March 15, 2026

Private Mortgages vs CMHC MLI for Toronto Multi-Family Buys: Rate, Speed, and LTV Breakdown

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s multi-family market is at a turning point in 2026. 🏙️ Rents have softened slightly from their 2024 peaks, but analysts predict a strong rebound by 2028 — and savvy investors are moving now to buy the dip. The central question every investor faces is this: should you move fast with a private mortgage at 7–12%, or wait for CMHC MLI’s 3.5–4.25% rates and superior leverage? This guide on Private Mortgages vs CMHC MLI for Toronto Multi-Family Buys: Rate, Speed, and LTV Breakdown cuts through the noise and gives you the numbers, timelines, and strategy to decide.

Key Takeaways 🔑

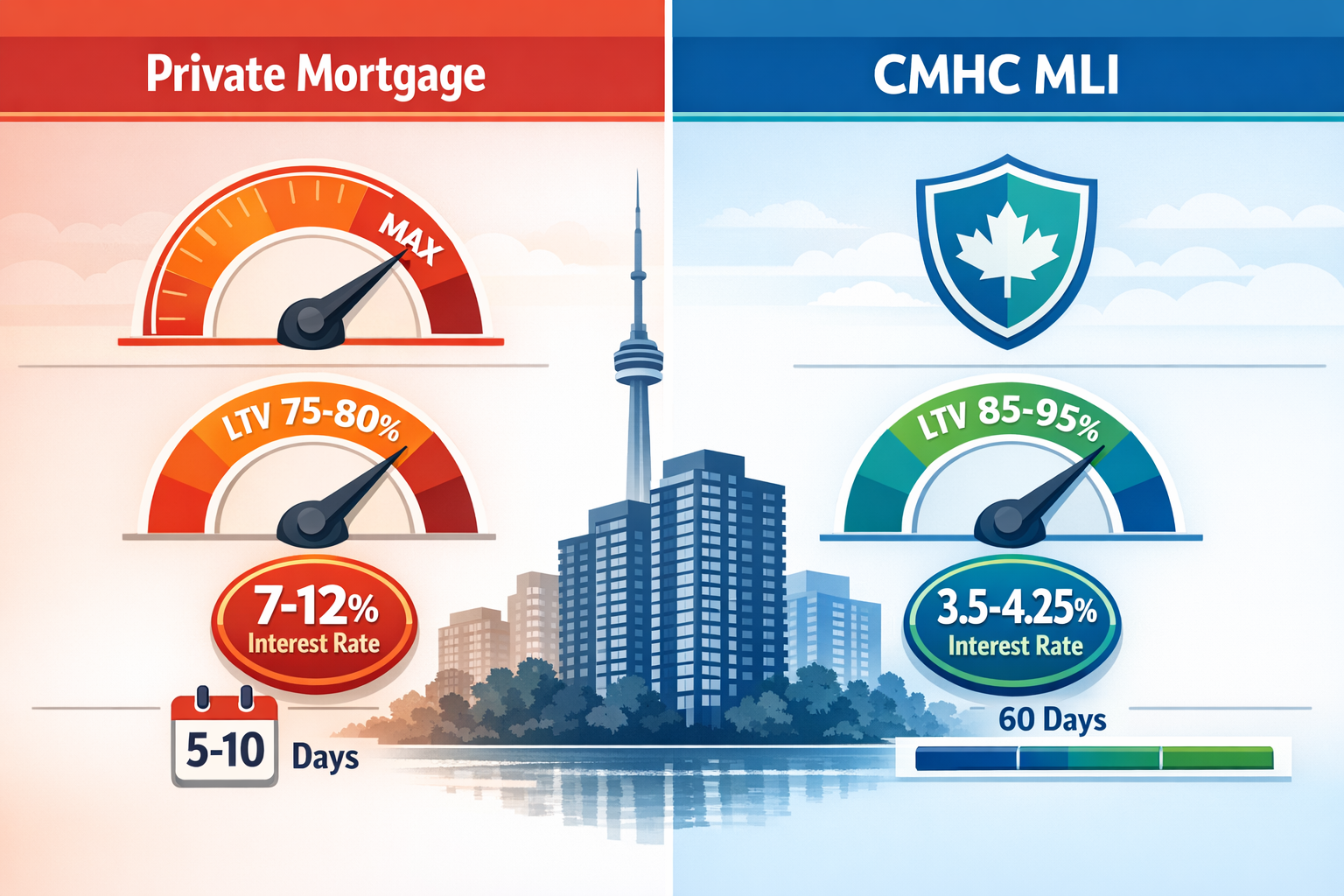

- Private mortgages close in 5–10 days at 7–12% interest with 75–80% LTV — ideal for time-sensitive, non-stabilized, or value-add deals.

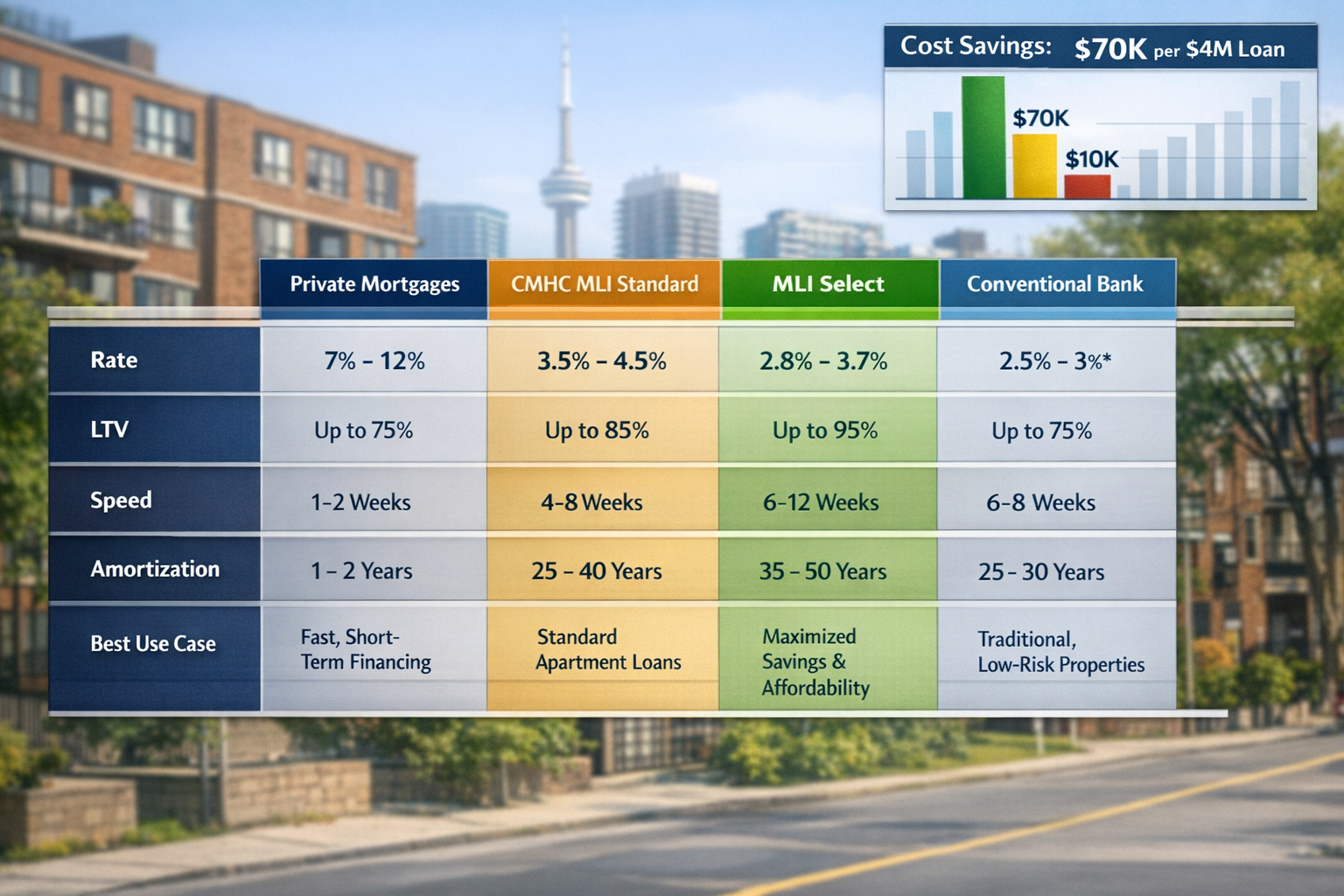

- CMHC MLI Standard offers 85% LTV at ~3.5–4.25% but takes 4–8 weeks; MLI Select pushes to 95% LTV with a 50-year amortization but demands 3–6 months and a rigorous points system.

- On a $4M loan, CMHC MLI can save approximately $70,000 per year in interest versus private financing. [1]

- Toronto’s vacancy rate is projected at 3.4% in 2026 with an economic rebound expected in H2, making stabilized assets ideal for CMHC. [3]

- The right choice depends on deal type, timeline, and property condition — not just rate.

Understanding the Two Paths: Private Mortgages vs CMHC MLI for Toronto Multi-Family Buys

Before diving into numbers, it helps to understand what each financing tool is actually built for.

What Is a Private Mortgage?

A private mortgage comes from individual investors or private lending companies — not banks or government-backed programs. In Toronto’s multi-family space, these loans are designed for speed and flexibility. Learn more about current private mortgage rates in Ontario.

Key characteristics in 2026:

- Rates: 7–12% (higher risk = higher cost)

- LTV: 75–80% (lenders want more equity as protection)

- Close time: 5–10 business days

- Best for: Non-stabilized buildings, renovations, bridge financing, or deals where speed wins

What Is CMHC MLI?

The CMHC Multi-Unit Mortgage Loan Insurance (MLI) program is a federal government-backed product designed to encourage affordable, energy-efficient rental housing. It comes in two main flavors:

| Feature | MLI Standard | MLI Select |

|---|---|---|

| Max LTV | 85% | 95% |

| Amortization | Up to 40 years | Up to 50 years |

| Rate Range | ~3.5–4.25% | ~3.5–4.25% |

| Approval Time | 4–8 weeks | 3–6 months |

| Points Required | None | 100+ points |

| Best For | Stabilized buys | Long-term affordable/green holds |

MLI Select requires investors to score 100+ points across affordability, energy efficiency, and accessibility criteria. [1] That’s a significant commitment — and one that can take months to satisfy.

💬 Pull Quote: “On a $4M loan, CMHC MLI can save approximately $70,000 per year compared to private financing — but only if your property qualifies and you can afford to wait.” [1]

Rate, Speed, and LTV Breakdown: The Numbers That Matter

Interest Rate Comparison

This is where the gap is most dramatic. Here’s how the options stack up in 2026:

| Financing Type | Rate Range | Annual Cost on $3M Loan |

|---|---|---|

| Private Mortgage | 7–12% | $210,000–$360,000 |

| Conventional Bank | 4.75–6.5% | $142,500–$195,000 |

| CMHC MLI Standard/Select | 3.5–4.25% | $105,000–$127,500 |

The math is clear: private mortgages are expensive. But that cost buys something — time and certainty of close.

For investors buying distressed or non-stabilized buildings in Toronto’s current softening market, a 5–10 day close can mean the difference between winning a deal and losing it. [1]

LTV Comparison: How Much Can You Borrow?

Loan-to-Value (LTV) determines how much of the purchase price a lender will finance. Higher LTV = less cash down.

- Private: 75–80% LTV → You need 20–25% down

- Conventional Bank: 60–75% LTV → You need 25–40% down [1]

- CMHC MLI Standard: 85% LTV → 15% down

- CMHC MLI Select: Up to 95% LTV → as little as 5% down

For a $5M Toronto apartment building, MLI Select could mean putting down just $250,000 versus $1–1.25M with a private lender. That’s a massive capital efficiency difference for investors scaling a portfolio.

However, it’s worth noting that CMHC recently eliminated multi-title property bundling, pushing investors toward single-title buildings with 5+ units. [1] This structural shift is reshaping how Toronto investors structure their acquisitions.

Speed: When Timing Is Everything ⏱️

Toronto’s multi-family market moves fast. Sellers under pressure — especially those facing the 2026 mortgage renewal wave — sometimes need to close in days, not months.

- Private mortgage: 5–10 business days

- CMHC MLI Standard: 4–8 weeks

- CMHC MLI Select: 3–6 months

A YouTube analyst reviewing MLI Select in early 2026 argued the program is the “wrong starting point” for many Toronto deals because Toronto’s high rents often don’t meet CMHC’s affordability thresholds for the points system. [8] Private financing fills that gap with flexibility.

Choosing the Right Tool: Strategic Scenarios for Toronto Investors

When Private Mortgages Win ✅

Private financing makes sense when:

- 🔨 The building needs renovation — CMHC won’t insure non-stabilized properties

- ⚡ You need to close in under 2 weeks — competitive offers, motivated sellers

- 🏗️ You’re bridging to CMHC — use private now, refinance into MLI once stabilized

- 📋 Income documentation is complex — private lenders care less about T4s. (See our guide on getting a mortgage approved as a self-employed borrower)

- 🏢 The building has fewer than 5 units or mixed-title issues

Private mortgages are also a lifeline for investors who don’t yet have the track record for CMHC approval. Think of them as a bridge, not a destination.

When CMHC MLI Wins ✅

CMHC financing is the better long-term play when:

- 🏦 The property is already stabilized with consistent rental income

- 📅 You have 2–6 months to complete the approval process

- 💰 Capital preservation matters — the rate savings are real and compounding

- 🌱 You can meet MLI Select’s points requirements (energy efficiency upgrades, below-market rents, accessibility features)

- 📈 You’re holding for 10+ years — the 50-year amortization dramatically lowers monthly payments

The Marcus & Millichap Toronto Multifamily Forecast for 2026 predicts vacancy at 3.4% with an economic rebound in H2 2026, making stabilized, CMHC-insured properties strong long-term holds. [3] The CMHC Spring 2026 Housing Supply Report also confirmed record rental apartment construction, with housing starts up 6% in 2025 — though labor shortages continue to delay completions. [7]

The Hybrid Strategy 🔄

Many experienced Toronto investors use both tools in sequence:

- Buy with private — fast close, win the deal

- Renovate and stabilize — improve NOI and occupancy

- Refinance into CMHC MLI — lock in low rates, pull equity

This approach lets investors move at market speed while ultimately accessing CMHC’s superior economics. It’s particularly effective in a softening rent environment where motivated sellers are more common. For investors exploring renovation financing, understanding how to refinance to add rental units can be a powerful tool.

Don’t Forget Conventional Bank Financing

Conventional bank financing sits in the middle ground — rates of 4.75–6.5%, LTV of 60–75%, and no points system. [1] It’s slower than private but faster than CMHC, and more flexible than MLI without the long-term commitments. For investors with strong equity and a proven track record, it’s a solid third option. Understanding how the mortgage stress test applies to multi-family purchases is essential before approaching any institutional lender.

Key Risks to Watch in 2026 ⚠️

- Private mortgage penalties can be steep if you exit early — review terms carefully. See our breakdown of mortgage penalties and how to avoid them.

- MLI Select’s 10–20 year commitment carries real penalties if you sell or refinance early. [1]

- Rising arrears — CMHC flagged increasing mortgage arrears in February 2026, making lender due diligence more rigorous across the board.

- Labor shortages are delaying new construction completions, which could tighten supply faster than expected and benefit existing multi-family owners. [7]

- Toronto rent softness in early 2026 may affect CMHC’s income stabilization requirements for MLI approval.

For investors managing rental properties as a self-employed individual, understanding your financing options is especially important in this environment.

Conclusion: Match the Tool to the Deal

The Private Mortgages vs CMHC MLI for Toronto Multi-Family Buys: Rate, Speed, and LTV Breakdown isn’t a contest with one winner — it’s a toolkit with two very different instruments.

Use private mortgages when speed, flexibility, or property condition rules out institutional financing. Accept the higher cost as the price of opportunity.

Use CMHC MLI when you have a stabilized asset, time to wait, and a long-term hold strategy. The rate savings and leverage are genuinely transformational at scale.

Actionable next steps:

- 📊 Assess your deal timeline — can you wait 4–8 weeks or do you need 5–10 days?

- 🏢 Evaluate property condition — is it stabilized enough for CMHC?

- 💡 Run the numbers — calculate annual savings of CMHC vs private on your specific loan amount

- 🔄 Consider the bridge strategy — private now, CMHC refinance later

- 📞 Speak with a mortgage broker who specializes in Toronto multi-family to map the right path for your portfolio

The 2026 market window — with softening rents and motivated sellers — won’t last forever. The investors who understand their financing options deeply will be best positioned for the 2028 rebound. Start your mortgage application today to explore which path fits your next Toronto multi-family acquisition.

References

[1] Private Mortgages For Toronto Multi Family Investors Capitalizing On 2026 Rental Recovery Trends – https://everythingmortgages.ca/blog/private-mortgages-for-toronto-multi-family-investors-capitalizing-on-2026-rental-recovery-trends/

[3] Toronto 2026 Multifamily Investment Forecast Market Report – https://www.marcusmillichap.com/research/market-report/multiple-markets/toronto-2026-multifamily-investment-forecast-market-report

[7] Spring 2026 Housing Supply Report – https://www.cmhc-schl.gc.ca/media-newsroom/news-releases/2026/spring-2026-housing-supply-report

[8] Watch – https://www.youtube.com/watch?v=PMEJjgmzh78