February 7, 2026

Non-QM Loans for Self-Employed Borrowers: Your Guide to Bank Statement Mortgages in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

For self-employed professionals, freelancers, and business owners, securing a mortgage has traditionally felt like navigating an obstacle course. Tax returns that strategically minimize income through business deductions—a smart financial move—suddenly become a liability when applying for a home loan. Traditional lenders want to see high reported income, but savvy entrepreneurs know that maximizing deductions is key to reducing tax burdens. This fundamental mismatch has left countless self-employed borrowers frustrated and shut out of homeownership.

Enter Non-QM Loans for Self-Employed Borrowers: Your Guide to Bank Statement Mortgages in 2026—a financing solution that’s rapidly transforming the mortgage landscape. These alternative lending products recognize that bank deposits, not tax returns, provide a more accurate picture of a self-employed person’s true earning power. As 2026 unfolds, the non-QM market is experiencing disciplined expansion, with bank statement loans leading the charge as the preferred option for entrepreneurs and independent contractors seeking mortgage approval.

Key Takeaways

✅ Non-QM loans accounted for approximately 9% of mortgage activity at the end of 2025, representing significant growth in alternative lending options for self-employed borrowers[6]

✅ Bank statement mortgages allow qualification using 2-24 months of bank deposits instead of tax returns, solving the income documentation challenge for self-employed professionals[4]

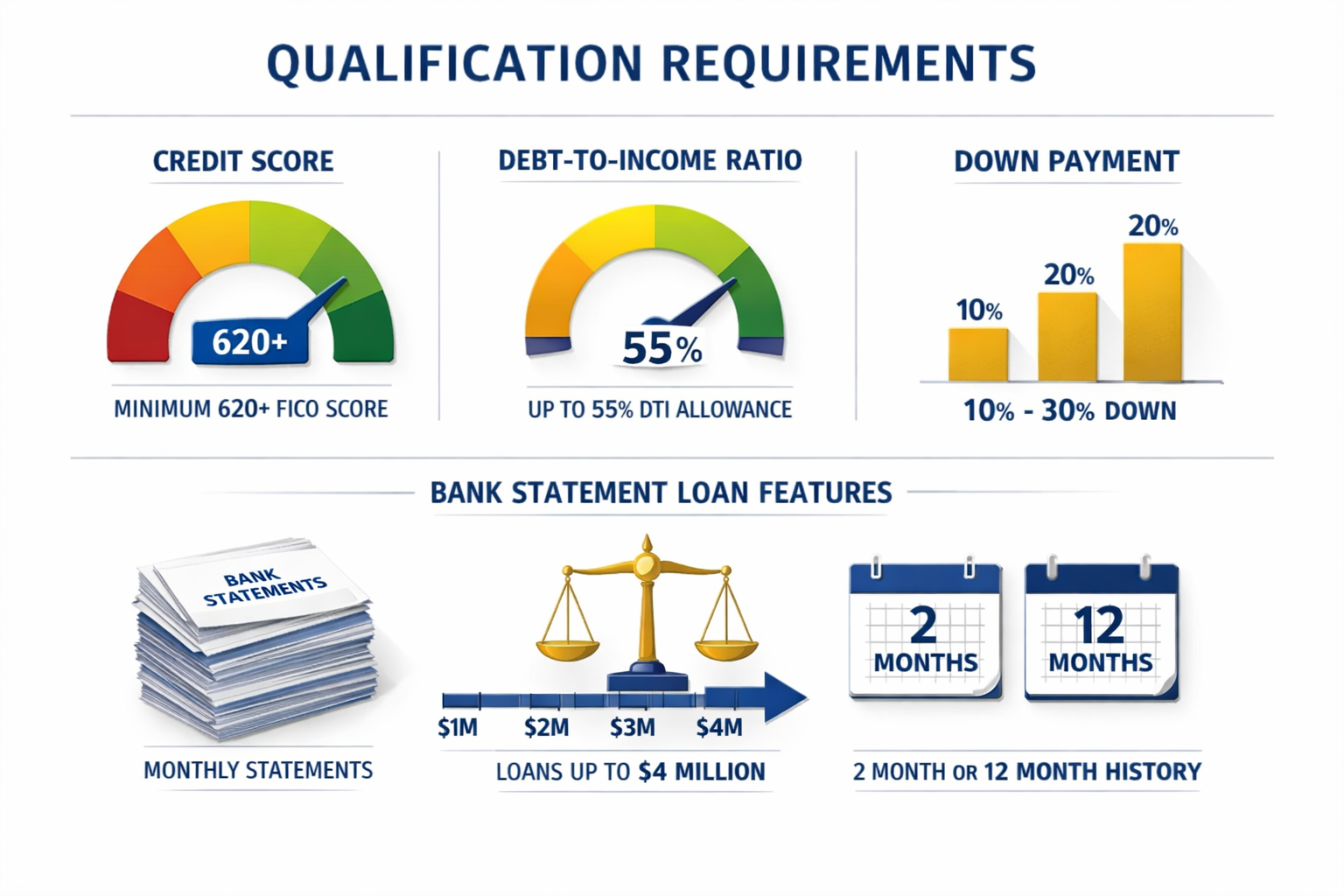

✅ Qualification requirements typically include a minimum 620 credit score, debt-to-income ratios up to 50-55%, and down payments ranging from 10-30%[1]

✅ Loan amounts can reach up to $4 million through specialized bank statement programs, making them viable for both primary residences and investment properties[1]

✅ 2026 trends show continued expansion of 2-month bank statement loans, offering faster qualification based on recent deposit activity rather than lengthy income history[4]

Understanding Non-QM Loans and Why Self-Employed Borrowers Need Them

What Are Non-QM Loans?

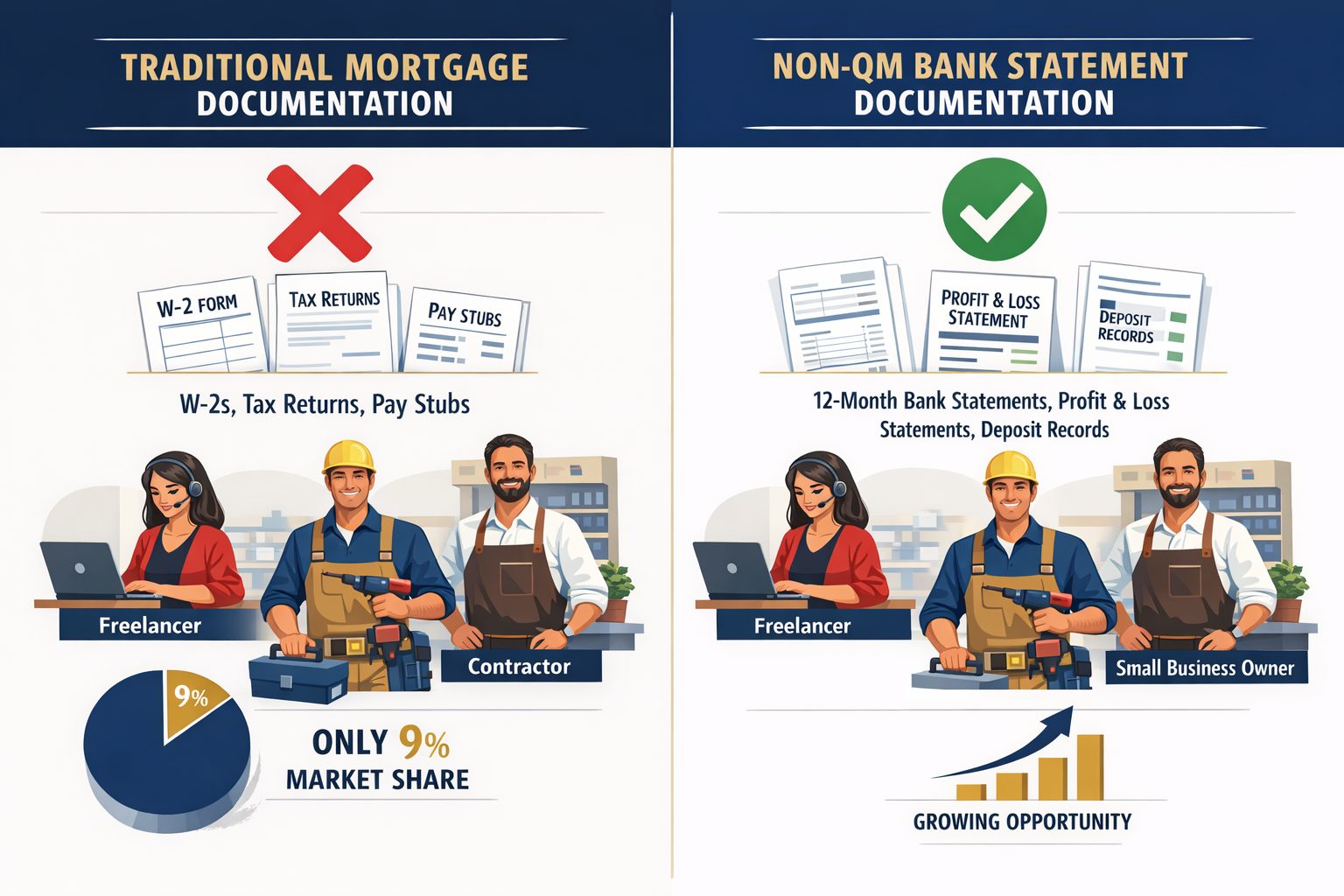

Non-Qualified Mortgage (Non-QM) loans are mortgage products that fall outside the strict guidelines established by government-sponsored enterprises like Fannie Mae and Freddie Mac. Unlike conventional mortgages that require W-2 income verification, tax returns, and rigid debt-to-income calculations, non-QM loans offer flexible underwriting that considers alternative documentation methods.

These loans aren’t “subprime” products—they’re designed for creditworthy borrowers whose income situations don’t fit the traditional employment mold. The non-QM lending environment in 2026 is shifting from rapid innovation to more disciplined, sustainable expansion focused on refinement and quality control[3].

The Self-Employed Income Documentation Problem

Self-employed professionals face a unique challenge when applying for traditional mortgages. Business owners legitimately reduce their taxable income through deductions for equipment, home office expenses, vehicle use, travel, and other business costs. While this strategy minimizes tax liability, it also reduces the income shown on tax returns—the very documents traditional lenders use to determine mortgage eligibility.

For example, a freelance consultant might deposit $120,000 annually into their business account but show only $65,000 in adjusted gross income after deductions. Traditional lenders would qualify them based on the lower figure, significantly limiting their purchasing power. This is where obtaining a mortgage when you’re self-employed becomes particularly challenging with conventional products.

Who Benefits from Bank Statement Mortgages?

Bank statement mortgages serve several key borrower segments in 2026:

- Freelancers and gig economy workers without traditional employment documentation

- Small business owners who maximize tax deductions

- Real estate investors with multiple income streams

- Commission-based professionals with variable income

- Independent contractors in the 1099 economy

- Self-employed professionals with less than two years of tax returns

Self-employed workers, gig-economy professionals, real estate investors, and borrowers with asset-based income streams are expected to remain core users of non-QM financing throughout 2026[3].

How Bank Statement Mortgages Work in 2026

The Bank Statement Qualification Process

Rather than analyzing tax returns, bank statement loans evaluate a borrower’s income by reviewing actual deposits into business or personal bank accounts. Lenders typically examine 12 to 24 months of statements, though 2-month bank statement loans are gaining particular traction in 2026 as they allow qualification based on recent deposit activity[4].

The income calculation process works as follows:

- Deposit Analysis: Lenders review all deposits to business and/or personal accounts

- Expense Factor: A standard expense ratio (typically 25-50%) is applied to account for business costs

- Income Averaging: The remaining amount is averaged over the statement period

- Qualification Calculation: This average becomes the qualifying income for debt-to-income ratio purposes

For those exploring mortgages for self-employed borrowers, this method provides a much more accurate representation of actual earning capacity.

2-Month vs. 12-Month vs. 24-Month Programs

| Program Type | Best For | Income Stability | Documentation |

|---|---|---|---|

| 2-Month | Recent income increases, seasonal businesses | Less emphasis on history | Most recent 2 months of statements |

| 12-Month | Consistent income patterns | Moderate stability required | Full year of banking activity |

| 24-Month | Established businesses | Strong pattern demonstration | Two years of statements |

The expansion of 2-month bank statement loans represents one of the most significant developments in the non-QM space for 2026, offering faster qualification pathways for borrowers with strong recent performance[4].

Personal vs. Business Bank Statements

Borrowers can qualify using either personal or business bank statements, depending on how they structure their finances:

Business Bank Statements are ideal for borrowers who:

- Operate as an LLC, S-Corp, or other business entity

- Keep business and personal finances separate

- Have clear business deposit patterns

Personal Bank Statements work better for:

- Sole proprietors who commingle funds

- Freelancers receiving payments to personal accounts

- Contractors without formal business structures

Some lenders allow a combination of both statement types to capture the complete income picture. Profit-and-loss statement loans are also gaining popularity among sole proprietors as an alternative documentation method[4].

Key Requirements for Non-QM Loans for Self-Employed Borrowers in 2026

Credit Score Requirements

While non-QM loans offer flexibility in income documentation, they still maintain credit standards. Most programs require:

- Minimum FICO score: 620 across most non-QM programs[1]

- Preferred range: 660-680+ for best rates and terms

- Recent credit events: Bankruptcy or foreclosure may require 2-4 year waiting periods

Borrowers with higher credit scores often qualify for lower interest rates and reduced down payment requirements. For those working to improve their credit position, reviewing 5 tips to rapidly improve your credit score can be beneficial before applying.

Debt-to-Income Ratio Flexibility

One of the most attractive features of Non-QM Loans for Self-Employed Borrowers: Your Guide to Bank Statement Mortgages in 2026 is the expanded debt-to-income (DTI) ratio allowances:

- Traditional mortgages: Typically cap DTI at 43-45%

- Non-QM programs: Allow DTI ratios up to 50% and sometimes higher[1]

- Bank statement loans: May permit DTI up to 55% with strong compensating factors[1]

This flexibility is crucial for self-employed borrowers who may have business debts, equipment financing, or other obligations that inflate their DTI calculations but don’t reflect their true financial capacity.

Down Payment Expectations

Down payment requirements for bank statement mortgages typically range from 10% to 30% of the loan amount[1]. The exact requirement depends on several factors:

- Credit score: Higher scores may qualify for lower down payments

- Loan amount: Larger loans often require more substantial down payments

- Property type: Investment properties typically require 20-30% down

- Compensating factors: Significant cash reserves can offset higher loan-to-value ratios

Larger down payments serve as strong compensating factors and can help secure better interest rates and terms. For borrowers struggling with down payment requirements, exploring alternative down payment options may provide additional strategies.

Cash Reserves and Asset Requirements

Non-QM lenders typically require borrowers to demonstrate liquid reserves after closing, usually:

- Primary residence: 6-12 months of mortgage payments (PITI)

- Investment property: 6-18 months of reserves

- Multiple properties: Additional reserves for each financed property

Acceptable reserve assets include:

- Savings and checking accounts

- Money market accounts

- Stocks, bonds, and mutual funds (typically 70% of value)

- Retirement accounts (60-70% of vested balance)

- Business accounts (with proper documentation)

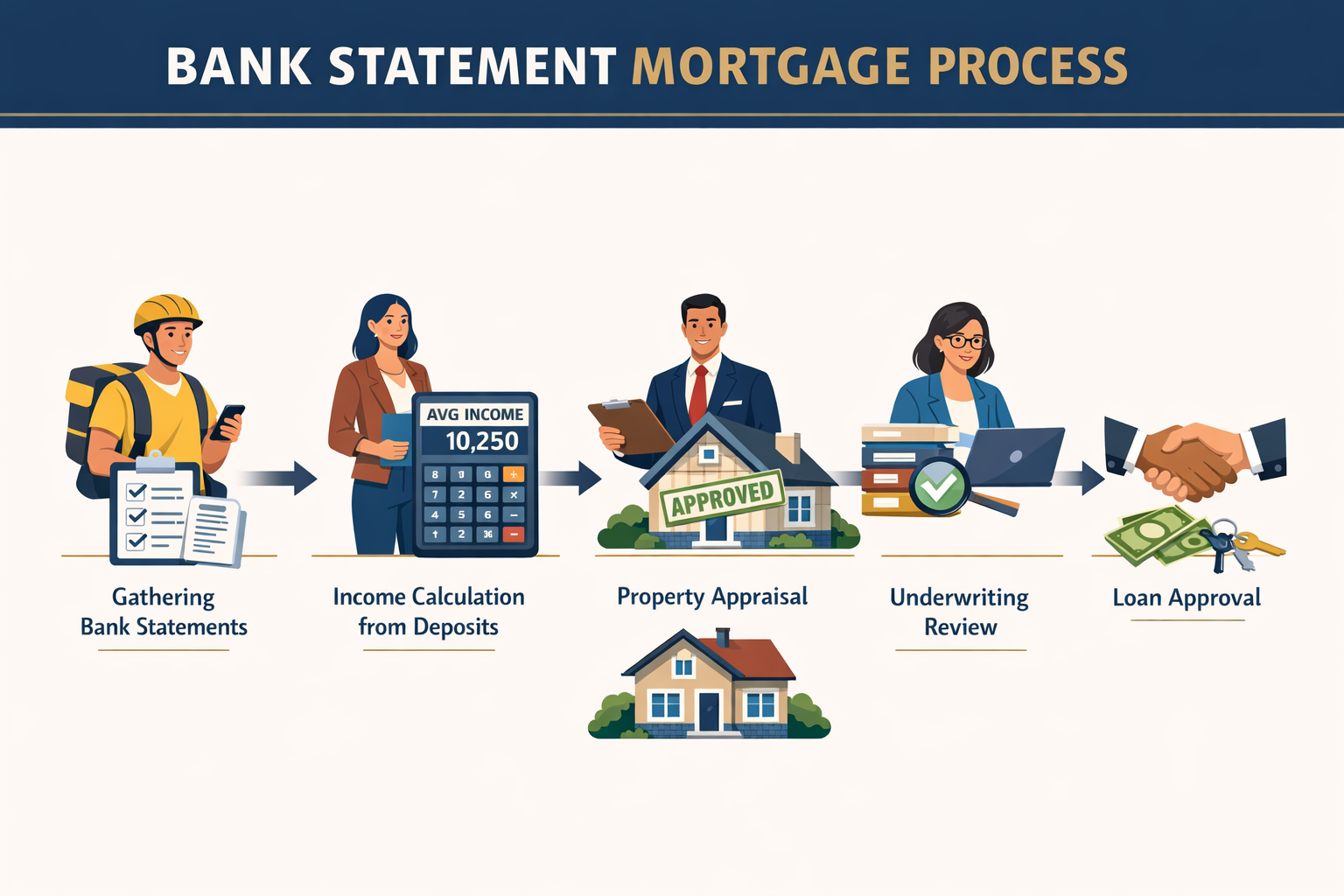

The Application Process: Step-by-Step Guide

Step 1: Gather Your Bank Statements

Collect consecutive monthly statements for the required period (2, 12, or 24 months). Ensure statements show:

- Account holder name

- Financial institution name

- Statement dates

- All deposits and withdrawals

- Beginning and ending balances

✅ Pro Tip: Organize statements chronologically and highlight business-related deposits to streamline the underwriting process.

Step 2: Prepare Additional Documentation

Beyond bank statements, you’ll need:

- Personal identification: Driver’s license or passport

- Business documentation: Business license, articles of incorporation, or DBA registration

- Credit authorization: Permission for lender to pull credit reports

- Property information: Purchase contract or property details for refinances

- Asset statements: Documentation of reserves and down payment funds

For comprehensive guidance, reviewing a mortgage document checklist can ensure nothing is overlooked.

Step 3: Income Calculation and Pre-Qualification

Your lender will calculate qualifying income by:

- Adding all business-related deposits

- Applying an expense factor (typically 25-50% depending on industry)

- Averaging the net amount over the statement period

- Calculating your DTI ratio using this income figure

This pre-qualification process helps establish your purchasing power before you begin house hunting. Understanding the importance of qualifying for a mortgage before buying property can save time and prevent disappointment.

Step 4: Property Selection and Appraisal

Once pre-qualified, you can confidently shop for properties within your approved range. After identifying a property:

- Submit a purchase offer

- Order a professional appraisal

- Ensure the property meets lender requirements

- Review appraisal results with your loan officer

Step 5: Underwriting and Approval

During underwriting, the lender will:

- Verify all documentation

- Confirm income calculations

- Review credit history and scores

- Assess property value and condition

- Evaluate overall risk profile

- Issue conditional approval with any final requirements

Step 6: Closing

After clearing all conditions, you’ll proceed to closing where you’ll:

- Review and sign final loan documents

- Provide down payment and closing costs

- Receive keys to your new property

The entire process typically takes 30-45 days from application to closing, though timelines vary based on documentation completeness and property complexity.

Advantages of Bank Statement Mortgages for Self-Employed Borrowers

🎯 True Income Recognition

Bank statement loans recognize your actual earning capacity rather than artificially reduced tax return income. This allows self-employed borrowers to qualify for mortgage amounts that truly reflect their financial capability.

📊 Flexible Documentation

No need for complex tax return analysis, profit-and-loss statements, or business financial statements (though P&L loans are available as alternatives). The straightforward bank statement review simplifies the process considerably.

⚡ Faster Processing

With fewer documentation requirements and simpler income verification, bank statement mortgages often close faster than traditional self-employed loans requiring extensive tax documentation.

💼 Business Deduction Benefits Preserved

You can continue maximizing legitimate business deductions for tax purposes without sacrificing mortgage qualification potential—the best of both worlds for savvy entrepreneurs.

🏠 Higher Loan Amounts

Specialized bank statement programs offer loan amounts up to $4 million[1], making them viable for luxury home purchases and high-value investment properties.

Potential Drawbacks and Considerations

Higher Interest Rates

Non-QM loans typically carry interest rates 0.5% to 2% higher than conventional mortgages due to the perceived additional risk. However, for borrowers who couldn’t otherwise qualify, this premium provides access to financing that wouldn’t exist through traditional channels.

Larger Down Payments

The 10-30% down payment requirement exceeds the 3-5% minimums available through conventional programs, requiring more upfront capital.

Prepayment Penalties

Some non-QM loans include prepayment penalties that charge fees for paying off or refinancing the loan within the first 2-5 years. Always review loan terms carefully and negotiate where possible.

Limited Lender Options

While growing, the non-QM market remains dominated by small- and medium-sized lenders[9], meaning fewer options than conventional mortgage shopping. Working with experienced mortgage brokers who specialize in non-QM products can help identify the best programs.

Income Volatility Scrutiny

Lenders carefully examine deposit patterns for consistency. Significant month-to-month variations may raise questions or require additional explanation, particularly with shorter statement periods.

2026 Market Trends and Outlook

Disciplined Market Expansion

The non-QM lending environment is transitioning from rapid innovation to more disciplined, sustainable expansion focused on refinement and quality control[3]. This maturation benefits borrowers through more competitive pricing and standardized underwriting.

Payment-Sensitive Borrowers

Self-employed borrowers in 2026 are increasingly payment-sensitive, requiring lenders to implement more careful product structuring to remain competitive[3]. This trend is driving innovation in rate structures and payment options.

Technology Integration

Advanced income calculation algorithms and automated bank statement analysis are streamlining the application process, reducing processing times and improving accuracy.

Expanded Acceptance

As non-QM loans represented approximately 9% of mortgage activity at the end of 2025[6], mainstream acceptance continues growing. More borrowers and real estate professionals recognize these products as legitimate, valuable financing options rather than “alternative” solutions.

Regulatory Stability

The non-QM market in 2026 operates within a more stable regulatory framework, providing borrower protections while maintaining the flexibility that makes these products valuable for self-employed professionals.

Comparing Non-QM Options: Bank Statement vs. Other Programs

Bank Statement Loans vs. Traditional Self-Employed Mortgages

| Feature | Bank Statement Loans | Traditional Self-Employed |

|---|---|---|

| Documentation | 2-24 months bank statements | 2 years tax returns + P&Ls |

| Income Calculation | Deposits minus expense factor | Tax return analysis |

| Processing Time | 30-45 days | 45-60 days |

| DTI Allowance | Up to 55% | Up to 45% |

| Credit Score | 620+ minimum | 620+ minimum |

| Down Payment | 10-30% | 3-20% |

Bank Statement Loans vs. Stated Income Loans

Stated income loans (where borrowers simply state their income without documentation) largely disappeared after the 2008 financial crisis. Modern bank statement loans provide the flexibility stated income loans offered but with actual documentation verification, making them sustainable and responsible lending products.

Bank Statement Loans vs. Asset-Based Loans

Asset-based loans qualify borrowers based on liquid assets rather than income. These work well for retirees or investors with significant wealth but limited income. Bank statement loans, conversely, focus on income flow and work better for active business owners with strong cash flow but potentially fewer accumulated assets.

For borrowers with multiple properties or complex financial situations, exploring second mortgage options may provide additional financing strategies.

Finding the Right Non-QM Lender

Specialized Non-QM Lenders

Small- and medium-sized lenders have dominated the non-QM market[9], often offering:

- More flexible underwriting

- Faster decision-making

- Specialized expertise in self-employed borrowers

- Competitive pricing within the non-QM space

Working with Mortgage Brokers

Mortgage brokers with non-QM expertise can:

- Access multiple lender programs

- Compare rates and terms across providers

- Navigate complex documentation requirements

- Advocate on your behalf during underwriting

Understanding what a mortgage broker does can help you leverage their expertise effectively.

Questions to Ask Potential Lenders

When evaluating non-QM lenders, ask:

- What bank statement programs do you offer (2-month, 12-month, 24-month)?

- What expense factors do you apply to different business types?

- Are there prepayment penalties?

- What are your minimum credit score and down payment requirements?

- What loan amounts do you offer?

- What is your typical processing timeline?

- Do you service loans in-house or sell them?

- What compensating factors do you consider?

Red Flags to Avoid

Be cautious of lenders who:

- Promise unrealistic terms or “guaranteed approval”

- Pressure you to misrepresent information

- Charge excessive upfront fees before processing

- Lack transparency about rates and terms

- Have poor reviews or regulatory complaints

Tips for Self-Employed Borrowers to Strengthen Their Application

🏦 Maintain Clean Banking Records

For at least 12 months before applying:

- Avoid overdrafts and NSF fees

- Maintain consistent deposit patterns

- Separate business and personal transactions when possible

- Document large or unusual deposits

📈 Build Strong Cash Reserves

Accumulate 6-12 months of reserves beyond your down payment to demonstrate financial stability and improve approval odds.

💳 Optimize Your Credit Profile

Before applying:

- Pay down credit card balances below 30% utilization

- Avoid opening new credit accounts

- Dispute any credit report errors

- Make all payments on time for at least 12 months

📋 Organize Business Documentation

Even though tax returns aren’t required, having organized business records demonstrates professionalism and may help with borderline applications:

- Business licenses and registrations

- Client contracts or agreements

- Business bank account statements

- Proof of business longevity

🤝 Consider a Co-Borrower

Adding a co-borrower with traditional W-2 income can:

- Strengthen the overall application

- Potentially qualify for better rates

- Increase purchasing power

- Provide additional income verification

💰 Increase Your Down Payment

If possible, exceeding minimum down payment requirements:

- Reduces lender risk

- May qualify you for better rates

- Provides equity cushion

- Demonstrates financial commitment

Real-World Scenarios: Who Benefits Most

Scenario 1: The Freelance Consultant

Profile: Sarah operates a successful marketing consulting business, depositing $15,000 monthly into her business account. After legitimate business deductions, her tax returns show only $85,000 annual income.

Traditional Mortgage: Would qualify based on $85,000 income Bank Statement Loan: Qualifies based on approximately $135,000 income (assuming 25% expense factor) Result: Sarah can afford a significantly more expensive home that matches her actual financial capacity.

Scenario 2: The Gig Economy Professional

Profile: Marcus works as a rideshare driver and food delivery contractor, earning $6,000-$8,000 monthly with deposits to his personal checking account. He has no traditional tax returns showing this income level.

Traditional Mortgage: Difficult to qualify without W-2 income Bank Statement Loan: Uses 12 months of personal bank statements showing consistent deposits Result: Marcus qualifies for homeownership despite non-traditional employment.

Scenario 3: The Real Estate Investor

Profile: Jennifer owns three rental properties and shows minimal taxable income after depreciation and expense deductions, but has strong cash flow.

Traditional Mortgage: Tax returns show little qualifying income Bank Statement Loan: Demonstrates strong deposit patterns from rental income Result: Jennifer can expand her investment portfolio despite low tax return income.

For professionals in specific fields, specialized programs like self-employed lawyer mortgages may offer additional benefits.

Common Mistakes to Avoid

❌ Waiting Until the Last Minute

Start preparing your bank statements and financial documentation 6-12 months before you plan to purchase. Clean banking records significantly improve approval odds.

❌ Mixing Personal and Business Funds Carelessly

While some commingling is acceptable, excessive mixing of personal and business transactions makes income calculation difficult. Maintain reasonable separation when possible.

❌ Making Large Unexplained Deposits

Large deposits without clear documentation raise red flags. If you receive a large payment, keep documentation showing its source and business purpose.

❌ Assuming All Non-QM Lenders Are Equal

Programs, rates, and terms vary significantly among non-QM lenders. Shop around and compare at least 3-5 options before committing.

❌ Neglecting to Explain Income Fluctuations

If your deposits vary significantly month-to-month, proactively explain seasonal patterns, large project payments, or business cycles to underwriters.

❌ Overlooking Total Cost of Borrowing

Focus on the total cost including interest rate, fees, and potential prepayment penalties rather than just the monthly payment.

For additional guidance, reviewing common mistakes to avoid when applying for a mortgage can prevent costly errors.

The Future of Non-QM Lending for Self-Employed Borrowers

The trajectory for Non-QM Loans for Self-Employed Borrowers: Your Guide to Bank Statement Mortgages in 2026 points toward continued growth and refinement. As the gig economy expands and more professionals choose self-employment, traditional lending criteria become increasingly misaligned with modern work patterns.

Key developments to watch include:

- Expanded automation in bank statement analysis reducing processing times

- More competitive pricing as market maturation increases competition

- Additional product variations tailored to specific self-employed segments

- Greater mainstream acceptance among real estate professionals and borrowers

- Enhanced borrower protections through refined regulatory frameworks

The non-QM market’s evolution from niche alternative to established financing option reflects fundamental changes in how Americans work and earn income. Bank statement mortgages aren’t a temporary workaround—they’re a permanent solution to a permanent shift in employment patterns.

Conclusion: Taking the Next Steps Toward Homeownership

For self-employed professionals who’ve felt excluded from homeownership due to traditional lending requirements, Non-QM Loans for Self-Employed Borrowers: Your Guide to Bank Statement Mortgages in 2026 offers a clear path forward. These programs recognize that tax returns don’t tell the whole story of entrepreneurial success and provide qualification pathways based on actual cash flow rather than artificially reduced taxable income.

Your Action Plan

Immediate Steps (This Month):

- Review 12-24 months of bank statements to assess deposit patterns

- Check your credit score and address any issues

- Calculate your potential qualifying income using a 25-50% expense factor

- Begin accumulating cash reserves for down payment and closing costs

Short-Term Steps (Next 3 Months):

- Research non-QM lenders and mortgage brokers specializing in bank statement loans

- Get pre-qualified to understand your purchasing power

- Clean up banking records and establish consistent deposit patterns

- Organize business documentation and financial records

Long-Term Steps (Next 6-12 Months):

- Build credit score above 660 for optimal rates and terms

- Accumulate larger down payment to reduce rates and monthly payments

- Establish stable income patterns over multiple statement periods

- Begin property search with realistic budget based on pre-qualification

The self-employed path to homeownership requires more preparation than traditional employment scenarios, but the destination is absolutely reachable. Bank statement mortgages have opened doors that were previously closed, allowing entrepreneurs, freelancers, and business owners to achieve the dream of homeownership while maintaining the tax strategies that make their businesses successful.

Don’t let traditional lending barriers hold you back. With proper preparation, the right lender, and understanding of how bank statement mortgages work, self-employed professionals can secure financing that reflects their true financial strength. The key is starting early, maintaining clean financial records, and working with lenders who understand the unique needs of self-employed borrowers.

Your entrepreneurial success shouldn’t prevent you from owning a home—it should enable it. Non-QM Loans for Self-Employed Borrowers: Your Guide to Bank Statement Mortgages in 2026 provides the roadmap. Now it’s time to take the first step on your journey to homeownership.

References

[1] Non Qm Loan Requirements – https://admortgage.com/blog/non-qm-loan-requirements/

[2] Who Are The Best Lenders For Self Employed Borrowers – https://www.nasb.com/blog/detail/who-are-the-best-lenders-for-self-employed-borrowers

[3] Non Qm Lending Poised For A More Disciplined Expansion In 2026 – https://www.mortgage-underwriters.org/mortgage-underwriting-news/2026/1/20/non-qm-lending-poised-for-a-more-disciplined-expansion-in-2026

[4] Non Qm Lending Trends To Watch In 2026 What Brokers Need To Prepare For – https://www.nqmf.com/non-qm-lending-trends-to-watch-in-2026-what-brokers-need-to-prepare-for/

[5] Mortgage Self Employed 1099 Business Get Approved – https://themortgagereports.com/18303/mortgage-self-employed-1099-business-get-approved

[6] Mortgage Monitor January 21 – https://www.amerisbank.com/Personal/Learn/Financial-Articles-Advice/Buying-A-Home/Mortgage-Monitor-January-21

[7] How Non Qm Loans Unlock Unique Financing Opportunities – https://eastcoastcap.com/2026/01/19/how-non-qm-loans-unlock-unique-financing-opportunities/

[8] 2026 Non Qm Market Outlook Building On A Rock Solid Foundation – https://foundationmortgage.com/2026-non-qm-market-outlook-building-on-a-rock-solid-foundation/

[9] 4 Trends That Will Help Mortgage Lenders Reach New Borrowers In 2026 – https://www.housingwire.com/articles/4-trends-that-will-help-mortgage-lenders-reach-new-borrowers-in-2026/