March 18, 2026

Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage renewal wave of 2026-2027 is approaching fast, and self-employed borrowers in Toronto face unique challenges that traditional employees don’t encounter. With mortgage defaults in the Greater Toronto Area surging 450% in early 2026[2], independent business owners need to take action now to protect their financial futures. The good news? Self-employed mortgage acceleration strategies can help build equity faster, reduce vulnerability to rate shocks, and strengthen your negotiating position when renewal time arrives.

For contractors, consultants, lawyers, and other self-employed professionals, the path to mortgage security looks different than it does for salaried workers. Income fluctuations, business write-offs, and lender scrutiny create additional hurdles—but also unique opportunities. By implementing Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals, independent professionals can transform their mortgage from a source of stress into a wealth-building tool that provides stability during uncertain economic times.

Key Takeaways

✅ Accelerated payment strategies can reduce your mortgage balance by 15-20% faster than standard payment schedules, building crucial equity before the 2026-2027 renewal period

💰 Lump-sum contributions using business profits during high-income months create immediate equity gains and reduce interest costs over the mortgage lifetime

📊 Self-employed borrowers with 20%+ equity gain significantly more negotiating power with lenders and access to better rates during renewal negotiations

⚠️ Three warning signs identified by the Bank of Canada—relying on credit for essentials, exceeding 33% credit utilization, and making minimum payments—signal mortgage delinquency risk[2]

🎯 Strategic documentation of income through gross-up methods and stated-income programs can improve qualification for refinancing and renewal opportunities

Understanding the 2026-2027 Renewal Challenge for Self-Employed Borrowers

The mortgage landscape has shifted dramatically for self-employed professionals in Toronto. Lenders apply heightened scrutiny to self-employed applicants, requiring extensive documentation that demonstrates stable, verifiable income[1]. This creates a perfect storm when combined with the upcoming renewal wave.

Nearly 2,800 families in the Greater Toronto Area have officially defaulted on their mortgages as of early 2026[2], and the situation is expected to intensify as hundreds of thousands of mortgages come up for renewal in 2026 and 2027. For self-employed borrowers, the challenge is twofold:

Higher qualification standards mean that even if you’ve been making payments successfully for five years, your renewal isn’t guaranteed at competitive rates. Lenders will reassess your income using current documentation, and if your reported income has decreased due to business write-offs or market conditions, you may face:

- Higher interest rates (potentially 1-2% above prime lending rates)

- Requests for additional down payments to maintain loan-to-value ratios

- Denial from your current lender, forcing you into alternative lending markets

- Stress test requirements that weren’t applied to your original mortgage

The K-shaped recovery currently underway means that while some high-income buyers are thriving and accessing new CMHC programs for properties in the $1M-$1.5M range, highly leveraged homeowners are hitting financial breaking points[2]. Self-employed borrowers often fall into this vulnerable category due to income volatility.

The solution? Build equity aggressively now, before your renewal date arrives. A stronger equity position transforms you from a risky borrower into an attractive client that lenders compete for.

Understanding how self-employed borrowers in Toronto can navigate the 2026 mortgage stress test is essential preparation for the renewal period ahead.

Core Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals

Building equity faster requires strategic action across multiple fronts. Here are the most effective Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals that independent professionals can implement immediately:

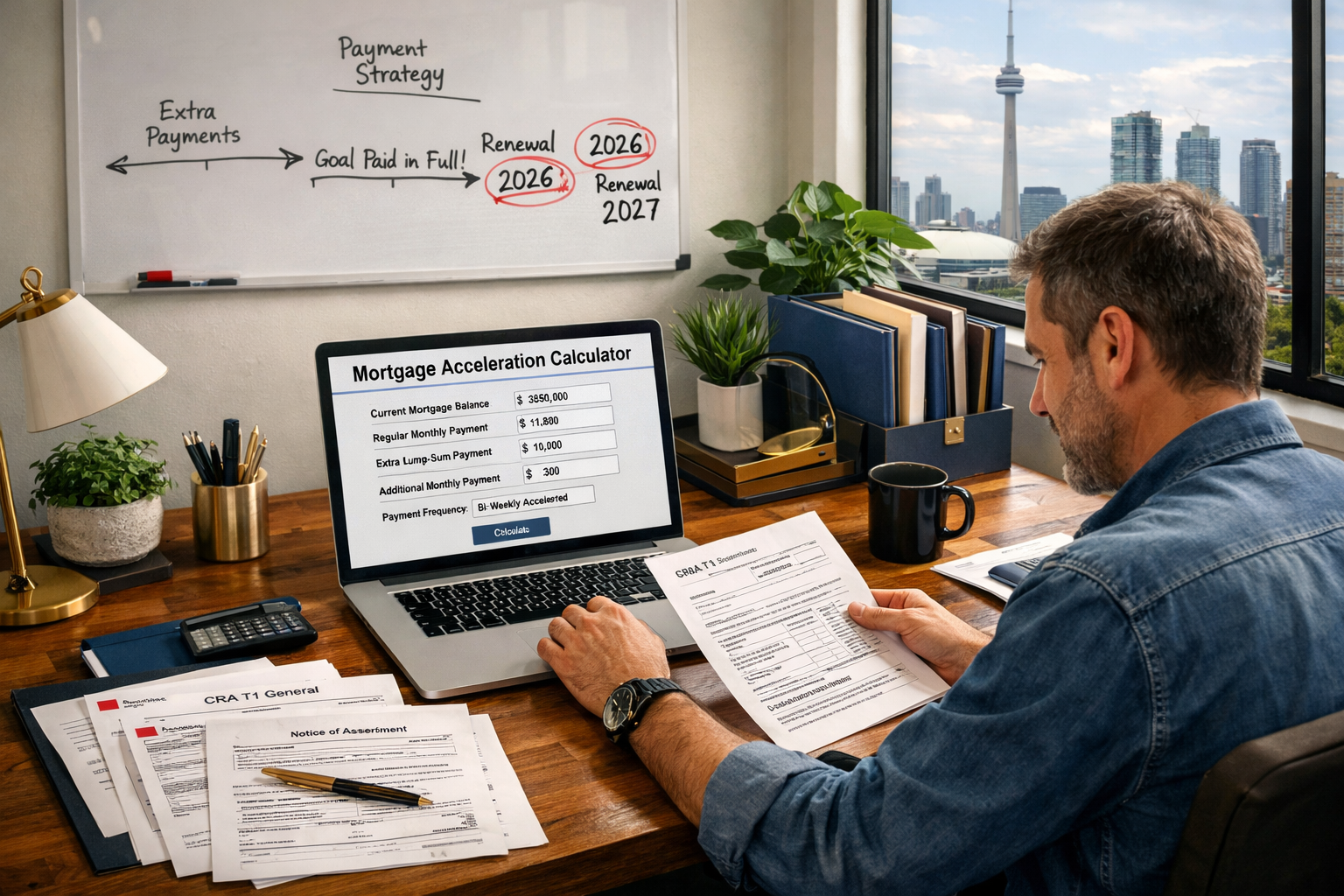

1. Accelerated Bi-Weekly Payment Plans 📅

Instead of making monthly mortgage payments, switch to accelerated bi-weekly payments. This simple change creates 26 half-payments per year (equivalent to 13 full monthly payments instead of 12).

The math: If your monthly payment is $2,500, you’ll pay an extra $2,500 annually—but the impact is far greater than the amount suggests because:

- Extra payments go directly to principal reduction

- Interest calculations decrease with each payment

- Compounding effects accelerate over time

For a $500,000 mortgage at 5.5% over 25 years, accelerated bi-weekly payments can save approximately $45,000 in interest and shave nearly 3 years off your amortization period.

Self-employed advantage: Align your payment schedule with client invoice cycles. If you receive payments bi-weekly or semi-monthly, this strategy ensures mortgage payments happen when cash flow is strongest.

2. Strategic Lump-Sum Contributions 💵

Most mortgages allow annual lump-sum payments of 10-20% of the original principal without penalty. For self-employed professionals with variable income, this is a powerful tool.

Implementation strategy:

- Set aside 15-20% of high-income months into a dedicated “mortgage acceleration account”

- Make your annual lump-sum payment during your highest-earning quarter

- Target the payment for early in the calendar year to maximize interest savings

Example: A contractor who earns $120,000 annually with seasonal peaks could save $15,000 during busy months (May-September) and make a $15,000 lump-sum payment in January. On a $400,000 mortgage balance, this single payment:

- Reduces principal by 3.75% immediately

- Saves approximately $800-1,000 in interest in year one alone

- Compounds over time, potentially saving $12,000-15,000 over the remaining mortgage term

For professionals exploring self-employed mortgages for contractors, understanding prepayment privileges is crucial during the application process.

3. Increase Payment Amounts Annually 📈

Many lenders allow you to increase your regular payment amount by 10-20% annually without penalty. Even modest increases create substantial equity gains.

The 5% annual increase strategy:

If your current mortgage payment is $2,000/month, increase it by just 5% ($100) each year:

- Year 1: $2,000/month

- Year 2: $2,100/month

- Year 3: $2,205/month

- Year 4: $2,315/month

- Year 5: $2,431/month

Over five years, this strategy can reduce your mortgage balance by an additional $18,000-22,000 compared to static payments, depending on your interest rate.

Self-employed timing: Implement payment increases after successful tax years or when you secure long-term contracts that provide income stability.

4. Income Smoothing for Consistent Overpayment 🎯

Self-employed professionals often experience feast-or-famine income cycles. Create an income smoothing system to maintain consistent mortgage acceleration:

- Calculate your average monthly income over the past 24 months

- Pay yourself a consistent “salary” from your business account

- Direct surplus income during high-earning months to mortgage acceleration

- Maintain a 3-6 month emergency fund before implementing aggressive acceleration

This approach provides the dual benefit of consistent mortgage payments (which lenders love to see) while maximizing equity building during profitable periods.

Professionals can learn more about tax smarts and maximizing benefits for the self-employed in Canada to optimize income reporting strategies.

Documentation and Income Optimization for Acceleration Success

Implementing Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals requires more than just making extra payments. You need to document your financial position strategically to maximize refinancing and renewal opportunities.

Three Primary Income Calculation Methods

Lenders use three main approaches to assess self-employed income[1]:

1. Line 150 Average Method

Your net income from CRA forms (Line 150 on T1 General) averaged over 2 years. This is the most conservative approach and often results in the lowest qualifying income.

2. Gross-Up Method

Partial add-back of legitimate business deductions like:

- Depreciation (CCA – Capital Cost Allowance)

- Home office expenses

- Vehicle expenses

- Business meal deductions

This method can increase your qualifying income by 15-30% compared to Line 150, making you eligible for better rates and terms.

3. Stated-Income Programs

Based on bank statements and business statements rather than tax-reported income. These programs recognize that self-employed professionals strategically minimize taxable income while maintaining strong cash flow.

Bank statement mortgages for self-employed borrowers have become increasingly popular in 2026 as lenders recognize the limitations of traditional income verification.

Essential Documentation for Renewal Preparation

Start gathering these documents 12-18 months before your renewal date:

📄 Core Documents:

- 2 years of T1 General tax returns

- 2 years of Notices of Assessment (NOA)

- Business financial statements (profit & loss, balance sheet)

- 6-12 months of business bank statements

- 6-12 months of personal bank statements

📄 Supporting Documents:

- Business registration and incorporation documents

- Client contracts demonstrating recurring revenue

- Accounts receivable aging reports

- Business licenses and professional certifications

- Letter from your accountant confirming income stability

📄 Equity Documentation:

- Recent property appraisal or comparative market analysis

- Records of all accelerated payments and lump-sum contributions

- Mortgage statements showing principal reduction

- Home improvement receipts that increase property value

Pro tip: Create a “renewal preparation folder” (digital or physical) and update it quarterly. This makes the renewal process seamless and demonstrates financial organization to lenders.

For IT consultants and tech professionals, getting a mortgage approved as an IT consultant in Toronto requires understanding how to present contract income effectively.

Optimizing Your Income Presentation

The key to successful renewal isn’t just building equity—it’s presenting your financial picture in the most favorable light:

Balance tax efficiency with mortgage qualification:

While minimizing taxable income saves money on taxes, it can hurt mortgage qualification. Work with your accountant to find the sweet spot where you:

- Maintain reasonable tax efficiency

- Show sufficient income for mortgage purposes

- Document business stability and growth trajectory

Demonstrate income stability:

Even if your income fluctuates, you can show stability through:

- Multi-year contracts with anchor clients

- Diversified client base (not dependent on 1-2 clients)

- Consistent revenue trends over 24-36 months

- Professional credentials that ensure ongoing demand

Highlight business growth:

If your business has grown over your mortgage term, document:

- Revenue increases year-over-year

- Expansion into new markets or service lines

- Addition of team members or contractors

- Investment in business infrastructure

This narrative transforms you from a “risky self-employed borrower” into a “successful business owner with growing income potential.”

Advanced Equity-Building Tactics for Self-Employed Professionals

Beyond basic acceleration strategies, sophisticated self-employed borrowers can implement advanced tactics to maximize equity growth before the 2026-2027 renewal period.

Leveraging Business Structure for Mortgage Advantage

Your business structure impacts both tax efficiency and mortgage qualification:

Incorporated professionals can:

- Pay themselves a strategic mix of salary and dividends

- Retain earnings in the corporation to fund lump-sum payments

- Demonstrate business stability through corporate financial statements

- Access corporate lending products for investment properties

Sole proprietors and partnerships should:

- Consider incorporation if annual revenue exceeds $100,000-150,000

- Document all income sources comprehensively

- Maintain clear separation between business and personal finances

- Build business credit alongside personal credit

For lawyers and legal professionals, self-employed mortgages for lawyers require understanding how to present partnership income and draw structures.

The All-In-One Mortgage Strategy

An all-in-one mortgage (also called a readvanceable mortgage) combines a mortgage, line of credit, and bank account into one product[3]. For self-employed professionals, this offers unique advantages:

How it works:

- Your mortgage, HELOC, and checking account are linked

- As you pay down your mortgage, your available HELOC credit increases

- All income deposits automatically reduce your mortgage balance

- You can redraw funds as needed for business expenses

Benefits for self-employed borrowers:

- Maximize interest savings by keeping all funds against mortgage

- Maintain liquidity for business opportunities or emergencies

- Simplify cash flow management across business and personal finances

- Build equity faster through daily interest calculations

Caution: This strategy requires discipline. It’s best suited for self-employed professionals with:

- Consistent positive cash flow

- Strong financial management skills

- Stable business operations

- Emergency reserves outside the mortgage product

Strategic Refinancing Before Renewal

If you’ve built significant equity through acceleration strategies, consider refinancing 6-12 months before your renewal date rather than waiting:

Advantages:

- Lock in rates before potential increases

- Access better terms with improved loan-to-value ratio

- Consolidate high-interest debt if needed

- Reset your mortgage with optimal terms for the next 5 years

When refinancing makes sense:

- You’ve reduced your LTV to 75% or below (from 85%+)

- Current rates are favorable compared to your renewal rate estimate

- You want to access equity for business investment or debt consolidation

- Your income documentation has improved significantly

Understanding current self-employed mortgage rates in Toronto helps you time refinancing decisions strategically.

Home Equity as Business Capital

Strategic self-employed borrowers recognize that home equity isn’t just about mortgage security—it’s potential business capital:

Conservative approach:

- Build equity to 30-35% through acceleration

- Maintain primary residence as secure asset

- Use equity only for emergency business needs

Growth-oriented approach:

- Build equity to 25-30% through acceleration

- Access HELOC for business expansion opportunities

- Invest in income-generating assets or business growth

- Ensure ROI on borrowed funds exceeds borrowing costs

The key: Never compromise your primary residence security for business risks. Maintain at minimum 20% equity as a safety buffer, and only leverage equity for business purposes with clear ROI projections and risk management plans.

For those considering home equity and how to use it, understanding the difference between HELOC vs. home equity loan options is essential.

Preparing for Your 2026-2027 Renewal: The Equity Advantage

As your renewal date approaches, the equity you’ve built through Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals becomes your most powerful negotiating tool.

The Power of Strong Equity Position

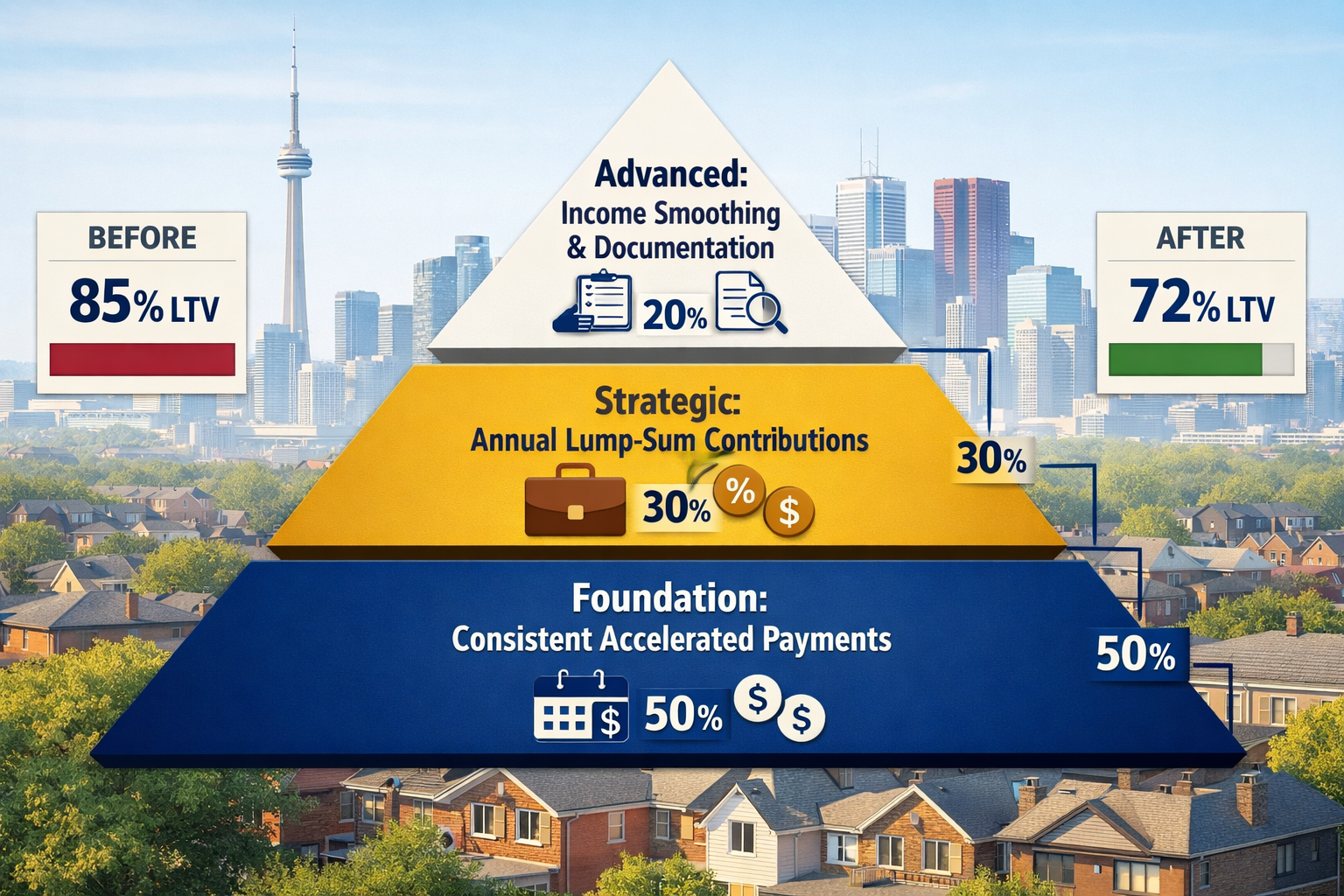

Borrowers with 20%+ equity gain:

✅ Access to A-lender rates – Traditional banks offer their best rates to borrowers with strong equity positions and documented income

✅ Negotiating leverage – Multiple lenders compete for your business when you present low risk

✅ Stress test advantages – Higher equity means lower required income to pass qualification tests

✅ Refinancing options – Ability to switch lenders without penalty if your current lender won’t offer competitive rates

✅ Rate discounts – Many lenders offer 0.10-0.25% rate reductions for borrowers with LTV below 65-70%

The numbers: A self-employed borrower who reduced their mortgage from $450,000 to $360,000 (20% equity gain) on a property worth $500,000 moves from 90% LTV to 72% LTV. This single change can result in:

- 0.50-0.75% better interest rate (saving $2,000-3,000 annually)

- Qualification with A-lenders instead of B-lenders

- Access to better mortgage features (portability, prepayment options)

- Reduced insurance requirements

Working with Mortgage Brokers

Mortgage brokers with self-employed expertise can match borrowers with specialized lenders who value non-traditional income structures[1]. As you approach renewal, a broker can:

🎯 Shop your mortgage across 20-30+ lenders to find optimal rates and terms

🎯 Present your income using the most favorable calculation method (Line 150, gross-up, or stated income)

🎯 Negotiate on your behalf using your strong equity position as leverage

🎯 Access alternative programs not available directly to consumers

🎯 Coordinate timing to ensure seamless transition at renewal without payment disruptions

The value of working with a mortgage broker in Toronto increases significantly for self-employed borrowers due to the complexity of income verification and lender options.

Warning Signs to Address Now

The Bank of Canada has identified three warning signs of mortgage delinquency[2]. If any apply to you, prioritize addressing them before renewal:

⚠️ Relying on consumer credit for essentials (groceries, utilities, basic expenses)

Action: Reduce business expenses, increase prices, or diversify income sources

⚠️ Credit utilization exceeding 33% on credit cards and lines of credit

Action: Implement debt reduction strategy, potentially using lump-sum mortgage funds to pay down high-interest debt first

⚠️ Making only minimum payments on debt obligations

Action: Create debt avalanche or snowball plan, temporarily pause mortgage acceleration to eliminate high-interest debt

Priority order for self-employed financial health:

- Emergency fund (3-6 months expenses)

- High-interest debt elimination (credit cards, unsecured lines)

- Mortgage acceleration (once 1 and 2 are secure)

- Investment and growth (once mortgage is on track)

Renewal Timeline and Action Steps

18 months before renewal:

- Begin gathering documentation

- Implement acceleration strategies

- Review current mortgage terms and prepayment options

12 months before renewal:

- Request property appraisal or CMA

- Calculate equity position

- Begin conversations with mortgage broker

6 months before renewal:

- Receive renewal offer from current lender

- Shop mortgage with broker across multiple lenders

- Compare total costs (not just rates)

3 months before renewal:

- Finalize lender selection

- Complete application and documentation

- Negotiate final terms

1 month before renewal:

- Confirm all details and conditions

- Arrange for seamless transition

- Set up new payment arrangements

Renewal date:

- New mortgage terms take effect

- Celebrate your improved position and lower payments! 🎉

For those interested in broader market trends, understanding 2026 self-employed mortgage rates in Toronto provides context for renewal negotiations.

Conclusion

The 2026-2027 mortgage renewal wave presents both challenges and opportunities for self-employed professionals in Toronto. While defaults have surged and lender scrutiny has intensified, borrowers who implement strategic Self-Employed Mortgage Acceleration Strategies in Toronto: Building Equity Faster to Weather 2026-2027 Renewals can transform their financial position from vulnerable to advantageous.

The core strategies—accelerated bi-weekly payments, strategic lump-sum contributions, annual payment increases, and income smoothing—provide a roadmap for building 15-20% additional equity before renewal. Combined with proper documentation, income optimization, and professional broker support, self-employed borrowers can access competitive rates and favorable terms despite the challenging market conditions.

Your next steps:

1️⃣ Calculate your current equity position and project where you’ll be at renewal with current payments versus accelerated strategies

2️⃣ Implement at least one acceleration strategy immediately – even small changes compound significantly over time

3️⃣ Begin organizing your documentation – create your renewal preparation folder today

4️⃣ Consult with a self-employed mortgage specialist to understand your options and optimize your income presentation

5️⃣ Monitor the three warning signs and address any financial vulnerabilities before they impact your renewal

The equity you build today becomes your negotiating power tomorrow. While you can’t control interest rates or lender policies, you can control your mortgage balance and financial presentation. Self-employed professionals who take proactive action now will enter their 2026-2027 renewals from a position of strength, securing better rates and terms while less-prepared borrowers struggle with limited options.

Don’t wait for your renewal notice to arrive. Start building your equity advantage today.

References

[1] Selfemployed Heres How To Qualify For A Mortgage In 2026 – https://melissadoxey.ca/news-and-events/news/selfemployed-heres-how-to-qualify-for-a-mortgage-in-2026/

[2] Watch – https://www.youtube.com/watch?v=PMEJjgmzh78

[3] All In One Mortgage Solution – https://citadelmortgages.ca/all-in-one-mortgage-solution/