February 4, 2026

DSCR Loans for Self-Employed Real Estate Investors: Top Rates and Strategies for 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

For self-employed real estate investors, traditional mortgage qualification can feel like navigating a maze blindfolded. Tax write-offs that benefit your business often work against you when lenders scrutinize your personal income statements. But what if you could qualify for investment property financing based solely on the property’s rental income—without ever showing a W-2 or personal tax return? That’s the revolutionary advantage of Debt Service Coverage Ratio (DSCR) loans, and in 2026, they’re becoming the go-to financing solution for savvy self-employed investors looking to scale their portfolios quickly.

DSCR Loans for Self-Employed Real Estate Investors: Top Rates and Strategies for 2026 represent a fundamental shift in how investment property financing works. Unlike conventional mortgages that demand extensive personal income documentation, DSCR loans approve based on one simple metric: whether the property’s rental income can cover its mortgage payment. With current rates stabilizing in the competitive 5.99% to 6.50% range and lenders expanding their programs throughout 2026, now is the perfect time to understand how these loans can accelerate your investment strategy[3].

Key Takeaways

✅ No Income Verification Required: DSCR loans qualify based entirely on rental income, eliminating the need for W-2s, tax returns, or personal income documentation—perfect for self-employed borrowers with complex tax situations[2]

✅ Competitive 2026 Rates: Current DSCR loan rates range from 5.99% to 6.50%, with the best rates available in the Midwest (5.75%-6.25%) and for single-family rentals averaging 6.25%[3][4]

✅ Faster Approval Timeline: DSCR loans typically close in 2-3 weeks compared to conventional mortgages at 4-6 weeks, enabling quick portfolio expansion[2]

✅ Flexible Qualification: Minimum DSCR ratios start at 0.80-1.0 with compensating factors, while ratios of 1.25+ unlock the best rates and terms[1][2]

✅ Scalable Portfolio Growth: Loan amounts up to $5,000,000+ determined by rental income potential rather than personal income limits, allowing rapid scaling for experienced investors[2]

Understanding DSCR Loans for Self-Employed Real Estate Investors in 2026

What Makes DSCR Loans Different?

The Debt Service Coverage Ratio (DSCR) is a simple but powerful calculation that determines whether a rental property generates enough income to cover its mortgage payment. The formula is straightforward:

DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment

A DSCR of 1.0 means the property breaks even—rental income exactly covers the payment. A DSCR of 1.25 means the property generates 25% more income than needed to cover the mortgage, providing a healthy cash flow cushion[8].

For self-employed investors, this calculation method is revolutionary. Traditional lenders want to see your personal income through W-2s, tax returns, and employment verification. But self-employed professionals often write off legitimate business expenses that reduce their taxable income—making them appear less qualified on paper than they actually are. Working with a specialized self-employed mortgage broker can help navigate these challenges, but DSCR loans eliminate the problem entirely[10].

Why Self-Employed Investors Love DSCR Loans

No Personal Debt-to-Income Ratio Consideration: Conventional mortgages calculate your debt-to-income (DTI) ratio by comparing all your monthly debt payments to your gross monthly income. For self-employed investors with multiple properties, business loans, or variable income, this can be a dealbreaker. DSCR loans ignore your personal DTI entirely, focusing only on the property’s ability to pay for itself[1].

Streamlined Documentation: Instead of providing two years of tax returns, profit-and-loss statements, bank statements, and employment verification letters, DSCR loans require minimal documentation. Most lenders need only a lease agreement or rental appraisal to establish income potential, along with basic credit and asset verification[2].

Portfolio Expansion Velocity: Because DSCR loans don’t count against your personal income limits, you can acquire multiple properties much faster than with conventional financing. Each property stands on its own merits, allowing experienced investors to scale their portfolios without hitting personal income ceiling constraints[10].

Top DSCR Loan Rates and Terms for 2026

Current Rate Environment

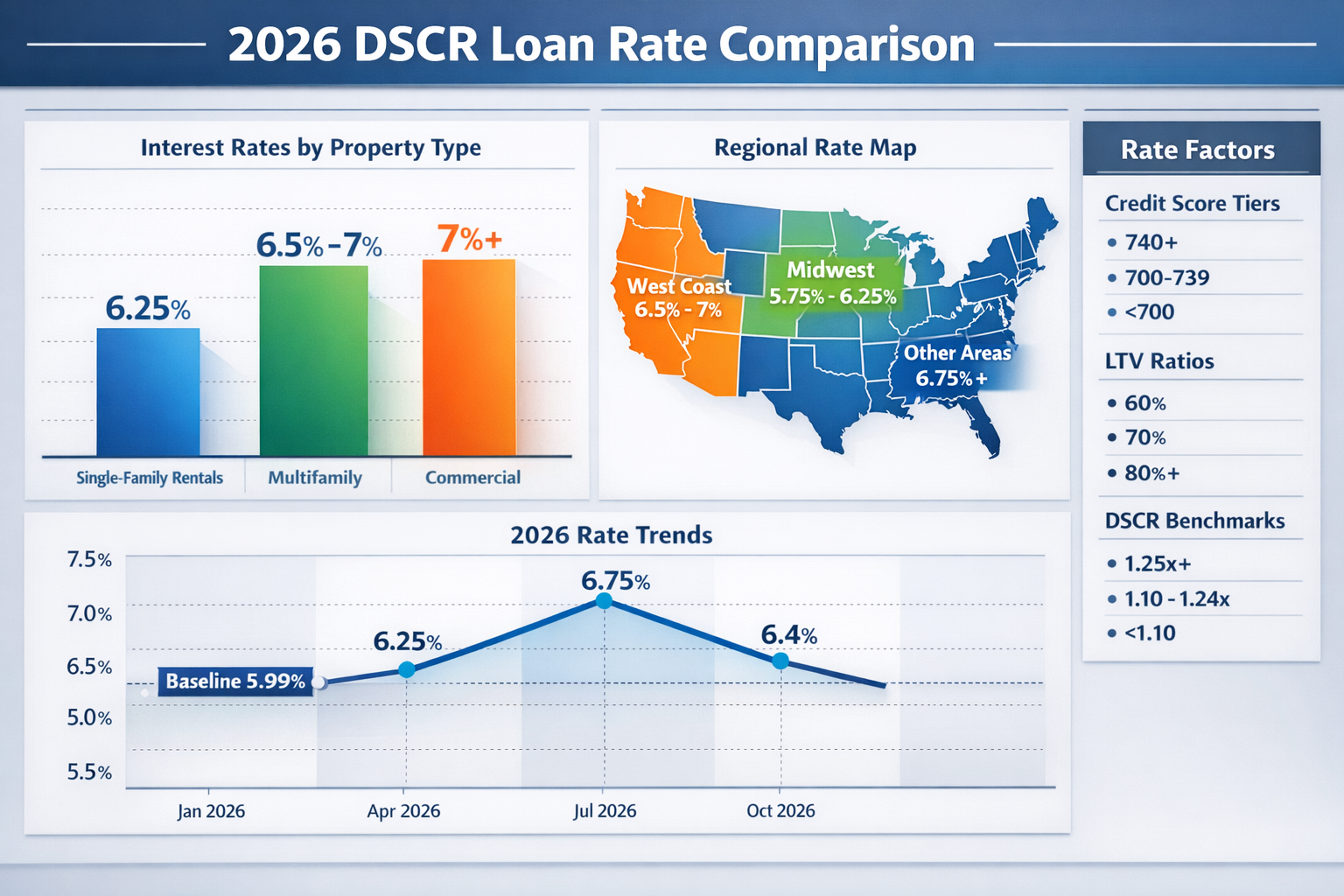

As of 2026, DSCR loan interest rates have stabilized in a competitive range that makes investment property acquisition attractive for self-employed professionals. Current baseline rates range from 5.99% to 6.50% depending on loan structure, property type, and borrower qualifications[3].

For context, conventional mortgage rates in 2026 hover in the 5% range, meaning DSCR loans typically carry a premium of approximately 1-1.5 percentage points. This premium reflects the higher risk profile associated with investment properties and the reduced documentation requirements—but for many self-employed investors, the trade-off is well worth it[4].

Rate Breakdown by Property Type

| Property Type | Average DSCR Rate Range | Typical LTV |

|---|---|---|

| Single-Family Rentals | 6.25% | 75-80% |

| Multifamily (2-4 units) | 6.5%-7% | 75-80% |

| Commercial Properties | 7%+ | 70-75% |

| Portfolio Refinances | 6.25%-6.75% | 70-75% |

Single-family rental properties command the most favorable rates, averaging around 6.25% in 2026. These properties are viewed as lower risk due to their broad market appeal and easier resale potential[4].

Multifamily properties (2-4 units) typically see rates in the 6.5% to 7% range. While they generate higher rental income, lenders perceive slightly elevated risk due to vacancy concerns and management complexity[4].

Commercial properties and larger multifamily buildings generally start at 7% and higher, reflecting their specialized nature and smaller buyer pool[4].

Regional Rate Variations

Geography plays a significant role in DSCR loan pricing for 2026. The Midwest offers the most competitive rates at 5.75%-6.25%, driven by stable rental markets, affordable property prices, and consistent demand[4].

West Coast properties command premium rates of 6.5%-7%, particularly in high-demand metropolitan areas like Los Angeles, San Francisco, and Seattle. These higher rates reflect elevated property values, market volatility, and increased lender risk exposure[4].

Southern and Eastern markets typically fall in the middle range, with rates varying based on local economic conditions, rental demand, and property appreciation trends.

Factors That Influence Your Rate

Several key factors determine where your specific rate falls within the range:

Credit Score Impact: Most DSCR programs require a minimum credit score of 640-680, with 660-700 being standard. However, rates improve significantly with scores above 700. A borrower with a 740+ credit score might secure rates 0.5-0.75 percentage points lower than someone with a 660 score[1][2].

DSCR Ratio: Your property’s DSCR directly impacts your rate. Properties with DSCR ratios of 1.25 or higher qualify for the best available rates. Ratios between 1.04-1.25 receive standard competitive pricing. Properties below 1.0 DSCR may still qualify with compensating factors but will face significantly higher rates and stricter terms[1][2].

Loan-to-Value (LTV) Ratio: Lower LTV ratios (larger down payments) result in better rates. Standard programs require 20-25% down (75-80% LTV), but experienced investors with strong credit and high DSCR properties may access programs up to 90% LTV—though at premium rates[1][2].

Property Condition and Location: Well-maintained properties in strong rental markets receive preferential pricing. Properties requiring significant repairs or located in declining markets face rate premiums or may not qualify at all.

Strategic Qualification Requirements for DSCR Loans in 2026

Credit Score Benchmarks

While DSCR loans are more flexible than conventional mortgages, credit score requirements remain important. Most lenders in 2026 set minimum scores at 640-680, with the majority of competitive programs requiring 660-700[1][2].

Here’s how credit scores typically impact your options:

- 740+ Credit: Access to best rates, highest LTV options, lowest DSCR requirements

- 700-739 Credit: Competitive rates, standard terms, wide lender selection

- 660-699 Credit: Standard approval, slightly elevated rates, more documentation

- 640-659 Credit: Limited lender options, higher rates, stricter DSCR requirements

- Below 640: May require alternative financing or private lenders

For self-employed investors working to optimize their credit profiles, focusing on payment history, credit utilization, and account age delivers the best results.

Down Payment and LTV Requirements

Standard DSCR loan programs require 20-25% down for purchases, translating to 75-80% loan-to-value ratios. This requirement is consistent across most lenders and property types[1][2].

Some specialized programs offer higher leverage:

- Experienced investors (typically 5+ financed properties) may access 85-90% LTV programs

- High DSCR properties (1.5+) sometimes qualify for reduced down payment requirements

- Portfolio refinances typically cap at 70-75% LTV to preserve equity cushion

Cash-out refinances generally require more conservative LTV ratios, often maxing out at 70-75% to ensure adequate equity protection for the lender.

DSCR Ratio Requirements and Examples

Understanding DSCR thresholds is critical for self-employed investors evaluating potential properties. Here’s how the ratio spectrum works in 2026:

DSCR 1.25+ (Ideal): This is the sweet spot for best rates and easiest approval.

Example: A property generating $3,000 monthly rent with a $2,400 monthly payment (including principal, interest, taxes, insurance, and HOA fees) yields a DSCR of 1.25 ($3,000 ÷ $2,400 = 1.25)[2].

This property qualifies for the best available rates and terms, demonstrating strong cash flow that provides a safety margin for vacancies and repairs.

DSCR 1.04-1.24 (Standard): Most properties fall in this range, qualifying for competitive rates with standard terms.

Example: $2,500 monthly rent against a $2,200 monthly payment produces a DSCR of 1.14 ($2,500 ÷ $2,200 = 1.14).

This property qualifies readily but won’t access the absolute lowest rates reserved for higher DSCR properties.

DSCR 0.80-1.03 (Compensating Factors Required): Properties in this range may still qualify, but lenders require compensating factors such as:

- Higher credit scores (720+)

- Larger down payments (30%+)

- Significant liquid reserves (12+ months)

- Strong property appreciation potential

- Experienced investor profile

Example: $2,100 monthly rent against a $2,400 monthly payment creates a DSCR of 0.88 ($2,100 ÷ $2,400 = 0.88)[2].

This property operates at a cash flow deficit, requiring the investor to contribute personal funds monthly. Approval requires demonstrating ability to sustain this negative cash flow through other income sources or reserves.

Reserve Requirements

Most DSCR lenders require 6-12 months of mortgage payment reserves per property. These reserves must be liquid assets (cash, savings, investment accounts) that demonstrate your ability to cover payments during vacancies or unexpected repairs[1].

For self-employed investors building portfolios, this requirement means maintaining substantial liquidity. A portfolio of five properties might require $60,000-$120,000 in demonstrable reserves, depending on payment amounts.

Strategies for Self-Employed Investors to Maximize DSCR Loan Benefits

Strategy 1: Optimize Property Selection for DSCR Performance

Not all investment properties are created equal for DSCR qualification. Self-employed investors should prioritize properties that naturally generate strong DSCR ratios:

Target Below-Market Purchase Prices: Properties purchased below market value allow for lower loan amounts relative to rental income, automatically improving DSCR ratios. Foreclosures, estate sales, and off-market deals often provide this advantage.

Focus on High-Rent Markets: Markets with strong rental demand and above-average rent-to-price ratios deliver better DSCR performance. Research markets where monthly rent exceeds 1% of purchase price for optimal cash flow.

Consider House Hacking Potential: Properties with additional income potential (basement suites, ADUs, room rentals) can significantly boost rental income calculations, improving DSCR ratios and qualification terms.

Strategy 2: Leverage Multiple DSCR Loans for Portfolio Scaling

One of the most powerful advantages for self-employed investors is the ability to acquire multiple DSCR loans simultaneously. Unlike conventional mortgages that count against your personal income limits, each DSCR loan stands independently[10].

This enables aggressive portfolio expansion strategies:

Simultaneous Acquisitions: Experienced investors can close on multiple properties within weeks, limited only by available capital for down payments and reserves rather than personal income constraints.

Geographic Diversification: Build portfolios across multiple markets to reduce concentration risk, taking advantage of regional rate variations and market cycles.

Property Type Diversification: Mix single-family rentals, small multifamily, and commercial properties to balance cash flow, appreciation potential, and risk profiles.

For self-employed professionals with access to capital, this strategy can accelerate wealth building far faster than conventional financing allows. Understanding mortgage market trends can help time these acquisitions effectively.

Strategy 3: Optimize Your Business Structure

Self-employed investors should carefully consider their business entity structure when acquiring DSCR loans:

LLC Ownership: Many DSCR lenders allow properties to be held in Limited Liability Companies, providing legal protection while maintaining financing eligibility. Some lenders require personal guarantees even for LLC-held properties.

Business Credit Building: While DSCR loans don’t require personal income verification, maintaining strong business credit can open additional financing options and strengthen your overall investor profile.

Tax Strategy Coordination: Work with a CPA to balance tax write-offs with financing goals. While DSCR loans don’t require tax returns, maintaining clean financial records supports your broader investment strategy.

Strategy 4: Time Your Acquisitions with Rate Cycles

Interest rate environments fluctuate, and strategic investors time their acquisitions accordingly. In 2026, with rates stabilized in the 5.99%-6.50% range, conditions favor action[3].

Monitor these indicators:

Central Bank Policy: Track Bank of Canada rate decisions and economic indicators that signal rate direction.

Lender Competition: Increased competition among DSCR lenders often leads to rate compression and more favorable terms. 2026 has seen expanding lender participation in this space.

Seasonal Patterns: Real estate markets often see reduced competition in winter months, potentially offering better purchase prices that improve DSCR ratios.

Strategy 5: Build Relationships with Specialized Lenders

Not all lenders offer DSCR programs, and those that do vary significantly in their terms, rates, and flexibility. Self-employed investors benefit from developing relationships with multiple specialized lenders:

Portfolio Lenders: These institutions hold loans on their own books rather than selling them, allowing more flexibility in underwriting and terms.

Non-QM Specialists: Lenders specializing in non-qualified mortgages often have the most competitive DSCR programs and understand self-employed investor needs.

Mortgage Brokers: Working with brokers who specialize in self-employed mortgages provides access to multiple lenders and programs, ensuring you secure optimal terms.

Common Pitfalls to Avoid with DSCR Loans

Pitfall 1: Underestimating Total Monthly Payments

Many investors calculate DSCR using only principal and interest, forgetting that lenders include property taxes, insurance, HOA fees, and sometimes maintenance reserves in the monthly payment calculation[8].

A property with $2,000 in principal and interest might have an additional $600 in taxes, $150 in insurance, and $100 in HOA fees—bringing the total payment to $2,850. Always calculate DSCR using the complete PITIA (Principal, Interest, Taxes, Insurance, Association fees) figure.

Pitfall 2: Overestimating Rental Income

Lenders typically use actual lease agreements for occupied properties or appraisal-based rental estimates for vacant properties. Optimistic rental projections won’t help your qualification[2].

Conservative rental income estimates protect both you and the lender. Factor in realistic vacancy rates (typically 5-10% annually) and market-rate rents, not aspirational pricing.

Pitfall 3: Ignoring Reserve Requirements

Self-employed investors sometimes focus entirely on down payment requirements while overlooking reserve requirements. Qualifying for multiple DSCR loans simultaneously requires substantial liquid reserves—often $50,000-$100,000+ depending on portfolio size[1].

Plan your capital allocation carefully, ensuring sufficient reserves remain after down payments and closing costs.

Pitfall 4: Choosing Properties Based Only on DSCR

While DSCR qualification is important, it shouldn’t be your only investment criterion. Properties with excellent DSCR ratios in declining markets or poor condition can still be terrible investments.

Evaluate properties holistically:

- Appreciation potential and market trends

- Property condition and deferred maintenance

- Neighborhood quality and crime statistics

- Local economic drivers and employment stability

- Exit strategy and resale potential

Pitfall 5: Failing to Compare Multiple Lenders

DSCR loan terms vary significantly across lenders. Rate differences of 0.25-0.75 percentage points are common, translating to thousands of dollars over the loan term.

Obtain quotes from at least 3-5 specialized lenders before committing. Compare not just rates, but also:

- Origination fees and closing costs

- Prepayment penalties

- Minimum DSCR requirements

- Maximum loan amounts

- Reserve requirements

- Closing timelines

Advanced DSCR Loan Strategies for Experienced Self-Employed Investors

Cash-Out Refinancing for Portfolio Expansion

Once you’ve built equity in existing rental properties, cash-out refinancing using DSCR loans can fund additional acquisitions without selling properties or accessing personal income-based financing.

Typical cash-out DSCR refinances allow up to 70-75% LTV, meaning a property worth $400,000 could support a loan of $280,000-$300,000. If your existing mortgage is $200,000, you could extract $80,000-$100,000 in cash for new down payments[2].

This strategy creates a compounding effect: each property’s appreciation funds the next acquisition, accelerating portfolio growth without requiring additional personal capital.

The DSCR SOFR ARM Strategy

Some lenders offer SOFR ARM (Adjustable Rate Mortgage) DSCR loans with initial rates 0.25-0.50 percentage points below fixed-rate options. These loans adjust every 6 months based on the Secured Overnight Financing Rate[5].

For investors planning shorter hold periods (3-5 years) or anticipating rate decreases, SOFR ARM products can reduce carrying costs and improve cash flow. However, they introduce interest rate risk that must be carefully evaluated against your investment timeline and risk tolerance.

The 1031 Exchange Integration

Self-employed investors using 1031 exchanges to defer capital gains taxes can leverage DSCR loans for replacement properties. The streamlined documentation and fast closing timelines (2-3 weeks) make DSCR loans ideal for meeting 1031 exchange deadlines[2].

Coordinate with a qualified intermediary and DSCR lender early in the exchange process to ensure smooth execution within the required 45-day identification and 180-day closing windows.

Portfolio Loan Consolidation

Some DSCR lenders offer portfolio loan programs that consolidate multiple properties under a single loan. This strategy can:

- Simplify management with one payment instead of multiple

- Potentially improve overall terms through volume discounts

- Create cross-collateralization that may unlock higher LTV ratios

- Streamline refinancing as portfolio values increase

However, cross-collateralization also means one property’s issues can affect your entire portfolio, so carefully evaluate the trade-offs with your financial advisor.

The Future of DSCR Loans: What Self-Employed Investors Should Watch in 2026

Expanding Lender Participation

The DSCR loan market has seen significant growth in recent years, with more lenders entering the space in 2026. This increased competition is driving:

Rate Compression: More lenders competing for business has narrowed the spread between DSCR and conventional rates from 2+ percentage points historically to the current 1-1.5 point range[3][4].

Product Innovation: Lenders are introducing new features like higher LTV options, lower minimum DSCR requirements, and flexible reserve structures to differentiate their offerings.

Technology Integration: Digital platforms are streamlining the DSCR application and approval process, with some lenders offering preliminary approvals within 24-48 hours.

Regulatory Considerations

While DSCR loans fall outside traditional qualified mortgage (QM) regulations, self-employed investors should monitor potential regulatory changes that could affect program availability or terms.

Currently, the regulatory environment remains favorable for non-QM products like DSCR loans, but staying informed about policy discussions helps investors anticipate and adapt to potential changes.

Market Cycle Positioning

Understanding where we are in the real estate market cycle helps self-employed investors make strategic decisions about DSCR loan utilization:

Current Environment (2026): Stabilized interest rates, moderating home prices in many markets, and strong rental demand create favorable conditions for cash-flowing investment properties.

Forward Outlook: Monitor economic indicators, employment trends, and inflation data that signal potential rate movements or market shifts.

Successful investors use favorable DSCR loan terms to acquire quality properties during optimal market conditions, positioning their portfolios for long-term appreciation and cash flow.

Practical Steps to Secure Your First DSCR Loan

Step 1: Assess Your Qualification Profile

Before property shopping, evaluate your qualification strength:

✅ Credit Score: Pull your credit reports and ensure scores meet minimum thresholds (660+ preferred)

✅ Available Capital: Calculate total funds available for down payment (20-25%), closing costs (2-4%), and reserves (6-12 months payments)

✅ Property Target: Identify markets and property types that align with your budget and DSCR requirements

✅ Entity Structure: Determine whether you’ll purchase personally or through an LLC

Step 2: Connect with Specialized Lenders

Research and contact 3-5 lenders offering DSCR programs. Ask specific questions:

- What are your current DSCR loan rates for my credit profile?

- What minimum DSCR ratio do you require?

- What documentation do you need for pre-qualification?

- What are your reserve requirements?

- What is your typical closing timeline?

- Do you allow LLC ownership?

- What are your total closing costs and fees?

Step 3: Get Pre-Qualified

Obtain pre-qualification letters from your top lender choices. This process typically requires:

- Credit authorization

- Basic asset verification (bank statements)

- Property type and location preferences

- Estimated purchase price or loan amount

Pre-qualification demonstrates seriousness to sellers and helps you move quickly when you find the right property.

Step 4: Analyze Properties Using DSCR Metrics

As you evaluate potential investments, calculate DSCR for each property:

- Determine monthly rental income (use comparable rentals or existing leases)

- Calculate total monthly payment (use online calculators or lender estimates including PITIA)

- Divide rental income by payment to get DSCR ratio

- Target properties with 1.25+ DSCR for best terms

This analysis should happen before making offers, ensuring you pursue only properties that will qualify for favorable DSCR loan terms.

Step 5: Submit Full Application

Once under contract, submit your complete DSCR loan application with:

- Purchase contract

- Property appraisal (ordered by lender)

- Lease agreement (if property is occupied) or rental market analysis

- Asset documentation (bank statements, investment accounts)

- Credit authorization

- Property insurance quote

- Entity documentation (if using LLC)

Step 6: Close and Scale

DSCR loans typically close in 2-3 weeks, significantly faster than conventional mortgages[2]. Use this speed advantage to:

- Negotiate shorter closing periods that strengthen your offers

- Acquire multiple properties in quick succession

- Capitalize on time-sensitive opportunities

- Build momentum in your portfolio expansion

After closing your first DSCR loan, apply the lessons learned to streamline subsequent acquisitions, refining your process with each transaction.

Conclusion: Leveraging DSCR Loans for Self-Employed Investment Success in 2026

DSCR Loans for Self-Employed Real Estate Investors: Top Rates and Strategies for 2026 represent a powerful financing tool that eliminates traditional barriers faced by self-employed professionals. By qualifying based on rental income rather than personal income documentation, these loans enable faster portfolio scaling, simplified approval processes, and strategic flexibility that conventional mortgages simply cannot match.

With current rates ranging from 5.99% to 6.50% and competitive terms available across property types and markets, 2026 presents an opportune environment for self-employed investors to leverage DSCR financing[3]. The key is approaching these loans strategically: understanding qualification requirements, optimizing property selection for strong DSCR ratios, building relationships with specialized lenders, and integrating DSCR loans into your broader investment strategy.

Your Next Steps

Ready to explore DSCR loans for your investment portfolio? Take these actions today:

🏠 Calculate Your Capacity: Review your credit, available capital, and target markets to determine how many properties you could acquire using DSCR financing

📊 Analyze Potential Properties: Use DSCR calculations to evaluate current listings in your target markets, identifying opportunities with 1.25+ ratios

🤝 Connect with Specialists: Reach out to experienced mortgage professionals who understand self-employed investor needs and can access competitive DSCR programs

📈 Build Your Strategy: Develop a 12-24 month acquisition plan that leverages DSCR loans to systematically grow your portfolio

💡 Continue Learning: Stay informed about market conditions, rate trends, and evolving DSCR programs to optimize your timing and terms

The combination of self-employment income flexibility and DSCR loan qualification creates unprecedented opportunities for real estate investors in 2026. By mastering these financing tools and applying strategic acquisition principles, self-employed professionals can build substantial rental portfolios that generate passive income, build equity, and create long-term wealth—all without the documentation headaches that traditional mortgages impose.

Start your DSCR loan journey today and unlock the full potential of your real estate investment ambitions. 🚀

References

[1] A Guide To Dscr Loans For Real Estate Investors – https://lendingone.com/insight/a-guide-to-dscr-loans-for-real-estate-investors/

[2] Dscr Loans – https://nationalmortgagecenter.com/dscr-loans

[3] Dscr Loan Interest Rates – https://homeabroadinc.com/mortgages/dscr-loan-interest-rates/

[4] Dscr Loan Interest Rates – https://trussfinancialgroup.com/blog/dscr-loan-interest-rates

[5] 6 Month Sofr Arm Dscr Loans For Real Estate Investors – https://griffinfunding.com/non-qm-mortgages/6-month-sofr-arm-dscr-loans-for-real-estate-investors/

[8] Dscr Calculator – https://newfi.com/calculators/dscr-calculator/

[10] Dscr Loans Self Employed – https://expresscapitalfinancing.com/blog/dscr-loans-self-employed/