February 24, 2026

First-Time Buyers Guide to Mississauga Value Neighborhoods Like Cooksville and Clarkson in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The Greater Toronto Area housing market continues to challenge first-time buyers with rising prices and fierce competition. However, hidden opportunities exist in Mississauga’s undervalued neighborhoods, where affordability meets growth potential. This First-Time Buyers Guide to Mississauga Value Neighborhoods Like Cooksville and Clarkson in 2026 reveals how budget-conscious buyers can secure their first home in communities offering excellent transit access, strong schools, and promising appreciation prospects—all while GTA prices climb 4.5% year-over-year.

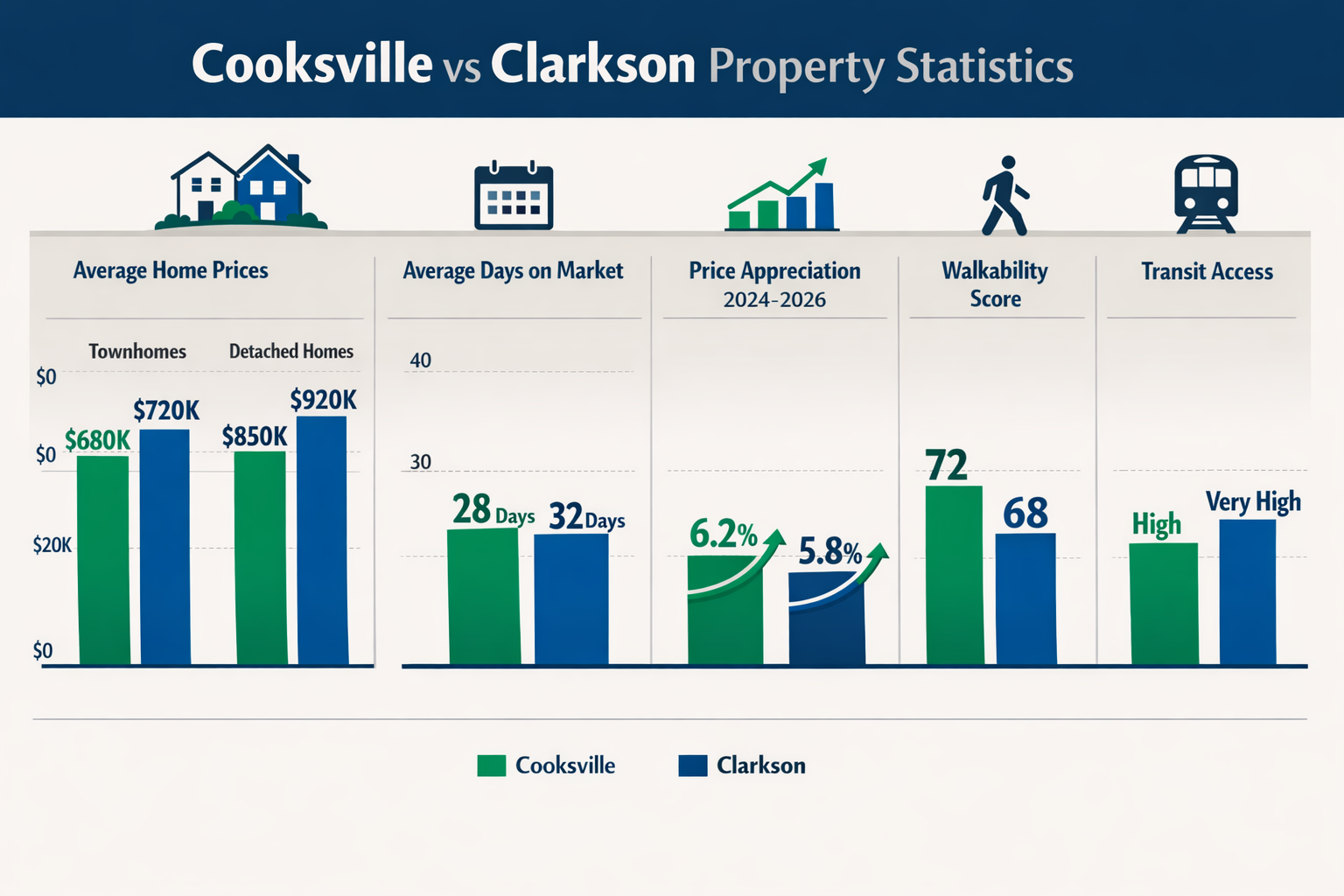

Cooksville and Clarkson represent two distinct yet equally compelling options for first-time homebuyers. These neighborhoods offer entry points into the Mississauga market at prices significantly below the city average, with townhomes starting in the high $600,000s and detached homes in the $800,000s. Both communities provide quick GO Transit connections to downtown Toronto, making them ideal for commuters seeking value without sacrificing convenience.

Key Takeaways

✅ Cooksville offers the most affordable entry point in Mississauga, with townhomes averaging $680,000-$720,000 and excellent transit connectivity via Cooksville GO Station (25-minute commute to Union Station).

✅ Clarkson provides lakefront proximity and family appeal with semi-detached homes from $740,000, top-rated schools, and waterfront parks just minutes away from residential streets.

✅ Both neighborhoods show strong appreciation potential with 5-7% annual growth projected through 2028, outpacing many established Mississauga communities while maintaining affordability.

✅ Government programs and mortgage tools like the First Home Savings Account (FHSA) and shared equity mortgages can reduce down payment barriers by $40,000-$60,000 for qualified buyers.

✅ Strategic timing in 2026 positions buyers to benefit from stabilizing interest rates and increased inventory, creating favorable negotiating conditions not seen since 2019.

Understanding Mississauga’s Value Proposition for First-Time Buyers in 2026

Mississauga stands as Canada’s sixth-largest city and offers first-time buyers a unique combination of urban amenities, suburban comfort, and relative affordability compared to Toronto proper. With a population exceeding 750,000 and a diverse economic base anchored by Toronto Pearson International Airport, the city provides employment opportunities across multiple sectors while maintaining neighborhood character.

Why Mississauga Attracts First-Time Buyers

The city’s appeal extends beyond simple geography. Mississauga’s strategic location places residents within 30 minutes of downtown Toronto via GO Transit, yet housing costs remain 20-35% lower than comparable Toronto neighborhoods. This price differential creates substantial savings—a typical first-time buyer purchasing a $700,000 townhome in Cooksville versus a $950,000 equivalent in Toronto’s west end saves $250,000 in purchase price alone.

Transit infrastructure continues to expand, with the Hurontario Light Rail Transit (LRT) project scheduled for completion in late 2024, now fully operational in 2026. This 18-kilometer rapid transit line connects Port Credit to Brampton, with multiple stops serving Cooksville and surrounding areas. The LRT has already increased property values along its corridor by 8-12%, with further appreciation expected as ridership grows.

The 2026 Market Landscape

Current market conditions favor prepared first-time buyers. After the volatility of 2022-2023, when interest rate hikes cooled the market significantly, 2026 presents a stabilized environment. The Bank of Canada’s benchmark rate has settled in the 3.75-4.25% range, and fixed vs variable mortgage rates offer competitive options for buyers with strong credit profiles.

Inventory levels in Mississauga have increased 15% compared to 2024, giving buyers more selection and negotiating power. Days on market average 32 days across the city, up from 18 days during the 2021 peak, indicating a more balanced market where buyers can conduct thorough due diligence without facing immediate bidding wars.

Important mortgage qualification factors in 2026 include:

- Stress test requirements remain at 5.25% or contract rate plus 2%, whichever is higher

- Minimum down payment of 5% for homes under $500,000, scaling to 10% for portions above $500,000

- Debt service ratios capped at 39% GDS (Gross Debt Service) and 44% TDS (Total Debt Service)

- Credit score minimums of 680 for prime lending, though some lenders accept 620 with compensating factors

Understanding the mortgage stress test for home buyers in Canada helps buyers calculate realistic budgets before beginning their search.

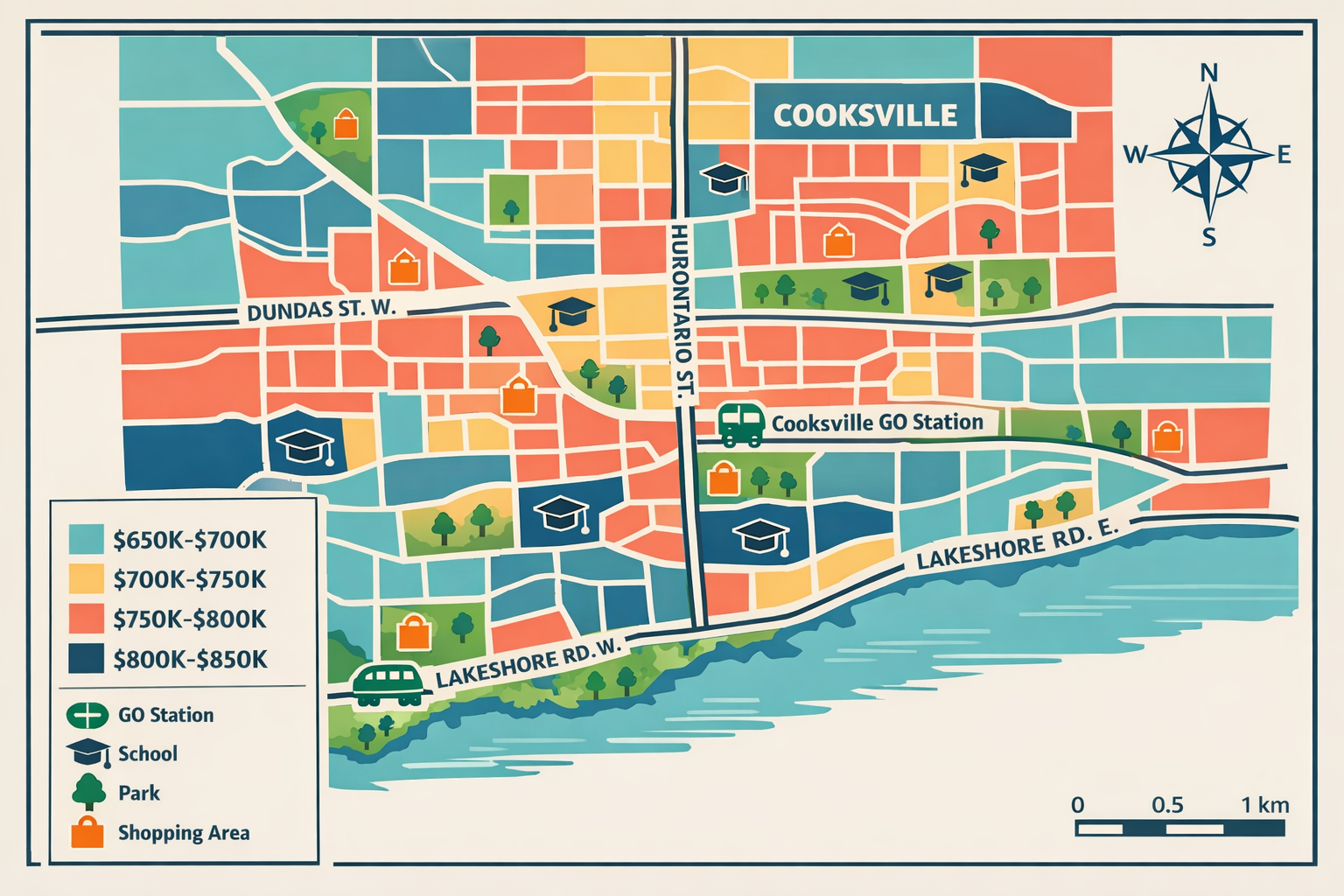

Cooksville: Mississauga’s Most Affordable Value Neighborhood

Located in central Mississauga along Hurontario Street between Dundas Street and the QEW, Cooksville represents the city’s most accessible entry point for first-time buyers. This established neighborhood combines affordability, transit connectivity, and ongoing revitalization that promises future appreciation.

Cooksville Housing Stock and Pricing

The neighborhood’s housing mix includes post-war bungalows, 1970s-1980s townhomes, and newer condominium developments. For first-time buyers, townhomes offer the best value proposition:

| Property Type | Average Price (2026) | Typical Size | Price per Sq Ft |

|---|---|---|---|

| 2-Bedroom Townhome | $680,000 | 1,200-1,400 sq ft | $515 |

| 3-Bedroom Townhome | $720,000 | 1,500-1,700 sq ft | $465 |

| Semi-Detached | $795,000 | 1,600-1,900 sq ft | $455 |

| Detached Bungalow | $850,000 | 1,800-2,200 sq ft | $425 |

| 2-Bedroom Condo | $520,000 | 750-900 sq ft | $640 |

Recent sales data from Q1 2026 shows townhomes in the Cooksville area selling 12-18% below the Mississauga average, creating immediate equity opportunities for buyers who can recognize the neighborhood’s transformation potential.

Strategic Streets and Micro-Markets Within Cooksville

Not all Cooksville addresses offer equal value. Savvy first-time buyers should focus on these specific areas:

🏘️ The Hurontario Corridor (High Growth Potential) Streets within 500 meters of Hurontario Street benefit from LRT proximity. Properties along Hillcrest Avenue, Paisley Boulevard, and Confederation Parkway have seen 9% appreciation in the past 18 months alone. Expect this trend to continue as LRT ridership increases and mixed-use developments add retail amenities.

🏘️ East Cooksville (Best Value) The area bounded by Hurontario Street, Dundas Street East, Mavis Road, and Burnhamthorpe Road offers the neighborhood’s most affordable options. Townhomes on streets like Durie Road, Trelawny Circle, and Stavebank Road regularly list in the $660,000-$690,000 range—exceptional value for properties within walking distance of Cooksville GO Station.

🏘️ West Cooksville (Family-Friendly) Closer to Cawthra Road, this section features larger lots and more detached homes. While prices run higher ($800,000-$900,000 for detached), the proximity to better-rated schools like Cooksville Creek Public School (7.2/10 Fraser Institute rating) and John Fraser Secondary School (6.8/10) attracts families willing to pay a premium.

Transit and Commute Times

Cooksville GO Station serves as the neighborhood’s crown jewel for commuters. Located at the intersection of Hurontario Street and the Lakeshore West GO line, the station provides:

- 25-minute express service to Union Station during peak hours

- 12 trains daily in each direction on weekdays

- All-day service with trains every 30 minutes off-peak

- Free parking (limited spaces) or paid parking at $7/day

The Hurontario LRT adds another layer of connectivity, with stops at Cooksville GO, Dundas Street, and multiple points north and south. A commuter living near Paisley Boulevard can reach Square One Shopping Centre in 8 minutes or Port Credit GO Station in 12 minutes via LRT—all without driving.

MiWay bus routes 3, 26, 28, and 66 provide additional local transit options, creating a walkability score of 72 for central Cooksville addresses (compared to Mississauga’s average of 58).

Schools and Family Amenities

Education quality influences long-term property values. Cooksville’s school ratings have improved steadily:

Public Elementary Schools:

- Cooksville Creek Public School: 7.2/10 (improving from 6.8/10 in 2023)

- Kenollie Public School: 6.9/10

- Fairwind Public School: 7.0/10

Catholic Elementary Schools:

- St. Catherine of Alexandria: 7.5/10

- Merciful Redeemer: 7.1/10

Secondary Schools:

- John Fraser Secondary School: 6.8/10 (acclaimed arts program)

- T.L. Kennedy Secondary School: 6.5/10

While these ratings trail Mississauga’s top-tier schools (which score 8.5+), they represent solid educational environments and show upward trajectories. Buyers should note that school catchment areas change, so verify current boundaries before purchasing.

Parks and recreation include Cooksville Creek Linear Park, offering walking trails and green space, plus the Huron Park Community Centre with swimming pools, fitness facilities, and programming for all ages.

Investment Potential and Appreciation Forecast

Cooksville’s transformation from overlooked neighborhood to emerging hotspot creates compelling appreciation potential. Several factors support optimistic projections:

- LRT-driven development: Over $2 billion in planned mixed-use developments along Hurontario Street will add retail, dining, and residential density

- GO Transit expansion: Planned service increases will reduce headways to 15 minutes by 2028

- Relative undervaluation: Current prices remain 15-20% below comparable transit-oriented neighborhoods in Toronto

- Rental demand: Proximity to Pearson Airport and employment hubs creates strong rental market (important for buyers considering future investment properties)

Conservative appreciation forecasts suggest 6-7% annual growth through 2028, potentially adding $42,000-$50,000 in equity to a $700,000 townhome purchase within two years.

Clarkson: Lakefront Charm with Family Appeal

Situated in south Mississauga along Lake Ontario, Clarkson offers a distinctly different value proposition than Cooksville. This established neighborhood combines waterfront proximity, mature tree canopy, strong schools, and a village-like atmosphere that attracts families seeking community character.

Clarkson Housing Market Overview

Clarkson’s housing stock skews toward detached and semi-detached homes built primarily in the 1960s-1980s, with pockets of newer townhome developments. Prices reflect the neighborhood’s desirability while remaining below premium Mississauga areas like Port Credit or Lorne Park:

| Property Type | Average Price (2026) | Typical Size | Price per Sq Ft |

|---|---|---|---|

| 2-Bedroom Townhome | $720,000 | 1,300-1,500 sq ft | $510 |

| 3-Bedroom Townhome | $765,000 | 1,600-1,800 sq ft | $455 |

| Semi-Detached | $825,000 | 1,700-2,000 sq ft | $465 |

| Detached 2-Storey | $920,000 | 2,000-2,400 sq ft | $420 |

| Detached Bungalow | $875,000 | 1,600-1,900 sq ft | $495 |

While Clarkson’s entry price exceeds Cooksville by $40,000-$75,000 depending on property type, buyers receive additional value through superior school ratings, lakefront access, and lower density that many families prioritize.

Prime Clarkson Streets for First-Time Buyers

Clarkson’s geography creates distinct micro-markets with varying price points:

🌊 North Clarkson (Best Value for First-Timers) The area north of the QEW between Clarkson Road and Southdown Road offers the neighborhood’s most affordable options. Semi-detached homes on streets like Birchview Drive, Tavistock Road, and Duncairn Drive list in the $780,000-$840,000 range. These properties provide Clarkson addresses with good school access while trading waterfront proximity for affordability.

🌊 Central Clarkson (Balanced Option) Between the QEW and Lakeshore Road, this section represents Clarkson’s core. Streets like Glengarry Road, Bromsgrove Road, and Bexhill Road feature well-maintained homes on mature lots. Expect pricing of $850,000-$950,000 for detached homes, with occasional townhome listings in the $720,000-$780,000 range providing entry opportunities.

🌊 South Clarkson (Premium Waterfront) South of Lakeshore Road, properties command premiums for lake proximity. While most detached homes exceed $1.2 million, townhome developments near Rattray Marsh offer occasional opportunities in the $800,000-$850,000 range for buyers prioritizing waterfront access.

Transit Connectivity and Commuting

Clarkson GO Station anchors the neighborhood’s transit infrastructure, located at Southdown Road and Lakeshore Road:

- 30-minute express service to Union Station (slightly longer than Cooksville due to fewer express trains)

- 10 trains daily in each direction on weekdays

- All-day service with trains every 30-60 minutes

- Ample parking with 1,100+ spaces at $7/day

While Clarkson lacks LRT access, MiWay bus routes 14, 23, and 91 connect to major employment areas and shopping districts. The neighborhood’s walkability score of 68 reflects its suburban character, where most residents drive for daily errands but can walk to the GO station, waterfront, and Clarkson Village shops.

Commuters should budget 35-40 minutes door-to-door for downtown Toronto travel, including parking and walking time—reasonable for the lifestyle benefits Clarkson provides.

Schools: Clarkson’s Competitive Advantage

Education quality represents one of Clarkson’s strongest selling points, with several schools ranking among Mississauga’s best:

Public Elementary Schools:

- Lorne Park Public School: 8.7/10 (top 5% provincially)

- Birchview Public School: 7.8/10

- Clarkson Public School: 7.4/10

Catholic Elementary Schools:

- St. Dominic: 8.2/10

- St. Christopher: 7.6/10

Secondary Schools:

- Lorne Park Secondary School: 8.1/10 (acclaimed academic programs)

- Clarkson Secondary School: 7.2/10

These ratings significantly exceed Cooksville’s schools and justify Clarkson’s price premium for families prioritizing education. Buyers should verify they fall within desired school catchments, as boundaries can shift.

Lifestyle and Community Features

Clarkson’s appeal extends beyond housing and schools to encompass lifestyle amenities:

Waterfront Access: Rattray Marsh Conservation Area offers 90 acres of protected wetland with boardwalk trails, birdwatching, and beach access—all free and within walking/cycling distance of most Clarkson homes.

Clarkson Village: This charming commercial district along Lakeshore Road features independent shops, cafes, restaurants, and services, creating a walkable village atmosphere rare in suburban Mississauga.

Parks and Recreation: Numerous neighborhood parks include Clarkson Park (with sports fields and playground), Jack Darling Memorial Park (waterfront park with beach and picnic areas), and the Waterfront Trail connecting to Port Credit and beyond.

Community Events: The Clarkson Village Business Improvement Area hosts seasonal events, farmers markets, and community gatherings that foster neighborhood connection.

This lifestyle package attracts buyers willing to pay Clarkson’s premium over Cooksville, particularly families with children and couples prioritizing outdoor recreation.

Appreciation Outlook for Clarkson

Clarkson’s established character limits dramatic transformation, but steady appreciation continues:

- Waterfront scarcity: Limited lakefront property in the GTA ensures sustained demand

- School quality: Top-rated schools drive family buyer competition

- Mature neighborhood stability: Low turnover creates supply constraints supporting prices

- GO Transit improvements: Planned service increases enhance commuter appeal

Projected appreciation of 5-6% annually through 2028 reflects Clarkson’s mature market status. While slightly below Cooksville’s growth potential, this translates to $45,000-$55,000 in equity on a $900,000 purchase over two years—solid returns with lower volatility than emerging neighborhoods.

First-Time Buyer Financial Strategies for Cooksville and Clarkson in 2026

Understanding available programs and mortgage options transforms aspiration into achievable homeownership. First-time buyers in 2026 can leverage several tools to overcome down payment and qualification challenges.

Government Programs and Incentives

Tax-Free First Home Savings Account (FHSA) 🏦

Introduced in 2023 and now fully established, the Tax-Free First Home Savings Account allows first-time buyers to contribute up to $8,000 annually (lifetime maximum $40,000) with tax-deductible contributions and tax-free withdrawals for home purchases.

Example: A buyer contributing the maximum $8,000 annually for five years accumulates $40,000 plus investment growth (assuming 4% annual returns, approximately $43,300). At a 30% marginal tax rate, the tax deductions save an additional $12,000. Combined, this generates $55,300 toward a down payment—the difference between qualifying for a $650,000 home versus $750,000.

First-Time Home Buyer Incentive 💰

While the federal First-Time Home Buyers Incentive program has evolved since its 2019 launch, shared equity mortgages remain available through CMHC for qualifying buyers. The program offers 5-10% of the purchase price as a shared equity loan, reducing monthly payments without interest charges (repayment occurs upon sale or after 25 years).

Home Buyers’ Plan (HBP)

Buyers with existing RRSPs can withdraw up to $35,000 per person ($70,000 for couples) tax-free to fund down payments, with 15 years to repay the withdrawal. This program stacks with FHSA contributions for maximum down payment power.

Land Transfer Tax Rebates

Ontario first-time buyers receive rebates up to $4,000 on provincial land transfer tax. For a $700,000 Cooksville townhome, total land transfer tax approximates $9,500, reduced to $5,500 after the rebate—meaningful savings during closing.

Mortgage Qualification Strategies

Optimizing Debt Service Ratios

Lenders evaluate two key ratios:

- Gross Debt Service (GDS): Housing costs ÷ gross income (maximum 39%)

- Total Debt Service (TDS): All debt payments ÷ gross income (maximum 44%)

For a $700,000 purchase with 10% down ($70,000), the mortgage amount of $630,000 at 5.5% amortized over 25 years creates monthly payments of approximately $3,850. Adding property tax ($300/month), heating ($100), and condo fees if applicable ($250), total housing costs reach $4,500 monthly.

To qualify under GDS limits: $4,500 ÷ 0.39 = $11,538 minimum monthly gross income ($138,456 annually)

Buyers falling short can improve qualification by:

- Paying down high-interest debt (credit cards, car loans) to improve TDS

- Increasing down payment to reduce mortgage amount and monthly payments

- Adding a co-signer to combine incomes (common for first-time buyers)

- Considering longer amortization (30 years with 20%+ down payment)

Understanding closing costs in Toronto helps buyers budget beyond the down payment, as legal fees, inspections, title insurance, and moving expenses add $8,000-$15,000 to upfront costs.

Down Payment Sources and Strategies

Minimum Requirements:

- 5% down for purchase prices up to $500,000

- 10% down for the portion between $500,000-$1,000,000

- 20% down for prices exceeding $1,000,000

For a $700,000 Cooksville townhome:

- First $500,000 requires 5% = $25,000

- Remaining $200,000 requires 10% = $20,000

- Total minimum down payment: $45,000

Gifted Down Payments: Most lenders accept gifted funds from immediate family members without requiring repayment. Proper documentation (gift letter) proves the funds are gifts, not loans that would affect debt ratios.

Borrowed Down Payments: While borrowing your entire down payment creates qualification challenges, combining saved funds with a small personal loan or line of credit can bridge gaps. Ensure monthly payments fit within TDS limits.

Sale of Assets: Selling investments, vehicles, or other assets provides down payment funds. Consider tax implications on investment sales and timing to avoid market volatility.

Choosing the Right Mortgage Product

Fixed vs variable rate mortgages present the fundamental choice for first-time buyers:

Fixed Rate Mortgages (Currently 5.19%-5.79% for 5-year terms):

- ✅ Payment certainty for budgeting

- ✅ Protection against rate increases

- ❌ Higher initial rates than variable

- ❌ Larger penalties for early termination

Variable Rate Mortgages (Currently 5.45%-5.95%, prime + 0.5-1.0%):

- ✅ Lower initial rates

- ✅ Potential savings if rates decline

- ✅ Lower break penalties

- ❌ Payment uncertainty

- ❌ Risk of rate increases

For first-time buyers with tight budgets, fixed rates provide peace of mind despite slightly higher costs. Buyers with income flexibility or expecting rate declines might prefer variable rates to capitalize on potential savings.

Comparing Cooksville vs Clarkson: Which Neighborhood Fits Your Needs?

Choosing between these value neighborhoods requires weighing priorities, budget constraints, and lifestyle preferences. This detailed comparison helps first-time buyers make informed decisions.

Price and Affordability Analysis

Winner: Cooksville 🏆

Cooksville offers entry prices $40,000-$75,000 lower than comparable Clarkson properties, creating easier qualification and lower monthly payments. For buyers maximizing budget efficiency, Cooksville provides more home per dollar.

Example Monthly Cost Comparison:

Cooksville 3-Bedroom Townhome ($720,000):

- Down payment (10%): $72,000

- Mortgage amount: $648,000

- Monthly mortgage (5.5%, 25 years): $3,960

- Property tax: $300

- Utilities/heating: $200

- Condo fees: $250

- Total monthly: $4,710

Clarkson 3-Bedroom Townhome ($765,000):

- Down payment (10%): $76,500

- Mortgage amount: $688,500

- Monthly mortgage (5.5%, 25 years): $4,205

- Property tax: $320

- Utilities/heating: $200

- Condo fees: $250

- Total monthly: $4,975

The $265 monthly difference ($3,180 annually) represents significant savings for first-time buyers, potentially funding emergency reserves, renovations, or accelerated mortgage payments.

Transit and Commute Comparison

Winner: Cooksville 🏆

Cooksville GO Station offers more frequent service and faster commutes (25 minutes express vs 30 minutes), plus LRT connectivity that Clarkson lacks. For daily Toronto commuters, Cooksville’s 5-minute time savings accumulates to 40+ hours annually—valuable time with family or for personal pursuits.

However, buyers working in western GTA locations (Oakville, Burlington, Milton) may find Clarkson’s positioning advantageous, with reverse commutes avoiding congestion.

School Quality Comparison

Winner: Clarkson 🏆

Clarkson’s schools significantly outperform Cooksville’s, with multiple institutions rating 7.5+ compared to Cooksville’s 6.5-7.2 range. For families with children or planning families, this educational advantage justifies Clarkson’s price premium.

Buyers should consider:

- Current family status: Families with school-age children benefit immediately from better schools

- Timeline: Buyers planning children in 5+ years may prioritize affordability now, planning to upsize later

- Alternative options: Private schools, French immersion programs, or specialized academies can supplement neighborhood schools

Lifestyle and Amenities Comparison

Winner: Clarkson 🏆

Clarkson’s waterfront access, village atmosphere, and mature neighborhood character create superior lifestyle amenities. Rattray Marsh, Jack Darling Park, and the Waterfront Trail offer recreation impossible to replicate in central Mississauga.

Cooksville counters with urban conveniences—more restaurants, shops, and services within walking distance due to higher density. Buyers prioritizing outdoor recreation and suburban tranquility prefer Clarkson; those valuing urban energy and walkable amenities lean toward Cooksville.

Investment and Appreciation Potential

Winner: Cooksville 🏆

Cooksville’s ongoing transformation and relative undervaluation create stronger appreciation potential (6-7% projected vs 5-6% for Clarkson). First-time buyers viewing their purchase as a 5-7 year stepping stone to larger homes should prioritize Cooksville’s equity-building potential.

Clarkson’s mature, stable character offers lower volatility and sustained demand, appealing to buyers planning longer-term residence (10+ years) who value predictability over maximum appreciation.

Decision Framework for First-Time Buyers

Choose Cooksville if you:

- Prioritize maximum affordability and lower monthly payments

- Commute daily to downtown Toronto

- Value urban conveniences and walkability

- Seek maximum appreciation potential for future equity

- Don’t have school-age children currently

- Embrace emerging neighborhoods and transformation

Choose Clarkson if you:

- Can stretch budget for superior schools and lifestyle

- Have or plan to have children soon

- Prioritize outdoor recreation and waterfront access

- Value established neighborhood character and stability

- Work in western GTA or have flexible commute

- Plan longer-term residence (10+ years)

Neither choice is objectively superior—the right neighborhood depends on individual circumstances, priorities, and financial capacity.

Practical Steps to Purchase in Cooksville or Clarkson

Understanding neighborhoods and financing options means nothing without actionable steps toward homeownership. This section provides a roadmap for first-time buyers targeting these Mississauga value neighborhoods in 2026.

Step 1: Financial Preparation (3-6 Months Before Searching)

Build Your Down Payment 💵

Maximize FHSA contributions, consolidate savings, and explore family gifts. Calculate your target down payment (minimum 10% for $700,000+ purchases) plus closing costs ($10,000-$15,000) and emergency reserves (3-6 months expenses).

Improve Your Credit Score

Lenders offer best rates to borrowers with 720+ credit scores. Improve your score by:

- Paying all bills on time for 6+ months

- Reducing credit utilization below 30% of limits

- Avoiding new credit applications

- Correcting errors on credit reports

How to improve your credit score in Canada provides detailed strategies for score optimization.

Reduce Existing Debt

Pay down high-interest credit cards and loans to improve debt service ratios. Each $500 monthly payment eliminated increases borrowing capacity by approximately $100,000.

Step 2: Mortgage Pre-Approval (1-2 Months Before Searching)

Obtain pre-approval before viewing properties to:

- Understand exact borrowing capacity

- Lock in interest rates (typically 90-120 day holds)

- Demonstrate seriousness to sellers

- Avoid disappointment from viewing unaffordable properties

The ins and outs of mortgage pre-approval in Ontario explains the process comprehensively.

Work with experienced mortgage brokers who access multiple lenders, securing better rates than single-bank applications. Pre-approval requires:

- Employment verification (pay stubs, T4s, employment letter)

- Income documentation (2 years for self-employed)

- Asset verification (bank statements, investment accounts)

- Credit check authorization

- Identification documents

Step 3: Assemble Your Team

Real Estate Agent: Choose agents specializing in Mississauga and familiar with Cooksville/Clarkson specifically. Request references from recent first-time buyer clients and verify their knowledge of local micro-markets.

Mortgage Broker: Independent brokers access 30+ lenders versus single-bank options, often securing rates 0.15-0.25% lower—saving thousands over mortgage terms.

Real Estate Lawyer: Essential for reviewing offers, conducting title searches, and managing closing. Budget $1,500-$2,500 for legal fees.

Home Inspector: Critical for identifying property issues before finalizing purchases. Budget $400-$600 for thorough inspections.

Step 4: Strategic Property Search

Define Must-Haves vs Nice-to-Haves

Prioritize non-negotiable features (bedrooms, bathrooms, parking, location) versus flexible preferences (finishes, yard size, basement). First-time buyers often compromise on cosmetic features to secure locations and layouts meeting core needs.

Focus on Target Streets

Reference the specific streets identified earlier in Cooksville (Hillcrest Avenue, Paisley Boulevard, Durie Road) and Clarkson (Birchview Drive, Tavistock Road, Glengarry Road) where value concentrates.

Monitor Market Activity

Track new listings daily, attend open houses to understand market conditions, and note how quickly properties sell and at what percentage of asking price. This intelligence informs offer strategies.

Step 5: Making Competitive Offers

2026 Market Conditions: The balanced market allows conditional offers (subject to financing, inspection, status certificate review for condos) without automatic rejection. However, well-priced properties still attract multiple offers.

Offer Strategy Components:

- Price: Based on comparable sales, property condition, and days on market

- Deposit: Typically $10,000-$25,000, demonstrating commitment

- Conditions: Financing (5-7 days), inspection (5-7 days), status certificate review for condos (10 days)

- Closing date: Flexible dates accommodate sellers, strengthening offers

- Inclusions: Specify appliances, fixtures, and chattels included

Negotiation Tips:

- Start with reasonable offers (95-98% of asking for fairly priced properties)

- Avoid lowball offers that offend sellers and close negotiation doors

- Be prepared to walk away if properties exceed budget or inspection reveals major issues

- Consider escalation clauses in multiple-offer situations (offering $X above highest competing bid up to maximum)

Step 6: Due Diligence and Closing

Home Inspection: Attend the inspection, ask questions, and understand major systems (roof, HVAC, electrical, plumbing). Budget $5,000-$15,000 for immediate repairs and $20,000-$30,000 for major system replacements within 5 years.

Final Walkthrough: Conduct final walkthrough 24 hours before closing to verify property condition matches agreement and all included items remain.

Closing Day: Your lawyer handles fund transfers, title registration, and key release. Expect to receive keys late afternoon on closing day.

Step 7: Post-Purchase Priorities

Emergency Fund: Maintain 3-6 months expenses for unexpected repairs, job loss, or rate increases at renewal.

Maintenance Budget: Allocate 1-2% of property value annually for maintenance and repairs ($7,000-$14,000 for a $700,000 home).

Mortgage Acceleration: Consider bi-weekly payments (equivalent to one extra monthly payment annually) or lump-sum payments (typically 10-20% of principal allowed annually) to build equity faster.

Rental Income: Properties with basement apartments or additional bedrooms can generate $1,200-$1,800 monthly rental income, substantially reducing carrying costs. Verify zoning permits legal basement apartments before purchasing.

Frequently Asked Questions: First-Time Buyers in Cooksville and Clarkson

Q: Can I afford a home in Cooksville or Clarkson with a $80,000 household income?

A: Challenging but potentially achievable with maximum down payment and minimal other debts. An $80,000 income supports approximately $31,200 in annual housing costs (39% GDS), or $2,600 monthly. After property tax, utilities, and condo fees ($750 combined), $1,850 remains for mortgage payments—supporting approximately $300,000 mortgage at current rates.

With a $300,000 mortgage, you’d need $400,000+ down payment for a $700,000 property—unrealistic for most first-time buyers. However, adding a co-signer, targeting lower-priced condos ($520,000-$580,000), or increasing income through side employment creates pathways to homeownership.

Q: How much should I budget for closing costs?

A: Expect 1.5-3% of purchase price for closing costs:

- Land transfer tax: $9,500 (minus $4,000 rebate = $5,500)

- Legal fees: $1,500-$2,500

- Home inspection: $400-$600

- Title insurance: $250-$400

- Property tax adjustment: $500-$1,500

- Utility connections: $200-$500

- Moving costs: $500-$2,000

Total: $9,000-$13,000 for a $700,000 purchase. Budget conservatively to avoid last-minute financial stress.

Q: Should I buy now or wait for prices to drop further?

A: Market timing is notoriously difficult. While prices stabilized from 2021 peaks, waiting risks:

- Interest rate increases reducing borrowing capacity

- Continued appreciation in value neighborhoods (6-7% annually projected)

- Rental costs exceeding potential savings from price decreases

If you’re financially prepared, have stable employment, and plan 5+ year residence, purchasing in 2026’s balanced market conditions offers reasonable entry points. Attempting to time the absolute market bottom often results in missed opportunities.

Q: What’s better for first-time buyers—townhomes or condos?

A: Townhomes offer more space, privacy, and typically stronger appreciation, but require higher purchase prices and maintenance responsibilities. Condos provide lower entry prices, included maintenance, and amenities, but face condo fees ($250-$450 monthly) and special assessments.

For buyers planning families or longer-term residence, townhomes generally prove superior despite higher costs. Buyers prioritizing minimal maintenance and maximum affordability may prefer condos as stepping stones to larger properties within 5-7 years.

Q: How do I compete with investors and cash buyers?

A: First-time buyers possess advantages investors lack:

- Access to government programs (FHSA, First-Time Home Buyer Incentive)

- Lower down payment requirements (minimum 5-10% vs 20% for investors)

- Emotional connection to properties, sometimes outweighing investor calculations

Strengthen your position through:

- Solid pre-approvals demonstrating financing certainty

- Flexible closing dates accommodating sellers

- Personal letters to sellers explaining your connection to the property

- Quick decision-making and clean offers without excessive conditions

Conclusion: Your Path to Homeownership in Mississauga’s Value Neighborhoods

This First-Time Buyers Guide to Mississauga Value Neighborhoods Like Cooksville and Clarkson in 2026 reveals that homeownership remains achievable despite GTA market challenges. Both neighborhoods offer distinct advantages—Cooksville provides maximum affordability and appreciation potential, while Clarkson delivers superior schools and lifestyle amenities—allowing buyers to align choices with priorities and budgets.

Success requires thorough preparation: building down payments through FHSA and family gifts, optimizing credit scores and debt ratios, securing pre-approvals, and assembling experienced professional teams. The 2026 market’s balanced conditions favor prepared buyers willing to act decisively when opportunities arise.

Your Next Steps

- Calculate your maximum budget using debt service ratio guidelines and stress test requirements

- Maximize down payment sources through FHSA contributions, RRSP withdrawals, and family gifts

- Obtain mortgage pre-approval to understand exact borrowing capacity and lock in rates

- Research specific streets in Cooksville and Clarkson matching your budget and priorities

- Assemble your team of real estate agent, mortgage broker, and lawyer with local expertise

- Begin viewing properties to understand market conditions and refine preferences

- Make informed offers based on comparable sales and professional guidance

The journey from aspiring homeowner to keys-in-hand requires patience, diligence, and strategic decision-making. However, thousands of first-time buyers successfully navigate this path annually, building equity and stability in Mississauga’s value neighborhoods.

Cooksville and Clarkson represent your opportunity to join their ranks in 2026—seize it with confidence, preparation, and the knowledge this guide provides. Your first home awaits in one of these emerging communities, offering not just shelter but a foundation for long-term financial growth and quality of life.

For personalized guidance on your specific situation, connect with experienced mortgage professionals who understand first-time buyer challenges and opportunities in Mississauga’s evolving market.