February 9, 2026

Self-Employed Mortgage Rates 2026: Expected Trends and How to Lock in the Best Rate

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage landscape for self-employed borrowers is shifting dramatically as 2026 unfolds. Industry experts predict that 30-year fixed mortgage rates will average between 5.9% and 6.2% in 2026, representing a significant improvement from the higher rates experienced in 2025[3]. Understanding Self-Employed Mortgage Rates 2026: Expected Trends and How to Lock in the Best Rate is crucial for entrepreneurs, freelancers, and business owners planning to purchase or refinance their homes this year.

Self-employed borrowers face unique challenges in the mortgage market, from stricter documentation requirements to higher credit score standards. However, with mortgage rates trending downward and innovative lending solutions emerging, 2026 presents promising opportunities for those who understand how to navigate the system strategically.

Key Takeaways

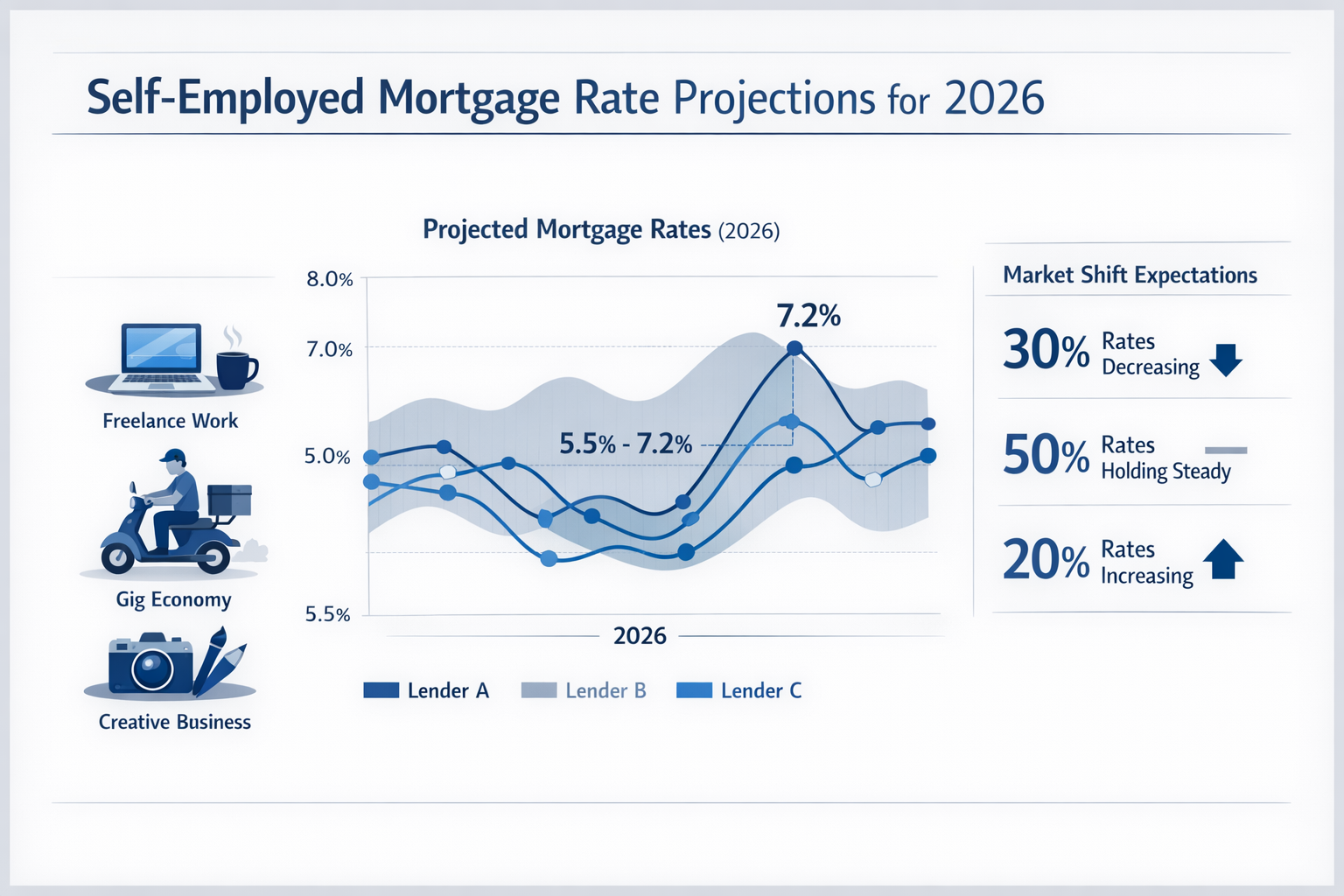

✅ Major lenders forecast rates between 5.9-6.4% for 2026, with Fannie Mae predicting 6.0% and the Mortgage Bankers Association expecting 6.4%[3]

✅ Self-employed borrowers need higher credit scores (620+ vs. 580 for traditional employees) and larger down payments (10-40% depending on loan type)[1]

✅ Bank statement loans can increase qualifying income by up to $80,000 in purchasing power compared to tax return documentation alone[1]

✅ Cash reserves of 2-6 months are required by most lenders, with 6-12 months recommended for financial security[1]

✅ Timing your application strategically during favorable rate periods and preparing documentation in advance can save thousands over the loan term

Understanding Self-Employed Mortgage Rates 2026: Expected Trends From Major Lenders

The consensus among financial institutions points to moderating mortgage rates throughout 2026, though predictions vary slightly based on economic assumptions and market analysis methodologies.

What Leading Institutions Predict

Fannie Mae has positioned itself as one of the more optimistic forecasters, projecting that 30-year fixed mortgage rates will average 6.0% in 2026, with further declines to 5.9% expected in 2027[3]. This forecast reflects expectations of continued Federal Reserve policy adjustments and stabilizing inflation.

The National Association of Home Builders offers a slightly higher prediction at 6.17% for 2026, declining to 6.01% in 2027[3]. Their forecast incorporates construction industry dynamics and housing supply considerations that influence overall market conditions.

Taking a more conservative stance, the Mortgage Bankers Association expects rates to settle at 6.4% in 2026 and 2027, with a modest increase to 6.5% projected for 2028[3]. This perspective accounts for persistent economic uncertainties and potential inflationary pressures.

Redfin, analyzing consumer behavior and real estate market trends, predicts rates will average 6.3% for 2026[3], positioning their forecast in the middle range of expert predictions.

Current Rate Environment

As of the fourth quarter of 2025, the average 30-year fixed mortgage rate stood at 6.24%[3], providing a baseline for understanding 2026 trends. For the week of February 5-11, 2026, market analysts predicted a 63% likelihood that rates would remain unchanged, with 25% expecting declines and only 13% anticipating increases[4].

This stability suggests that self-employed borrowers have a relatively predictable environment for planning their mortgage applications, though monitoring weekly fluctuations remains important for optimal timing.

Factors Driving Rate Trends

Several macroeconomic factors influence the mortgage rate forecasts for 2026:

📊 Federal Reserve Policy: Central bank decisions on interest rates directly impact mortgage pricing. As inflation moderates, the Fed’s approach to monetary policy becomes more accommodative, supporting lower mortgage rates.

🏠 Housing Market Dynamics: Supply and demand imbalances in the housing market create pressure on rates. Limited inventory and sustained buyer demand can keep rates elevated despite broader economic trends.

💼 Economic Growth Indicators: GDP growth, employment data, and consumer spending patterns all contribute to lender confidence and rate-setting decisions.

🌍 Global Economic Conditions: International market volatility, geopolitical events, and foreign investment flows affect U.S. Treasury yields, which mortgage rates closely track.

For self-employed borrowers specifically, understanding these trends helps contextualize why fixed mortgage rates may not always follow Bank of Canada cuts and similar central bank actions.

How Self-Employed Status Affects Your Mortgage Rate and Qualification

Self-employed borrowers encounter distinct challenges that can impact both the rates they’re offered and their ability to qualify for mortgages. Understanding these differences is essential for developing an effective application strategy.

Higher Credit Score Requirements

Credit score standards are significantly more stringent for self-employed applicants. Most FHA lenders require credit scores of at least 600-620 for self-employed borrowers, compared to the standard 580 minimum for W-2 employees[1]. This higher threshold exists because lenders view the combination of variable income and lower credit scores as compounding risk factors.

Conventional loan programs typically expect self-employed borrowers to maintain scores of 640 or higher for competitive rates, with the best rates reserved for those with scores above 740. Each 20-point increment in credit score can translate to rate differences of 0.25-0.50%, representing thousands of dollars over the loan term.

Down Payment Expectations

Down payment minimums are more substantial for self-employed borrowers compared to traditional employees. While conventional loans for W-2 workers may accept as little as 3% down through certain programs, self-employed applicants typically need 5-10% down for conventional financing[1].

Bank statement loan programs, which offer alternative documentation pathways for self-employed borrowers, usually require 10-40% down depending on several factors[1]:

- Credit score: Lower scores necessitate larger down payments

- Loan amount: Jumbo loans require higher equity contributions

- Property type: Investment properties demand more substantial down payments than primary residences

- Income documentation method: Alternative documentation typically requires more skin in the game

These higher down payment requirements serve dual purposes: they reduce lender risk and demonstrate the borrower’s financial capacity and commitment to the property.

Debt-to-Income Ratio Considerations

Interestingly, debt-to-income (DTI) ratio requirements remain comparable between self-employed and traditionally employed borrowers. Conventional loans typically cap DTI at 43-50%, while FHA loans may permit ratios up to 50-57% with compensating factors such as substantial cash reserves or exceptional credit history[1].

However, the calculation of income for DTI purposes differs significantly for self-employed borrowers. Lenders typically average two years of tax returns, deducting business expenses to arrive at qualifying income. This methodology often results in lower qualifying income than actual cash flow, making the DTI calculation more restrictive in practice.

Cash Reserve Requirements

Substantial cash reserves are essential for self-employed mortgage approval. Lenders typically require self-employed borrowers to maintain 2-6 months of mortgage payments in accessible savings beyond the down payment and closing costs[1].

For example, if monthly mortgage payments total $2,000, borrowers need $4,000-$12,000 in reserves after closing. These funds must be in liquid accounts—not retirement funds subject to withdrawal penalties—and documented through bank statements.

Beyond minimum requirements, financial advisors recommend self-employed borrowers maintain 6-12 months of additional reserves to protect against income disruptions inherent in self-employment[1]. This cushion provides peace of mind for both borrower and lender.

Income Documentation Challenges and Solutions

Traditional mortgage underwriting relies heavily on W-2 forms and pay stubs, which self-employed borrowers cannot provide. Instead, lenders require:

📄 Two years of personal tax returns with all schedules 📄 Two years of business tax returns (for incorporated businesses) 📄 Year-to-date profit and loss statements 📄 Business license and proof of ongoing operations 📄 Bank statements (personal and business)

The challenge arises because many self-employed individuals legitimately minimize taxable income through business deductions, reducing their qualifying income for mortgage purposes. Our guide on mortgages for self-employed borrowers explores these documentation requirements in detail.

Bank statement loan programs offer an innovative solution. These programs analyze bank deposits and cash flow rather than tax returns, applying an expense factor (typically 40-50%) to gross deposits to calculate qualifying income[1].

This approach can dramatically increase purchasing power. A borrower with $180,000 in annual bank deposits using a 40% expense factor could qualify with $9,000 monthly income ($180,000 × 0.60 ÷ 12), compared to just $5,417 shown on tax returns. This difference represents approximately $80,000 more in purchasing power[1].

For specialized professionals, self-employed mortgages for doctors and other high-income professionals offer additional tailored solutions.

Strategies to Lock in the Best Self-Employed Mortgage Rates in 2026

Securing optimal mortgage rates requires strategic preparation, timing, and understanding of available loan products. Self-employed borrowers who implement these strategies position themselves for the most favorable terms.

Optimize Your Credit Profile

Credit score improvement delivers the most significant impact on mortgage rates. For self-employed borrowers starting below 700, every point gained translates to better rate options.

Immediate actions to boost credit scores:

🔹 Pay down credit card balances below 30% of limits (ideally under 10%) 🔹 Dispute inaccuracies on credit reports through all three bureaus 🔹 Avoid new credit applications for 6-12 months before applying 🔹 Maintain perfect payment history on all existing accounts 🔹 Keep old accounts open to preserve credit history length 🔹 Become an authorized user on accounts with excellent payment history

Starting this process 12-18 months before applying allows time for meaningful improvements to reflect in credit scores.

Prepare Comprehensive Documentation

Documentation preparation distinguishes successful self-employed applications from rejected ones. Lenders scrutinize self-employed income more carefully, making organization critical.

Essential documentation checklist:

✅ Two years of complete personal tax returns (all schedules) ✅ Two years of business tax returns (if applicable) ✅ Year-to-date profit and loss statement ✅ 12-24 months of business bank statements ✅ 12-24 months of personal bank statements ✅ Business license and articles of incorporation ✅ CPA letter verifying income and business continuity ✅ Client contracts demonstrating ongoing revenue ✅ Explanation letters for income fluctuations

Organizing these documents in advance accelerates the underwriting process and demonstrates professionalism to lenders. Our mortgage document checklist provides additional guidance.

Build Substantial Cash Reserves

Cash reserves serve multiple strategic purposes: meeting lender requirements, demonstrating financial stability, and providing genuine protection against income variability.

Target reserve levels should include:

Minimum tier: 2-6 months of mortgage payments (lender requirement) Recommended tier: 6-12 months of total housing expenses Optimal tier: 12-24 months of all obligations

These reserves should be maintained in liquid accounts such as savings, checking, or money market accounts. While retirement accounts can sometimes count toward reserves, they carry restrictions that limit their utility.

Self-employed borrowers should also maintain separate reserves for business operations, ensuring mortgage reserves remain untouched even during business fluctuations.

Consider Alternative Loan Programs

Bank statement loan programs represent the most significant innovation for self-employed borrowers in recent years. These programs offer several advantages:

💡 Income calculation based on deposits rather than tax returns 💡 Faster approval processes with less documentation 💡 Flexibility for borrowers who write off substantial business expenses 💡 Competitive rates for borrowers with strong credit and down payments

However, bank statement loans typically require larger down payments (10-40%) and may carry slightly higher rates than conventional programs. The trade-off often proves worthwhile for borrowers whose tax returns understate actual cash flow.

Stated income programs have re-emerged in limited forms through certain lenders, though with much stricter requirements than pre-2008 versions. These programs suit borrowers with complex income structures or significant assets relative to income.

For those exploring various options, reviewing innovative mortgage solutions for self-employed Canadians provides valuable insights into emerging products.

Time Your Application Strategically

Rate timing can save thousands over the loan term. While perfectly timing the market proves impossible, certain strategies improve odds of securing favorable rates:

Monitor rate trends weekly: Rates fluctuate based on economic data releases, Federal Reserve announcements, and market sentiment. Following weekly trends helps identify favorable application windows.

Consider rate lock options: Once approved, rate locks (typically 30-60 days) protect against increases during the closing process. Extended locks may carry fees but provide certainty.

Evaluate fixed vs. variable rates: With rates expected to decline gradually through 2026-2027, some borrowers may benefit from variable rate products that adjust downward. However, this strategy carries risk if economic conditions change. Our guide on fixed vs. variable rates explores this decision framework.

Seasonal considerations: Mortgage application volume affects processing times and sometimes pricing. Applying during slower periods (typically late fall and winter) may result in faster processing and more lender attention to your application.

Work with Specialized Lenders

Lender selection significantly impacts approval odds and rate offerings for self-employed borrowers. Not all lenders maintain equal expertise or appetite for self-employed applications.

Mortgage brokers specializing in self-employed borrowers access multiple lender programs and understand which underwriters offer the most favorable terms for specific situations. They can match borrower profiles with lenders most likely to approve and offer competitive rates.

Portfolio lenders keep loans on their own books rather than selling them to secondary markets, allowing more flexibility in underwriting standards. These lenders may accommodate unique income documentation or property types that conventional lenders reject.

Credit unions sometimes offer more personalized underwriting for self-employed members, particularly those with established banking relationships and strong deposit histories.

When obtaining a mortgage when you’re self-employed, the right lender partnership makes all the difference.

Maximize Qualifying Income

Income maximization strategies help self-employed borrowers qualify for larger loan amounts without changing actual earnings:

Timing income recognition: If possible, accelerate income into the current tax year to boost qualifying income averages.

Minimizing non-cash deductions: Depreciation and other non-cash expenses reduce taxable income but don’t represent actual cash outflows. Some lenders add back certain non-cash deductions when calculating qualifying income.

Documenting income trends: If income is increasing year-over-year, providing context and documentation of growth trajectories can influence underwriter decisions.

Combining household income: If applying jointly, ensure both incomes are properly documented and included in qualification calculations.

Considering asset-based qualification: Some programs qualify borrowers based on liquid assets rather than income, suitable for high-net-worth individuals with variable income.

Understand Rate Adjustment Factors

Rate adjustments beyond base rates affect the actual rate offered to individual borrowers. Understanding these factors helps set realistic expectations:

| Factor | Potential Rate Impact | Mitigation Strategy |

|---|---|---|

| Credit Score < 740 | +0.25% to +1.00% | Improve score before applying |

| Down Payment < 20% | +0.25% to +0.50% | Increase down payment or accept PMI |

| Cash-Out Refinance | +0.375% to +0.625% | Consider HELOC alternative |

| Investment Property | +0.50% to +1.00% | Maximize down payment |

| Condo (vs. Single-Family) | +0.125% to +0.25% | Ensure HOA meets lender requirements |

| Loan Amount > Conforming Limit | +0.25% to +0.75% | Consider conforming loan if possible |

Self-employed borrowers should focus on factors within their control—primarily credit score, down payment, and cash reserves—to minimize rate adjustments.

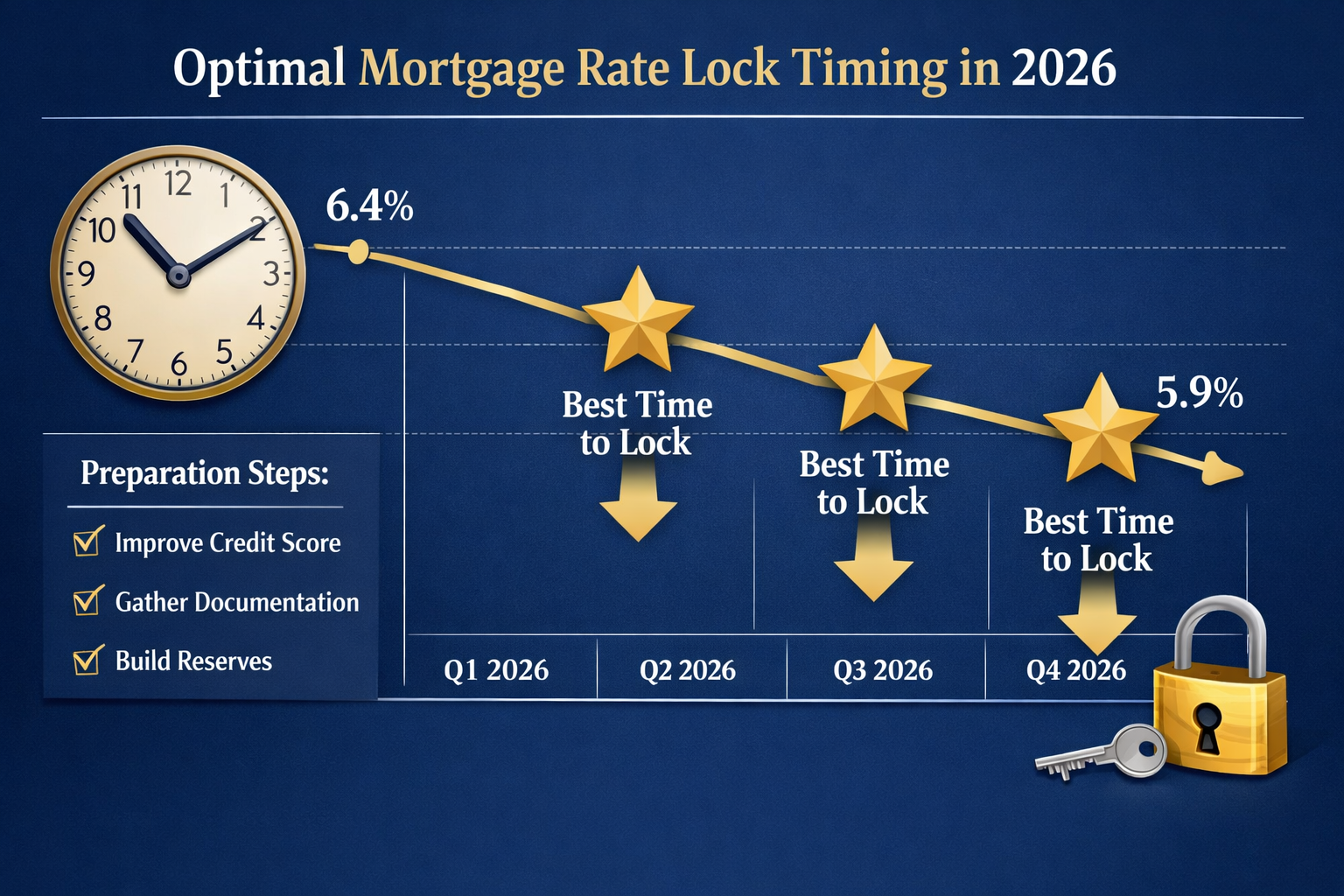

Lock in Rates at Optimal Times

Rate lock timing balances protection against increases with flexibility to capture decreases. Standard rate locks last 30-60 days, covering typical closing periods.

Float-down options allow borrowers to lock a rate but capture lower rates if they decline before closing, usually for a fee of 0.25-0.50% of the loan amount. This option suits borrowers applying during periods of rate volatility or expected decline.

Extended locks (90-120 days) accommodate longer closing timelines for new construction or complex transactions, though they typically carry fees of 0.125-0.25% per 30-day extension.

Given that expert forecasts suggest 63% likelihood of stable rates in early 2026[4], borrowers approved during favorable rate periods should consider locking promptly rather than gambling on further declines.

Preparing for the 2026 Mortgage Market: Action Steps

With rates expected to trend between 5.9-6.4% throughout 2026, self-employed borrowers should take proactive steps to position themselves for successful applications and optimal rates.

12-Month Preparation Timeline

Months 12-9 Before Application:

- Review credit reports and dispute inaccuracies

- Begin reducing credit card balances below 30% utilization

- Organize two years of tax returns and business documentation

- Establish relationship with mortgage broker specializing in self-employed borrowers

- Begin building cash reserves if below target levels

Months 8-6 Before Application:

- Continue credit optimization efforts

- Consult with CPA about income documentation strategies

- Research loan programs and lender options

- Determine target home price and down payment amount

- Review and understand easier qualification options for self-employed borrowers

Months 5-3 Before Application:

- Finalize documentation package

- Avoid major purchases or credit applications

- Maintain consistent business income and banking patterns

- Get pre-qualified to understand borrowing capacity

- Monitor mortgage rate trends and economic indicators

Months 2-0 Before Application:

- Obtain formal pre-approval

- Begin home search within approved budget

- Maintain all accounts in good standing

- Keep cash reserves intact and accessible

- Prepare for appraisal and underwriting process

Monitoring Economic Indicators

Self-employed borrowers benefit from understanding economic signals that influence mortgage rates:

📈 Federal Reserve announcements: Policy changes directly impact rate trajectories 📈 Inflation reports: CPI and PCE data influence Fed decisions 📈 Employment data: Job market strength affects economic outlook 📈 Treasury yields: 10-year Treasury rates closely correlate with mortgage rates 📈 Housing market reports: Supply, demand, and price trends signal market conditions

Following these indicators helps borrowers anticipate rate movements and time applications strategically.

Building Lender Relationships

Established banking relationships can benefit self-employed mortgage applications. Lenders familiar with a borrower’s financial patterns, business stability, and deposit history may offer more favorable underwriting consideration.

Strategies for building relationships include:

🤝 Maintaining business and personal accounts with potential mortgage lenders 🤝 Establishing credit lines or business loans demonstrating repayment reliability 🤝 Working with local banks or credit unions where personal relationships matter 🤝 Communicating openly about business model and income patterns

These relationships don’t guarantee approval but can provide advantages during underwriting, particularly for borderline applications.

Understanding Market Cycles

Mortgage rate cycles follow broader economic patterns. The 2026 forecast of gradual rate decline reflects expectations of moderating inflation and potential Federal Reserve rate cuts.

However, self-employed borrowers should prepare for multiple scenarios:

Optimistic scenario: Rates decline to 5.5-5.9% by late 2026, creating refinancing opportunities for those who purchased earlier in the year.

Base case scenario: Rates stabilize in the 6.0-6.4% range as forecasted, providing predictable planning environment.

Pessimistic scenario: Economic disruptions or inflation resurgence push rates back toward 6.5-7.0%, making current conditions more favorable in retrospect.

Preparing for various scenarios through adequate reserves and conservative borrowing ensures financial stability regardless of market direction.

Conclusion: Securing Your Self-Employed Mortgage in 2026

The mortgage landscape for self-employed borrowers in 2026 presents both challenges and opportunities. With expert forecasts predicting rates between 5.9% and 6.4%—a meaningful improvement from recent years—self-employed entrepreneurs, freelancers, and business owners have a window to secure favorable financing for their homeownership goals.

Success requires understanding the unique requirements self-employed borrowers face: higher credit score standards (620+ vs. 580), larger down payments (10-40% for alternative programs), substantial cash reserves (2-6 months minimum, 6-12 months recommended), and comprehensive income documentation. However, innovative solutions like bank statement loans can increase qualifying income by up to $80,000 in purchasing power for borrowers whose tax returns understate actual cash flow.

Strategic preparation makes the difference between approval and rejection, between optimal rates and costly premiums. Starting 12-18 months before applying, self-employed borrowers should focus on credit optimization, documentation organization, reserve building, and lender relationship development.

Timing matters in capturing favorable rates. While perfectly timing the market proves impossible, monitoring weekly rate trends, understanding economic indicators, and working with specialized lenders positions borrowers to act when opportunities arise. With 63% likelihood of stable rates in early 2026, those approved during favorable periods should consider locking promptly.

Your Next Steps

✅ Review your credit reports from all three bureaus and begin addressing any issues ✅ Calculate your cash reserves and determine gaps between current levels and targets ✅ Organize two years of tax returns and business documentation ✅ Connect with a mortgage specialist experienced in self-employed applications ✅ Monitor rate trends weekly to identify optimal application timing ✅ Explore loan programs including conventional, FHA, and bank statement options ✅ Develop a 12-month preparation timeline customized to your situation

The path to homeownership as a self-employed borrower requires more preparation than traditional employment situations, but the rewards of building equity and securing housing stability make the effort worthwhile. With mortgage rates trending favorably in 2026 and innovative lending solutions expanding access, self-employed borrowers who prepare strategically can achieve their homeownership goals on competitive terms.

For personalized guidance on your self-employed mortgage journey, explore our self-employed mortgage solutions or connect with a specialist who understands the unique challenges and opportunities you face in 2026’s evolving mortgage market.

References

[1] Selfemployed Mortgage Guide For Strategies To Get Approved – https://www.amerisave.com/learn/selfemployed-mortgage-guide-for-strategies-to-get-approved

[2] Arpine Self – https://mortgage.bankofamerica.com/arpine-self?article=202601TR&p=real-estate-professionals

[3] Mortgage Interest Rates Forecast – https://www.rocketmortgage.com/learn/mortgage-interest-rates-forecast

[4] Rate Trends – https://www.bankrate.com/mortgages/rate-trends/

[5] 4 Trends That Will Help Mortgage Lenders Reach New Borrowers In 2026 – https://www.housingwire.com/articles/4-trends-that-will-help-mortgage-lenders-reach-new-borrowers-in-2026/

[6] Mortgage Market Reset 2026 – https://foundationmortgage.com/mortgage-market-reset-2026/

[7] Watch – https://www.youtube.com/watch?v=_QypG-4ugtE