business-for-Self Program

Sagen (formerly Genworth Canada) offers a similar Business-for-Self program with flexible income verification options[7]:

- Accepts various documentation types beyond traditional tax returns

- Considers business financial statements and bank statements

- Provides mortgage insurance for down payments as low as 5%

- Evaluates income based on business performance and cash flow

These programs specifically address the income verification challenges that prevent many self-employed borrowers from accessing competitive mortgage rates.

Alternative Lender Programs

Beyond traditional banks and insured mortgage programs, alternative lenders in 2026 offer specialized products for self-employed borrowers:

Credit unions: Often more flexible with income documentation and willing to consider unique situations

Mortgage investment corporations (MICs): Provide short-term financing for borrowers who don’t qualify with traditional lenders

Private lenders: Offer asset-based lending with minimal income verification but higher rates

For borrowers with strong business fundamentals but complex income situations, exploring easier qualification options for self-employed borrowers can identify suitable programs.

Common Pitfalls and How to Avoid Them

Understanding common mistakes helps self-employed borrowers navigate the mortgage process more successfully.

Insufficient Documentation Preparation

Problem: Scrambling to gather documents after finding a property creates stress and delays approval.

Solution: Begin assembling documentation 6-12 months before house hunting. Maintain organized files with:

- 3 years of NOAs and T1 returns

- 2 years of business financial statements

- 6-12 months of bank statements

- Current business licenses and registrations

- Contracts and invoices demonstrating ongoing business

Inconsistent Income Reporting

Problem: Significant year-over-year income variations raise lender concerns about stability.

Solution: Work with accountants to maintain consistent income reporting. If income must fluctuate, document reasons (business expansion, market conditions) and provide context to lenders.

Ignoring GDS/TDS Limits During Property Search

Problem: Falling in love with properties beyond qualifying capacity wastes time and creates disappointment.

Solution: Get pre-qualified before house hunting. Understand exact GDS/TDS limits and search within realistic price ranges. Use mortgage affordability calculators to establish budgets.

Mixing Business and Personal Finances

Problem: Commingled finances make income verification difficult and raise lender concerns about financial management.

Solution: Maintain separate business and personal bank accounts. Use business accounts exclusively for business transactions and pay yourself regular, documented salary or draws.

Applying Too Soon After Starting Business

Problem: Applying before establishing 2-year income history results in automatic rejections from traditional lenders.

Solution: Wait until completing 2 full tax years of self-employment, or explore alternative lender programs designed for newer businesses. Consider stated-income programs if business fundamentals are strong but history is short.

Neglecting Tax Compliance

Problem: Outstanding tax balances or unfiled returns immediately disqualify borrowers from most mortgage programs.

Solution: Maintain current tax filings and pay all taxes owed before applying. If tax debt exists, establish payment plans with CRA and resolve arrears before pursuing mortgages.

Conclusion

Successfully navigating Income Verification Strategies for Self-Employed Toronto Mortgages: Overcoming GDS/TDS Barriers in 2026 requires understanding lender requirements, strategic financial planning, and comprehensive documentation preparation. Self-employed borrowers face stricter scrutiny than traditionally employed applicants, but with proper preparation, competitive mortgage approval is entirely achievable.

The foundation of success lies in demonstrating consistent, verifiable income through Notices of Assessment and T1 General tax returns covering at least 2 years. Supplementing these core documents with business financial statements, bank statements, and profit/loss reports strengthens applications and addresses lender concerns about income stability.

For borrowers whose tax returns don’t reflect true earning capacity, alternative paths exist through bank statement loans, stated-income programs, and specialized lenders who evaluate business-level performance rather than personal taxable income. While these options typically carry higher interest rates, they provide viable pathways to homeownership for entrepreneurs and business owners with strong cash flow but lower reported income.

Meeting the 35% GDS and 42% TDS thresholds requires strategic planning: optimizing income reporting, reducing existing debt obligations, choosing appropriate property price points, and timing applications to showcase peak business performance. Working with mortgage brokers who specialize in self-employed applications provides access to multiple lenders and expertise in positioning applications for success.

Next Steps for Self-Employed Toronto Homebuyers

✅ Assess current documentation: Gather 2-3 years of NOAs, T1 returns, and business financial statements

✅ Calculate GDS/TDS ratios: Determine current debt service ratios and identify improvement opportunities

✅ Optimize financial positioning: Reduce debt, improve credit scores, and adjust income reporting strategies

✅ Consult specialized professionals: Connect with mortgage brokers experienced in self-employed applications

✅ Explore multiple lender options: Consider A-lenders, B-lenders, and alternative programs to maximize approval odds

✅ Get pre-qualified: Understand exact borrowing capacity before beginning property searches

✅ Monitor rate trends: Stay informed about 2026 mortgage rate forecasts to time applications strategically

The Toronto real estate market in 2026 offers opportunities for well-prepared self-employed borrowers who understand lender requirements and present comprehensive, well-documented applications. With strategic planning and expert guidance, overcoming GDS/TDS barriers and securing competitive mortgage financing is not just possible—it’s a realistic goal for entrepreneurs and business owners ready to invest in Toronto homeownership.

For comprehensive support throughout the mortgage process, explore our full range of resources on mortgages for self-employed borrowers and connect with specialists who understand the unique challenges and opportunities self-employed professionals face in today’s mortgage market.

References

[1] Can You Get A Mortgage With A Self Employed Status In Canada – https://lendinghub.ca/blog/can-you-get-a-mortgage-with-a-self-employed-status-in-canada

[2] Self Employed Mortgage – https://www.ratehub.ca/self-employed-mortgage

[3] Self Employed Mortgage – https://wowa.ca/self-employed-mortgage

[4] Self Employed Mortgage Options Qualifications In Canada – https://www.nesto.ca/mortgage-basics/self-employed-mortgage-options-qualifications-in-canada/

[5] Documenting Your Income For A Mortgage When Youre Self Employed – https://thegenesisgroup.ca/documenting-your-income-for-a-mortgage-when-youre-self-employed/

[6] Understanding Income Verification For Self Employed Mortgage Applicants – https://mortgagesquad.ca/understanding-income-verification-for-self-employed-mortgage-applicants/

[7] Business For Self – https://www.sagen.ca/products-and-services/business-for-self/

[8] Self Employed – https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/self-employed