March 20, 2026

Self-Employed Mortgage Qualification Without Minimizing Taxes: How to Prove Income While Growing Your Business

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Self-employed business owners face a unique challenge when applying for mortgages in 2026: lenders want to see high income on tax returns, but savvy entrepreneurs intentionally minimize taxable income to reduce their tax burden. This creates a frustrating catch-22 where the same tax optimization strategies that help grow your business can prevent you from qualifying for your dream home. Understanding Self-Employed Mortgage Qualification Without Minimizing Taxes: How to Prove Income While Growing Your Business is essential for entrepreneurs who want both financial success and homeownership.

The good news? There are proven strategies to demonstrate your true earning power beyond what appears on your Notice of Assessment (NOA). Lenders in 2026 have developed alternative income verification methods specifically designed for self-employed borrowers who reinvest heavily in their businesses. This comprehensive guide reveals how to navigate the mortgage qualification process while maintaining your business growth strategy.

Key Takeaways

- Alternative documentation methods like bank statement programs and CPA letters can prove income beyond tax returns, helping self-employed borrowers qualify without sacrificing tax optimization strategies

- Two years of consistent business history remains the industry standard, but proper documentation of profit trends and client relationships can strengthen applications even with lower reported taxable income

- Strategic timing and preparation including maintaining clean financial records, building strong credit scores, and working with specialized lenders can significantly improve approval odds for growing businesses

- Add-back strategies allow lenders to recalculate income by adding legitimate business deductions back into qualifying income calculations

- Bank statement loan programs offer qualification based on deposits rather than tax returns, providing flexibility for entrepreneurs with significant write-offs

Understanding the Self-Employed Income Dilemma

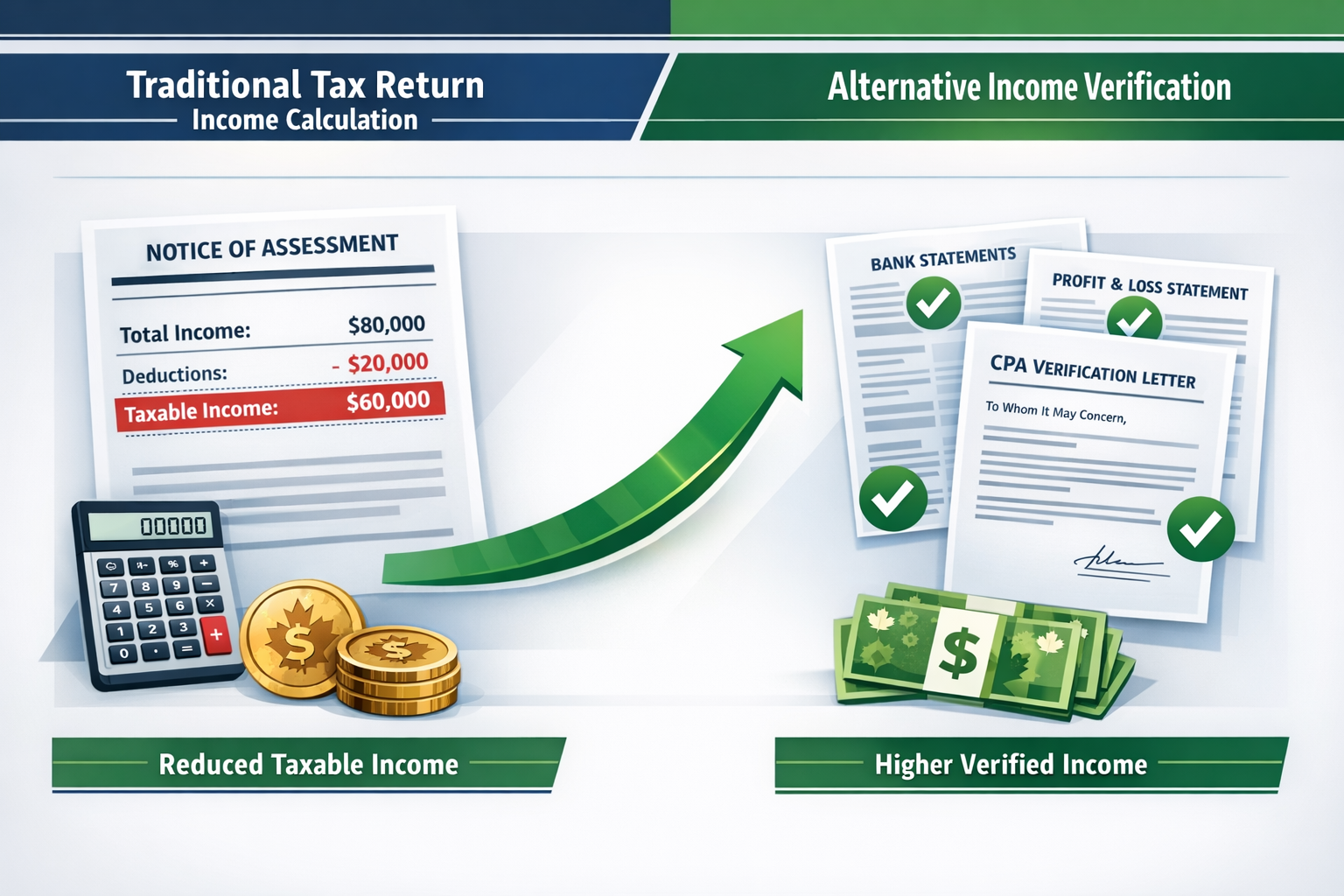

Self-employed professionals, freelancers, and business owners routinely face a fundamental conflict between tax efficiency and mortgage qualification. While traditional employees receive straightforward T4 slips showing gross income, entrepreneurs report net income after deducting legitimate business expenses. These deductions—from home office costs to equipment purchases and travel expenses—reduce taxable income and save thousands in taxes annually.

However, mortgage lenders traditionally assess qualification based on taxable income reported on tax returns. When a business owner writes off $40,000 in legitimate expenses, their taxable income drops by that same amount, potentially disqualifying them from the mortgage they could easily afford based on actual cash flow.

This creates a painful dilemma: Should you minimize deductions to show higher income for mortgage qualification, or continue optimizing taxes at the expense of homeownership goals? The answer in 2026 is that you don’t have to choose one over the other.

How Lenders Calculate Self-Employed Income

Traditional lenders calculate self-employed income by averaging the past two years of net income from tax returns[1]. They examine:

- Personal tax returns (complete with all schedules)

- Business tax returns (Forms 1120, 1120S, 1065, depending on structure)

- Schedule C or Schedule SE showing self-employment income

- Year-to-date profit and loss statements for the current year

The lender takes your net business income (after all deductions) and averages it over 24 months. If your income shows a declining trend, they may weight recent years more heavily or only use the lower year. This conservative approach protects lenders but often underestimates the true financial capacity of growing businesses.

Self-Employed Mortgage Qualification Without Minimizing Taxes: Documentation Strategies That Work

The key to Self-Employed Mortgage Qualification Without Minimizing Taxes: How to Prove Income While Growing Your Business lies in alternative documentation strategies that reveal your actual earning power. These methods have gained significant traction among Canadian lenders who recognize that tax returns don’t tell the complete story for entrepreneurs.

Bank Statement Loan Programs

Bank statement loans have emerged as a game-changer for self-employed borrowers in 2026. Instead of relying solely on tax returns, these programs analyze 12-24 months of personal or business bank statements to calculate income[4]. Lenders examine deposits to determine consistent cash flow and earning capacity.

Key features of bank statement loan programs include:

- Deposit-based qualification: Lenders calculate income from total deposits minus returns and transfers

- Expense ratio application: Typically 50% of deposits count as income (assuming 50% business expenses)

- Higher credit requirements: Minimum scores range from 660-760 depending on the lender

- Larger down payments: Often require 15-20% down payment

- Competitive rates: While slightly higher than conventional mortgages, rates remain reasonable

This approach works exceptionally well for entrepreneurs who show strong cash flow but claim significant tax deductions. Your bank statements reveal the business revenue flowing through your accounts, providing a more accurate picture than net taxable income.

Income Add-Back Strategies

Sophisticated lenders understand that certain business deductions reduce taxable income without affecting your ability to pay a mortgage. Add-back strategies allow underwriters to recalculate qualifying income by adding back legitimate business expenses[2].

Common add-backs include:

| Deduction Type | Why It Adds Back | Impact on Qualification |

|---|---|---|

| Depreciation | Non-cash expense that doesn’t reduce available funds | Can add $5,000-$30,000+ annually |

| Home office deduction | Expense you’ll continue paying as homeowner | Adds $6,000-$15,000 annually |

| Vehicle expenses | Business use continues regardless of mortgage | Adds $8,000-$20,000 annually |

| Meals and entertainment | Discretionary expenses (50% deductible) | Adds $3,000-$10,000 annually |

| Business travel | Can be reduced if necessary | Adds $5,000-$15,000 annually |

By working with lenders who understand add-back calculations, you can potentially increase your qualifying income by $20,000-$50,000 or more without changing your actual tax strategy. This is particularly valuable for those seeking self-employed mortgage rates that remain competitive.

CPA Letters and Professional Verification

A certified accountant’s letter carries significant weight with mortgage underwriters[2][3]. This professional verification provides third-party confirmation of your business operations, income trends, and financial stability.

An effective CPA letter should include:

✅ Confirmation of business operation and your role

✅ Statement of income trends showing stability or growth

✅ Explanation of any income irregularities or seasonal fluctuations

✅ Verification of business legitimacy and ongoing operations

✅ Professional assessment of financial health

This documentation helps humanize your application beyond numbers on tax forms. It demonstrates that a financial professional has reviewed your situation and confirms your ability to handle mortgage payments. Combined with other documentation, CPA letters strengthen applications significantly.

Year-to-Date Profit and Loss Statements

Current-year financial performance matters enormously when qualifying for mortgages. Year-to-date (YTD) profit and loss statements show lenders how your business is performing right now, not just historically[3].

Strong YTD statements can offset lower previous years by demonstrating:

- 📈 Revenue growth compared to the same period last year

- 💰 Improved profit margins from business optimization

- 📊 Consistent monthly performance reducing perceived risk

- 🎯 Seasonal pattern explanations for businesses with cyclical income

Prepare professional YTD statements that clearly show revenue, cost of goods sold, operating expenses, and net profit. These should be prepared by your accountant or using professional accounting software, not handwritten spreadsheets.

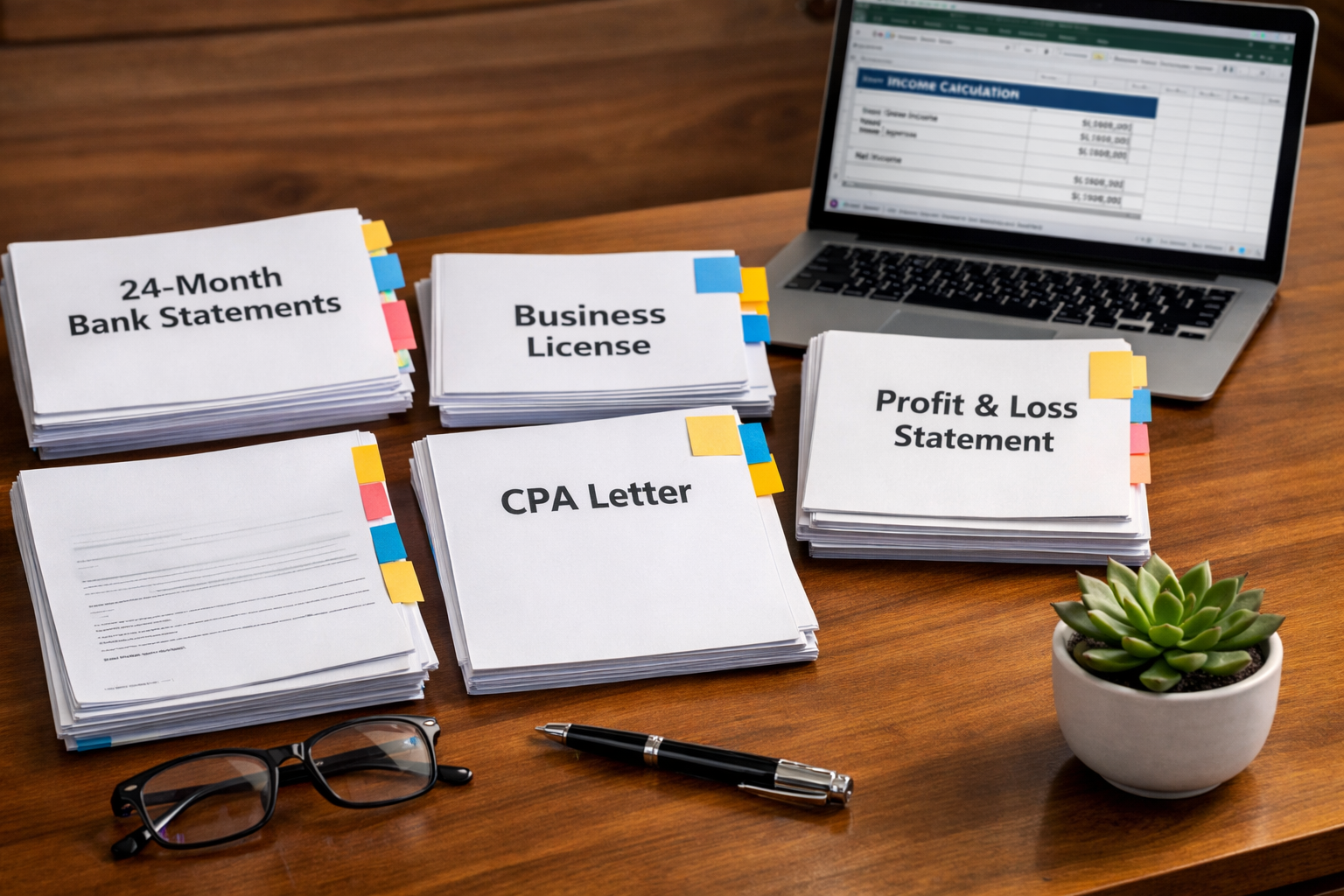

Essential Documentation for Self-Employed Mortgage Applications

Beyond alternative income verification, self-employed applicants must provide comprehensive documentation proving business legitimacy and financial stability. Being prepared with these documents accelerates the approval process and demonstrates professionalism to lenders.

Personal Financial Documents

Personal tax returns remain foundational even when using alternative qualification methods[1][5]. Prepare:

- ✅ Complete personal tax returns for the past two years with all schedules

- ✅ Schedule SE (Self-Employment Tax) showing your business income

- ✅ Notice of Assessment from CRA for both years

- ✅ Personal bank statements for the past 3-6 months

- ✅ Investment account statements showing additional assets

- ✅ Credit report with scores above 660 (ideally 700+)

Maintaining excellent personal credit is crucial. If your score needs improvement, review our guide on how to improve your credit score in Canada before applying.

Business Financial Documents

Comprehensive business documentation proves legitimacy and sustainability[1][5][6]:

- ✅ Business tax returns for two years (T2, T2125, or partnership returns)

- ✅ Business license and registration documents

- ✅ Articles of incorporation or business registration certificates

- ✅ Business bank statements for 12-24 months

- ✅ General ledger and accounting records

- ✅ Accounts receivable aging showing money owed to you

- ✅ Business debt schedules listing all obligations

For those with less than one year of accounts, additional documentation becomes even more critical to demonstrate business viability.

Proof of Business Stability

Lenders want assurance your business will continue generating income throughout the mortgage term. Provide evidence of stability through:

Client contracts and agreements: Long-term contracts or retainer agreements demonstrate predictable income streams[2][3]. Include:

- Current client roster with contact information

- Signed contracts showing future revenue commitments

- Letters from major clients confirming ongoing relationships

- Purchase orders or project agreements

Business continuity evidence: Show your business has staying power:

- Professional liability insurance policies

- Commercial lease agreements for business premises

- Business website and marketing materials

- Industry certifications and professional designations

- Membership in professional associations

Income verification letters: Have major clients provide letters confirming your working relationship and typical project values. These third-party verifications add credibility beyond self-reported information.

Optimizing Your Financial Position for Mortgage Approval

Strategic preparation significantly improves approval odds when pursuing Self-Employed Mortgage Qualification Without Minimizing Taxes: How to Prove Income While Growing Your Business. These optimization strategies work best when implemented 12-24 months before applying.

Strategic Tax Planning for Mortgage Years

While you shouldn’t sacrifice long-term tax efficiency, strategic adjustments during mortgage application years can improve qualification without excessive tax burden:

Timing large deductions: If planning major equipment purchases or renovations, consider timing these expenses for years when you’re not applying for mortgages. Taking $30,000 in equipment deductions the year before applying reduces qualifying income significantly.

Balancing salary and dividends: For incorporated business owners, adjusting the mix between salary (T4 income) and dividends can optimize both tax efficiency and mortgage qualification. Salary income often receives more favorable treatment from lenders.

Documenting add-backs proactively: Keep detailed records of which expenses are add-back eligible. Work with your accountant to clearly separate these on financial statements, making the underwriter’s job easier.

Maintaining consistent income reporting: Avoid dramatic year-to-year fluctuations if possible. Lenders prefer stable or growing income trends over volatile patterns, even if the average is similar.

Building Strong Debt-to-Income Ratios

Your debt-to-income (DTI) ratio represents total monthly debt payments divided by gross monthly income. Most conventional programs require DTI below 43%[1][3], though some lenders accept up to 50% with compensating factors.

Improve your DTI by:

💪 Paying down existing debts: Eliminate or reduce credit card balances, car loans, and personal lines of credit before applying

💪 Avoiding new debt: Don’t take on new financing for vehicles, equipment, or major purchases during the 6-12 months before applying

💪 Increasing qualifying income: Use the alternative documentation strategies discussed earlier to maximize recognized income

💪 Reducing monthly obligations: Consider paying off smaller debts entirely rather than maintaining multiple small monthly payments

Remember that lenders calculate DTI using your qualifying income (which may differ from actual cash flow) and all reported debt obligations. Understanding stress testing requirements helps you prepare for qualification calculations.

Down Payment Strategies

Larger down payments reduce lender risk and can compensate for unconventional income documentation. Self-employed borrowers often benefit from targeting:

- 20% down payment: Avoids mortgage insurance and demonstrates financial discipline

- 25-30% down payment: Significantly improves approval odds with alternative documentation

- Documented savings history: Show funds accumulated over time rather than sudden large deposits

Acceptable down payment sources include:

✅ Personal savings and investment accounts

✅ Sale of existing property

✅ Gift from immediate family (with proper gift letter)

✅ RRSP withdrawal under Home Buyers’ Plan

✅ Sale of business assets (with proper documentation)

Avoid using borrowed funds for down payments, as this creates additional debt obligations and raises red flags with underwriters.

Working With Specialized Lenders

Not all lenders understand self-employed income complexities equally well. Specialized mortgage brokers and lenders who focus on self-employed borrowers offer significant advantages:

🎯 Experience with alternative documentation: They know which programs accept bank statements, add-backs, and CPA letters

🎯 Access to multiple lenders: Brokers can shop your application to lenders most likely to approve your specific situation

🎯 Guidance on documentation: They help you prepare the strongest possible application package

🎯 Problem-solving expertise: When challenges arise, experienced specialists find creative solutions

Consider exploring alternative income verification options and understanding the five key things about self-employed mortgages before beginning your search.

Common Mistakes to Avoid

Even well-prepared self-employed applicants make critical errors that derail mortgage applications. Avoid these common pitfalls:

Mixing Personal and Business Finances

Separate bank accounts are essential for clean documentation. When personal and business transactions mix in the same account, lenders struggle to calculate actual business income. This creates confusion and often results in conservative income calculations that work against you.

Establish dedicated business accounts at least 12-24 months before applying for mortgages. This separation also simplifies tax preparation and provides cleaner documentation for underwriters.

Inconsistent Income Reporting

Discrepancies between bank statements, tax returns, and profit/loss statements raise red flags. Ensure all documentation tells a consistent story:

- Bank deposits should align with reported revenue

- P&L statements should match tax return figures

- Explanations should accompany any discrepancies

- Large one-time deposits should be clearly documented

Applying Too Soon After Business Changes

Major business transitions create uncertainty for lenders. Avoid applying immediately after:

- ❌ Changing business structure (sole proprietor to corporation)

- ❌ Switching industries or primary business focus

- ❌ Significant business expansion or contraction

- ❌ Adding or losing major clients

Wait 12-24 months after major changes to establish a track record in your new situation. If you must apply sooner, provide extensive documentation explaining the transition and demonstrating stability.

Neglecting Credit Management

Self-employed applicants need excellent credit scores to compensate for income documentation challenges[2]. Minimum scores typically start at 620 for conventional loans, but 700+ significantly improves approval odds and rate offerings.

Protect your credit by:

- Paying all obligations on time without exception

- Keeping credit utilization below 30% of limits

- Avoiding new credit inquiries before applying

- Correcting any errors on credit reports immediately

- Maintaining older credit accounts for history length

Timeline and Preparation Strategy

Successful self-employed mortgage qualification requires strategic planning well before you’re ready to purchase. Follow this timeline for optimal results:

24 Months Before Application

- 📅 Establish separate business and personal bank accounts

- 📅 Begin working with a qualified accountant familiar with mortgage qualification

- 📅 Document all income sources and maintain organized records

- 📅 Review credit reports and begin improvement strategies

- 📅 Research lenders who specialize in self-employed mortgages

12 Months Before Application

- 📅 Optimize tax strategy balancing efficiency with qualification needs

- 📅 Build emergency fund and down payment savings

- 📅 Obtain business licenses and professional certifications

- 📅 Establish relationships with major clients and request letters

- 📅 Pay down existing debts to improve DTI ratio

6 Months Before Application

- 📅 Consult with specialized mortgage broker

- 📅 Prepare preliminary documentation package

- 📅 Request CPA letter outlining business stability

- 📅 Compile year-to-date profit and loss statements

- 📅 Avoid major business or personal financial changes

3 Months Before Application

- 📅 Obtain mortgage pre-approval to understand qualification amount

- 📅 Finalize documentation package with all required materials

- 📅 Ensure all bank statements show consistent deposits

- 📅 Confirm credit scores meet lender requirements

- 📅 Begin serious property search within qualified budget

Application Time

- 📅 Submit complete documentation package

- 📅 Respond promptly to any underwriter requests

- 📅 Maintain stable business operations throughout process

- 📅 Avoid making major purchases or taking on new debt

- 📅 Keep all financial accounts current and in good standing

Understanding what to expect during the mortgage process helps you navigate each stage confidently.

Alternative Mortgage Options for Self-Employed Borrowers

When traditional qualification proves challenging despite alternative documentation, several backup options exist:

Stated Income Programs

Some private lenders offer stated income mortgages where you declare your income without extensive documentation. These programs typically require:

- Larger down payments (25-35%)

- Higher interest rates (2-4% above conventional rates)

- Shorter terms (1-2 years before refinancing)

- Strong credit scores (680+)

While more expensive, stated income programs can bridge the gap until you establish sufficient documentation for conventional financing. Learn more about how to get a mortgage without traditional income verification.

Co-Signer or Co-Borrower Strategies

Adding a co-signer with traditional employment income can strengthen applications significantly. The co-signer’s income supplements yours for qualification purposes, though they assume equal responsibility for the mortgage.

Consider co-signing arrangements carefully, ensuring all parties understand obligations and implications.

Portfolio Lenders

Portfolio lenders keep mortgages on their own books rather than selling them to secondary markets. This flexibility allows more creative underwriting approaches and consideration of factors beyond standard guidelines.

Portfolio lenders may accept:

- Unique income documentation packages

- Non-traditional employment situations

- Complex business structures

- Compensating factors like substantial assets

Private Mortgages

As a last resort, Private Mortgages offer qualification based primarily on property equity rather than income verification. While expensive (rates of 7-12%), they provide short-term solutions while you build conventional qualification credentials.

Private mortgages work best as 1-2 year bridges, not long-term financing solutions.

Conclusion

Navigating Self-Employed Mortgage Qualification Without Minimizing Taxes: How to Prove Income While Growing Your Business requires strategic planning, comprehensive documentation, and working with lenders who understand entrepreneurial finances. The traditional conflict between tax optimization and mortgage qualification no longer needs to prevent homeownership.

By leveraging alternative documentation methods—including bank statement programs, income add-backs, CPA verification letters, and current profit and loss statements—self-employed borrowers can demonstrate true earning capacity beyond what appears on tax returns. These strategies allow you to maintain tax-efficient business operations while qualifying for competitive mortgage rates.

Success requires preparation starting 12-24 months before application, maintaining organized financial records, building strong credit profiles, and working with specialized mortgage professionals who understand self-employed income complexities. The documentation burden is heavier than for traditional employees, but the reward is homeownership without sacrificing business growth strategies.

Your Next Steps

Take action today to position yourself for mortgage approval:

- Assess your current documentation: Review what you have and identify gaps in your financial records

- Consult with specialists: Connect with accountants and mortgage brokers experienced in self-employed financing

- Implement financial separation: Establish dedicated business accounts if you haven’t already

- Build your documentation package: Begin compiling the comprehensive materials lenders require

- Optimize your credit profile: Address any credit issues and maintain excellent payment history

- Research lender options: Identify which lenders offer the programs best suited to your situation

Remember that establishing the right financial mindset supports both business success and homeownership goals. With proper preparation and the right guidance, self-employed professionals can secure excellent mortgage terms while continuing to grow thriving businesses.

The path to homeownership as a self-employed borrower in 2026 is clearer than ever before. Take the first step today by organizing your documentation and connecting with professionals who specialize in helping entrepreneurs achieve their real estate goals.

References

[1] Self Employed Mortgage – https://www.rocketmortgage.com/learn/self-employed-mortgage

[2] Calculating Self Employed Income For Mortgage – https://mymortgageinsider.com/calculating-self-employed-income-for-mortgage/

[3] Qualifying Mortgage When Youre Self Employed – https://myhome.freddiemac.com/blog/homebuying/qualifying-mortgage-when-youre-self-employed

[4] Selfemployed Mortgage Guide For Strategies To Get Approved – https://www.amerisave.com/learn/selfemployed-mortgage-guide-for-strategies-to-get-approved

[5] What Documents Do Self Employed Need For Mortgage – https://www.chase.com/personal/mortgage/education/buying-a-home/what-documents-do-self-employed-need-for-mortgage

[6] Mortgage Self Employed – https://www.wellsfargo.com/mortgage/learn/mortgage-self-employed/