March 14, 2026

How Toronto’s CMHC 30-Year Amortization Boost Fuels Private Mortgage Demand for $1M-$1.5M Freeholds in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

A quiet policy change in late 2024 is reshaping who can buy a Toronto freehold — and how they pay for it. 🏡

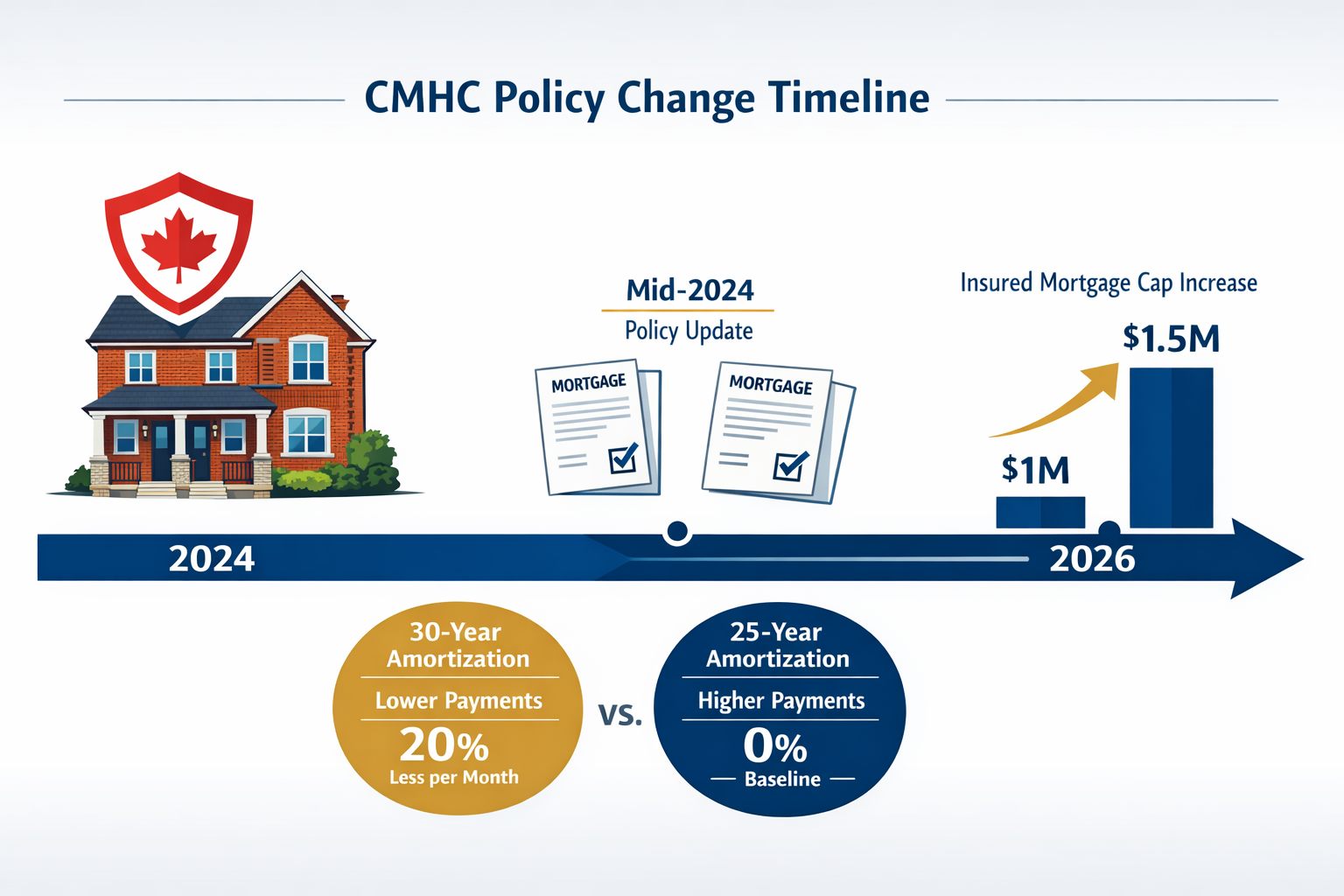

When the federal government expanded CMHC’s 30-year amortization rules effective December 15, 2024, it did more than lower monthly payments. It effectively tripled buying power for a specific group of high-net-worth first-time buyers eyeing Toronto’s most competitive segment: freehold homes priced between $1 million and $1.5 million [7]. At the same time, understanding how Toronto’s CMHC 30-year amortization boost fuels private mortgage demand for $1M-$1.5M freeholds in 2026 means looking at two very different buyer stories — the newly empowered purchaser and the struggling renewer forced into alternative financing.

Key Takeaways 📌

- CMHC’s December 2024 rule change raised the insured mortgage cap to $1.5M and extended 30-year amortizations to all first-time buyers — not just new construction purchasers [7].

- Toronto freeholds in the $1M–$1.5M range are now the most active segment, with semi-detached homes averaging $1,027,376 in February 2026.

- Condo market weakness (down 8.9% year-over-year) is pushing buyers toward freeholds, intensifying demand in this price band.

- Private mortgage lenders are filling gaps where CMHC rules still fall short — particularly for self-employed buyers and those with non-traditional income.

- Two distinct buyer groups are driving private mortgage demand: leveraged first-time buyers needing hybrid financing and existing homeowners facing renewal shock.

The CMHC Rule Change That Rewrote Toronto’s Freehold Math

Before December 2024, buying an insured mortgage on a home over $1 million was simply not possible in Canada. The old cap stopped at $999,999. That meant buyers of Toronto freeholds — where even a semi-detached in East York or Leslieville routinely crosses $1 million — needed a 20% down payment minimum, disqualifying thousands of otherwise-qualified buyers from the market.

The new rules changed three things at once [7]:

| Feature | Old Rule | New Rule (Dec 15, 2024) |

|---|---|---|

| Insured mortgage cap | $999,999 | $1,500,000 |

| 30-year amortization eligibility | New construction only | All first-time buyers |

| Minimum down payment (on $1.5M) | 20% ($300,000) | As low as 10% |

This matters enormously in Toronto. A buyer purchasing a $1.2M semi-detached freehold now needs roughly $120,000–$144,000 as a down payment rather than $240,000. Monthly payments on a 30-year amortization at current rates are also meaningfully lower than on a 25-year schedule — freeing up cash flow and qualifying more buyers at the stress test level.

For a deeper look at how the 30-year amortization works in practice, see this breakdown of 30-year amortization options for first-time buyers.

Why Freeholds — Not Condos — Are Winning

The condo market tells a sobering story. Condo apartments averaged just $626,650 in February 2026 — down 8.9% year-over-year — with supply far outpacing demand. CMHC Deputy Chief Economist Tania Bourassa-Ochoa warned that “homeownership supply, particularly in the condominium segment, continues to face significant challenges in the face of falling presales” [1]. For the first time this century, rental starts exceeded condo starts in the City of Toronto [1].

Buyers who once considered condos as a stepping stone are now bypassing them entirely. The hunt for affordability in Toronto real estate has shifted decisively toward freeholds — specifically semi-detached and detached homes in the $1M–$1.5M range where the new CMHC rules now apply.

Toronto realtor data from February 2026 supports this: freehold detached homes recorded 1,683 sales — up 24.5% month-over-month — while semi-detached homes averaged $1,027,376 with 336 sales. The GTA’s sales-to-new-listings ratio climbed to 36.1% in February 2026, up from 28.6% in January, signaling early stabilization [2].

Two Buyer Profiles Driving Private Mortgage Demand in 2026

Understanding how Toronto’s CMHC 30-year amortization boost fuels private mortgage demand for $1M-$1.5M freeholds in 2026 requires recognizing that not every buyer fits neatly into CMHC’s box. Two distinct profiles are emerging — and both are turning to private lenders.

🏆 Profile 1: The High-Net-Worth Leveraged First-Time Buyer

These buyers have strong assets and income but complex financial pictures. Think IT consultants, incorporated professionals, or self-employed entrepreneurs who report income in ways that traditional lenders struggle to assess. They can afford a $1.2M–$1.4M freehold. They may even qualify for CMHC insurance in theory. But their stated income vs. actual income gap creates underwriting friction at the big banks.

💬 “Buyers in the $1.2M range are getting significant activity — but many need creative financing to close the gap between what they earn and what lenders will approve.” — Toronto real estate market observation [2]

For these buyers, a hybrid financing structure is increasingly common:

- First mortgage: CMHC-insured, 30-year amortization, at competitive bank rates

- Second mortgage: Private lender bridge, typically 1–2 year term at 7–12%

This layered approach lets buyers access freeholds they couldn’t otherwise purchase. Learn more about private mortgage options in Ontario to understand how these structures work.

Self-employed buyers face unique documentation hurdles. Resources like guidance on how self-employed borrowers can secure insurable mortgage rates in 2026 are increasingly relevant for this cohort.

😟 Profile 2: The Renewal-Shock Homeowner Seeking Private Relief

On the other side of the market are homeowners who bought freeholds between 2019 and 2022 at peak prices and are now facing mortgage renewals at rates significantly higher than their original terms. Many locked in at 1.5–2.5% and are now renewing at 4.5–5.5%. Monthly payments can jump by $800–$1,500 or more.

For those who don’t qualify for traditional renewal terms — perhaps due to job changes, self-employment transitions, or credit events — private lenders offer a short-term bridge. Understanding the mortgage renewal shock and refinancing options for Toronto homebuyers is critical for this group.

Where CMHC’s 30-Year Rules Still Fall Short — and Private Lenders Step In

Critics of the expanded CMHC program point out a key limitation: the rules are “too restrictive to have a notable impact in Canada’s pricier cities” [4]. Even with a 30-year amortization and a $1.5M cap, buyers still face:

- The mortgage stress test, which requires qualifying at roughly 2% above the contract rate

- Strict income documentation requirements that disadvantage self-employed buyers

- New construction premiums that negate savings — professionals note new builds demand “a much higher price per square foot, so any cost savings would quickly be negated” [4], pushing buyers toward resale freeholds instead

This is where private lenders are transforming the borrowing landscape in 2026, offering financing that traditional banks overlook. Private lenders in Ontario are filling gaps with faster approvals, flexible income verification, and short-term bridge solutions.

For buyers navigating the stress test, this Canadian mortgage stress test cheat sheet provides essential context. And for those exploring private loan lenders in Ontario, understanding rate premiums (typically 7–12% vs. 4–5.5% at banks) helps set realistic expectations.

What Buyers Should Know Before Choosing Private Financing

✅ Private mortgages are short-term tools — typically 1–2 year terms, designed as bridges to conventional financing. ✅ Higher rates are the trade-off for speed and flexibility — factor this into total cost of ownership. ✅ Exit strategy matters — have a clear plan to refinance into a CMHC-insured or conventional mortgage within the private term. ✅ Work with a licensed mortgage broker who can compare all lender tiers — A-lenders, B-lenders, and private — simultaneously.

Use the mortgage calculator tools to model different amortization and rate scenarios before committing.

Conclusion: Navigating the New Freehold Financing Reality in 2026

How Toronto’s CMHC 30-year amortization boost fuels private mortgage demand for $1M-$1.5M freeholds in 2026 is a story of policy meeting market reality — with gaps that private lenders are eager to fill. The expanded CMHC rules are genuinely powerful for qualified first-time buyers, lowering entry barriers into Toronto’s most sought-after housing segment. But they don’t solve every problem, and they leave a meaningful portion of buyers — the self-employed, the recently renewed, the income-complex — still needing alternative solutions.

✅ Actionable Next Steps

- Assess your buyer profile — Are you a first-time buyer who fits CMHC’s new rules, or do you need a hybrid or private solution?

- Get pre-approved early — Toronto’s freehold market moves quickly; a pre-approval signals seriousness to sellers.

- Explore all lender tiers — A-lenders, B-lenders, and private lenders each serve different needs. Don’t assume the bank is your only option.

- Model your amortization — Compare 25-year vs. 30-year payment scenarios using an online calculator to understand the real monthly impact.

- Consult a licensed mortgage broker — Especially if you’re self-employed or facing renewal, professional guidance can save thousands.

Toronto’s freehold market in 2026 rewards the prepared buyer. The CMHC changes opened a door — knowing how to walk through it is the next step.

References

[1] CMHC Insurance – https://wowa.ca/calculators/cmhc-insurance

[2] Toronto First Time Buyers Bidding Wars – https://storeys.com/toronto-first-time-buyers-bidding-wars/

[4] 30 Year Mortgage Amortization Experts – https://storeys.com/30-year-mortgage-amortization-experts/

[7] Breaking News 30 Year Amortizations For All First Time Home Buyers Insured Mortgages Up To 1 5 Million – https://www.ratehub.ca/blog/breaking-news-30-year-amortizations-for-all-first-time-home-buyers-insured-mortgages-up-to-1-5-million/