March 23, 2026

Private Mortgages for Toronto’s Larger Loan Borrowers: Qualifying on $344K+ Balances in a Cooling 2026 Market

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

New borrowers are stepping into Toronto’s housing market carrying a median mortgage balance of $344,000 — and banks are making it harder than ever to get approved. Tighter federal rules, stricter debt ratio calculations, and a cooling market have pushed thousands of high-balance borrowers toward an alternative that’s gaining serious traction: private mortgages. For anyone navigating Private Mortgages for Toronto’s Larger Loan Borrowers: Qualifying on $344K+ Balances in a Cooling 2026 Market, understanding how these loans work — and how to qualify — can be the difference between owning a home and losing a deal. [1]

Key Takeaways 🏠

- Private lenders approve in 24–48 hours based on property equity, not just income — a critical advantage for $344K+ borrowers rejected by banks

- OSFI’s 2026 rule changes tightened bank lending standards, pushing more high-balance Toronto borrowers toward private mortgage solutions [1]

- Toronto’s benchmark home price dropped 7.9% YoY to $938,800 in February 2026, creating more equity cushion for private approvals [1]

- Private mortgage rates run 8–14%, but they serve as a short-term bridge — most borrowers exit to B-lenders or banks within 12–24 months [5]

- Ontario’s new suitability assessments for private mortgages add borrower protections, especially for loans above $344K [1]

Why Banks Are Saying No to $344K+ Borrowers in 2026

Toronto’s housing market has cooled significantly. With five months of supply and benchmark prices sitting at $938,800 as of February 2026, it looks like a buyer’s market on the surface. But qualifying for a mortgage? That’s a different story entirely. [1]

OSFI’s Capital Adequacy Requirements (CAR), updated and effective Q1 2026, fundamentally changed how banks calculate borrower debt ratios. Rental income can no longer be double-counted, and high-balance borrowers face stricter scrutiny across the board. The result: thousands of financially capable Torontonians — self-employed professionals, investors, and even salaried workers with complex income — are hitting walls at major banks. [1]

💬 “Private mortgages have become a 24–48 hour bridge for Toronto borrowers facing 2026 bank rejections. The key is having a clear 12–24 month exit strategy from day one.” — Manzeel Patel, Mortgage Broker, Everything Mortgages [5]

The Bank of Canada has flagged that approximately 1.2 million mortgage renewals are under pressure in 2026 amid elevated household debt levels. For asset-rich but income-complex borrowers, private lenders are filling the gap that banks have left open. [10]

Understanding how easy it is to get a private mortgage starts with recognizing that private lenders evaluate deals differently — equity first, income second.

How Private Mortgages for Toronto’s Larger Loan Borrowers Work: Qualifying on $344K+ Balances

Private mortgages in Toronto are issued by individual investors or mortgage investment corporations (MICs), not chartered banks. They operate outside OSFI’s strict lending framework, which means they can approve borrowers that banks turn away.

The Core Qualification Formula

Private lenders focus on three primary factors:

| Factor | What Lenders Look For |

|---|---|

| Loan-to-Value (LTV) | Typically 65–80% max LTV on Toronto properties |

| Property Value | Confirmed via independent appraisal |

| Exit Strategy | Clear plan to refinance within 12–24 months |

| Credit Score | Minimum ~550–600; lower scores accepted with strong equity |

| Income Documentation | Flexible — bank statements, NOAs, or stated income accepted |

For a $344K+ mortgage balance on a Toronto property valued at $938,800, an LTV of roughly 37–40% gives private lenders significant comfort. Even in a cooling market, that equity buffer is substantial. [1][2]

What CMHC Changes Mean for High-Balance Borrowers

CMHC’s February 2026 overhaul raised insurance premiums to approximately 7% for high-financing construction projects and imposed CPI-only rental income increases. For borrowers pursuing multi-unit properties or new builds, this makes insured financing more expensive — and private mortgages a logical bridge.

However, there’s good news on the insured side: the insured mortgage cap was raised to $1.5 million effective December 15, 2024. A buyer purchasing a $1.25M Toronto home now needs only $100,000 down (versus the previous $250,000), reducing — but not eliminating — the need for private options on larger balances. [1]

For borrowers who don’t fit neatly into insured categories, understanding how the mortgage stress test applies is essential before approaching any lender.

Comparing Private Lenders to B-Lenders: Which Is Right for $344K+ Balances?

Not every borrower who gets rejected by a bank needs a private mortgage. B-lenders (trust companies and alternative lenders) occupy a middle ground that’s worth exploring first.

Side-by-Side Comparison

| Feature | B-Lender | Private Lender |

|---|---|---|

| Rate Range | 5.0% – 6.5% | 8% – 14% |

| Approval Time | 1–2 weeks | 24–48 hours |

| Credit Minimum | ~620–650 | ~550+ |

| Income Verification | Moderate flexibility | High flexibility |

| Best For | Moderate credit, steady income | Complex income, urgent closings |

| Loan Term | 1–5 years | 6–12 months (renewable) |

B-lenders are the better choice for $344K+ borrowers with moderate credit and some income documentation. Private lenders shine when speed, flexibility, or income complexity makes B-lender approval unlikely. [5][9]

Lendworth analysts confirm that Ontario homeowners with $344K+ mortgages are increasingly turning to private lenders specifically because of bank inflexibility following OSFI’s updated oversight — with private lenders emphasizing equity over income in GTA’s high-cost environment. [2]

For self-employed borrowers specifically, qualifying for a Toronto mortgage without T4 slips in 2026 outlines alternative documentation paths that can work with both B-lenders and private options.

The OSFI Stress Test Exemption Worth Knowing

OSFI’s straight-switch exemption (introduced November 2024) allows uninsured high-balance borrowers to switch lenders at renewal without requalifying under the stress test, provided the loan terms remain unchanged. This is a meaningful option for borrowers with existing $344K+ mortgages who need to move lenders without triggering full requalification. [3]

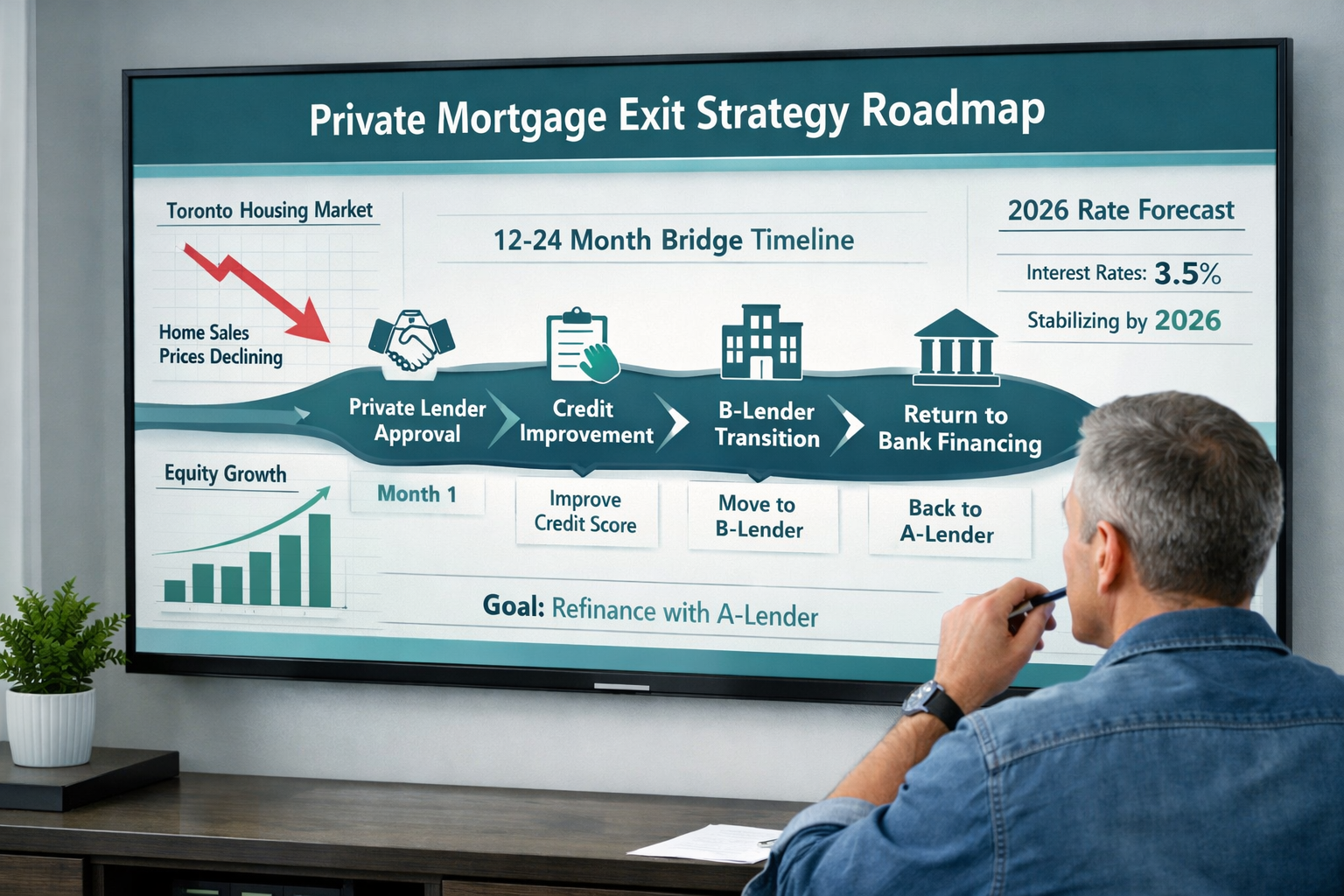

Building a Private Mortgage Exit Strategy That Works

The most important conversation any private mortgage borrower can have is about how to get out. Private rates of 8–14% are not meant to be permanent — they are a bridge, not a destination. [5]

A Practical 12–24 Month Exit Roadmap 🗺️

Month 1–3: Stabilize

- Close the private mortgage and address the immediate need (purchase, renewal, or refinance)

- Begin improving your credit score — even small gains open B-lender doors

- Organize income documentation (NOAs, bank statements, contracts)

Month 4–9: Build Qualification Strength

- Reduce outstanding consumer debt

- Maintain consistent income records

- Monitor Toronto property values — rising equity accelerates the exit

Month 10–18: Transition to B-Lender or Bank

- Approach B-lenders with improved credit and documentation

- Consider mortgage refinancing options to consolidate and lower your rate

- If credit and income qualify, return to conventional lending

Month 18–24: Full Exit

- Refinance into a conventional or insured mortgage at standard rates

- Lock in a competitive term using current Bank of Canada rate stability (forecast at 2.25% for 2026)

🔑 Key insight: Fitch Ratings notes that Canadian mortgage repricing is stressing lower-priority consumer debt for high-balance holders — making a clean exit strategy essential to protect credit standing during the private mortgage period. [10]

Ontario’s New Borrower Protections in 2026

Ontario’s February 2026 regulatory proposals expand Level 1 mortgage agents’ access to CMHC lenders while adding mandatory suitability assessments for private mortgage recommendations. For borrowers carrying $344K+ balances, this means brokers are now required to demonstrate that a private mortgage genuinely serves the borrower’s interests — not just the lender’s. [1]

This is a meaningful consumer protection. Before signing any private mortgage agreement, ensure your broker walks through the importance of qualifying for a mortgage before buying — including a full review of fees, lender fees (typically 1–3%), and renewal terms.

Costs to Budget For on a $344K+ Private Mortgage

| Cost Item | Typical Range |

|---|---|

| Interest Rate | 8% – 14% annually |

| Lender Fee | 1% – 3% of loan amount |

| Broker Fee | 1% – 2% of loan amount |

| Legal Fees | $1,500 – $3,000 |

| Appraisal Fee | $400 – $600 |

On a $344,000 balance at 10% interest, monthly carrying costs run approximately $2,867 — significantly higher than bank rates. This reinforces why the exit strategy isn’t optional; it’s the entire plan. [7]

For borrowers exploring whether best private mortgage rates in Ontario can be negotiated lower, current Ontario private mortgage rate benchmarks provide a useful starting point for comparison.

Conclusion: Private Mortgages as a Strategic Tool, Not a Last Resort

Private Mortgages for Toronto’s Larger Loan Borrowers: Qualifying on $344K+ Balances in a Cooling 2026 Market are no longer a fringe option — they are a mainstream bridge for capable borrowers navigating a system that has become increasingly rigid. OSFI’s tighter rules, CMHC’s premium increases, and a cooling Toronto market have created a gap that private lenders are uniquely positioned to fill. [1][2]

The borrowers who succeed with private mortgages are those who treat them as a strategic 12–24 month tool — entering with a clear plan, managing costs carefully, and executing a disciplined exit toward conventional financing.

Actionable Next Steps ✅

- Get a professional assessment — Work with a licensed mortgage broker to determine if a B-lender or private lender is the right fit for your $344K+ balance

- Know your equity position — Order an independent appraisal to confirm your LTV before approaching any lender

- Build your exit plan first — Identify your target lender for month 18–24 before signing the private mortgage

- Review Ontario’s new suitability rules — Ensure your broker provides a documented suitability assessment under 2026 regulations

- Compare all-in costs — Factor in lender fees, broker fees, and legal costs alongside the interest rate

Toronto’s cooling market is creating opportunity — but only for borrowers who understand the tools available to them. Private mortgages, used strategically, are one of the most powerful tools in that kit.

References

[1] Playing By New Rules What Changed For Toronto Real Estate In 2025 2026 – https://www.getwhatyouwant.ca/playing-by-new-rules-what-changed-for-toronto-real-estate-in-2025-2026

[2] Ontario Homeowners Are Using Private Mortgages To Survive 2026 Heres Why Banks Arent The First Call Anymore – https://www.lendworth.ca/blog/lendworth-blog-1/ontario-homeowners-are-using-private-mortgages-to-survive-2026-heres-why-banks-arent-the-first-call-anymore-717

[3] Client Conversations That Win Mortgage Renewals In A Cooling Market – https://brokers.thecmigroup.ca/blog/client-conversations-that-win-mortgage-renewals-in-a-cooling-market/

[5] Private Mortgages For First Time Buyers In Toronto Navigating 2026 Affordability Challenges – https://everythingmortgages.ca/blog/private-mortgages-for-first-time-buyers-in-toronto-navigating-2026-affordability-challenges/

[7] Private Mortgage In Ontario – https://bestrates.ca/private-mortgage-in-ontario

[9] Private Mortgages In Toronto Essential Strategies For Surviving 2026 Renewal Payment Shocks – https://everythingmortgages.ca/blog/private-mortgages-in-toronto-essential-strategies-for-surviving-2026-renewal-payment-shocks/

[10] Canadian Mortgage Repricing May Pressure Lower Priority Consumer Debt – https://www.fitchratings.com/research/structured-finance/canadian-mortgage-repricing-may-pressure-lower-priority-consumer-debt-23-02-2026