March 23, 2026

BoC Holds at 2.25% in March 2026: Lowest Variable Rates for Self-Employed Toronto Buyers Under Stress Test

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The Bank of Canada’s decision to maintain its overnight rate at 2.25% on March 18, 2026, has created a unique window of opportunity for Self-Employed Homebuyers in Toronto. With variable mortgage rates now sitting at historic lows of 3.95% for five-year terms, and the qualifying stress test rate at just 5.25%, self-employed borrowers who typically face stricter income verification requirements can finally access affordable financing. This rate hold, the second consecutive pause in 2026, comes at a critical time when inflation has cooled to 1.8% and the housing market shows signs of stabilization[2][4].

For self-employed professionals—from freelance consultants to small business owners—understanding how the BoC holds at 2.25% in March 2026 translates into the lowest variable rates for self-employed Toronto buyers under stress test conditions is essential for making informed mortgage decisions.

Key Takeaways

✅ Variable rates at 3.95% represent the lowest qualifying rates for self-employed borrowers in years, with stress testing at just 5.25%

✅ The BoC held rates at 2.25% on March 18, 2026, marking the second consecutive pause as inflation dropped to 1.8%[2][4]

✅ Self-employed buyers face unique challenges but can leverage bank statement mortgages and alternative documentation to qualify at these favorable rates

✅ Mid-2026 rate increases are possible if energy-driven inflation broadens, making current variable rates a time-sensitive opportunity[3][6]

✅ Strategic mortgage selection matters: Variable rates offer flexibility and savings now, but fixed options provide protection against potential hikes

Understanding the March 2026 BoC Rate Decision and Its Impact on Mortgage Markets

The Bank of Canada’s March 18, 2026, announcement to hold its overnight rate at 2.25% sent positive ripples through the mortgage market[2]. This decision, which kept the Bank Rate at 2.5% and the deposit rate at 2.20%, reflects the central bank’s confidence that inflation is moving toward its 2% target despite recent global disruptions[2][4].

Why the BoC Held Rates Steady

Several key economic factors influenced the BoC’s decision to maintain rates:

Inflation Progress: Consumer Price Index (CPI) inflation eased significantly to 1.8% in February 2026, down from 2.3% in January[2][4]. Core inflation measures—which strip out volatile components—are now hovering close to the BoC’s 2% target, indicating that previous rate cuts have successfully cooled price pressures without triggering a recession.

Weak GDP Growth: Canada’s economy contracted by 0.6% in the fourth quarter of 2025, weaker than economists expected[4]. This contraction was primarily driven by larger-than-anticipated inventory drawdowns, though domestic demand remained relatively strong with over 2% growth from consumer and government spending[4].

Soft Labour Market: Unemployment climbed to 6.7% in February 2026, with employment gains from Q4 2025 largely reversed in the first two months of the year[2]. This softening labour market suggests the economy has sufficient slack to prevent wage-driven inflation from accelerating.

“The Governing Council judges that monetary policy is now sufficiently stimulative to support continued economic growth and keep inflation close to target.” — Bank of Canada, March 18, 2026[4]

How Rate Holds Translate to Variable Mortgage Rates

When the BoC holds its overnight rate at 2.25%, lenders’ prime rates typically sit around 4.20%, which directly influences variable mortgage rates. Most competitive variable-rate mortgages offer discounts from prime, resulting in actual rates of approximately 3.95% for well-qualified borrowers with strong credit profiles.

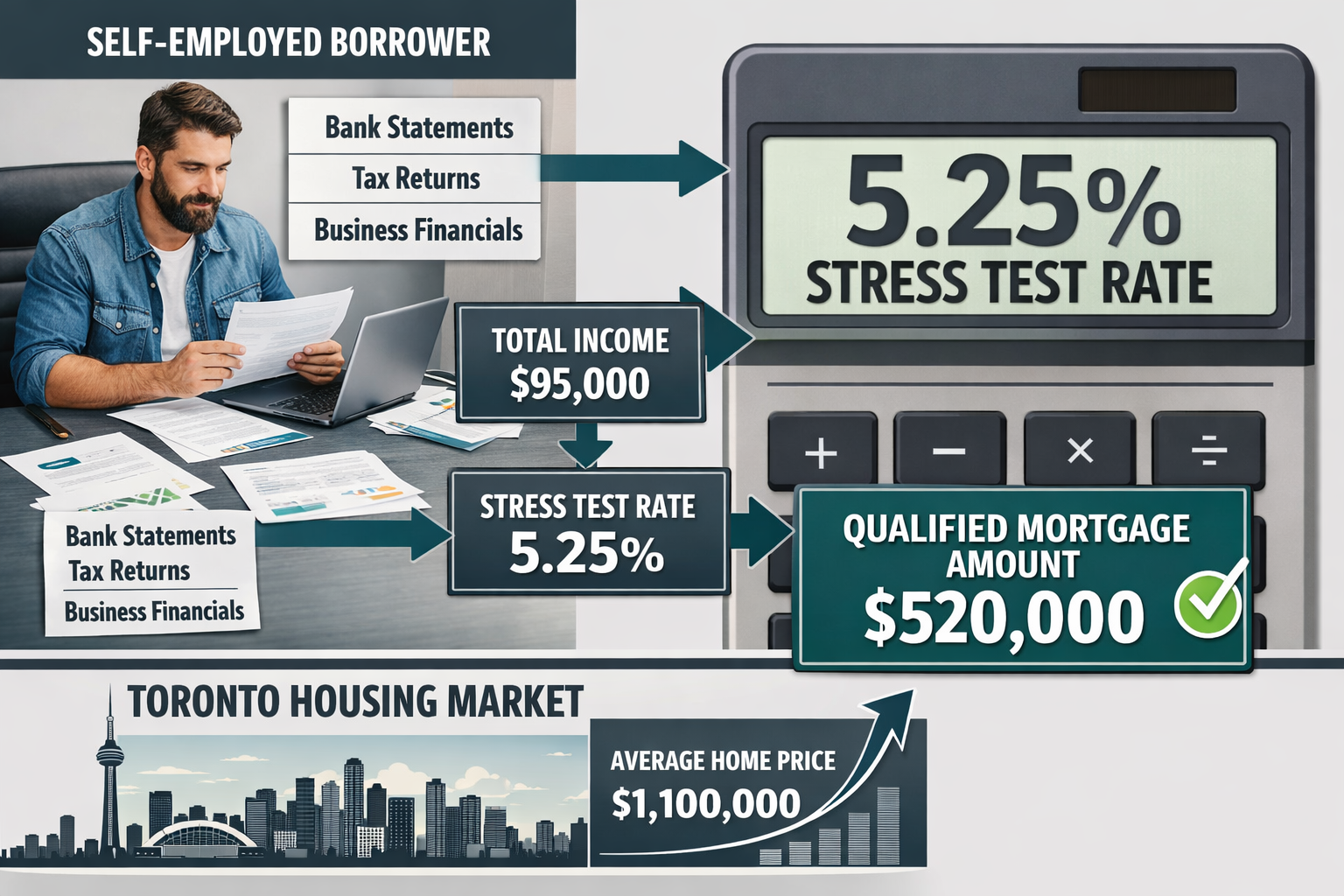

For self-employed buyers in Toronto, this creates a compelling opportunity. The qualifying stress test rate is calculated as either the contract rate plus 2% or 5.25%, whichever is higher. With variable rates at 3.95%, borrowers must qualify at 5.25%—the lowest stress test threshold in recent years.

Geopolitical Risks on the Horizon

While the rate hold is positive news, the BoC acknowledged significant geopolitical risks. The effective closure of the Strait of Hormuz threatens approximately 20% of global oil supply, and transportation bottlenecks could affect fertilizer and other commodities[6]. Global energy prices have risen sharply since the Middle East conflict outbreak, which will boost inflation in the near term[1][2].

The central bank emphasized it will “look through” temporary energy price increases only if they remain contained. If inflation pressures broaden beyond energy, the BoC may need to adjust policy accordingly[1]. Markets are already pricing in potential rate hikes later in 2026 if these risks materialize[3][6].

BoC Holds at 2.25% in March 2026: What This Means for Self-Employed Toronto Buyers Under Stress Test

Self-employed borrowers have historically faced more stringent mortgage qualification requirements than salaried employees. Without T4 slips showing consistent income, lenders scrutinize business financials, tax returns, and bank statements more carefully. However, the BoC holds at 2.25% in March 2026 has created the lowest variable rates for self-employed Toronto buyers under stress test conditions in years.

The Self-Employed Income Verification Challenge

Traditional mortgage qualification relies heavily on employment letters and T4 income statements. Self-employed professionals—including contractors, freelancers, consultants, and small business owners—typically don’t have these documents. Instead, they must provide:

- Two years of Notice of Assessments (NOAs) from the Canada Revenue Agency

- Business financial statements (often reviewed or audited)

- Corporate tax returns (T2s for incorporated businesses)

- Bank statements showing consistent cash flow

- Contracts or invoices demonstrating ongoing business activity

Many self-employed individuals legitimately write off business expenses to minimize taxable income, which can significantly reduce their “stated income” for mortgage purposes. A contractor earning $120,000 gross might show only $65,000 in net income after legitimate deductions—severely limiting borrowing capacity under traditional qualification methods.

How the Current Stress Test Works for Self-Employed Buyers

The federal mortgage stress test requires all borrowers to qualify at the higher of:

- The contract rate plus 2%, or

- 5.25% (the current minimum qualifying rate)

With variable rates at 3.95%, self-employed buyers must qualify at 5.25%. While this might seem restrictive, it’s actually the most favorable stress test environment in several years. When rates were higher in 2023-2024, borrowers had to qualify at 7% or more, drastically reducing purchasing power.

Example Qualification Scenario:

A self-employed graphic designer in Toronto with:

- Stated income: $75,000 (after business deductions)

- Down payment: $100,000 (20%)

- Purchase price target: $500,000

- Monthly debts: $400 (car payment)

Using a 5.25% stress test rate with a 25-year amortization:

- Maximum mortgage: $400,000

- Required gross debt service ratio (GDS): Under 39%

- Required total debt service ratio (TDS): Under 44%

This buyer would qualify for approximately $475,000-$500,000 purchase price, depending on property taxes and condo fees. At higher stress test rates of 6.5% or 7%, the same borrower might only qualify for $425,000-$450,000.

Alternative Documentation Options for Self-Employed Borrowers

Recognizing the challenges self-employed buyers face, several alternative mortgage programs have emerged:

Bank Statement Mortgages 📊

These programs allow borrowers to qualify using 12-24 months of business bank statements rather than tax returns. Lenders analyze deposits to calculate average monthly income, typically using 50-75% of gross deposits as qualifying income. This approach helps self-employed borrowers whose tax returns don’t reflect their true earning capacity.

Stated Income Mortgages

Available through alternative lenders, these mortgages allow borrowers to “state” their income with minimal documentation. Interest rates are typically 0.5-1.5% higher than prime lending rates, but qualification is significantly easier. These work well for self-employed buyers with strong credit (680+) and substantial down payments (20%+).

Business-for-Self (BFS) Programs

Some lenders offer specialized programs for incorporated professionals like doctors, lawyers, and accountants. These professional mortgage programs may require only one year of income history and offer more flexible qualification criteria.

For comprehensive guidance on qualifying for mortgages without T4 slips, self-employed Toronto buyers should explore all available documentation pathways.

Maximizing Qualification with Current Low Rates

To take advantage of the BoC holds at 2.25% in March 2026 and secure the lowest variable rates for self-employed Toronto buyers under stress test conditions, consider these strategies:

✅ Minimize debt before applying: Pay down credit cards, car loans, and lines of credit to improve debt service ratios

✅ Optimize tax strategies: Work with an accountant to balance tax deductions against mortgage qualification needs (see tax strategies for self-employed)

✅ Build strong bank statement history: Maintain consistent deposits and avoid large irregular transactions for 12+ months before applying

✅ Increase down payment: Larger down payments (25-30%+) can unlock better rates and easier qualification with alternative lenders

✅ Consider co-borrowers: Adding a salaried spouse or partner can significantly improve qualification capacity

Variable vs. Fixed Mortgage Rates: Strategic Considerations for Self-Employed Buyers in 2026

With the BoC holding rates steady and variable mortgages at 3.95%, self-employed Toronto buyers face a critical decision: lock in a fixed rate for stability or embrace variable rates for potential savings and flexibility?

Current Rate Landscape (March 2026)

| Mortgage Type | Typical Rate | Stress Test Rate | Monthly Payment (on $400K) |

|---|---|---|---|

| 5-Year Variable | 3.95% | 5.25% | $2,088 |

| 5-Year Fixed | 4.49% | 6.49% | $2,240 |

| 3-Year Fixed | 4.29% | 6.29% | $2,195 |

| 1-Year Fixed | 4.69% | 6.69% | $2,283 |

Rates are approximate and vary by lender, credit profile, and down payment. Monthly payments assume 25-year amortization.

Advantages of Variable Rates for Self-Employed Buyers

Lower Initial Payments 💰

Variable rates currently offer savings of approximately $150-200 per month compared to five-year fixed rates. Over a year, this represents $1,800-2,400 in reduced housing costs—meaningful savings for self-employed professionals managing variable income streams.

Flexibility and Portability

Variable-rate mortgages typically come with more flexible terms:

- Lower penalties: Usually three months’ interest rather than the punitive Interest Rate Differential (IRD) calculations used for fixed mortgages

- Easier to break: If business circumstances change or you need to sell, variable mortgages are less expensive to exit

- Rate decreases benefit you immediately: If the BoC cuts rates further (unlikely but possible), variable-rate holders benefit immediately

Better Stress Test Qualification

The lower contract rate means easier qualification at the 5.25% stress test minimum, maximizing purchasing power for self-employed buyers with complex income documentation.

When Fixed Rates Make More Sense

Income Stability Concerns

Self-employed income can fluctuate seasonally or with economic conditions. If your business faces potential volatility, the predictable payments of a fixed-rate mortgage provide budgeting certainty.

Rate Increase Protection

With geopolitical risks threatening to push inflation higher, markets are pricing in potential BoC rate hikes in late 2026[3][6]. If the overnight rate increases to 3.25% or higher, variable rates could climb to 4.95-5.20%, eliminating current savings.

Psychological Comfort

Some borrowers simply sleep better knowing their rate won’t change. If rate uncertainty causes stress, the premium for fixed rates (currently about 0.54%) may be worth the peace of mind.

Mid-2026 Rate Forecast: What Self-Employed Buyers Should Watch

The next BoC rate announcement is scheduled for April 29, 2026[4]. Several factors will influence rate direction:

📈 Upward Pressure Factors:

- Energy price inflation from Middle East supply disruptions

- Stronger-than-expected consumer spending

- Wage growth acceleration

- Persistent core inflation above 2%

📉 Downward Pressure Factors:

- Continued GDP weakness or contraction

- Rising unemployment beyond 7%

- Housing market deterioration

- Global recession concerns

Most economists expect the BoC to hold rates steady through mid-2026, with a slight bias toward a 0.25% increase in Q3 or Q4 if energy-driven inflation proves persistent[3]. For self-employed buyers, this suggests:

- Variable rates remain attractive for those comfortable with moderate risk and who can absorb potential 0.25-0.50% increases

- Short-term fixed rates (1-2 years) offer a compromise, locking in rates slightly above current variable levels while maintaining flexibility to refinance if rates fall

- Long-term fixed rates (5+ years) make sense for risk-averse borrowers or those with tight debt service ratios

For additional context on how mortgage rates respond to economic conditions, understanding the broader economic picture is essential.

Actionable Steps: How Self-Employed Toronto Buyers Can Secure the Best Rates Today

Taking advantage of the BoC holds at 2.25% in March 2026 and securing the lowest variable rates for self-employed Toronto buyers under stress test conditions requires strategic preparation and expert guidance.

Step 1: Assess Your Financial Documentation (2-3 Months Before)

Gather Essential Documents:

- Last two years of personal tax returns (T1 Generals) and NOAs

- Last two years of business tax returns (T2s if incorporated)

- Year-to-date profit and loss statements

- Business bank statements (12-24 months)

- Personal bank statements (3-6 months)

- Credit report (check for errors)

Optimize Your Financial Profile:

- Ensure consistent business deposits for at least 12 months

- Pay down high-interest debt to improve credit score and debt ratios

- Avoid large irregular deposits that might require explanation

- Keep business and personal finances clearly separated

Step 2: Get Pre-Qualified with Multiple Lenders (1-2 Months Before)

Don’t limit yourself to big banks. Self-employed borrowers often get better treatment from:

- Mortgage brokers who have access to 30+ lenders, including those specializing in self-employed mortgages

- Credit unions that may offer more flexible underwriting

- Alternative lenders providing bank statement mortgage programs

- Private lenders for complex situations (though rates are higher)

Questions to Ask:

- What documentation do you require for self-employed borrowers?

- Do you offer bank statement or stated income programs?

- What is your current variable rate and stress test qualification rate?

- What are the penalties for breaking the mortgage early?

- Are there any professional programs for my occupation?

Step 3: Time Your Application Strategically

Best Times to Apply:

- After tax season: Once NOAs are available (typically May-June)

- During strong business periods: When recent bank statements show robust cash flow

- Before rate increases: If BoC signals potential hikes, lock in rates quickly

Avoid Applying When:

- You’ve just changed business structure (incorporation, partnership changes)

- Recent large business expenses have temporarily reduced cash flow

- You’re between contracts or in a seasonal low period

Step 4: Consider Rate Holds and Conversion Options

Most lenders offer 90-120 day rate holds, allowing you to lock in current rates while you house hunt. For self-employed buyers, this is especially valuable given the longer qualification process.

Rate Hold Strategy:

- Get pre-approved and hold the 3.95% variable rate

- If rates drop before closing, many lenders allow you to take the lower rate

- If rates rise, you’re protected at the held rate

Some lenders also offer variable-to-fixed conversion options without penalty, giving you the flexibility to lock in if rates start climbing mid-term.

Step 5: Work with Specialists Who Understand Self-Employed Challenges

The mortgage landscape for self-employed borrowers is complex and constantly evolving. Working with professionals who specialize in non-traditional income verification can mean the difference between approval and rejection.

Benefits of Specialist Mortgage Brokers:

- Access to lenders you won’t find on your own

- Experience structuring applications to maximize approval odds

- Knowledge of which lenders are currently most flexible with self-employed income

- Ability to present your financial situation in the best light

- No cost to you (lenders pay broker commissions)

Step 6: Understand Total Homeownership Costs in Toronto

Beyond mortgage payments, Toronto homebuyers face significant additional costs:

- Property taxes: $3,000-8,000+ annually depending on location and property value

- Home insurance: $1,200-2,500 annually

- Condo fees: $400-800+ monthly for condos

- Utilities: $150-300+ monthly

- Maintenance reserve: 1-3% of home value annually

- Legal fees: $1,500-3,000 at closing

Ensure your budget accounts for these costs, especially since self-employed income can fluctuate.

Step 7: Plan for Future Rate Changes

Even with today’s favorable rates, prudent financial planning means preparing for potential increases:

Stress Test Your Own Budget:

- Calculate payments at your variable rate plus 1-2%

- Ensure you can comfortably afford payments if rates rise to 5-6%

- Build an emergency fund covering 6-12 months of expenses

- Consider accelerated payment options to build equity faster

Refinancing Opportunities:

- Monitor rate trends and be prepared to refinance if significantly better options emerge

- Understand your mortgage’s portability and refinancing terms

- Keep documentation current in case you need to qualify again

Conclusion: Seizing the Opportunity While Rates Remain Low

The Bank of Canada’s decision to hold rates at 2.25% in March 2026 has created a remarkable opportunity for self-employed Toronto homebuyers. With variable mortgage rates at 3.95% and stress test qualification at just 5.25%, self-employed professionals face the most favorable borrowing conditions in years—despite the unique documentation challenges they typically encounter.

However, this window may not remain open indefinitely. Geopolitical tensions threatening global energy supplies, combined with persistent inflation risks, could push the BoC toward rate increases in late 2026[3][6]. Self-employed buyers who act strategically now can lock in these historically low rates before conditions change.

Key Actions to Take This Week:

- Review your financial documentation and identify any gaps that need addressing

- Connect with a mortgage broker specializing in self-employed borrowers to understand your qualification potential

- Get pre-approved and secure a rate hold to protect against potential increases

- Compare variable and fixed options based on your risk tolerance and income stability

- Explore alternative documentation programs like bank statement mortgages if traditional qualification is challenging

The combination of the BoC holds at 2.25% in March 2026 and the lowest variable rates for self-employed Toronto buyers under stress test conditions represents a unique convergence of favorable factors. Self-employed professionals who have been waiting for the right time to enter the Toronto housing market should seriously consider whether this opportunity aligns with their financial goals and homeownership timeline.

Remember, successful mortgage qualification as a self-employed borrower requires preparation, proper documentation, and expert guidance. By taking action now and working with specialists who understand the nuances of self-employed mortgage approval, Toronto’s self-employed professionals can turn today’s favorable rate environment into tomorrow’s homeownership success.

References

[1] Bank Of Canada Meeting Recap One Supply Shock After Another – https://www.rbc.com/en/economics/canadian-analysis/data-flashes/bank-of-canada-meeting-recap-one-supply-shock-after-another/

[2] The Full Statement From The Bank Of Canada March 2026 Rate Decision 20260318 – https://investinglive.com/centralbank/the-full-statement-from-the-bank-of-canada-march-2026-rate-decision-20260318/

[3] Bank Of Canada Interest Rate March 2026 – https://stories.td.com/ca/en/article/bank-of-canada-interest-rate-march-2026

[4] Fad Press Release 2026 03 18 – https://www.bankofcanada.ca/2026/03/fad-press-release-2026-03-18/

[6] Bank Of Canada Rate Announcement March 2026 – https://globalnews.ca/news/11735955/bank-of-canada-rate-announcement-march-2026/