February 19, 2026

Rental-to-Ownership Arbitrage: How Strong GTA Rents Are Making First-Time Buyers Reconsider Their Timeline in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

“

The Greater Toronto Area housing market has entered a unique phase in 2026 where an unexpected opportunity is emerging for renters. With rental prices remaining elevated while home prices have softened by 6-7% year-over-year, many first-time buyers are discovering a compelling financial reality: monthly mortgage payments on affordable homes are now comparable to—or even cheaper than—monthly rent[2]. This phenomenon, known as rental-to-ownership arbitrage, is creating a psychological shift that’s accelerating purchase decisions among prospective homebuyers who previously felt locked out of the market.

Despite overall buyer intentions declining to just 22% of GTA residents planning to purchase in 2026, first-time buyers still represent approximately 45% of prospective purchasers[2][5]. This significant segment is now recalculating their timelines as they realize that continuing to rent may cost more than owning, even when factoring in maintenance, property taxes, and other homeownership expenses.

Key Takeaways

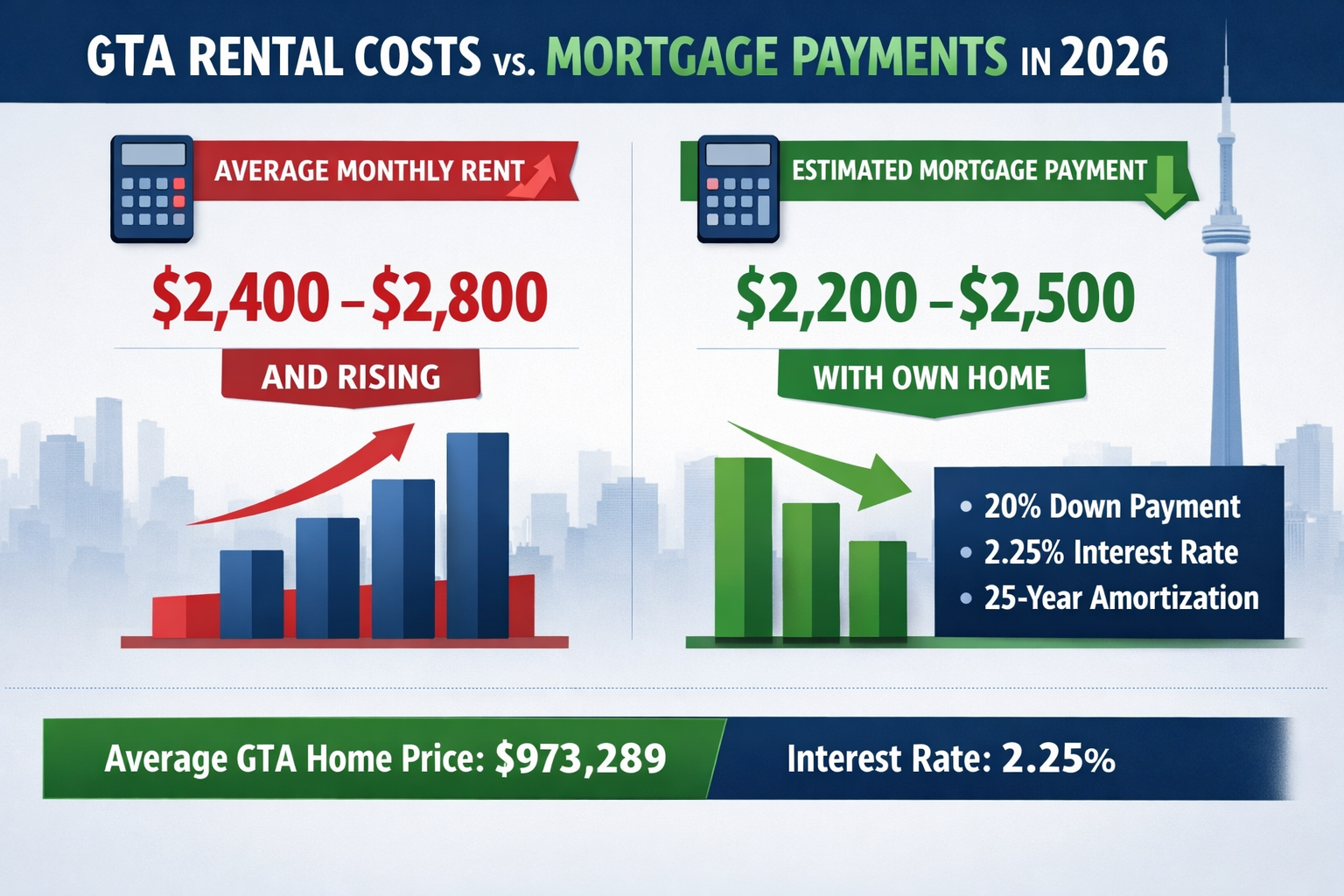

✅ Monthly mortgage payments on GTA homes are now competitive with rental costs, with average home prices at $973,289 and interest rates at 2.25%[2][3]

✅ Home prices have declined 6-7% year-over-year, creating improved affordability conditions for first-time buyers willing to act now[1][2]

✅ Elevated inventory levels give buyers increased negotiating power, particularly in the condominium market where supply has caught up with demand[2]

✅ First-time buyers represent 45% of prospective purchasers in 2026, making them a critical force in the market despite lower overall buyer intentions[2]

✅ Strategic timing and proper financial preparation can help renters transition to ownership and build long-term wealth through home equity

Understanding Rental-to-Ownership Arbitrage in the 2026 GTA Market

Rental-to-ownership arbitrage refers to the financial strategy of recognizing when the cost of homeownership becomes equal to or less than renting, creating an opportunity to build equity instead of paying a landlord. In the current GTA market, this arbitrage opportunity has become particularly pronounced due to several converging factors.

The Current State of GTA Home Prices

The GTA housing market has experienced significant price corrections in recent months. The average selling price currently sits at approximately $973,289, representing a 6.5% decline from January 2025[2]. The MLS Home Price Index has declined approximately 8% year-over-year, signaling a broader softening across multiple property types[2].

This price moderation comes after years of rapid appreciation that pushed homeownership out of reach for many first-time buyers. The mid-$900K average represents a meaningful improvement in affordability, particularly when combined with the Bank of Canada’s interest rate of 2.25%—a level not seen in several years[3].

Rental Market Dynamics

While some segments of the rental market are experiencing temporary relief with incentives like free months and move-in bonuses, particularly in high-density areas where new supply has temporarily outpaced demand[1][3], rental demand remains fundamentally strong. This strength is supported by ongoing immigration and secondary household formation[2].

The rental market faces long-term supply challenges due to planning delays and development costs[2]. Additionally, temporary resident targets face a 43% reduction for 2026, which may affect future rental demand patterns[6]. However, for current renters, the monthly cost of housing remains elevated compared to historical norms.

The Mathematics of Arbitrage

Consider a typical scenario for a first-time buyer in 2026:

| Housing Option | Monthly Cost | Annual Cost | Equity Building |

|---|---|---|---|

| Renting (1-bedroom condo) | $2,400-$2,800 | $28,800-$33,600 | $0 |

| Owning (starter condo/townhouse) | $2,200-$2,600* | $26,400-$31,200 | Yes (principal payments) |

*Includes mortgage payment, property tax, maintenance fees, and basic insurance

This calculation reveals the arbitrage opportunity: renters are often paying the same or more than owners, but receiving zero equity in return. Every month of renting represents a missed opportunity to build wealth through principal reduction and potential property appreciation.

For prospective buyers exploring this transition, understanding the First Time Home Buyer Tax Credit in Canada can provide additional financial benefits that further improve the arbitrage equation.

How Strong GTA Rents Are Making First-Time Buyers Reconsider Their Timeline

The decision to accelerate a home purchase timeline isn’t made lightly. However, several factors specific to 2026 are pushing first-time buyers to reconsider waiting for “perfect” conditions.

The Psychological Shift from Renting to Owning

For years, first-time buyers have been told to “save more” and “wait for better conditions.” However, the current market is creating a fundamental shift in this thinking. When renters realize they’re already paying ownership-level costs without building equity, the psychological barrier to homeownership diminishes significantly.

This shift is particularly powerful because it reframes the purchase decision from “Can I afford to buy?” to “Can I afford NOT to buy?” When monthly costs are comparable, the opportunity cost of continued renting becomes painfully clear.

Inventory Advantages in 2026

One of the most significant advantages for first-time buyers in 2026 is elevated inventory levels, which provide increased negotiating power[2]. Unlike the frenzied seller’s market of previous years, buyers now have time to:

- 🏘️ Compare multiple properties without facing immediate bidding wars

- 💰 Negotiate price reductions and favorable terms

- 🔍 Conduct thorough inspections without waiving conditions

- ⏰ Take time for due diligence before making final decisions

The condominium market, in particular, offers strong opportunities for first-time buyers. With new supply coming online and temporary demand softening, buyers can find well-located units at prices that make the rental-to-ownership arbitrage particularly attractive.

Interest Rate Environment

The Bank of Canada’s current interest rate of 2.25% represents a significant improvement from the higher rates experienced in previous years[3]. This lower rate environment directly impacts affordability by reducing monthly mortgage payments.

For first-time buyers choosing between fixed vs. variable rates, the current environment offers competitive options in both categories. Lower rates mean that the same monthly payment can support a larger mortgage amount, or alternatively, buyers can reduce their monthly costs while maintaining their target purchase price.

The 45% Factor

First-time buyers represent approximately 45% of prospective purchasers in the GTA market[2]. This substantial proportion means that lenders, builders, and sellers are actively competing for this segment’s business. This competition translates to:

- Better mortgage products designed specifically for first-time buyers

- Incentive programs from builders and developers

- More flexible qualification criteria from alternative lenders

- Government programs like the Tax-Free First Home Savings Account

Understanding how 2026 mortgage renewals impact first-time home buyers can also provide insights into market dynamics and timing considerations.

Strategic Considerations for First-Time Buyers Evaluating Rental-to-Ownership Arbitrage

While the arbitrage opportunity is compelling, successful execution requires careful planning and strategic decision-making. First-time buyers must avoid common mistakes that can undermine the financial benefits of homeownership.

Financial Preparation Essentials

Before making the leap from renting to owning, prospective buyers should ensure they have:

1. Adequate Down Payment

The minimum down payment requirements in Canada are:

- 5% for homes up to $500,000

- 10% for the portion between $500,000 and $1,000,000

- 20% for homes over $1,000,000

For a home priced at the current GTA average of $973,289, buyers would need approximately $72,329 as a minimum down payment (5% on first $500K + 10% on remaining $473,289).

2. Emergency Fund

Homeownership comes with unexpected expenses. Financial experts recommend maintaining 3-6 months of housing costs in an accessible emergency fund to cover repairs, maintenance, or temporary income disruptions.

3. Closing Costs

Budget for additional closing costs including:

- Land transfer tax (with potential first-time buyer rebates)

- Legal fees (typically $1,500-$3,000)

- Home inspection ($400-$600)

- Title insurance ($200-$400)

- Moving expenses

Understanding legal fees for Toronto homebuyers helps avoid surprises at closing.

Property Selection Strategy

Not all properties offer equal arbitrage opportunities. First-time buyers should prioritize:

Location Fundamentals 🗺️

- Proximity to transit and employment centers

- Neighborhood stability and appreciation potential

- Access to amenities and services

Property Type Considerations 🏢

- Condos: Lower entry price, but ongoing maintenance fees

- Townhouses: Middle ground between condos and detached homes

- Freehold properties: Higher initial cost, but no condo fees

Future Flexibility 🔄

- Potential for rental income (basement suite, extra bedroom)

- Resale potential in 5-7 years

- Adaptability to changing life circumstances

For buyers considering rental property investment as a future strategy, selecting a property with income potential can provide additional financial flexibility.

Mortgage Qualification Strategy

Qualifying for a mortgage requires meeting specific criteria:

Income Requirements 💼

- Gross Debt Service (GDS) ratio: typically under 39%

- Total Debt Service (TDS) ratio: typically under 44%

- Stable employment history (2+ years preferred)

Credit Requirements 📊

- Minimum credit score: 680+ for best rates (600+ minimum)

- Clean credit history with no recent delinquencies

- Low credit utilization (under 30% of available credit)

Stress Test Compliance 🧮

- Must qualify at the higher of: contract rate + 2% OR 5.25%

- Ensures borrowers can handle rate increases

Working with experienced professionals who understand how to choose the right mortgage lender can significantly improve qualification success.

Timing the Market vs. Time in the Market

A common question among first-time buyers is whether to wait for further price declines or act now. While new-home sales have hit the lowest levels in 45 years[3], suggesting continued market softness, the rental-to-ownership arbitrage framework suggests a different perspective:

The Case for Acting Now:

- Every month of renting is a month of zero equity building

- Interest rates remain favorable and could rise

- Inventory levels provide negotiating leverage

- Price declines may be offset by future appreciation

The Case for Waiting:

- Potential for further price corrections

- Time to save a larger down payment

- Opportunity to improve credit scores

- Market stabilization may provide more certainty

The optimal decision depends on individual circumstances, but the arbitrage opportunity suggests that waiting indefinitely while paying rent equal to ownership costs may be the most expensive option.

Market Outlook and Long-Term Implications for GTA First-Time Buyers

Understanding where the market is heading can help first-time buyers make informed decisions about their rental-to-ownership timeline.

Price Trajectory Forecasts

Market analysts forecast the average GTA selling price to remain in the $1.00M-$1.03M range for 2026[2], suggesting relative stability from current levels around $973,289. This stability creates a predictable environment for planning purchases, unlike the volatile appreciation or depreciation cycles that create uncertainty.

The 6-7% year-over-year price decline has brought homes back to more sustainable valuation levels[1][2]. While further modest declines are possible, particularly in over-supplied segments, dramatic price crashes appear unlikely given:

- Strong underlying demand fundamentals

- Limited new construction starts

- Immigration continuing to support population growth

- Interest rates stabilizing at manageable levels

Supply and Demand Dynamics

The balance between supply and demand will continue to evolve throughout 2026:

Supply Factors:

- Elevated inventory in condominium market

- Slower new construction due to development challenges

- Existing homeowners staying put due to mortgage lock-in effect

- Potential for increased listings if economic uncertainty grows

Demand Factors:

- Only 22% of GTA residents intend to purchase in 2026[2][5]

- First-time buyers representing 45% of this reduced pool[2]

- Temporary resident reductions affecting rental-to-ownership transitions[6]

- Affordability pressures continuing to constrain some buyers[2]

This supply-demand balance suggests a buyer-friendly market with negotiating opportunities, particularly for well-prepared first-time buyers who can act decisively.

Building Long-Term Wealth Through Homeownership

The rental-to-ownership arbitrage isn’t just about monthly cash flow—it’s about long-term wealth creation. Consider the 10-year outlook:

Scenario: First-Time Buyer Purchasing in 2026

- Purchase price: $975,000

- Down payment: $75,000 (7.7%)

- Mortgage: $900,000 at 4.5% over 25 years

- Monthly payment: ~$5,000 (including taxes, fees)

After 10 Years:

- Principal paid down: ~$150,000

- Potential appreciation (2% annually): ~$195,000

- Total equity gain: ~$345,000 (plus original $75,000 down payment)

Rental Alternative:

- Same $5,000/month paid in rent

- Total paid: $600,000

- Equity gained: $0

This simplified comparison illustrates why the rental-to-ownership arbitrage opportunity is so powerful. Even with modest appreciation, homeownership builds substantial wealth through forced savings (principal paydown) and potential appreciation.

Risk Factors to Monitor

While the arbitrage opportunity is compelling, first-time buyers should remain aware of potential risks:

⚠️ Economic Uncertainty

- Recession risks could impact employment and income

- Economic downturns may pressure home values further

⚠️ Interest Rate Volatility

- Variable rate mortgages carry rate increase risk

- Renewal risk for fixed-rate mortgages after term expires

⚠️ Maintenance and Unexpected Costs

- Older properties may require significant repairs

- Condo special assessments can create financial stress

⚠️ Life Flexibility

- Homeownership reduces geographic mobility

- Selling costs (realtor fees, legal costs) can be substantial

⚠️ Market Timing Risk

- Short-term price declines possible

- Illiquidity compared to renting month-to-month

Proper planning, adequate emergency funds, and realistic expectations can mitigate these risks while capturing the arbitrage opportunity.

Actionable Steps for Renters Considering the Transition to Ownership in 2026

For renters who recognize the rental-to-ownership arbitrage opportunity and want to act, here’s a practical roadmap:

Step 1: Assess Your Financial Readiness (Weeks 1-2)

📋 Create a comprehensive financial inventory:

- Calculate current monthly rent and annual housing costs

- Review credit reports from both Equifax and TransUnion

- Determine available savings for down payment and closing costs

- List all debts and monthly obligations

- Calculate debt-to-income ratios

🎯 Set clear financial targets:

- Minimum down payment required for target price range

- Emergency fund goal (6 months of housing costs)

- Credit score improvement targets if needed

- Debt reduction priorities

Step 2: Get Pre-Approved for a Mortgage (Weeks 3-4)

🏦 Connect with mortgage professionals:

- Consult with a mortgage broker who understands first-time buyer needs

- Compare rates and terms from multiple lenders

- Understand the difference between pre-qualification and pre-approval

- Get a formal pre-approval letter with a specific amount

💡 Understand your borrowing capacity:

- Maximum mortgage amount you qualify for

- Comfortable monthly payment based on your budget

- Impact of different down payment amounts

- Options for different mortgage terms and types

Step 3: Define Your Property Criteria (Weeks 4-6)

🏠 Establish clear search parameters:

- Geographic areas that fit your lifestyle and budget

- Property types that match your needs (condo, townhouse, detached)

- Must-have features vs. nice-to-have features

- Maximum price range based on pre-approval

🔍 Research neighborhoods thoroughly:

- Future development plans and infrastructure projects

- School ratings (even if you don’t have children—impacts resale)

- Crime statistics and community safety

- Walkability scores and transit access

- Comparable sales data for realistic pricing expectations

Step 4: Begin Active Property Search (Weeks 6-12)

👀 Implement a systematic search strategy:

- Set up automated alerts on major real estate platforms

- Attend open houses to understand market conditions

- Work with a buyer’s agent who knows the first-time buyer market

- Track properties, price changes, and days on market

- Visit neighborhoods at different times of day

📊 Analyze the rental-to-ownership arbitrage for each property:

- Calculate total monthly ownership costs (mortgage, taxes, fees, insurance)

- Compare to your current rent

- Estimate equity building potential

- Assess appreciation potential based on location and property type

Step 5: Make Strategic Offers (Weeks 12+)

💪 Negotiate from a position of strength:

- Leverage elevated inventory levels for better terms

- Request seller concessions where appropriate

- Include appropriate conditions (financing, inspection, status certificate review)

- Don’t rush—take time for proper due diligence

- Be prepared to walk away if the numbers don’t work

🔎 Complete thorough due diligence:

- Professional home inspection for all property types

- Condo status certificate review (if applicable)

- Title search and survey review

- Final walkthrough before closing

- Verify all representations made by seller

Step 6: Close and Transition to Ownership (Final Weeks)

✅ Finalize all closing requirements:

- Secure homeowner’s insurance

- Arrange for utilities transfer

- Complete final mortgage approval and funding

- Review all closing documents with your lawyer

- Arrange for moving logistics

🎉 Celebrate and plan for success:

- Set up automatic mortgage payments

- Create a home maintenance schedule and budget

- Build your emergency fund if not yet at target

- Consider prepayment options to accelerate equity building

- Review your mortgage annually to ensure it still meets your needs

Common Questions About Rental-to-Ownership Arbitrage in the GTA

Is now really a good time to buy in the GTA?

For first-time buyers who are financially prepared, 2026 presents a unique opportunity. The combination of moderated prices (down 6-7% year-over-year), favorable interest rates (2.25%), and elevated inventory creates conditions that haven’t existed in years[1][2][3]. The rental-to-ownership arbitrage opportunity means that waiting could cost more than buying, particularly if you’re already paying rent equivalent to ownership costs.

What if prices continue to decline?

While further price declines are possible, trying to time the absolute bottom of the market is extremely difficult and often counterproductive. Consider:

- Every month of renting while waiting is a month of zero equity building

- If prices decline another 5%, but you’ve built 5% equity through principal payments, you’re neutral

- Transaction costs mean you need to hold property for 3-5 years regardless

- Long-term appreciation typically outweighs short-term fluctuations

The focus should be on long-term wealth building rather than short-term market timing.

How much do I really need for a down payment?

The minimum down payment depends on the purchase price:

- 5% for the first $500,000 of the purchase price

- 10% for the portion between $500,000 and $1,000,000

- 20% for any portion over $1,000,000

For the current GTA average price of $973,289, you would need approximately $72,329 as a minimum down payment. However, larger down payments reduce monthly costs and eliminate mortgage insurance requirements at 20%+.

What about maintenance costs and unexpected expenses?

Homeownership does involve additional costs beyond the mortgage payment:

- Property taxes: Typically 0.6-1.1% of property value annually in GTA

- Home insurance: $1,000-$2,500 annually depending on coverage

- Maintenance and repairs: Budget 1% of home value annually

- Condo fees: $300-$800+ monthly for condominiums

- Utilities: Often higher than when renting

However, these costs are largely predictable and should be factored into your rental-to-ownership arbitrage calculation. Many of these expenses (particularly maintenance and improvements) also build value in your property.

Can I really compete with investors and experienced buyers?

Absolutely. In fact, first-time buyers have several advantages in the 2026 market:

- Access to first-time buyer programs and incentives

- Lower down payment requirements (5% vs. 20% for investors)

- Emotional connection to properties (willing to pay for “home” not just “investment”)

- Ability to occupy immediately without tenant considerations

- Less likely to be deterred by minor cosmetic issues

The elevated inventory and reduced competition (only 22% of GTA residents planning to purchase) means less competition overall[2][5].

Conclusion: Making Rental-to-Ownership Arbitrage Work for Your Timeline

The 2026 GTA real estate market presents a compelling opportunity for first-time buyers who have been sitting on the sidelines. Rental-to-ownership arbitrage—the recognition that monthly ownership costs are now competitive with rental costs—creates a powerful financial incentive to reconsider purchase timelines.

With home prices down 6-7% year-over-year to an average of $973,289, interest rates at 2.25%, and elevated inventory providing negotiating leverage, the conditions for first-time buyers are the most favorable they’ve been in years[1][2][3]. The fact that first-time buyers represent 45% of prospective purchasers demonstrates that this segment remains a vital force in the market despite overall buyer intentions declining to just 22% of GTA residents[2][5].

The key insight is this: if you’re already paying rent equivalent to ownership costs, every month you delay is a month of missed equity building. While no one can predict the exact bottom of the market, the rental-to-ownership arbitrage framework suggests that waiting for perfect conditions while paying ownership-level rent may be the most expensive option.

Your Next Steps

Ready to explore whether rental-to-ownership arbitrage makes sense for your situation? Here’s what to do:

Calculate your personal arbitrage opportunity by comparing your current rent to estimated ownership costs for properties in your target range

Get pre-approved for a mortgage to understand your exact borrowing capacity and monthly payment obligations

Review available first-time buyer programs including the Tax-Free First Home Savings Account and First Time Home Buyer Tax Credit

Connect with experienced professionals who understand the first-time buyer market and can guide you through the process

Start your property search strategically with clear criteria and realistic expectations

Take action when you find the right opportunity rather than waiting for perfect conditions that may never arrive

The rental-to-ownership arbitrage opportunity in the 2026 GTA market won’t last forever. As market conditions normalize and prices stabilize, the gap between rental costs and ownership costs will likely narrow. First-time buyers who recognize this opportunity and act strategically can position themselves for long-term financial success through homeownership.

Remember: the best time to buy is when you’re financially prepared and the numbers work for your situation. In 2026, for many GTA renters, that time is now.

References

[1] Watch – https://www.youtube.com/watch?v=Cueg_pFxT5U

[2] Trreb 2026 Market Outlook Year In Review What Gta Home Buyers Sellers And Realtors Need To Know – https://keystonera.ca/trreb-2026-market-outlook-year-in-review-what-gta-home-buyers-sellers-and-realtors-need-to-know/

[3] Gta Real Estate Trends 2026 Analysis 2026 01 28 – https://rcibrealestate.ca/gta-real-estate-trends-2026-analysis-2026-01-28/

[4] academic.oup – https://academic.oup.com/restud/advance-article/doi/10.1093/restud/rdaf092/8293019

[5] Gta Home Sales And Prices Expected To Remain Stable In 2026 Amid Ongoing Affordability Pressures 3415 – https://idhomes.today/blog/gta-home-sales-and-prices-expected-to-remain-stable-in-2026-amid-ongoing-affordability-pressures-3415

[6] The 2026 Gta Real Estate Perfect Storm – https://jastan.ca/the-2026-gta-real-estate-perfect-storm/