March 24, 2026

Self-Employed Toronto Mortgages at March 2026 Rates: Locking 3.94% 5-Year Fixed Before BoC Stability Ends

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The window of opportunity is narrowing. With the Bank of Canada holding its overnight rate at 2.25% as of March 18, 2026, self-employed borrowers in Toronto face a critical decision: lock in competitive 5-year fixed rates around 3.94% or gamble on continued stability. Self-Employed Toronto Mortgages at March 2026 Rates: Locking 3.94% 5-Year Fixed Before BoC Stability Ends represents more than just a mortgage decision—it’s a strategic financial move in an uncertain economic landscape.

For self-employed professionals, contractors, and business owners navigating Toronto’s competitive real estate market, understanding current rate offerings and qualification requirements has never been more crucial. With average detached home prices exceeding $1.4 million in the Greater Toronto Area, even small rate differences translate into tens of thousands of dollars over a mortgage term.

Key Takeaways

✅ 5-year fixed rates for self-employed borrowers range from 2.99% to 3.94%, with several competitive lenders offering rates in the 3.89-3.99% range as of March 2026[1]

✅ The BoC maintained its overnight rate at 2.25% on March 18, 2026, creating a temporary stability window that may not last through mid-2026[8]

✅ Self-employed borrowers must qualify at the stress test rate of 5.25%, making income documentation and debt ratios critical for approval on properties up to $1.5M

✅ Variable rates currently sit below 3.98%, but market consensus suggests potential volatility as economic conditions evolve

✅ Toronto’s competitive lending landscape includes over 340 mortgage brokers and 50+ private lenders, creating opportunities for rate negotiation[2]

Understanding Self-Employed Toronto Mortgages at March 2026 Rates

The mortgage landscape for self-employed borrowers has transformed dramatically over the past 20 months. The Bank of Canada’s aggressive rate cuts—from 5.0% in June 2024 to the current 2.25%—have created unprecedented opportunities for those who can navigate the qualification process[4].

Current Rate Environment for Self-Employed Borrowers

5-year fixed rates represent the sweet spot for most self-employed Toronto homebuyers in March 2026. According to current market data, several lenders offer compelling options:

- Hypotheca and MortgagestoGo: 3.94% across insured, insurable, and uninsured categories ($2,613.86 monthly payment on $500,000 mortgage)[1]

- True North Mortgage: 2.99% (lowest available rate, specific qualification criteria apply)[1]

- Mortio Financial Corp: 3.99% for insured mortgages ($2,627.39 monthly on $500,000)[1]

- City Wide Financial Corp, Mainstreet Credit Union: 3.99% across all insurance categories[1]

These rates compare favorably to shorter terms. 1-year fixed rates average 4.69% for insured mortgages and jump to 5.59% for uninsured products—a significant premium that makes longer terms more attractive[1].

Why the 3.94% Rate Matters for Toronto Properties

Toronto’s real estate market presents unique challenges. With the average detached home price exceeding $1,400,000[2], mortgage amounts are substantially higher than the national average. Consider the impact:

| Mortgage Amount | Monthly Payment @ 3.94% | Monthly Payment @ 4.69% | 5-Year Savings |

|---|---|---|---|

| $500,000 | $2,613.86 | $2,768.45 | $9,275 |

| $1,000,000 | $5,227.72 | $5,536.90 | $18,550 |

| $1,500,000 | $7,841.58 | $8,305.35 | $27,826 |

For self-employed borrowers purchasing properties in Toronto’s competitive neighborhoods—from Leslieville to North York—these savings represent real financial flexibility. The difference between 3.94% and 4.69% on a $1.2 million mortgage exceeds $22,000 over five years.

The Bank of Canada’s Current Stance

The BoC’s March 18, 2026 decision to maintain the overnight rate at 2.25% (keeping prime at 4.45%)[8] signals a pause in the cutting cycle. However, markets are pricing in potential additional cuts through July 2026, though timing remains uncertain[3].

This creates a strategic dilemma: lock in today’s fixed rates or bet on further variable rate declines? For our comprehensive analysis of self-employed mortgage rate trends in 2026, the data suggests caution favors fixed products.

Qualification Requirements for Self-Employed Toronto Mortgages at March 2026 Rates

Securing Self-Employed Toronto Mortgages at March 2026 Rates: Locking 3.94% 5-Year Fixed Before BoC Stability Ends requires meticulous preparation. Unlike traditional employees, self-employed borrowers face enhanced scrutiny of income stability and documentation.

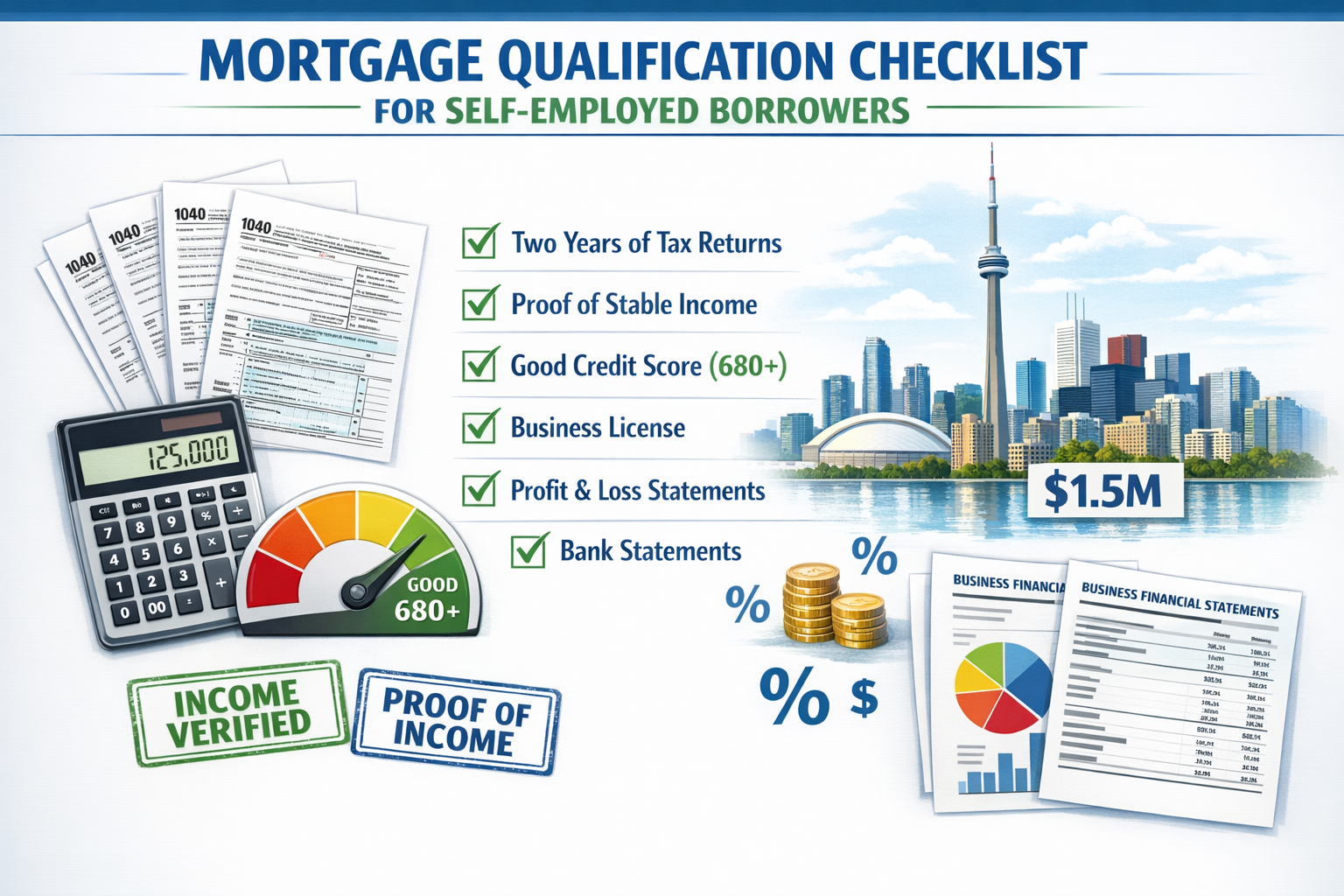

Essential Documentation Checklist

For properties up to $1.5M, self-employed borrowers must provide:

📋 Income Verification

- Two years of complete personal tax returns (T1 Generals with Notice of Assessment)

- Two years of business financial statements (if incorporated)

- Corporate tax returns (T2s) for incorporated businesses

- Year-to-date profit and loss statements

- Business license and articles of incorporation

📋 Credit and Identity

- Credit score of 680+ for optimal rates (higher scores secure better terms)[2]

- Government-issued photo identification

- Proof of down payment source (gift letters if applicable)

📋 Property Documentation

- Purchase agreement or offer

- Property appraisal (arranged by lender)

- Property tax statements

- Condo documents (if applicable)

For detailed guidance on documentation requirements for self-employed mortgage approval in Toronto, proper preparation can accelerate approval timelines by weeks.

Income Calculation Methods

Lenders use different approaches to calculate self-employed income:

Traditional Method (A-Lenders)

- Average net income from two years of tax returns

- Add-backs for depreciation, CCA, and non-recurring expenses

- Typically requires 20% down payment minimum

Stated Income Programs

- Available through alternative lenders

- Higher rates (typically 0.25-0.75% premium)

- Larger down payments (25-35% common)

- Suitable for newer businesses or complex income structures

Bank Statement Programs

- Income verified through 12-24 months of business bank statements

- Gross deposits analyzed (typical multiplier: 50-70% of deposits)

- Ideal for cash-heavy businesses

- Learn more about bank statement mortgages for self-employed borrowers

Credit Score Impact on Rates

Credit scores significantly influence self-employed mortgage rates[2]. Here’s the typical rate structure:

- 740+: Access to best rates (3.94% tier)

- 680-739: Standard rates (typically +0.10-0.25%)

- 620-679: Subprime rates (typically +0.50-1.00%)

- Below 620: Private lender territory (6-12% rates)

Improving your credit score by even 50 points before applying can save thousands annually. For self-employed professionals, maintaining clean business credit alongside personal credit creates the strongest application profile.

GTA Property-Specific Considerations

Toronto’s diverse neighborhoods present varying qualification challenges:

Downtown Core ($800K-$2M condos)

- Higher condo fees impact debt ratios

- Stricter building approval requirements

- Reserve fund scrutiny by lenders

Suburban Detached ($1.2M-$1.8M)

- Property tax considerations

- Appraisal challenges in rapidly appreciating areas

- Larger mortgage amounts require stronger income proof

Luxury Properties ($1.5M+)

- Often require uninsured mortgages (20%+ down)

- More conservative income calculations

- Additional asset verification

For IT consultants and tech professionals, our guide on getting approved as an IT consultant in Toronto addresses industry-specific qualification strategies.

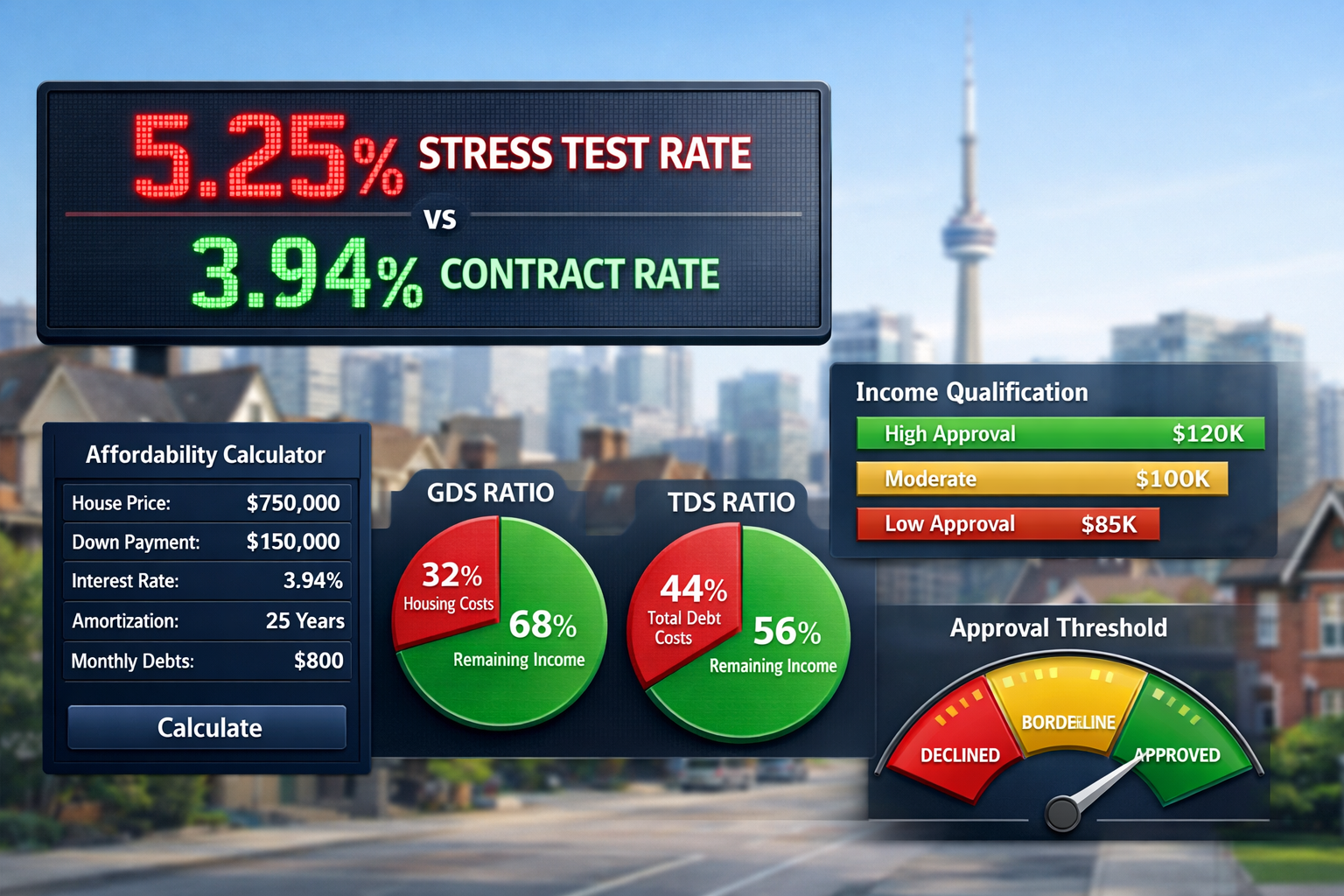

The Stress Test Reality: Qualifying at 5.25% for Self-Employed Toronto Mortgages

The mortgage stress test remains the single biggest hurdle for self-employed borrowers in 2026. Even if you secure a contract rate of 3.94%, you must prove you can afford payments at 5.25%—the greater of the contract rate plus 2% or the Bank of Canada’s qualifying rate.

How the Stress Test Impacts Borrowing Power

The stress test reduces purchasing power by approximately 15-20% compared to qualifying at contract rates. For self-employed Toronto buyers, this translates to:

| Annual Income | Max Purchase @ 3.94% | Max Purchase @ 5.25% | Reduction |

|---|---|---|---|

| $100,000 | $585,000 | $485,000 | $100,000 |

| $150,000 | $877,500 | $727,500 | $150,000 |

| $200,000 | $1,170,000 | $970,000 | $200,000 |

| $250,000 | $1,462,500 | $1,212,500 | $250,000 |

Assumptions: 20% down payment, no other debts, property taxes $4,000/year, heating $1,200/year

For self-employed borrowers with variable income streams, the stress test calculation uses conservative income averaging, making qualification more challenging than for salaried employees.

Debt Service Ratio Requirements

Lenders evaluate two critical ratios:

Gross Debt Service (GDS) Ratio

- Maximum: 39% of gross income

- Includes: mortgage payment, property taxes, heating, 50% of condo fees

- Formula: (Monthly housing costs ÷ Gross monthly income) × 100

Total Debt Service (TDS) Ratio

- Maximum: 44% of gross income

- Includes: all GDS items plus credit cards, car loans, lines of credit, other debts

- Formula: (Total monthly debt obligations ÷ Gross monthly income) × 100

💡 Pro Tip: Pay down consumer debts before applying. Eliminating a $500 monthly car payment can increase borrowing capacity by $80,000-$100,000.

Strategies to Maximize Qualification

1. Income Optimization

- Time your application after strong income years

- Maximize legitimate business expense add-backs

- Consider co-applicants with stable income

2. Debt Reduction

- Pay off high-interest consumer debts

- Reduce credit card limits (unused credit counts against you)

- Consolidate debts strategically

3. Down Payment Enhancement

- Larger down payments reduce stress test impact

- 25% down often unlocks better rate tiers

- Consider gifted down payments (properly documented)

4. Alternative Documentation

- Explore stated income programs for complex situations

- Consider bank statement loan programs for newer businesses

- Work with brokers experienced in self-employed applications

For comprehensive strategies, review our ultimate guide to securing mortgages for self-employed Canadians.

Fixed vs. Variable: Making the Right Choice for Self-Employed Toronto Mortgages

The debate between fixed and variable rates takes on added complexity for Self-Employed Toronto Mortgages at March 2026 Rates: Locking 3.94% 5-Year Fixed Before BoC Stability Ends. With the BoC holding steady but markets anticipating potential cuts, which path offers better value?

Current Variable Rate Landscape

Variable rates currently sit below 3.98%[3], offering immediate savings compared to the 3.94% 5-year fixed benchmark. However, variable rates fluctuate with the Bank of Canada’s policy decisions, creating uncertainty.

Variable Rate Advantages:

- ✅ Lower starting rates (typically 0.10-0.30% below fixed)

- ✅ Potential to benefit from future rate cuts

- ✅ Lower penalties if breaking early (three months interest vs. IRD)

- ✅ Flexibility to convert to fixed rates

Variable Rate Risks:

- ⚠️ Payment uncertainty if rates rise

- ⚠️ Budgeting challenges for self-employed with irregular income

- ⚠️ Potential for trigger rates in some products

- ⚠️ Psychological stress of rate volatility

For self-employed borrowers with variable income streams, the predictability of fixed payments often outweighs the potential savings of variable products. When your business income fluctuates seasonally or project-based, knowing your exact mortgage payment provides crucial financial stability.

Rate Forecast Through 2027

Market analysts project varying scenarios for Canadian mortgage rates:

Consensus View (as of March 2026)

- BoC overnight rate: stable at 2.25% through Q2 2026[8]

- Potential additional cuts: 0.25-0.50% by Q3 2026[3]

- 5-year fixed rates: likely range 3.75-4.25% through 2026[4]

- Variable rates: tracking 0.20-0.40% below fixed rates

Bullish Scenario (Rate Cuts)

- Additional 0.75-1.00% in cuts by end of 2026

- Variable rates could drop to 3.25-3.50%

- Fixed rates compress to 3.50-3.75%

Bearish Scenario (Rate Stability/Increases)

- No further cuts; potential modest increases in 2027

- Variable rates rise to 4.25-4.50%

- Fixed rates climb to 4.50-5.00%

For detailed analysis, see our comparison of fixed vs. variable rates for Toronto buyers in 2026.

Break-Even Analysis

When does variable beat fixed? Consider this scenario:

Assumptions:

- Mortgage amount: $1,000,000

- Fixed rate: 3.94%

- Variable rate: 3.70% (current)

- Term: 5 years

Year 1-2: Variable saves approximately $2,400 annually Break-even point: Variable rate would need to rise above 4.20% and stay there for the remaining term to eliminate savings

However, if rates rise to 4.50% in year 3 and remain elevated, the variable borrower could pay $5,000-$8,000 more over the five-year term.

Recommendation for Self-Employed Borrowers

For most self-employed Toronto buyers in March 2026, locking in 3.94% 5-year fixed rates offers the best risk-adjusted value:

- Income Stability: Fixed payments align with business planning

- Rate Protection: Shields against potential future increases

- Historical Context: 3.94% remains historically attractive

- Stress Reduction: Eliminates rate uncertainty during business fluctuations

- Budget Certainty: Critical for tax planning and business investment decisions

Variable rates suit self-employed borrowers with:

- Exceptionally stable, high income

- Large cash reserves (6+ months payments)

- High risk tolerance

- Flexibility to increase payments if rates rise

- Plans to sell or refinance within 2-3 years

Lender Options and Rate Shopping Strategies

Toronto’s competitive lending landscape offers self-employed borrowers significant advantages. With over 340 mortgage brokers and more than 50 private lenders[2], strategic rate shopping can save thousands.

Lender Categories for Self-Employed Borrowers

Big Six Banks

- Rates: 3.99-4.29% for self-employed

- Pros: Relationship banking, branch access

- Cons: Stricter documentation, slower approvals

- Best for: Established businesses, strong financials

Credit Unions

- Rates: 3.89-4.09% (competitive)

- Pros: Flexible underwriting, local decision-making

- Cons: Regional restrictions, smaller loan limits

- Best for: Community-focused borrowers, unique situations

Monoline Lenders

- Rates: 3.94-3.99% (most competitive)

- Pros: Best rates, mortgage specialists

- Cons: No branch network, mortgage-only relationship

- Best for: Rate-focused borrowers, straightforward applications

Alternative Lenders

- Rates: 4.50-7.00%

- Pros: Flexible income verification, faster approvals

- Cons: Higher rates, additional fees

- Best for: Newer businesses, complex income, bruised credit

Private Lenders

- Rates: 7.00-12.00%

- Pros: Asset-based lending, minimal income verification

- Cons: High rates, short terms (1-2 years)

- Best for: Bridge financing, credit challenges, unique properties

For those exploring alternative options, our guide on mortgages for self-employed borrowers provides comprehensive lender comparisons.

Rate Negotiation Tactics

1. Use Broker Competition

- Obtain quotes from 3-4 brokers

- Leverage competing offers

- Ask about volume discounts and promotions

2. Timing Matters

- Apply mid-week (better lender response times)

- Avoid month-end (lender capacity constraints)

- Consider rate hold periods (90-120 days)

3. Relationship Leverage

- Existing banking relationships can yield 0.10-0.20% discounts

- Consolidating business and personal banking

- High net worth programs for significant assets

4. Down Payment Optimization

- 20% vs. 25% down can unlock better rate tiers

- 35% down often qualifies for premium pricing

- Consider short-term private financing to reach thresholds

Hidden Costs and Fees

Beyond rates, evaluate total borrowing costs:

| Fee Type | Typical Range | Negotiable? |

|---|---|---|

| Appraisal | $300-$500 | Sometimes |

| Application | $0-$500 | Often waived |

| Lender Legal | $0-$1,000 | Varies |

| Broker Fee | $0 (lender-paid) | N/A |

| Discharge Fee | $200-$400 | No |

| Prepayment Penalty | Varies | No |

Rate vs. Features Trade-off: The absolute lowest rate may come with restrictions. Consider:

- Prepayment privileges (10-20% annual lump sum)

- Portability options (if you might move)

- Refinance flexibility

- Penalty calculations (fixed-rate penalties can be substantial)

For self-employed borrowers planning business expansion or property upgrades, flexible prepayment options often provide more value than saving 0.10% on rate.

Action Plan: Securing Your Self-Employed Toronto Mortgage at March 2026 Rates

With Self-Employed Toronto Mortgages at March 2026 Rates: Locking 3.94% 5-Year Fixed Before BoC Stability Ends representing a time-sensitive opportunity, a strategic action plan is essential.

90-Day Pre-Approval Timeline

Days 1-30: Financial Preparation

- ✅ Gather 2 years of tax returns and NOAs

- ✅ Compile business financial statements

- ✅ Pull credit reports and address any issues

- ✅ Calculate maximum affordable purchase price

- ✅ Accumulate down payment and closing costs

- ✅ Reduce consumer debts to improve ratios

Days 31-60: Lender Research and Application

- ✅ Interview 3-4 mortgage brokers specializing in self-employed

- ✅ Compare rate quotes and terms

- ✅ Submit complete application packages

- ✅ Obtain 90-120 day rate holds

- ✅ Complete property search with pre-approval in hand

Days 61-90: Property Purchase and Finalization

- ✅ Make offer with financing condition

- ✅ Arrange property appraisal

- ✅ Finalize mortgage approval

- ✅ Review and sign commitment

- ✅ Coordinate with lawyer for closing

Red Flags to Avoid

🚩 Application Mistakes

- Overstating income (lenders verify everything)

- Hiding debts or liabilities

- Recent credit inquiries (apply for nothing during process)

- Changing jobs or business structure mid-application

🚩 Property Issues

- Overpriced properties (appraisal shortfalls kill deals)

- Condo approval problems (not all buildings qualify)

- Properties requiring immediate major repairs

- Unusual property types (lenders prefer standard residential)

🚩 Timing Errors

- Waiting for “perfect” rates (missing current opportunities)

- Applying without complete documentation

- Underestimating closing timelines

- Failing to secure rate holds early

When to Act

The case for locking in rates now rather than waiting:

✅ Lock In Now If:

- You’ve found your ideal property

- You have complete documentation ready

- Your income and credit qualify at 3.94%

- You value payment certainty

- You’re purchasing within 90-120 days

⏸️ Consider Waiting If:

- You’re 6+ months from purchase

- Your income will significantly improve next tax year

- You’re expecting large business sale or windfall

- Credit repair is underway

- You have strong conviction rates will drop substantially

For most self-employed Toronto buyers, the risk of waiting outweighs potential rewards. Rate holds protect you from increases while allowing you to benefit from decreases within the hold period.

Conclusion

Self-Employed Toronto Mortgages at March 2026 Rates: Locking 3.94% 5-Year Fixed Before BoC Stability Ends represents a compelling opportunity for self-employed professionals, contractors, and business owners navigating one of Canada’s most competitive real estate markets. With the Bank of Canada maintaining its overnight rate at 2.25% and competitive 5-year fixed rates clustering around 3.94%, the current environment favors decisive action over speculation.

The combination of historically attractive rates, temporary BoC stability, and Toronto’s unique property market creates a narrow window for self-employed borrowers to secure favorable financing. While variable rates below 3.98% offer tempting short-term savings, the predictability of fixed payments aligns better with the income variability inherent in self-employment.

Key Success Factors

📊 Documentation Excellence: Complete, accurate financial records remain the foundation of successful self-employed mortgage applications. Two years of tax returns, business statements, and clear income trails separate approvals from rejections.

💰 Strategic Qualification: Understanding the 5.25% stress test and optimizing debt ratios before applying maximizes borrowing power. For Toronto properties averaging $1.4 million, even small qualification improvements translate to substantial purchasing power increases.

🎯 Lender Selection: Toronto’s competitive landscape—with 340+ brokers and 50+ private lenders—rewards strategic shopping. The difference between 3.94% and 4.29% on a $1 million mortgage exceeds $18,000 over five years.

⏰ Timing Discipline: With markets pricing in potential rate volatility through mid-2026, securing rate holds now protects against increases while preserving flexibility for decreases.

Next Steps

Immediate Actions (This Week):

- Pull your credit reports and review for accuracy

- Gather two years of complete tax returns and business financials

- Calculate your maximum qualification using the 5.25% stress test

- Contact specialized mortgage brokers for self-employed borrowers

- Obtain rate quotes and 90-120 day rate holds

Short-Term Actions (Next 30 Days):

- Address any credit issues or outstanding debts

- Submit complete mortgage pre-approval applications

- Secure pre-approval with rate hold

- Begin serious property search with clear budget

- Review our comprehensive guide on how self-employed borrowers in Toronto can secure insurable mortgage rates

Long-Term Strategy:

- Maintain clean business and personal credit

- Document income consistently and conservatively

- Build relationships with mortgage professionals

- Monitor rate trends and BoC policy decisions

- Plan business structure to optimize mortgage qualification

The opportunity to lock in Self-Employed Toronto Mortgages at March 2026 rates of 3.94% for 5-year fixed terms won’t last indefinitely. As BoC stability potentially ends and market conditions evolve, self-employed borrowers who act decisively with proper preparation will secure the most favorable financing for their Toronto property purchases.

Whether you’re a tech consultant in Liberty Village, a contractor in Etobicoke, or a business owner eyeing North York, the combination of competitive rates, strategic preparation, and expert guidance can transform mortgage approval from obstacle to opportunity. The time to act is now—before rate stability ends and opportunities narrow.

References

[1] Self Employed – https://rates.ca/guides/mortgage/self-employed

[2] Toronto Ontario – https://myperch.io/mortgage-rates-canada/toronto-ontario/

[3] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[4] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast

[8] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/