November 12, 2025

Mortgage News 2025 Toronto: Expert Insights on Rates, Trends, and Market Forecasts

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Mortgage News 2025 Recap

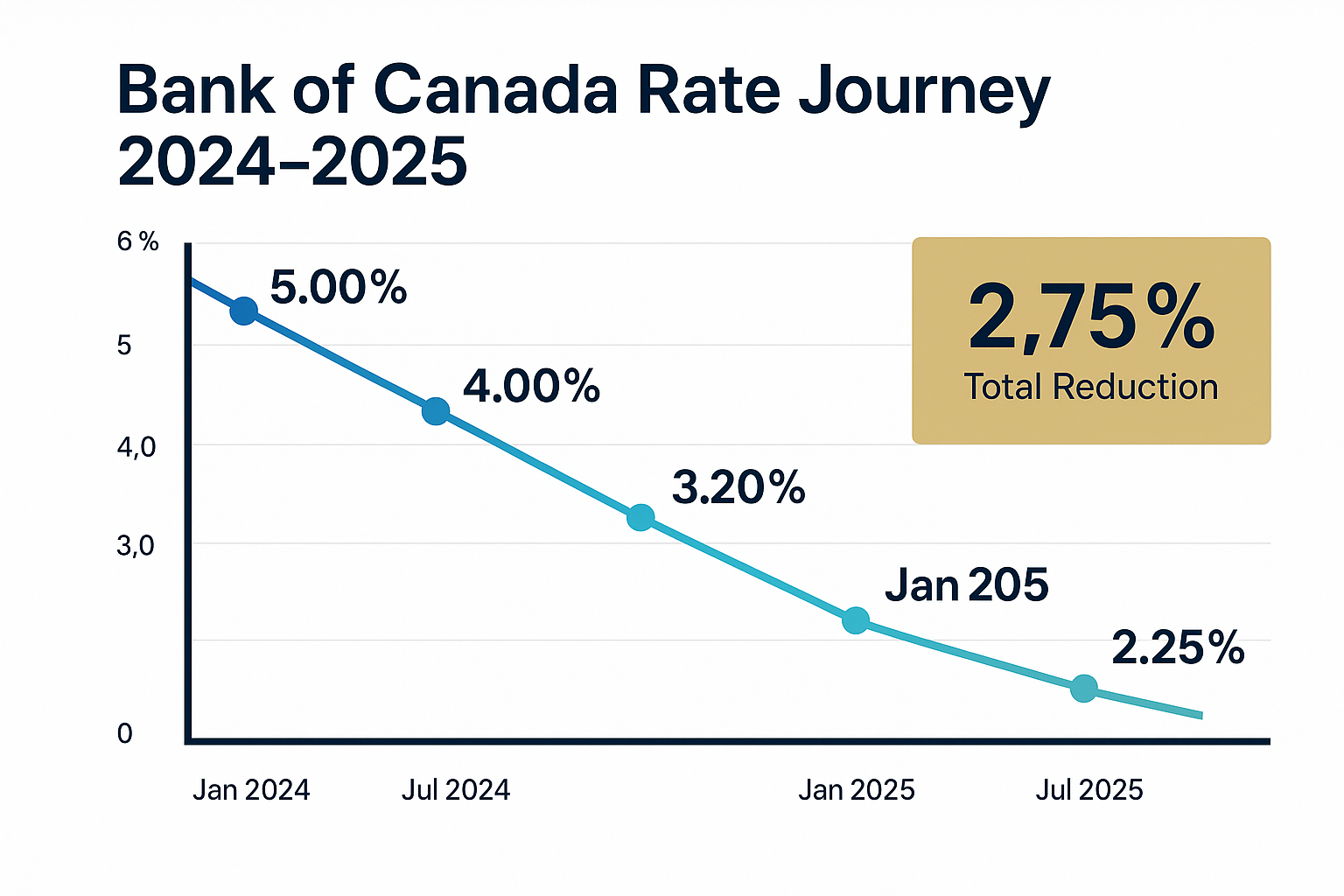

The Toronto real estate market is experiencing a pivotal shift in 2025, and mortgage borrowers are witnessing the most significant rate changes in over two years. After enduring the highest borrowing costs in decades throughout 2024, homeowners and prospective buyers in Canada’s largest city are finally catching a break. The mortgage news 2025 Toronto landscape reveals a dramatic transformation: the Bank of Canada has slashed its policy rate from 5% to 2.25% as of October 29, 2025, creating unprecedented opportunities for both first-time buyers and existing homeowners looking to refinance or switch lenders.

- 🏦 Bank of Canada has reduced rates to 2.25% from 5% in 2024, with another potential 0.25% cut expected December 10, 2025

- 📉 5-year fixed mortgage rates now available at 4.59% at major banks like RBC, with special offers providing additional savings

- 💰 Variable rate mortgages currently at 3.95% (Prime minus 0.50%), forecasted to drop to approximately 4% by year-end

- 🔄 Mortgage switching incentives worth up to $5,700 available before December 31, 2025, making it an ideal time to shop around

- 📊 Variable rates projected to outperform fixed rates if the Bank of Canada continues its rate reduction trajectory through 2026

Understanding the Current Mortgage Rate Environment in Toronto

The mortgage news 2025 Toronto market tells a story of recovery and opportunity. After weathering the storm of aggressive rate hikes throughout 2023 and early 2024, Toronto homeowners are experiencing relief as borrowing costs decline significantly. This shift represents more than just numbers on a page—it translates to real savings for families across the Greater Toronto Area.

The Bank of Canada’s Rate Reduction Strategy

The central bank’s decision to reduce the policy rate from 5% to 2.25% represents one of the most aggressive easing cycles in recent Canadian monetary history. This 2.75 percentage point reduction has occurred over multiple decision meetings throughout 2024 and 2025, with each cut bringing tangible relief to mortgage holders.

Key Rate Timeline:

| Date | Policy Rate | Change | Impact on Mortgages |

|---|---|---|---|

| Early 2024 | 5.00% | Baseline | Highest rates in decades |

| Mid-2024 | 4.50% | -0.50% | Initial relief begins |

| Late 2024 | 3.25% | -1.25% | Significant improvement |

| October 29, 2025 | 2.25% | -1.00% | Current competitive environment |

| December 10, 2025 (projected) | 2.00% | -0.25% | Potential further reduction |

This downward trajectory has created a buyer-friendly environment in Toronto’s traditionally competitive real estate market. Variable rate mortgages, which move in tandem with the Bank of Canada’s policy rate, have become increasingly attractive options for borrowers who believe rates will continue declining.

How Toronto’s Market Differs from National Trends

While the Bank of Canada sets monetary policy for all of Canada, Toronto’s mortgage market exhibits unique characteristics. The city’s robust employment market, continued immigration, and limited housing supply create distinct dynamics that influence how mortgage products perform.

Toronto borrowers typically face:

- Higher property values requiring larger mortgage amounts

- More competitive lending with numerous financial institutions vying for market share

- Greater product variety including specialized programs for condo buyers and investors

- Stricter qualification requirements due to elevated property prices

Fixed vs. Variable Mortgage Rates: The 2025 Toronto Perspective

One of the most critical decisions facing Toronto mortgage borrowers in 2025 involves choosing between fixed and variable rate products. The mortgage news 2025 Toronto data reveals compelling arguments for both options, depending on individual circumstances and risk tolerance.

Current Fixed Rate Offerings

Fixed-rate mortgages provide payment certainty and protection against future rate increases. As of November 2025, major lenders in Toronto are offering competitive fixed-rate products:

RBC Fixed Rate Products (November 2025):

- 1-year fixed: 5.84% (posted rate)

- 3-year fixed: 4.39% (special offer rates available)

- 5-year fixed: 4.59% (special offer rates available)

- 10-year fixed: 6.74% (posted rate)

The 3-year fixed rate at 4.39% has emerged as particularly attractive for Toronto borrowers seeking certainty through 2026 without committing to the longer 5-year term. This product sits 0.25% lower than comparable variable rates and provides an excellent middle ground for those anticipating economic uncertainty.

Variable Rate Mortgage Advantages

Variable rate mortgages in Toronto currently offer rates based on the Prime Rate minus a discount. With the current Prime Rate at 4.45%, discounts ranging from 0.5% to 1.5% are available across major Canadian lenders.

RBC Variable Rate Example:

- Prime Rate: 4.45%

- Discount: -0.50%

- Effective Rate: 3.95% (for closed 25-year amortization)

The appeal of variable rates in 2025 centers on the expectation that the Bank of Canada will continue reducing rates. Mortgage forecasters project variable rates declining to approximately 4% by the end of 2025, with modest downward trends continuing into 2026.

“Variable rate mortgages are projected to outperform 5-year fixed mortgages if the Bank of Canada continues rate reductions through 2026.” — Canadian Mortgage Trend Analysis, 2025

Making the Right Choice for Your Situation

Toronto borrowers should consider several factors when choosing between fixed and variable:

Choose Fixed Rates If:

- ✅ You prioritize budget certainty and stable payments

- ✅ You believe rates have bottomed and will rise soon

- ✅ You have limited financial flexibility for payment increases

- ✅ You’re purchasing at the upper limit of your affordability

- ✅ You plan to stay in the property for the full term

Choose Variable Rates If:

- ✅ You believe the Bank of Canada will continue cutting rates

- ✅ You can handle potential payment fluctuations

- ✅ You have financial flexibility and emergency savings

- ✅ You’re comfortable with calculated financial risk

- ✅ You want to maximize potential savings over the term

Mortgage News 2025 Toronto: Special Offers and Incentives

The competitive Toronto mortgage market has spawned numerous special offers and incentives as lenders battle for market share. Understanding these promotions can translate to thousands of dollars in savings.

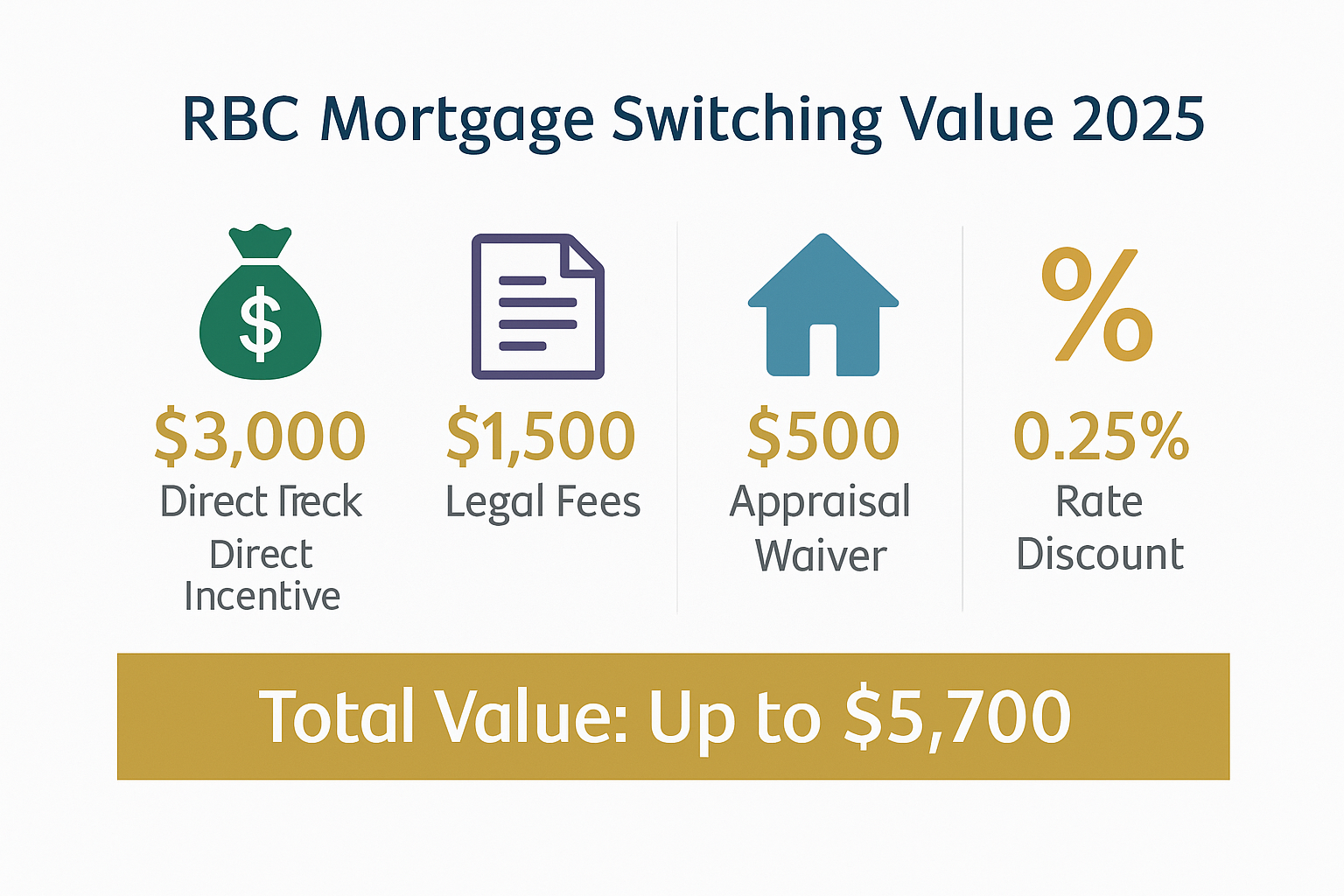

RBC Mortgage Switching Incentive Program

One of the most significant promotions in the mortgage news 2025 Toronto landscape is RBC’s mortgage switching incentive, offering up to $5,700 in value for customers who switch their mortgage before December 31, 2025.

Program Components:

| Benefit | Value | Eligibility |

|---|---|---|

| Cash-back incentive | Up to $3,000 | Minimum mortgage amount |

| Legal fee coverage | Up to $1,500 | Standard switching process |

| Appraisal fee waiver | $300-$500 | All qualified applicants |

| Rate discount | 0.10-0.25% | Purchase and switch transactions |

| Total Potential Value | $5,700+ | Combined benefits |

This incentive makes 2025 an optimal time for Toronto homeowners to evaluate their current mortgage arrangements. Many borrowers who locked in at higher rates in 2023 or early 2024 can now switch to significantly lower rates while pocketing substantial cash incentives.

Special Offer Rates vs. Posted Rates

Understanding the difference between posted rates and special offer rates is crucial for Toronto borrowers. Posted rates serve as benchmark figures that lenders advertise publicly, while special offer rates represent the actual competitive rates available to qualified borrowers.

The gap between these rates can be substantial:

- Posted 5-year fixed: 6.99%

- Special offer 5-year fixed: 4.59%

- Savings: 2.40 percentage points

On a $600,000 mortgage (typical for Toronto condos), this difference translates to approximately $850 per month in payment savings—or over $10,000 annually.

First-Time Home Buyer Programs in Toronto

Toronto first-time buyers have access to specialized programs and incentives in 2025:

Federal Programs:

- 🏠 First Home Savings Account (FHSA): Tax-free savings up to $40,000

- 💵 Home Buyers’ Plan: Withdraw up to $35,000 from RRSP

- 📋 First-Time Home Buyer Incentive: Shared-equity mortgage (income restrictions apply)

Provincial Programs (Ontario):

- 💰 Land Transfer Tax Rebate: Up to $4,000 for first-time buyers

- 🏘️ Ontario Housing Programs: Various municipal initiatives

Lender-Specific Programs:

- Lower down payment options (5% minimum)

- Reduced mortgage insurance premiums

- Flexible qualification criteria

- Extended amortization periods (up to 30 years for insured mortgages)

Bond Yields and Their Impact on Toronto Mortgage Rates

While the Bank of Canada’s policy rate directly influences variable mortgage rates, fixed mortgage rates are primarily determined by bond yields. Understanding this relationship is essential for interpreting mortgage news 2025 Toronto and making informed borrowing decisions.

The Bond Yield Connection

Five-year Government of Canada bond yields serve as the benchmark for 5-year fixed mortgage rates. Lenders typically price their fixed-rate products at a spread above the bond yield to cover costs and profit margins.

October 2025 Bond Market Conditions:

- 5-year bond yield: 2.7%

- Typical lender spread: 1.8-2.0%

- Resulting mortgage rate: 4.5-4.7%

- Actual RBC special offer: 4.59%

The bond yield at 2.7% in October 2025 creates potential upward pressure on 5-year fixed mortgage rates. If bond yields rise due to inflation concerns or economic growth, fixed mortgage rates could increase even if the Bank of Canada continues cutting its policy rate.

Why Bond Yields Matter to Toronto Borrowers

Toronto mortgage applicants should monitor bond yields because:

- Early warning system: Bond yields often move before mortgage rates change

- Rate lock timing: Understanding yield trends helps optimize rate lock decisions

- Fixed vs. variable decision: Rising yields favor variable rates; falling yields favor fixed rates

- Renewal strategy: Existing mortgage holders can time renewals based on yield trends

Current Bond Market Outlook

Financial analysts project that 5-year bond yields will remain in the 2.5-3.0% range through late 2025 and early 2026, assuming:

- Inflation remains controlled near the 2% target

- Economic growth continues at moderate pace

- No major global economic disruptions occur

- Bank of Canada maintains gradual easing approach

This relatively stable outlook suggests fixed mortgage rates in Toronto will likely remain in the 4.3-4.8% range for the remainder of 2025, barring unexpected economic developments.

Mortgage Qualification Rules and Stress Test Requirements

Toronto’s elevated property prices make mortgage qualification particularly challenging. The federal mortgage stress test ensures borrowers can handle potential rate increases, but it also limits purchasing power in expensive markets like Toronto.

The Mortgage Stress Test Explained

All federally regulated lenders must qualify borrowers at the higher of:

- The contract rate plus 2%, OR

- The Bank of Canada’s benchmark qualifying rate (currently 5.25%)

Practical Example:

A Toronto buyer securing a 5-year fixed rate at 4.59% must qualify at:

- Contract rate + 2% = 6.59%

- Benchmark rate = 5.25%

- Qualification rate: 6.59% (the higher of the two)

This means a household earning $120,000 annually might qualify for:

- Without stress test: $650,000 mortgage

- With stress test: $520,000 mortgage

- Reduction in purchasing power: $130,000

Strategies to Improve Qualification

Toronto borrowers can enhance their qualification prospects through:

Income Optimization:

- 📊 Include all eligible income sources (bonuses, commissions, rental income)

- 💼 Add a co-borrower or guarantor

- 📈 Demonstrate consistent income history (2+ years preferred)

- 🏢 Provide comprehensive employment verification

Debt Management:

- 💳 Pay down high-interest credit cards

- 🚗 Eliminate or reduce car loans

- 📱 Cancel unused credit facilities

- 🔄 Consolidate debts to lower payments

Down Payment Strategies:

- 🏠 Increase down payment to reduce mortgage amount

- 👨👩👧 Accept gift funds from family members

- 💰 Utilize RRSP Home Buyers’ Plan

- 📊 Leverage First Home Savings Account

Alternative Lender Options

Toronto borrowers who don’t qualify with major banks have alternatives:

Credit Unions:

- More flexible qualification criteria

- Relationship-based lending approach

- Competitive rates for members

- Local decision-making authority

Mortgage Finance Companies (MFCs):

- Specialized programs for self-employed

- Alternative income verification methods

- Higher rates but easier qualification

- Bridge financing options

Private Lenders:

- Asset-based lending (property value focus)

- Minimal income verification

- Short-term solutions (1-2 years)

- Higher rates (7-12% typical)

Toronto Real Estate Market Trends Affecting Mortgage Demand

The mortgage news 2025 Toronto landscape cannot be separated from broader real estate market conditions. Property values, inventory levels, and buyer sentiment all influence mortgage product demand and pricing.

Current Toronto Housing Market Indicators

Average Property Prices (Q4 2025):

- Detached homes: $1,450,000

- Semi-detached: $1,125,000

- Townhouses: $875,000

- Condos: $685,000

Market Activity Metrics:

- Sales volume: Up 18% year-over-year

- New listings: Up 12% year-over-year

- Average days on market: 22 days

- Sale-to-list price ratio: 99.5%

The declining mortgage rates have stimulated renewed buyer activity across Toronto, particularly in the condo segment where first-time buyers dominate. The combination of lower rates and modest price corrections from 2024 peaks has created improved affordability conditions.

Condo Market Dynamics

Toronto’s condo market exhibits unique characteristics affecting mortgage demand:

Positive Factors:

- ✅ Lower entry price points ($500,000-$750,000 range)

- ✅ Strong rental demand supporting investor activity

- ✅ New supply concentrated in transit-accessible locations

- ✅ Maintenance fees stabilizing after 2024 increases

Challenges:

- ⚠️ Higher property taxes on investment properties

- ⚠️ Stricter rental regulations limiting investor appeal

- ⚠️ Oversupply concerns in some submarkets

- ⚠️ Special assessments for aging buildings

Suburban vs. Urban Mortgage Trends

The mortgage news 2025 Toronto story differs between urban core and suburban markets:

Downtown Toronto (Core):

- Preference for variable rates (anticipating further cuts)

- Shorter mortgage terms (3-year products popular)

- Higher proportion of investor mortgages

- More sophisticated borrowers shopping multiple lenders

Suburban GTA (905 Region):

- Preference for fixed rates (budget certainty)

- Longer mortgage terms (5-year products dominant)

- Higher proportion of family purchases

- Greater reliance on mortgage brokers

Working with Mortgage Brokers vs. Direct Lenders

Toronto borrowers face an important decision: work with a mortgage broker or approach lenders directly. Each option offers distinct advantages in the current rate environment.

Mortgage Broker Advantages

Benefits of Using a Broker:

- Access to multiple lenders: Brokers work with 20-40+ lenders including banks, credit unions, and alternative lenders

- Rate shopping efficiency: One application reaches multiple lenders simultaneously

- Expert guidance: Professional advice on product selection and qualification strategies

- No direct cost: Lenders pay broker commissions; clients pay nothing

- Specialized expertise: Access to niche products and programs

- Negotiation leverage: Brokers can often secure better rates and terms

When Brokers Excel:

- Complex income situations (self-employed, commissioned)

- Challenging credit histories

- Unique property types (rural, mixed-use)

- Time-sensitive transactions

- Maximum rate optimization desired

Direct Lender Advantages

Benefits of Going Direct:

- Relationship banking: Existing customers may receive preferential treatment

- Bundled products: Package mortgages with banking, investments, and insurance

- Loyalty rewards: Long-term customer discounts and benefits

- Simplified process: Single point of contact for all financial needs

- Branch access: Face-to-face service for those who prefer it

When Direct Lending Works:

- Straightforward income and credit

- Existing relationship with preferred lender

- Loyalty rewards or discounts available

- Comfort with single-lender approach

- Time to shop multiple banks independently

The Hybrid Approach

Many savvy Toronto borrowers employ a hybrid strategy:

- Research independently: Understand current rates and products

- Consult a broker: Get professional assessment and multiple quotes

- Approach preferred bank: Request to match or beat broker’s best offer

- Make informed decision: Choose based on rate, terms, and relationship value

This approach ensures borrowers secure competitive rates while maintaining flexibility in lender selection.

Refinancing and Renewal Strategies for 2025

Existing Toronto homeowners represent a significant portion of mortgage activity in 2025. With rates declining substantially from 2023-2024 peaks, refinancing and renewal strategies deserve careful consideration.

When Refinancing Makes Sense

Compelling Refinancing Scenarios:

Scenario 1: Rate Arbitrage

- Current mortgage: 5.8% (locked in 2023)

- Available rate: 4.59% (2025 market)

- Savings: 1.21 percentage points

On a $500,000 mortgage with 20 years remaining:

- Current monthly payment: $3,485

- New monthly payment: $3,145

- Monthly savings: $340

- Annual savings: $4,080

If penalty to break current mortgage is $8,000, the payback period is less than 2 years—making refinancing financially attractive.

Scenario 2: Debt Consolidation

- Mortgage: $400,000 at 4.59%

- Credit cards: $30,000 at 19.99%

- Car loan: $20,000 at 7.5%

- Refinanced mortgage: $450,000 at 4.89%

This strategy eliminates high-interest debt, reduces total monthly payments, and potentially improves credit scores—though it extends debt repayment timelines.

Calculating Refinancing Penalties

Toronto homeowners must understand prepayment penalties before refinancing:

Fixed-Rate Mortgages:

Penalty = Greater of:

- Three months’ interest, OR

- Interest Rate Differential (IRD)

IRD calculations can be substantial, especially when:

- Significant time remains on the term

- Current rates are much lower than contract rate

- Original mortgage was at a deeply discounted rate

Variable-Rate Mortgages:

Penalty = Three months’ interest (typically much lower than fixed penalties)

Example Penalty Calculation:

$500,000 mortgage at 5.8% with 3 years remaining:

- Three months’ interest: $7,250

- IRD calculation: $18,500

- Penalty owed: $18,500 (the greater amount)

Borrowers should request penalty calculations from current lenders before proceeding with refinancing.

Renewal Optimization Strategies

Approximately one-third of Toronto mortgages renew annually. The 2025 environment offers unique opportunities for renewal optimization.

Renewal Best Practices:

- Start early: Begin shopping 120 days before maturity

- Don’t auto-renew: Lenders’ initial offers are rarely their best

- Shop competitors: Obtain at least 3 competitive quotes

- Negotiate aggressively: Use competing offers as leverage

- Consider term length: Match term to financial goals and rate outlook

- Review features: Ensure prepayment privileges meet future needs

2025 Renewal Scenarios:

| Original Term | Original Rate | Renewal Rate | Monthly Savings ($500K) |

|---|---|---|---|

| 2020 5-year | 2.49% | 4.59% | -$550 (increase) |

| 2022 5-year | 4.89% | 4.59% | $90 |

| 2023 5-year | 6.29% | 4.59% | $485 |

Borrowers who locked in during 2020-2021’s ultra-low rates will face payment increases, making budgeting and financial planning essential.

The December 2025 Bank of Canada Decision: What to Expect

The mortgage news 2025 Toronto landscape will be significantly influenced by the Bank of Canada’s next policy rate decision scheduled for December 10, 2025. Market analysts anticipate a potential additional 0.25% reduction, which would bring the policy rate to 2.00%.

Factors Influencing the December Decision

Arguments for Further Rate Cuts:

- 📉 Inflation control: CPI trending near 2% target

- 🏠 Housing market stability: No signs of overheating

- 💼 Employment concerns: Modest softening in job market

- 🌍 Global uncertainty: International economic headwinds

- 💰 Consumer debt levels: High household debt requiring relief

Arguments Against Further Cuts:

- 📈 Economic resilience: GDP growth exceeding expectations

- 💵 Currency concerns: CAD weakness vs. USD

- 🏦 Financial stability: Preventing excessive risk-taking

- 🔄 Lag effects: Previous cuts still working through economy

- ⚖️ Neutral rate proximity: Approaching estimated neutral rate of 2.25-2.75%

Impact on Toronto Mortgage Borrowers

If the Bank Cuts to 2.00%:

Variable rate mortgages would immediately benefit:

- Current Prime Rate: 4.45%

- New Prime Rate: 4.20%

- Variable mortgage (Prime – 0.50%): 3.70%

This would make variable rates approximately 0.90 percentage points lower than 5-year fixed rates, creating strong incentive for variable rate selection.

If the Bank Holds at 2.25%:

The pause would signal:

- Confidence in current economic trajectory

- Reduced urgency for additional stimulus

- Potential floor for near-term rate cuts

- Increased attractiveness of fixed rates

Positioning Your Mortgage Strategy

For Pending Purchases:

If closing before December 10:

- Consider rate holds (typically 90-120 days)

- Evaluate both fixed and variable options

- Build flexibility into closing timelines

If closing after December 10:

- Wait for decision before finalizing rate choice

- Maintain backup options with multiple lenders

- Consider variable rates if cut materializes

For Renewals:

Maturing before December 10:

- Negotiate aggressively using potential cut as leverage

- Consider shorter terms (6-month, 1-year) to capture future cuts

- Ensure prepayment privileges allow refinancing if rates drop further

Maturing after December 10:

- Await decision before committing to term length

- Prepare multiple scenarios (cut vs. hold)

- Maintain communication with lender/broker

Mortgage Technology and Digital Application Trends

The mortgage news 2025 Toronto story includes significant technological advancement. Digital mortgage platforms, AI-powered qualification tools, and streamlined application processes are transforming how Toronto borrowers secure financing.

Digital Mortgage Platforms

Major lenders now offer fully digital mortgage experiences:

Features of Modern Digital Platforms:

- 📱 Mobile-first applications: Complete entire process on smartphone

- 🤖 AI-powered pre-qualification: Instant approval estimates

- 📄 Document upload: Photo-based income and asset verification

- ✍️ Electronic signatures: No paper documentation required

- 📊 Real-time status tracking: Monitor application progress

- 💬 Chatbot support: 24/7 automated assistance

Benefits for Toronto Borrowers:

- ⏱️ Speed: Applications completed in 15-30 minutes

- 🏠 Convenience: Apply from home, office, or showing

- 🔒 Security: Bank-level encryption and data protection

- 📈 Transparency: Clear visibility into requirements and timelines

- 🎯 Accuracy: Reduced errors through automated data validation

Open Banking and Mortgage Applications

Canada’s open banking framework is revolutionizing mortgage qualification:

How Open Banking Works:

- Borrower grants secure access to banking data

- Lender retrieves income, employment, and savings information directly

- Automated verification replaces manual document review

- Faster decisions with reduced documentation burden

Advantages:

- ✅ Eliminates need for pay stubs and tax returns

- ✅ Reduces application time from days to hours

- ✅ Improves accuracy through direct data access

- ✅ Enhances fraud prevention

- ✅ Streamlines self-employed income verification

Artificial Intelligence in Mortgage Underwriting

AI and machine learning are transforming mortgage underwriting in Toronto:

AI Applications:

- Credit risk assessment: More nuanced evaluation beyond credit scores

- Property valuation: Automated comparative market analysis

- Fraud detection: Pattern recognition identifying suspicious applications

- Income verification: Advanced analysis of non-traditional income

- Approval prediction: Instant feedback on qualification likelihood

Impact on Borrowers:

Toronto applicants with non-traditional profiles benefit most from AI underwriting:

- Self-employed individuals

- Gig economy workers

- Recent immigrants

- Those with limited credit history

- Borrowers with previous credit issues

Regional Considerations: GTA Submarkets and Mortgage Patterns

The Greater Toronto Area encompasses diverse submarkets, each with unique mortgage patterns and preferences that influence the mortgage news 2025 Toronto narrative.

Downtown Toronto Core

Market Characteristics:

- Average property price: $850,000 (condos)

- Typical down payment: 20-25%

- Preferred mortgage term: 3-year fixed or variable

- Investor percentage: 35-40% of purchases

Mortgage Preferences:

- Higher adoption of variable rates

- Shorter terms for flexibility

- Greater use of mortgage brokers

- More sophisticated rate shopping

- Frequent use of HELOC products

North York and Scarborough

Market Characteristics:

- Average property price: $950,000 (mixed housing)

- Typical down payment: 20%

- Preferred mortgage term: 5-year fixed

- First-time buyer percentage: 45-50%

Mortgage Preferences:

- Conservative fixed-rate selection

- Longer amortization periods

- High use of first-time buyer programs

- Family-focused product features

- Emphasis on payment stability

Mississauga and Brampton

Market Characteristics:

- Average property price: $1,100,000 (detached)

- Typical down payment: 15-20%

- Preferred mortgage term: 5-year fixed

- Multi-generational household percentage: 30%

Mortgage Preferences:

- Strong preference for fixed rates

- Multiple income sources common

- Higher use of extended families for down payments

- Preference for direct lender relationships

- Emphasis on long-term payment certainty

Vaughan and Markham

Market Characteristics:

- Average property price: $1,350,000 (detached)

- Typical down payment: 25-30%

- Preferred mortgage term: 5-year fixed

- Investment property percentage: 25%

Mortgage Preferences:

- Mix of fixed and variable rates

- Larger mortgages requiring jumbo products

- Sophisticated financial planning

- Multiple property portfolios common

- Higher use of private banking services

Tax Implications and Mortgage Interest Deductibility

Understanding tax considerations is essential for Toronto mortgage borrowers, particularly investors and those using creative financing strategies.

Principal Residence Mortgage Interest

For owner-occupied properties, mortgage interest is not tax-deductible in Canada. This differs from the United States and affects financial planning:

Implications:

- Higher effective borrowing costs compared to tax-deductible scenarios

- Greater emphasis on mortgage paydown strategies

- Importance of comparing after-tax investment returns vs. mortgage prepayment

- Consideration of Smith Maneuver for tax optimization

Investment Property Mortgage Interest

Rental property mortgage interest is tax-deductible against rental income:

Example:

- Rental property mortgage: $500,000 at 4.59%

- Annual interest: $22,950

- Rental income: $36,000

- Taxable rental income: $13,050 (after interest deduction)

Additional Deductible Expenses:

- Property taxes

- Insurance premiums

- Maintenance and repairs

- Property management fees

- Condo fees (if applicable)

The Smith Maneuver Strategy

The Smith Maneuver converts non-deductible mortgage interest into tax-deductible investment loan interest:

How It Works:

- Establish readvanceable mortgage with HELOC component

- Make regular mortgage payments

- As principal is paid down, borrow equivalent amount from HELOC

- Invest HELOC funds in income-producing investments

- Deduct HELOC interest as investment expense

Requirements:

- Disciplined investment approach

- Comfort with investment risk

- Sufficient income to support dual borrowing

- Long-term commitment (10+ years)

Potential Benefits:

- Tax deductions on interest payments

- Accelerated wealth building through investments

- Eventual tax-free principal residence sale

Risks:

- Investment losses possible

- Increased total debt load

- Complexity requiring professional advice

- CRA scrutiny if not properly structured

Mortgage Insurance Requirements and Costs

Toronto’s elevated property prices often push borrowers into mortgage insurance requirements. Understanding these costs is crucial for accurate budgeting.

When Mortgage Insurance Is Required

CMHC/Genworth/Canada Guaranty insurance is mandatory when:

- Down payment is less than 20% of purchase price

- Property price is under $1,000,000

- Borrower meets qualification criteria

Insurance Premium Rates (2025):

| Down Payment | Loan-to-Value | Premium Rate | Premium on $500K |

|---|---|---|---|

| 5-9.99% | 90.01-95% | 4.00% | $20,000 |

| 10-14.99% | 85.01-90% | 3.10% | $15,500 |

| 15-19.99% | 80.01-85% | 2.80% | $14,000 |

| 20%+ | 80% or less | 0% | $0 |

Strategies to Avoid or Minimize Insurance Costs

Option 1: Increase Down Payment to 20%

Advantages:

- ✅ Eliminate insurance premium entirely

- ✅ Lower monthly payments

- ✅ Build equity faster

- ✅ Access to wider range of lenders

Challenges:

- ⚠️ Requires significant additional savings

- ⚠️ Delays purchase timeline

- ⚠️ May miss market opportunities

Option 2: Gifted Down Payment

Many Toronto first-time buyers receive down payment gifts from family:

Requirements:

- Gift letter confirming non-repayable nature

- Documentation of gift source

- Demonstration that gift is genuine (not disguised loan)

- Lender-specific policies vary

Option 3: Blended Mortgage Strategy

For properties over $1,000,000:

- First mortgage: 80% of first $1M (uninsured)

- Second mortgage: 20% of amount over $1M

- Avoids insurance while minimizing down payment

Example:

- Property price: $1,200,000

- First mortgage: $800,000 (80% of $1M)

- Second mortgage: $240,000 (60% of $200K over $1M)

- Down payment required: $160,000 (13.3%)

Preparing for Your Mortgage Application: Essential Documentation

Successful Toronto mortgage applications require thorough documentation. Being prepared accelerates approval and demonstrates financial responsibility.

Employment and Income Verification

Salaried Employees:

Required documents:

- ✅ Recent pay stubs (latest 2-3)

- ✅ T4 slips (previous 2 years)

- ✅ Notice of Assessment (previous 2 years)

- ✅ Employment letter confirming position, salary, tenure

- ✅ Year-to-date earnings statement

Self-Employed Borrowers:

Required documents:

- ✅ Notice of Assessment (previous 2 years minimum)

- ✅ T1 Generals (complete tax returns)

- ✅ Financial statements (if incorporated)

- ✅ Business license and registration

- ✅ Proof of business continuity (contracts, invoices)

Commissioned or Bonus Income:

Required documents:

- ✅ Two-year history of commission/bonus income

- ✅ Employer letter confirming compensation structure

- ✅ T4 slips showing bonus/commission breakdown

- ✅ Recent pay stubs

- ✅ Employment contract if applicable

Asset and Down Payment Verification

Savings and Investments:

Required documents:

- ✅ Bank statements (90 days minimum)

- ✅ Investment account statements

- ✅ RRSP/TFSA statements

- ✅ Gift letter (if applicable)

- ✅ Sale of property proceeds (if applicable)

Source of Down Payment:

Lenders scrutinize down payment sources to ensure:

- Funds are legitimate and documented

- No undisclosed borrowing occurred

- Sufficient reserves remain after closing

- Gift funds are properly documented

Credit and Debt Documentation

Credit Requirements:

- ✅ Credit score: 680+ for best rates (600+ minimum for insured)

- ✅ Clean payment history (no recent late payments)

- ✅ Reasonable credit utilization (under 30%)

- ✅ Established credit history (2+ years preferred)

Debt Documentation:

Required for all debts:

- ✅ Credit card statements

- ✅ Auto loan details

- ✅ Student loan balances

- ✅ Line of credit statements

- ✅ Other mortgage or loan obligations

Property Documentation

Purchase Transactions:

- ✅ Accepted offer to purchase

- ✅ MLS listing details

- ✅ Property tax assessment

- ✅ Condo status certificate (if applicable)

- ✅ Home inspection report (recommended)

Refinance Transactions:

- ✅ Current mortgage statement

- ✅ Property tax bill

- ✅ Recent appraisal (if available)

- ✅ Condo financial statements (if applicable)

- ✅ Proof of property insurance

Common Mortgage Mistakes Toronto Borrowers Should Avoid

Learning from others’ errors can save thousands of dollars and significant stress. These common mistakes plague Toronto mortgage applicants regularly.

Mistake #1: Failing to Get Pre-Approved

The Error:

Beginning property search without mortgage pre-approval.

Consequences:

- Wasted time viewing unaffordable properties

- Disappointment when qualifying for less than expected

- Lost opportunities in competitive bidding situations

- Delayed closing timelines

Solution:

Obtain full pre-approval (not just pre-qualification) before serious house hunting. This involves:

- Complete application submission

- Full documentation review

- Credit check and verification

- Conditional approval letter

- Rate hold (90-120 days typical)

Mistake #2: Ignoring the Total Cost of Homeownership

The Error:

Focusing exclusively on mortgage payments while ignoring other ownership costs.

Consequences:

- Budget strain from unexpected expenses

- Inability to handle emergency repairs

- Forced sale due to financial pressure

Toronto Homeownership Costs Beyond Mortgage:

| Expense Category | Monthly Cost (Estimate) |

|---|---|

| Property taxes | $400-$800 |

| Home insurance | $150-$300 |

| Utilities | $200-$400 |

| Maintenance reserve | $200-$500 |

| Condo fees (if applicable) | $400-$800 |

| Total Additional | $1,350-$2,800 |

Solution:

Budget for total housing costs at 35-40% of gross income maximum, not just mortgage payments.

Mistake #3: Choosing Rate Over Features

The Error:

Selecting mortgage based solely on lowest rate while ignoring critical features.

Consequences:

- Expensive penalties when circumstances change

- Inability to make lump sum payments

- Restricted portability when moving

- Limited refinancing options

Important Mortgage Features:

- Prepayment privileges: 10-20% annual lump sum typical

- Payment flexibility: Ability to increase payments

- Portability: Transfer mortgage to new property

- Assumability: Allow buyer to take over mortgage

- Penalty calculation: Understand break costs

- Conversion options: Switch from variable to fixed

Solution:

Evaluate mortgages holistically, considering both rate and features aligned with likely future needs.

Mistake #4: Maxing Out Borrowing Capacity

The Error:

Borrowing the maximum amount for which you qualify.

Consequences:

- No financial cushion for emergencies

- Vulnerability to income disruptions

- Inability to handle rate increases

- Stress and reduced quality of life

Solution:

Borrow conservatively based on comfortable payment levels, not maximum qualification. Consider:

- Future income changes (parental leave, career changes)

- Interest rate increases at renewal

- Lifestyle goals beyond housing

- Emergency fund maintenance

- Retirement savings continuation

Mistake #5: Neglecting to Shop Around

The Error:

Accepting the first mortgage offer without comparison shopping.

Consequences:

- Overpaying by 0.10-0.50% in rate

- Missing better features and terms

- Losing thousands in potential savings

Example:

On a $600,000 mortgage over 25 years:

- Rate difference: 0.25%

- Monthly payment difference: $85

- Total 5-year cost difference: $5,100

Solution:

Obtain minimum three competitive quotes from:

- Your primary bank

- At least one competing bank

- A mortgage broker with access to multiple lenders

Future Outlook: Mortgage Predictions for 2026 and Beyond

While the mortgage news 2025 Toronto landscape shows improvement, understanding longer-term trends helps borrowers make strategic decisions.

Interest Rate Projections

Consensus Forecast for 2026:

Bank of Canada Policy Rate:

- Current (October 2025): 2.25%

- End of 2025 projection: 2.00%

- Mid-2026 projection: 1.75-2.00%

- End of 2026 projection: 2.00-2.25%

5-Year Fixed Mortgage Rates:

- Current: 4.59%

- End of 2025 projection: 4.30-4.60%

- 2026 range projection: 4.00-4.75%

Variable Mortgage Rates:

- Current: 3.95%

- End of 2025 projection: 3.70-4.00%

- 2026 range projection: 3.50-4.25%

Toronto Real Estate Market Outlook

Price Projections:

Most analysts forecast modest appreciation in Toronto property values:

- 2025 full-year: +3% to +5%

- 2026 projection: +4% to +7%

- 2027 projection: +3% to +6%

Factors Supporting Price Growth:

- 📈 Strong immigration continuing

- 🏗️ Limited new supply relative to demand

- 💼 Robust employment market

- 🏦 Improved mortgage affordability

- 🌍 Toronto’s global city status

Factors Limiting Price Growth:

- 📊 Elevated interest rates (historical context)

- 💰 Affordability constraints

- 🏢 Work-from-home reducing downtown demand

- 📉 Economic uncertainty

- 🏘️ Increased condo supply

Regulatory Changes on the Horizon

Potential Policy Developments:

Mortgage Qualification:

- Possible stress test adjustments

- Enhanced verification for self-employed

- Tighter rules for investment properties

- Changes to amortization limits

Housing Supply Initiatives:

- Zoning reform encouraging density

- Incentives for purpose-built rentals

- Foreign buyer restrictions continuation

- Vacant home tax expansion

Consumer Protection:

- Enhanced mortgage disclosure requirements

- Improved prepayment penalty transparency

- Stronger regulation of alternative lenders

- Open banking implementation

Conclusion: Navigating the 2025 Toronto Mortgage Landscape

The mortgage news 2025 Toronto narrative is overwhelmingly positive for borrowers. With the Bank of Canada’s aggressive rate cutting from 5% to 2.25%, Toronto homeowners and prospective buyers are experiencing the most favorable mortgage conditions in over two years. Five-year fixed rates at 4.59%, variable rates at 3.95%, and the potential for further reductions create genuine opportunities for both purchases and refinancing.

However, success in this environment requires informed decision-making. The choice between fixed and variable rates, understanding qualification requirements, evaluating lender options, and timing decisions around Bank of Canada announcements all significantly impact financial outcomes.

Actionable Next Steps

For Prospective Buyers:

- Get pre-approved immediately to understand borrowing capacity and lock in current rates

- Compare at least three lenders to ensure competitive rate and favorable terms

- Build comprehensive budget including all homeownership costs beyond mortgage

- Monitor Bank of Canada decision on December 10, 2025, before finalizing rate choice

- Consider variable rates if comfortable with payment fluctuations and believe rates will continue declining

For Current Homeowners:

- Calculate refinancing economics including penalties and potential savings

- Request penalty quote from current lender if considering early refinancing

- Start renewal shopping 120 days before maturity to maximize negotiating leverage

- Evaluate mortgage switching incentives like RBC’s $5,700 offer before December 31, 2025

- Review mortgage features to ensure alignment with current and future needs

For All Borrowers:

- Stay informed about economic indicators and Bank of Canada communications

- Maintain strong credit to qualify for best rates and terms

- Build emergency reserves equal to 3-6 months of housing costs

- Consult professionals including mortgage brokers, financial planners, and tax advisors

- Think long-term aligning mortgage decisions with comprehensive financial goals

The Toronto mortgage market in 2025 offers genuine opportunities for those who approach it strategically. By understanding the current environment, avoiding common mistakes, and making informed decisions aligned with personal circumstances, borrowers can secure favorable financing that supports their homeownership goals while building long-term financial security.

The combination of declining rates, competitive lender offerings, and improving market conditions creates a window of opportunity that savvy Toronto borrowers should not overlook. Whether purchasing your first home, upgrading to accommodate a growing family, or optimizing existing mortgage arrangements, 2025 presents conditions that favor informed, decisive action.