March 12, 2026

Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

{“cover”:”Professional landscape format (1536×1024) hero image featuring bold text overlay ‘Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026’ in extra large 72pt white sans-serif font with dark shadow and semi-transparent navy overlay box, positioned center-upper third. Background shows dramatic Toronto skyline with CN Tower at dusk, modern condominium buildings, overlay of mortgage documents and calculator with CMHC logo visible. Foreground includes diverse self-employed professionals (freelancer with laptop, small business owner) looking hopeful toward cityscape. Color scheme: deep navy blue, gold accents, white text, professional editorial quality with high contrast, magazine cover aesthetic, financial empowerment theme”,”content”:[“Landscape format (1536×1024) detailed infographic showing side-by-side comparison of 25-year versus 30-year amortization payment structures for Toronto home prices $1M-$1.5M range. Left side displays traditional 25-year timeline with higher monthly payments in bold red numbers, right side shows 30-year extended amortization with reduced monthly payments in green. Center features large percentage savings calculation with downward arrow, CMHC logo watermark, clean financial charts with gridlines, professional blue and white color scheme, calculator and home icons, mortgage approval checkmarks, modern minimalist design with clear data visualization”,”Landscape format (1536×1024) conceptual illustration showing self-employed documentation pathway without T4 slips. Center features diverse self-employed workers (contractor with hard hat, creative professional at desk, consultant with tablet) surrounded by floating alternative income verification documents including bank statements, Notice of Assessment forms, business financial statements, invoices, contracts. Documents arranged in organized flow chart pattern with green approval checkmarks, CMHC guidelines document visible, professional office background slightly blurred, warm lighting, empowering business atmosphere, modern flat design elements mixed with photorealistic people, trust and accessibility theme”,”Landscape format (1536×1024) detailed visual representation of mortgage stress test qualification process specific to self-employed borrowers. Split-screen composition: left side shows traditional employment income verification with T4 forms marked with red X, right side displays self-employed alternative pathways with multiple green checkmarks. Center features large calculator display showing qualifying income calculations, interest rate percentages, debt service ratio formulas overlaid as transparent graphics. Background includes Toronto real estate imagery, mortgage broker reviewing documents with self-employed client, professional consultation setting, charts showing income add-backs for business deductions, confident and solution-focused atmosphere, corporate blue and green color palette”,”Landscape format (1536×1024) strategic action plan visualization for self-employed Toronto homebuyers in 2026. Foreground shows organized checklist or roadmap with numbered steps (1-5) featuring icons for documentation, mortgage broker consultation, pre-approval, property search, closing. Background displays successful diverse self-employed buyers holding house keys in front of Toronto residential property, mix of detached homes and modern condos. Includes visual elements of timeline calendar showing optimal application periods, interest rate trend arrows, CMHC 30-year amortization benefit callout boxes, professional financial planning aesthetic with gold and navy accents, aspirational and actionable mood, clean infographic style merged with lifestyle photography”]”}

The Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026 represents a transformative shift in Canadian mortgage accessibility. For self-employed professionals, freelancers, and small business owners navigating Toronto’s competitive real estate market, the extended amortization period introduced by CMHC in August 2024 has opened doors that were previously locked tight. With home prices in the $1 million to $1.5 million range dominating Toronto’s housing landscape, the ability to stretch mortgage payments over 30 years instead of the traditional 25 has fundamentally changed the affordability equation—particularly for those without traditional T4 income slips.

This comprehensive guide explores how self-employed Toronto buyers can leverage these new rules to qualify for mortgages, reduce monthly payments, and finally achieve homeownership in one of Canada’s most expensive real estate markets.

Key Takeaways

✅ Extended amortization reduces monthly payments by approximately 10-15% for Toronto homes in the $1M-$1.5M range, making homeownership more accessible for self-employed buyers with fluctuating incomes.

✅ CMHC’s relaxed documentation requirements now allow self-employed borrowers to qualify using alternative income verification methods, including bank statements and business financial statements.

✅ Self-employed applicants need only 24 months of business experience (down from previous stricter requirements) to qualify for CMHC-insured mortgages with 30-year amortizations.

✅ Income add-backs for legitimate business deductions significantly improve qualifying income calculations, helping self-employed professionals overcome traditional lending barriers.

✅ Strategic mortgage planning and professional guidance are essential to navigate the stress test and maximize approval odds under the new 2026 rules.

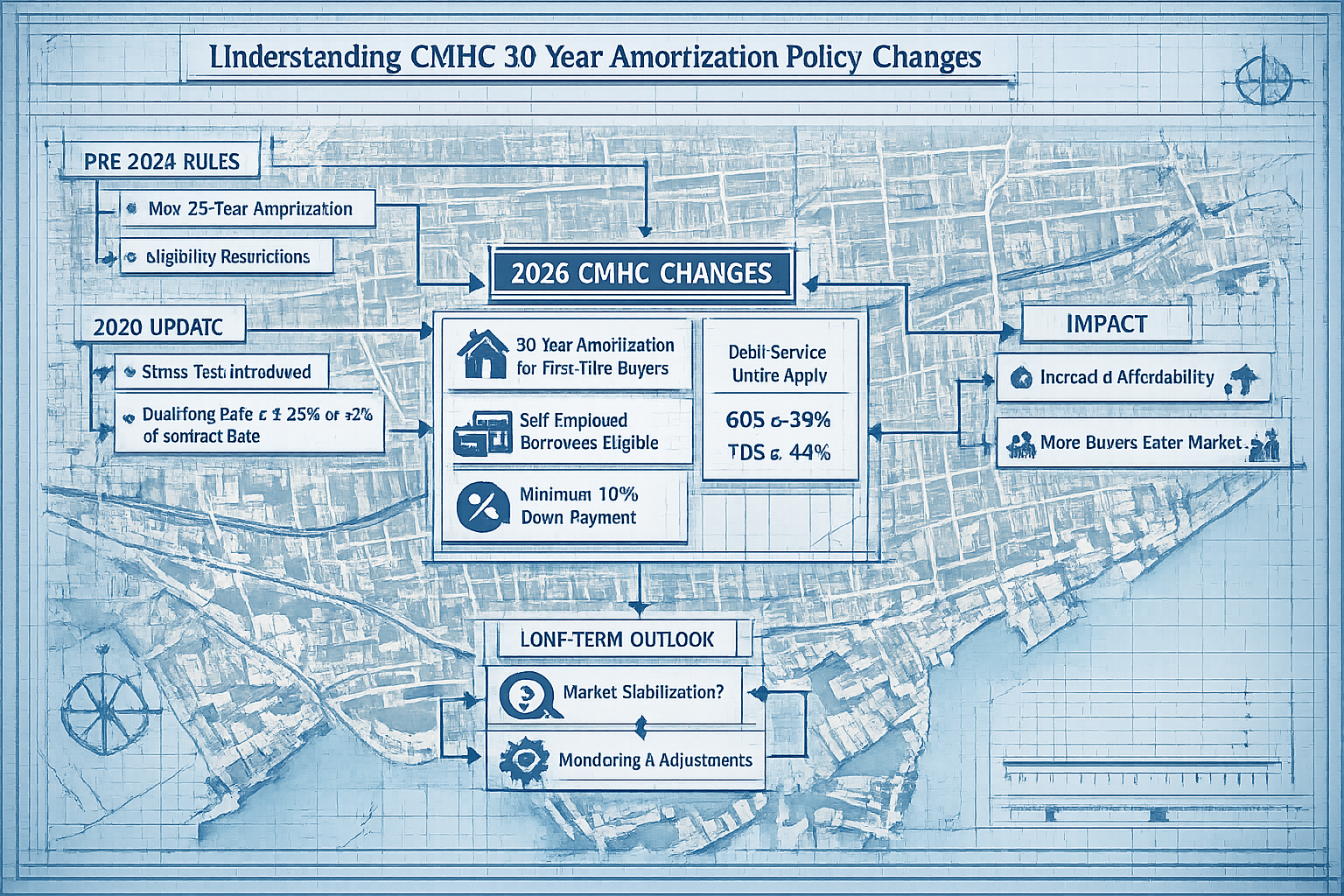

Understanding the CMHC 30-Year Amortization Policy Changes

The Canada Mortgage and Housing Corporation (CMHC) implemented significant policy changes effective August 1, 2024, that continue to reshape the mortgage landscape in 2026. These modifications specifically target first-time homebuyers and purchasers of newly constructed properties, extending the maximum amortization period from 25 years to 30 years for insured mortgages.

Who Qualifies for 30-Year Amortization?

The eligibility criteria for extended amortization are straightforward but specific:

- First-time homebuyers purchasing any property type

- Any buyer purchasing newly constructed homes or condominiums

- Properties with purchase prices up to $1 million (insured mortgage threshold)

- Buyers with minimum down payments of 5-19.99% (requiring CMHC insurance)

For self-employed Toronto buyers, this represents a critical opportunity. The city’s average home price hovers around $1.1 million in 2026, with many entry-level condominiums and townhouses falling within the eligible price range.

The Financial Impact: Real Numbers for Toronto Buyers

The mathematical advantage of 30-year amortization becomes immediately apparent when examining Toronto’s typical home prices:

| Home Price | Down Payment (10%) | Mortgage Amount | 25-Year Monthly Payment* | 30-Year Monthly Payment* | Monthly Savings |

|---|---|---|---|---|---|

| $900,000 | $90,000 | $810,000 | $4,347 | $3,821 | $526 |

| $1,000,000 | $100,000 | $900,000 | $4,830 | $4,245 | $585 |

| $1,200,000** | $240,000 | $960,000 | $5,152 | $4,528 | $624 |

*Assumes 5.5% interest rate **Requires 20% down payment; not CMHC-insured

These monthly savings of $500-600+ translate to annual savings of $6,000-7,200, which can be redirected toward business investments, emergency funds, or other financial priorities—particularly valuable for self-employed individuals managing variable income streams.

For self-employed borrowers exploring their options, understanding how to obtain a mortgage when you’re self-employed provides essential foundational knowledge.

Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers: Qualification Strategies

The Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026 extends far beyond simple payment reduction. The real game-changer lies in how these rules interact with CMHC’s relaxed documentation requirements for self-employed borrowers.

Alternative Income Verification Methods

Traditional mortgage qualification relies heavily on T4 slips and employment letters—documents self-employed professionals simply don’t have. CMHC’s updated guidelines now explicitly recognize alternative documentation:

📋 Acceptable Income Documentation for Self-Employed Borrowers:

- Notice of Assessment (NOA) from the Canada Revenue Agency (typically 2 years)

- Business financial statements prepared by accountants

- Bank statements showing consistent deposits (6-12 months)

- Contracts and invoices demonstrating ongoing business relationships

- Corporate tax returns (T2) for incorporated businesses

- GST/HST statements proving business revenue

The critical advantage? Income add-backs for legitimate business expenses that reduce taxable income but don’t affect actual cash flow. These include:

- Vehicle expenses and depreciation

- Home office deductions

- Business meals and entertainment (50%)

- Professional development and training

- Equipment depreciation

- Travel expenses

For example, a self-employed consultant showing $80,000 in net income on their NOA might actually have $105,000 in qualifying income after adding back $25,000 in legitimate business deductions. This additional $25,000 can mean the difference between mortgage approval and rejection.

Self-employed Toronto buyers should review comprehensive guidance on qualifying for mortgages without T4 slips in 2026 to understand all available pathways.

The 24-Month Business Experience Requirement

CMHC now requires only 24 months of self-employment history in the same field, a significant relaxation from previous stricter requirements. This change particularly benefits:

- Recent entrepreneurs who left traditional employment to start businesses

- Freelancers who transitioned from contract work to full self-employment

- Gig economy workers who formalized their income streams

- Professional service providers (consultants, designers, developers) establishing practices

The 24-month timeline is calculated from the mortgage application date backward, and lenders typically want to see:

✔️ Consistent or growing income over the period ✔️ Stable business operations without major gaps ✔️ Industry-relevant experience (even if employed previously) ✔️ Proper business registration and tax compliance

Navigating the Mortgage Stress Test as Self-Employed

The federal mortgage stress test remains a significant hurdle for all borrowers, including self-employed applicants. In 2026, borrowers must qualify at the higher of:

- The contract rate plus 2%, OR

- 5.25% (the current benchmark rate)

For self-employed buyers with fluctuating incomes, this creates unique challenges. However, the combination of 30-year amortization and income add-backs provides powerful tools to overcome stress test barriers.

Example Scenario:

Maria, a self-employed graphic designer in Toronto, wants to purchase a $950,000 condo with a 15% down payment ($142,500). Her mortgage amount would be $807,500.

- Actual interest rate offered: 5.2%

- Stress test rate: 7.2% (5.2% + 2%)

- Net income on NOA: $85,000

- Income add-backs: $18,000 (home office, vehicle, equipment depreciation)

- Total qualifying income: $103,000

With 25-year amortization:

- Monthly payment at stress test rate: $5,180

- Required annual income: $155,400 (at 40% TDS ratio)

- Result: Does not qualify ❌

With 30-year amortization:

- Monthly payment at stress test rate: $4,550

- Required annual income: $136,500 (at 40% TDS ratio)

- Result: Qualifies with room to spare ✅

This example demonstrates how the extended amortization period can be the deciding factor for self-employed Toronto buyers. For detailed strategies, explore how self-employed borrowers can navigate the 2026 mortgage stress test.

Maximizing Approval Odds: Practical Steps for Self-Employed Toronto Buyers in 2026

Understanding the Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026 requires more than theoretical knowledge—it demands strategic action. Here are proven steps to maximize mortgage approval odds:

1. Optimize Your Financial Documentation 📊

12 Months Before Applying:

- Separate business and personal finances completely (dedicated business bank account)

- Maximize income reporting while remaining tax-compliant (reduce unnecessary write-offs)

- Maintain consistent deposits to business accounts (avoid large irregular transactions)

- Document all income sources with contracts, invoices, and payment records

- Improve credit score to 680+ (ideally 700+) for best rates

6 Months Before Applying:

- Engage a qualified accountant to prepare business financial statements

- Request Notice of Assessment from CRA (ensure it’s current and accurate)

- Compile 6-12 months of bank statements showing healthy cash flow

- Reduce consumer debt to improve debt service ratios

- Avoid major purchases that could impact credit or savings

3 Months Before Applying:

- Calculate realistic qualifying income (including add-backs)

- Determine maximum affordable purchase price using 30-year amortization

- Get pre-approved with a mortgage broker experienced in self-employed applications

- Identify target properties within approved price range

2. Work with Self-Employed Mortgage Specialists

Not all lenders or mortgage brokers have equal expertise with self-employed applications. The complexity of income verification, add-backs, and CMHC guidelines requires specialized knowledge.

Key questions to ask potential mortgage brokers:

- How many self-employed clients have you helped in the past 12 months?

- Which lenders are most flexible with self-employed income verification?

- Can you help identify all eligible income add-backs for my situation?

- What documentation will maximize my qualifying income?

- Do you have relationships with CMHC-approved lenders offering 30-year amortization?

For current rate options, review self-employed mortgage rates in Toronto for 2026 to understand competitive offerings.

3. Understand Total Debt Service (TDS) Ratios

Lenders evaluate mortgage applications using two critical ratios:

Gross Debt Service (GDS) Ratio:

- Includes: mortgage payment, property taxes, heating, 50% of condo fees

- Maximum: 39% of gross income

Total Debt Service (TDS) Ratio:

- Includes: GDS + all other debt payments (credit cards, car loans, student loans)

- Maximum: 44% of gross income

For self-employed buyers, reducing or eliminating consumer debt before applying can dramatically improve approval odds. Even small monthly obligations (a $300 car payment or $150 minimum credit card payment) can reduce borrowing capacity by $50,000-75,000.

4. Consider Alternative Lender Options

If traditional CMHC-insured mortgages prove challenging, self-employed Toronto buyers have additional options:

B-Lenders:

- More flexible income verification

- Higher interest rates (typically 0.5-1.5% above prime lenders)

- Useful for complex income situations or credit challenges

- May offer bridge financing until traditional qualification is possible

Private Lenders:

- Asset-based lending (focused on property value, not income)

- Short-term solutions (6-24 months typically)

- Higher rates and fees

- Strategic for immediate purchases with refinancing plans

For comprehensive information, explore mortgages for self-employed borrowers covering all lender categories.

5. Strategic Timing and Market Conditions

Toronto’s real estate market in 2026 presents unique opportunities for strategic buyers. With inventory levels stabilizing and competition moderating from the frenzied 2021-2022 period, self-employed buyers have more negotiating power.

Optimal timing strategies:

- Apply during strong income months when bank statements show higher deposits

- Time applications after tax filing when NOAs are current and accurate

- Target properties within CMHC limits ($1 million or less) to access 30-year amortization

- Consider newly constructed properties which qualify for extended amortization regardless of buyer status

- Monitor interest rate trends and lock in rates when favorable

Toronto Market Context: Opportunities for Self-Employed Buyers in 2026

The Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026 must be understood within the broader Toronto real estate context. Several market factors create a favorable environment for strategic self-employed purchasers:

Current Market Conditions 🏘️

Price Stabilization: Toronto’s average home price has stabilized around $1.1 million in early 2026, down from peak levels but still representing significant value in desirable neighborhoods. This creates opportunities for:

- First-time buyers entering previously unaffordable markets

- Condo purchasers accessing units in the $700,000-$950,000 range (within CMHC limits)

- Townhouse buyers in emerging areas like North York and Etobicoke

Inventory Improvements: Active listings have increased 15-20% compared to 2024 levels, giving buyers more options and negotiating leverage. Self-employed buyers with solid pre-approvals can negotiate more effectively in this balanced market.

Interest Rate Environment: With Bank of Canada rates stabilizing in the 4.5-5.5% range, mortgage rates have become more predictable. Fixed rates in the high 4% to low 5% range make 30-year amortizations particularly attractive for long-term affordability planning.

Geographic Opportunities Within Toronto

Not all Toronto neighborhoods offer equal value for self-employed buyers working with CMHC-insured mortgages. Strategic areas within the $1 million threshold include:

High-Value Neighborhoods:

- North York (Willowdale, Bayview Village): Condos $650,000-$900,000, excellent transit access

- Etobicoke (Mimico, Long Branch): Townhouses $850,000-$980,000, waterfront proximity

- East York (Leaside borders): Condos and semis $800,000-$950,000, family-friendly

- Scarborough (Agincourt, Milliken): Townhouses $700,000-$850,000, growing amenities

- Downtown Core (smaller units): 1-bedroom condos $600,000-$800,000, urban lifestyle

These areas offer the dual advantage of staying within CMHC insurance limits while providing strong long-term appreciation potential and quality of life.

The K-Shaped Recovery and Self-Employment

Toronto’s economy in 2026 reflects a “K-shaped recovery” where different sectors experience divergent outcomes. Self-employed professionals in technology, professional services, creative industries, and skilled trades have generally maintained or increased incomes, positioning them well for homeownership.

This economic pattern means:

✅ Strong demand for self-employed services continues ✅ Income stability for established self-employed professionals ✅ Growing acceptance of self-employment by lenders ✅ Competitive advantage for buyers with flexible income documentation

However, self-employed buyers must demonstrate this stability through comprehensive documentation and strategic financial planning.

Common Challenges and Solutions for Self-Employed Toronto Buyers

Despite the advantages of extended amortization, self-employed buyers still face unique challenges. Here’s how to address the most common obstacles:

Challenge 1: Variable Income Documentation

Problem: Income fluctuates month-to-month or seasonally, making consistent qualification difficult.

Solutions:

- Use 2-year income averaging to smooth fluctuations

- Highlight growing income trends over the qualification period

- Provide forward contracts demonstrating future income stability

- Consider joint applications with partners who have traditional employment

- Work with lenders experienced in seasonal business cycles

Challenge 2: Recent Business Start or Transition

Problem: Less than 24 months of self-employment history in current business.

Solutions:

- Demonstrate relevant industry experience from previous employment

- Provide comprehensive business plan showing growth trajectory

- Consider waiting until 24-month threshold is met (if timeline permits)

- Explore alternative lender programs with more flexible requirements

- Leverage strong credit scores and larger down payments to offset limited history

Challenge 3: Maximizing Tax Write-Offs vs. Mortgage Qualification

Problem: Aggressive tax deductions reduce reported income, limiting mortgage qualification.

Solutions:

- Plan ahead (2-3 years before home purchase) to balance tax strategy with income reporting

- Work with accountants who understand mortgage qualification requirements

- Utilize income add-backs for depreciation and non-cash deductions

- Consider reducing discretionary write-offs in qualification years

- Maintain detailed records of all business expenses for add-back justification

Challenge 4: Credit History Concerns

Problem: Self-employment sometimes correlates with irregular credit usage or past financial challenges.

Solutions:

- Rebuild credit systematically (secured credit cards, small installment loans)

- Pay all bills on time for 12+ months before applying

- Reduce credit utilization to below 30% of available limits

- Dispute any errors on credit reports immediately

- Consider credit counseling if serious issues exist

Challenge 5: Down Payment Accumulation

Problem: Self-employed income variability makes saving large down payments challenging.

Solutions:

- Automate savings from business accounts to personal savings

- Utilize RRSP Home Buyers’ Plan ($35,000 per person, $70,000 per couple)

- Accept gifted down payments from family (with proper documentation)

- Consider vendor take-back mortgages in private sales

- Explore down payment assistance programs for first-time buyers

For those exploring refinancing or switching lenders, review advantages for self-employed borrowers at renewal to understand all available options.

Long-Term Financial Planning: Beyond the Initial Purchase

The Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026 extends well beyond the initial home purchase. Strategic long-term planning ensures sustainable homeownership:

Amortization Flexibility and Prepayment Strategies

While 30-year amortization provides immediate affordability, self-employed buyers should leverage prepayment privileges during high-income periods:

Typical prepayment options:

- 10-20% annual lump sum payments (penalty-free)

- 10-20% payment increases (reducing amortization)

- Double-up payments on regular payment dates

Strategic approach:

- Make minimum payments during lean business months

- Apply lump sum prepayments during profitable quarters or after large contracts

- Gradually reduce amortization toward 20-25 years as income stabilizes

- Save thousands in interest while maintaining payment flexibility

Renewal Planning for Self-Employed Borrowers

Mortgage renewals present unique opportunities for self-employed buyers. In 2026, typical mortgage terms are 3-5 years, meaning renewal planning should begin early:

Renewal optimization strategies:

- Maintain excellent documentation throughout the mortgage term

- Build strong payment history (never miss payments)

- Increase credit score continuously

- Reduce other debts before renewal

- Shop multiple lenders 120 days before renewal

- Consider switching lenders for better rates or terms

For self-employed borrowers, renewal is often easier than initial qualification because:

- Property equity has increased

- Payment history demonstrates reliability

- Business track record is longer

- Income patterns are better established

Building Long-Term Wealth Through Toronto Real Estate

Toronto real estate has historically appreciated 4-6% annually over long periods. For self-employed buyers, homeownership provides:

Financial benefits:

- Forced savings through mortgage principal reduction

- Appreciation gains (tax-free on principal residences)

- Inflation hedge as property values typically rise with inflation

- Equity access through refinancing for business investment

- Retirement security through paid-off property ownership

Strategic considerations:

- Location selection matters—choose areas with growth potential

- Property type affects appreciation (detached vs. condo)

- Maintenance and improvements preserve and enhance value

- Market timing is less critical over 10+ year horizons

- Leverage carefully—don’t overextend despite approval amounts

Tax Planning Integration

Self-employed Toronto homeowners should integrate real estate ownership into comprehensive tax planning:

Potential strategies:

- Home office deductions (if legitimately used for business)

- RRSP contributions to reduce taxable income while building retirement savings

- TFSA maximization for tax-free investment growth

- Income splitting with spouse/partner where applicable

- Professional tax advice to optimize overall financial position

Conclusion: Seizing the Opportunity in 2026

The Impact of CMHC 30-Year Amortization Rules on Self-Employed Toronto Buyers in 2026 represents a genuine paradigm shift in mortgage accessibility. For the first time in decades, self-employed professionals, freelancers, and entrepreneurs have a clear pathway to Toronto homeownership that acknowledges their unique financial circumstances.

Key Success Factors 🎯

Documentation Excellence: Comprehensive, well-organized financial records demonstrating income stability and business viability are non-negotiable. Start preparing 12-18 months before your intended purchase.

Professional Guidance: Working with mortgage brokers who specialize in self-employed applications and understand income add-backs can mean the difference between approval and rejection.

Strategic Timing: Align your mortgage application with strong income periods, current tax filings, and favorable market conditions to maximize approval odds.

Realistic Expectations: While 30-year amortization dramatically improves affordability, it’s not a magic solution. Responsible borrowing within your means remains essential.

Long-Term Planning: View homeownership as a multi-decade wealth-building strategy, not just a transaction. Leverage prepayment privileges and renewal opportunities to optimize your mortgage over time.

Actionable Next Steps

For self-employed Toronto buyers ready to capitalize on the 2026 opportunities:

- Assess your current financial position using the qualification criteria outlined above

- Engage a qualified accountant to optimize income reporting and identify add-backs

- Connect with a self-employed mortgage specialist for pre-approval assessment

- Calculate your maximum purchase price using 30-year amortization scenarios

- Begin property research in neighborhoods within CMHC insurance limits

- Prepare comprehensive documentation 6-12 months in advance

- Monitor market conditions and interest rate trends for optimal timing

The combination of extended amortization, relaxed documentation requirements, and Toronto’s stabilizing market creates a unique window of opportunity. Self-employed buyers who approach the process strategically, with professional guidance and comprehensive preparation, can successfully navigate the path to homeownership in Canada’s largest and most dynamic real estate market.

The door to Toronto homeownership is open wider than it’s been in years for self-employed professionals. With the right preparation and strategy, 2026 could be the year you turn the key in your own front door.

For additional guidance on securing competitive rates without traditional income verification, explore self-employed mortgage rates in 2026 and learn how to position yourself for the best possible terms.