March 12, 2026

Purpose-Built Rental Financing in Toronto: Why Private Mortgages Are Filling the Gap for Developer Joint Ventures in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s rental housing crisis has reached a tipping point. With vacancy rates near historic lows and demand surging across the GTA, developers are racing to build — but traditional lenders are pumping the brakes. Purpose-Built Rental Financing in Toronto: Why Private Mortgages Are Filling the Gap for Developer Joint Ventures in 2026 has become one of the most urgent conversations in Canadian real estate. Increasingly, developers are partnering with nonprofits and exploring alternative capital structures, while private mortgages emerge as the critical bridge financing tool for projects that big banks view as too complex or too risky.

Key Takeaways 🏗️

- Traditional lenders are pulling back on purpose-built rental (PBR) projects due to tighter OSFI capital rules, leaving a significant financing gap.

- Private mortgages (typically 8–14% rates, 24–48 hour approvals) are stepping in where banks and even CMHC programs fall short in speed and flexibility.

- Joint ventures (JVs) between developers, nonprofits, and private capital are now the dominant structure for getting new rental supply off the ground in Toronto.

- Government incentives — including development charge deferrals, property tax cuts, and CMHC’s 95% loan programs — help but come with long timelines and affordability strings attached.

- 2026 is a pivotal year, with over $1.3 billion in new GTA rental initiatives launched and city-backed programs targeting 7,000+ new rental units.

Toronto’s Rental Supply Crisis: Setting the Stage

Canada’s housing starts rose 6% in 2025, driven largely by record rental apartment construction — yet ownership supply remains under severe pressure [6]. In Toronto specifically, the City has committed $461.1 million to create approximately 7,000 rental units (5,600 of which are purpose-built), with construction starts targeted before the end of 2026 [1].

The numbers tell a compelling story:

| Metric | Detail |

|---|---|

| City of Toronto rental investment | $461.1 million |

| Target new rental units | ~7,000 (5,600 PBRs) |

| High Art Capital initiative | $1.3 billion GTA rental fund |

| BOF mezzanine debt commitment | $300 million |

| Condo units targeted for conversion | 2,200 |

On March 10, 2026, High Art Capital announced a landmark $1.3 billion GTA Rental and Affordable Housing Initiative, anchored by the Building Ontario Fund’s (BOF) $300 million mezzanine debt commitment [2]. The initiative targets converting unsold condos into 2,200 rental units — including affordable workforce housing — signalling a dramatic pivot in how developers are thinking about their asset mix.

💡 Pull Quote: “The shift from condo-first to rental-first development isn’t just a trend — it’s a structural realignment of Toronto’s real estate economy.”

For a broader look at how Toronto’s affordability pressures are reshaping buyer and renter decisions, see this analysis on rental-to-ownership arbitrage in the GTA in 2026.

Why Traditional Lenders Are Stepping Back

OSFI’s Tightening Grip

The Office of the Superintendent of Financial Institutions (OSFI) has significantly tightened its Investment Properties and Real Estate Exposure (IPRRE) rules. These rules force banks to hold more capital against rental property loans, which directly increases the cost and reduces the availability of financing for developers [4].

The practical result? Banks are passing higher rates and stricter terms to borrowers — or declining PBR deals altogether. This creates a structural financing gap that private lenders are uniquely positioned to fill.

Understanding how stress testing works in the Canadian mortgage market is essential context here — these regulatory hurdles apply at every level of the lending stack.

Government Programs: Helpful but Slow

Government-backed options like CMHC’s Apartment Construction Loan Program (ACLP) offer up to 95% financing at low rates — a genuinely powerful tool. But accessing it requires:

- ✅ “Frequent Builder” status with CMHC

- ✅ Weeks or months of approval timelines

- ✅ Meeting specific affordability requirements

- ✅ Navigating complex application processes [1]

Toronto’s Community Housing Pre-Development Fund (CHPF) 2026 offers approximately $10 million in interest-free repayable loans to community housing providers for pre-development work, repayable once capital financing is secured [5]. The ARRCHI 2026 program provides competitive grant funding to close gaps for rent-geared-to-income (RGI) and supportive rentals, prioritizing rapid construction starts [8].

These programs are valuable — but they serve specific borrowers and timelines. For the broader developer market, especially joint ventures with mixed capital structures, the gap remains wide open.

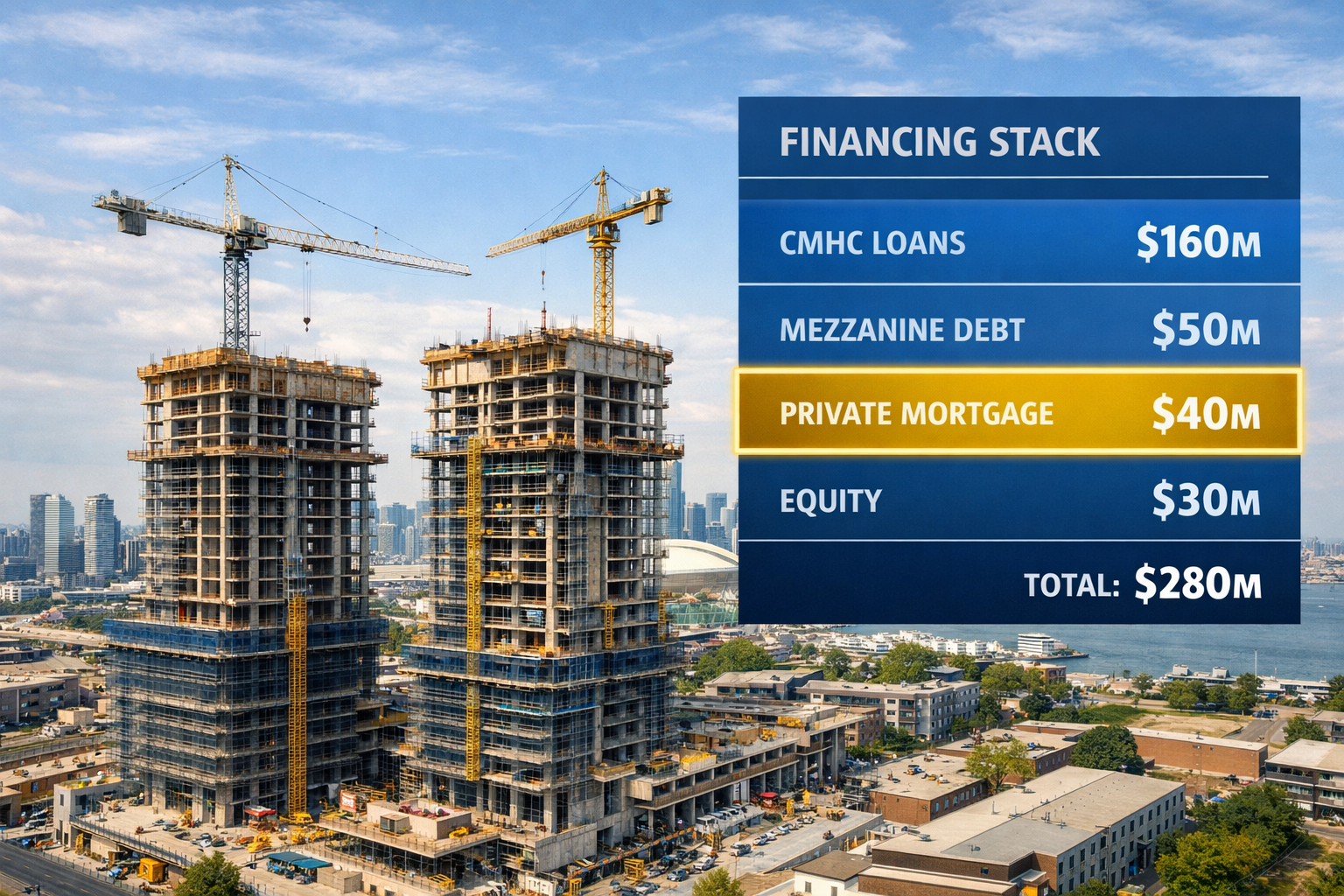

How Private Mortgages Are Filling the Gap for Developer Joint Ventures in 2026

The Private Mortgage Advantage

This is where Purpose-Built Rental Financing in Toronto: Why Private Mortgages Are Filling the Gap for Developer Joint Ventures in 2026 becomes most relevant for practitioners on the ground. Private mortgages offer:

- ⚡ Speed: Approvals in 24–48 hours vs. weeks or months

- 🔄 Flexibility: Custom structures for complex JV arrangements

- 📋 Accessibility: Less rigid qualification requirements than Schedule A banks

- 💰 Rates: Typically 8–14%, reflecting the higher risk profile [1][4]

For developers who need to move quickly — whether to lock in a land deal, bridge to CMHC approval, or fund pre-construction costs — private capital is often the only viable option.

To understand the full landscape of private mortgage approval in Ontario, this detailed resource on private mortgage approval breaks down what lenders actually look for.

Joint Venture Structures: What Developers Need to Know

Miller Thomson’s February 2026 analysis of Canadian real estate JVs highlights key structural considerations [7]:

- Limited Partnerships (LPs) are the most common vehicle, with a General Partner (GP) controlled by JV parties managing operations

- Non-resident investors require “blocker” entities to maintain Canadian partnership status for tax and financing benefits

- Proper structure is critical for accessing both government programs and private financing

💡 Pull Quote: “Getting the JV structure wrong doesn’t just create tax problems — it can disqualify the entire project from both CMHC programs and private lender participation.”

A high-profile example: Dream and CentreCourt’s 49 Ontario Street project secured $647.6 million in government financing plus development charge (DC) waivers for 1,226 units, with 22% designated as affordable [3]. This kind of blended capital stack — government loans + DC incentives + private bridge financing — is becoming the template for large-scale PBR in Toronto.

City Incentives: Real Benefits, Real Strings

Toronto’s PBR incentive package includes:

| Incentive | Details |

|---|---|

| DC deferrals | Indefinite deferrals for qualifying projects |

| Property tax reduction | 15% cut for 35 years on 20,000 PBRs |

| Affordability requirement | 20% affordable units for 40–99 years |

These incentives meaningfully reduce upfront costs [1][9]. But the affordability covenants — locking 20% of units at below-market rents for decades — limit pure-market returns. This is precisely why private capital is often structured as a bridge or mezzanine layer rather than long-term hold financing. Developers use private mortgages to get projects started, then refinance into CMHC or institutional debt once the project stabilizes.

For context on how refinancing strategies work in these scenarios, this comprehensive guide to mortgage refinancing covers the key mechanics.

Practical Implications for Developers and Investors

Who Benefits Most from Private PBR Financing?

Private mortgage solutions for purpose-built rental projects are best suited for:

- JV developers who need bridge capital while awaiting CMHC approval

- Condo-to-rental conversions where traditional lenders see elevated risk

- Smaller developers who don’t qualify for “Frequent Builder” CMHC status

- Mixed-use projects with complex income streams that banks struggle to underwrite

- Nonprofits partnering with private developers who need flexible pre-development financing

The March 2026 panel featuring Starlight Investments emphasized that accelerating PBR construction requires both policy changes and alternative capital structures working in tandem [10]. Private mortgages are not a replacement for government programs — they are a complement that fills timing and structural gaps.

Comparing Financing Options at a Glance

| Feature | Bank/CMHC | Private Mortgage |

|---|---|---|

| Approval speed | Weeks to months | 24–48 hours |

| Max LTV | Up to 95% (CMHC) | Typically 65–80% |

| Rate range | 4–6% (CMHC ACLP) | 8–14% |

| Flexibility | Low | High |

| Qualification | Strict (Frequent Builder) | Asset-based |

| Best for | Stabilized projects | Bridge/pre-construction |

For developers exploring how to structure their equity and debt layers, understanding ADU and condo investment comparisons in Toronto provides useful context on alternative property strategies.

Additionally, developers working with self-employed partners or non-traditional income structures should review how self-employed borrowers can qualify for mortgages in 2026, as JV participants often fall into this category.

Conclusion: Actionable Steps for 2026

Purpose-Built Rental Financing in Toronto: Why Private Mortgages Are Filling the Gap for Developer Joint Ventures in 2026 is not just a headline — it’s a roadmap for how the city’s rental supply crisis will actually get solved. The financing landscape is complex, but the path forward is clear for those who understand the tools available.

Actionable Next Steps 🎯

- Audit your JV structure — Ensure your LP/GP arrangement is optimized for both CMHC eligibility and private lender participation. Get legal advice on blocker entities if non-resident capital is involved.

- Engage a private mortgage broker early — Don’t wait until bank financing falls through. Private bridge capital should be part of the plan from day one.

- Apply for city incentives proactively — DC deferrals and property tax reductions can dramatically improve project economics, even with affordability covenants attached.

- Layer your capital stack — The most successful 2026 PBR projects combine CMHC long-term debt, mezzanine financing (like BOF’s commitment), and private bridge mortgages.

- Monitor CMHC ACLP timelines — If Frequent Builder status is achievable, pursue it. The 95% financing at low rates is transformative for project returns.

The gap between Toronto’s rental housing need and its supply is real — and so is the financing gap that private mortgages are filling. For developers, investors, and JV partners ready to move in 2026, understanding this landscape isn’t optional. It’s the competitive edge.

📞 Ready to explore private mortgage options for your next purpose-built rental project? Connect with the Everything Mortgages team to discuss your financing structure today.

References

[1] Incoming Purpose Built Rentals What This Mean For Investors – https://www.gta-homes.com/real-insights/market/incoming-purpose-built-rentals-what-this-mean-for-investors/

[2] High Art Capital Announces Gta Rental And Affordable Housing Initiative In Partnership With Building Ontario Fund – https://www.newsfilecorp.com/release/288033/High-Art-Capital-Announces-GTA-Rental-and-Affordable-Housing-Initiative-in-Partnership-with-Building-Ontario-Fund

[3] Canada Developer Strategy 2026 – https://storeys.com/canada-developer-strategy-2026/

[4] Toronto Real Estate Osfi Mortgage Crackdown 2026 Toronto Investors – https://www.elevatepartners.ca/resources/toronto-real-estate-osfi-mortgage-crackdown-2026-toronto-investors/

[5] 96ec Chpf 2026 Program Guidelines – https://www.toronto.ca/wp-content/uploads/2026/03/96ec-CHPF-2026-Program-Guidelines.pdf

[6] Spring 2026 Housing Supply Report – https://www.cmhc-schl.gc.ca/media-newsroom/news-releases/2026/spring-2026-housing-supply-report

[7] What Developers And Investors Often Miss In Canadian Real Estate Joint Ventures – https://www.millerthomson.com/en/insights/real-estate/what-developers-and-investors-often-miss-in-canadian-real-estate-joint-ventures/

[8] 9739 2026 Arrchi Program Guidelines – https://www.toronto.ca/wp-content/uploads/2026/03/9739-2026-ARRCHI-Program-Guidelines.pdf

[9] Backgroundfile 249853 – https://www.toronto.ca/legdocs/mmis/2024/ex/bgrd/backgroundfile-249853.pdf

[10] How Canada Can Turn Housing Investments Into More Rental Homes – https://thehub.ca/2026/03/12/how-canada-can-turn-housing-investments-into-more-rental-homes/