February 7, 2026

Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Securing a mortgage as a self-employed professional has historically felt like navigating an obstacle course blindfolded. While traditional employees simply hand over W-2 forms and pay stubs, entrepreneurs, freelancers, and business owners face scrutiny that can feel overwhelming. But 2026 brings a refreshing shift: stabilizing mortgage rates combined with innovative lending alternatives are creating unprecedented opportunities for self-employed borrowers to access competitive financing without jumping through the traditional income verification hoops.

Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification is no longer a distant dream—it’s a practical reality for those who understand the evolving lending landscape. As of early February 2026, the 30-year fixed mortgage rate sits at 6.114%, with experts projecting rates to remain within the 5.9% to 6.3% range throughout the year[4][3]. While these rates represent modest relief compared to recent peaks, they’re far from the pandemic-era lows of 3–4%. The silver lining? Self-employed borrowers who meet lender criteria can now access the exact same mortgage rates as traditionally employed applicants[5].

Key Takeaways

✅ Rate parity is achievable: Self-employed borrowers can secure identical rates to W-2 employees when using proper documentation strategies

💰 Bank statement mortgages unlock purchasing power: Using 12–24 months of deposit history can increase qualifying income by approximately $80,000 compared to tax returns[2]

📊 2026 rates remain stable: Current rates hover around 6.114% with projections of 5.9%–6.3% throughout the year, creating predictable planning opportunities[4][3]

🏠 Down payment strategies matter: Increasing down payment from 10% to 20% can save $124,920 over 30 years while eliminating PMI requirements[2]

📝 Alternative verification is mainstream: Lenders now offer multiple pathways beyond traditional tax returns, including bank statement programs and DSCR loans

Understanding the 2026 Mortgage Rate Environment for Self-Employed Borrowers

The mortgage landscape in 2026 presents a unique opportunity for self-employed professionals. Unlike the volatile rate swings of previous years, the current environment offers relative stability—a critical advantage when planning significant financial commitments.

Current Rate Benchmarks and Projections

As of February 4-6, 2026, the 30-year fixed mortgage rate stands at 6.114%, representing a slight uptick of 5 basis points from the previous week[4]. This modest increase aligns with broader market expectations, as 63% of mortgage industry experts predict rates will remain unchanged in the February 5-11 period, while 25% expect declines and only 13% anticipate increases[7].

For self-employed borrowers planning their mortgage strategy, this stability is invaluable. The projected rate range of 5.9% to 6.3% throughout 2026 provides a predictable window for financial planning[3]. While these rates won’t match the historic lows of 3–4% seen during the pandemic, they represent a significant improvement from the peaks experienced in recent years.

Why Self-Employed Borrowers Can Access Competitive Rates

A common misconception persists that self-employed professionals automatically face higher mortgage rates. This belief is outdated and simply untrue in 2026’s lending environment. Self-employed borrowers meeting lender criteria can access exactly the same mortgage rates as traditionally employed applicants[5].

The key difference isn’t the rate itself—it’s the documentation pathway used to qualify. Traditional lenders evaluate risk based on income stability and debt-to-income ratios, not employment classification. When self-employed borrowers demonstrate consistent income through appropriate documentation channels, they eliminate the perceived “risk premium” that once justified higher rates.

For comprehensive guidance on navigating the mortgage process as a self-employed Canadian, explore our ultimate guide to securing a mortgage for self-employed Canadians.

Interest Rate Trends and Economic Factors

Several economic factors influence the 2026 rate environment:

- Federal Reserve policy: Gradual adjustments to benchmark rates create ripple effects across mortgage markets

- Inflation stabilization: Moderating inflation reduces pressure for aggressive rate increases

- Housing market dynamics: Balanced supply and demand prevent extreme rate volatility

- Global economic conditions: International factors contribute to overall rate stability

Understanding these broader trends helps self-employed borrowers time their mortgage applications strategically. For insights on how changing interest rates affect mortgages, review our analysis on Canada’s changing interest rate effects on mortgages.

Alternative Documentation Methods: Self-Employed Mortgage Rates 2026 Without Traditional Verification

The most significant advancement in Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification comes from the proliferation of alternative documentation methods. These pathways recognize that tax returns don’t always reflect a self-employed borrower’s true financial capacity.

Bank Statement Mortgage Programs

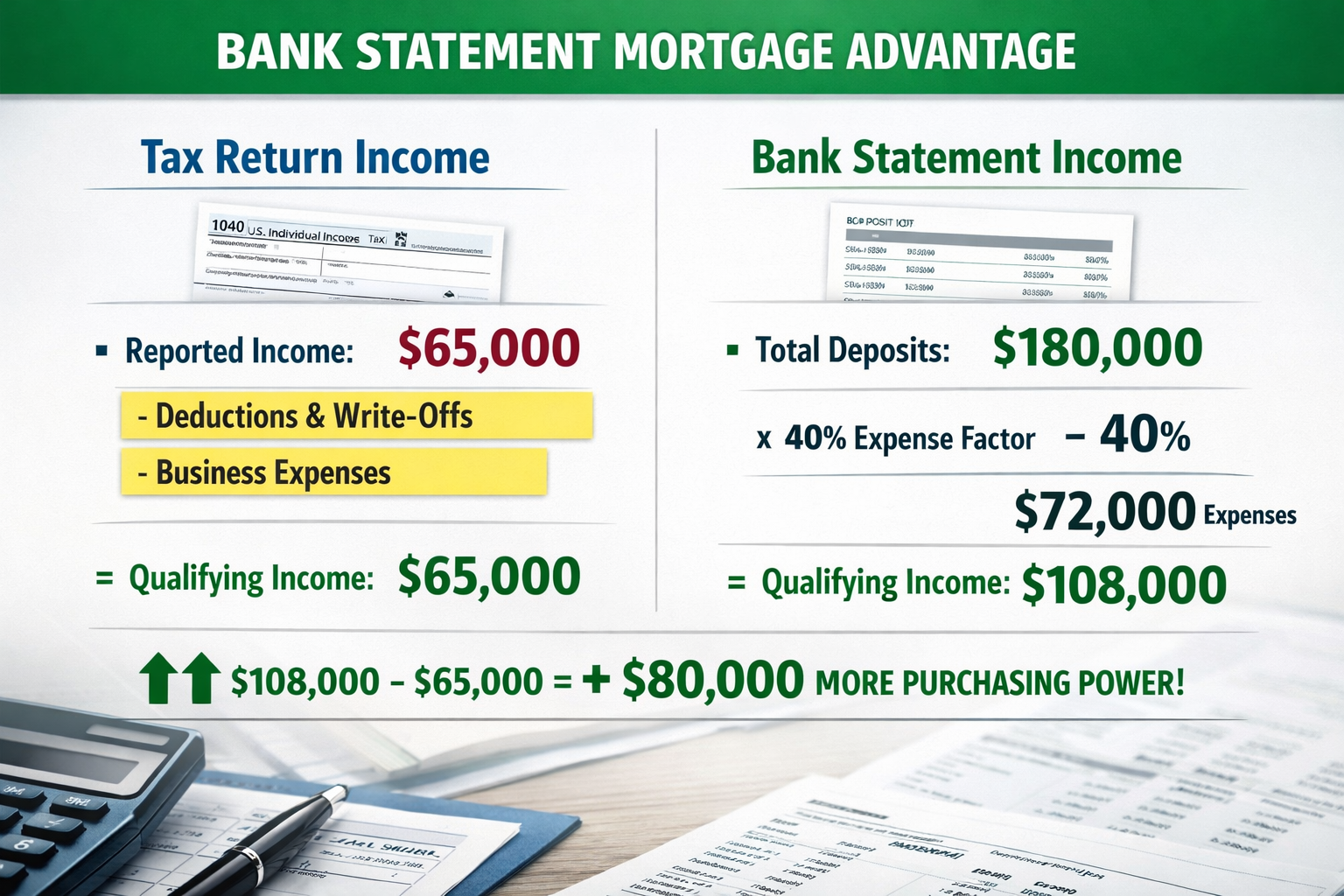

Bank statement mortgages have emerged as the gold standard for self-employed borrowers who legitimately reduce taxable income through business deductions. These programs qualify borrowers using 12–24 months of deposit history rather than tax returns[3].

Here’s how the math works in your favor:

| Documentation Method | Annual Income Shown | Monthly Qualifying Income | Purchasing Power Advantage |

|---|---|---|---|

| Traditional Tax Returns | $65,000 | $5,417 | Baseline |

| Bank Statement (40% expense factor) | $180,000 deposits | $9,000 | +$80,000 purchasing power |

This dramatic difference occurs because lenders apply a standard 40% expense factor to bank deposits, assuming that 60% represents actual income. For a self-employed professional with $180,000 in annual deposits, this yields $9,000 in monthly qualifying income versus just $5,417 from tax returns—approximately $80,000 more in purchasing power[2].

Bank statement programs particularly benefit:

- 🏗️ Contractors who maximize equipment and material deductions

- 💼 Business owners with significant depreciation expenses

- 🎨 Creative professionals who write off home office and supplies

- 🚗 Rideshare and delivery drivers claiming vehicle expenses

Learn more about these innovative approaches in our guide to alternative income verification and self-declared income mortgages.

Debt Service Coverage Ratio (DSCR) Loans

DSCR loans represent another powerful alternative for self-employed borrowers, particularly those with investment properties. These loans qualify borrowers based on the property’s income-generating capacity rather than personal income documentation.

The DSCR calculation is straightforward:

DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment

A DSCR of 1.0 means the property generates exactly enough income to cover the mortgage. Most lenders require a minimum DSCR of 1.15–1.25, providing a safety buffer. The beauty of DSCR loans is that personal tax returns become irrelevant—the property’s performance speaks for itself.

Stated Income and No-Doc Programs

While true “no-doc” loans disappeared after the 2008 financial crisis, modern stated income programs offer streamlined verification for highly qualified borrowers. These programs typically require:

- ✅ Excellent credit scores (typically 700+)

- ✅ Substantial down payments (20–40%)

- ✅ Significant liquid reserves

- ✅ Established business history

The trade-off for reduced documentation is often higher interest rates (typically 0.5–1.5% above conventional rates) and larger down payment requirements. However, for borrowers who value privacy or have complex income structures, these programs provide viable pathways to homeownership.

For those exploring how to qualify without traditional income documentation, our article on how to get a mortgage in Canada without any income offers additional strategies.

Business Income Verification Strategies

Self-employed borrowers can also leverage their business income more effectively by understanding what lenders actually evaluate:

Two-year income averaging: Lenders typically average the most recent two years of business income, which means a strong recent year can offset a weaker previous year.

Profit and Loss statements: Current-year P&L statements prepared by a CPA can demonstrate income trends that haven’t yet appeared on tax returns.

1099 documentation: Independent contractors receiving 1099 forms have clearer income trails that lenders find easier to verify.

Business bank accounts: Separating business and personal finances creates cleaner documentation and demonstrates financial sophistication.

Discover how to maximize your business income for mortgage approval in our comprehensive guide on getting approved for a mortgage using your business income.

Qualification Requirements and Down Payment Strategies for Self-Employed Mortgage Rates 2026

Understanding qualification requirements and strategically planning down payments can dramatically impact both approval odds and long-term costs for self-employed borrowers pursuing Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification.

Minimum Self-Employment History

Most lenders require at least two years of self-employment to verify income stability and capacity to cover mortgage payments[1]. This requirement reflects lenders’ need to see consistent income patterns across economic cycles and seasonal variations.

However, exceptions exist:

- 📚 Related work history: One year of self-employment may suffice if preceded by related W-2 employment in the same field

- 🎓 Education credentials: Advanced degrees or certifications in your field can reduce experience requirements

- 💪 Strong financials: Exceptional credit scores and substantial down payments can offset shorter business histories

The two-year requirement isn’t arbitrary—it provides lenders with sufficient data to calculate income averages, identify trends, and assess sustainability. Self-employed borrowers should plan accordingly, recognizing that starting a business and immediately qualifying for a mortgage presents significant challenges.

Down Payment Requirements by Loan Type

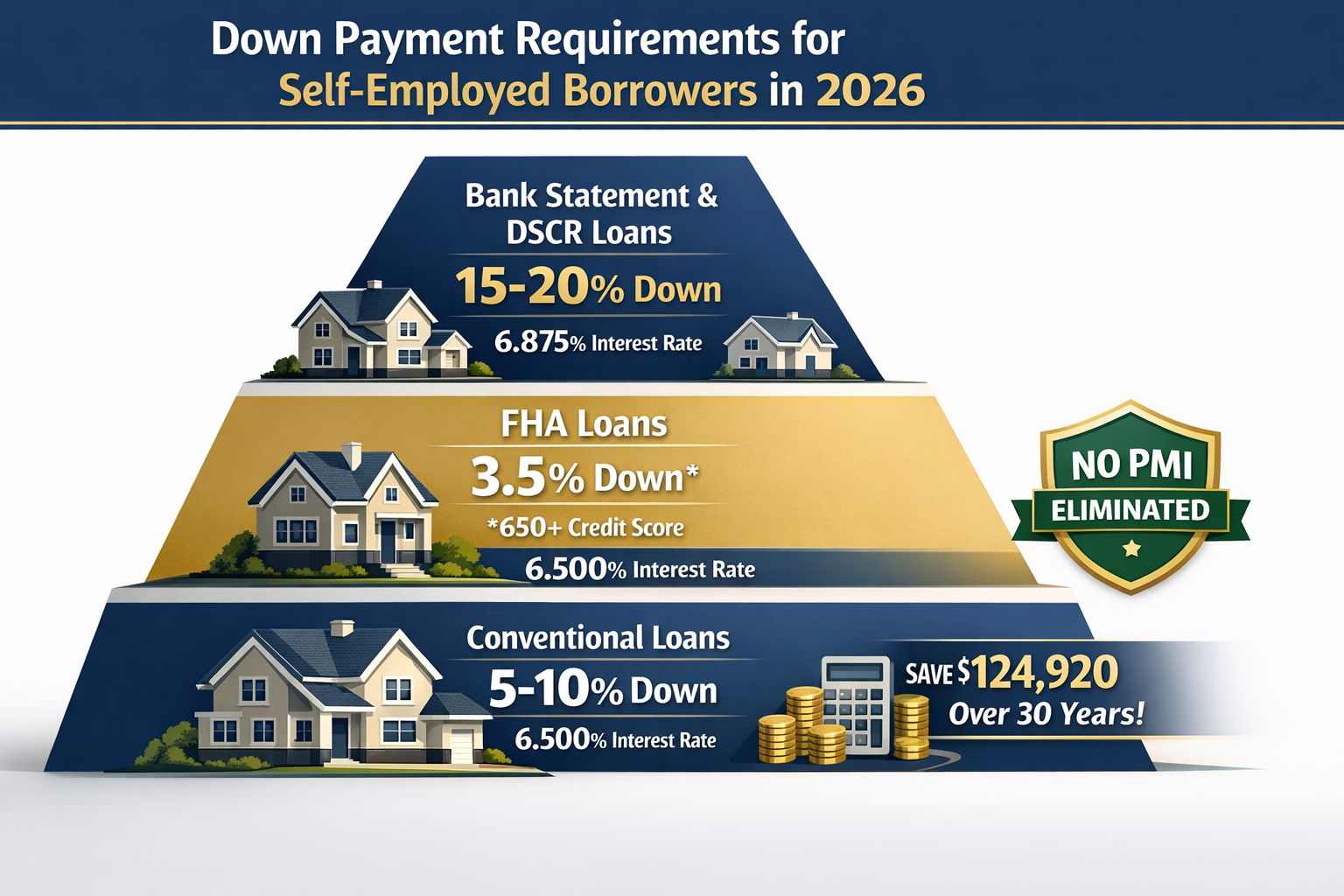

Down payment requirements vary significantly based on loan type and documentation method:

Conventional Loans: Self-employed borrowers typically need 5–10% down to offset additional documentation requirements, compared to as little as 3% for traditional W-2 borrowers[1][2].

FHA Loans: These government-backed loans require just 3.5% down but impose higher credit score requirements for self-employed applicants[1]. FHA loans also require mortgage insurance regardless of down payment size.

Bank Statement and DSCR Loans: Alternative documentation programs typically require 15–20% down, with some non-QM loans requesting up to 40% depending on credit score and loan amount[2][3].

VA and USDA Loans: Self-employed veterans and rural borrowers may qualify for zero-down programs, though income documentation requirements remain stringent.

The Financial Impact of Down Payment Size

The down payment amount directly influences both interest rates and long-term costs. Consider this real-world comparison:

Scenario A: 10% Down Payment

- Loan amount: $320,000

- Interest rate: 6.875%

- Monthly payment: $2,106

- PMI: $213/month (until 20% equity)

- Total 30-year cost: $758,160

Scenario B: 20% Down Payment

- Loan amount: $320,000

- Interest rate: 6.500%

- Monthly payment: $1,759

- PMI: $0

- Total 30-year cost: $633,240

The difference? $347 in monthly savings and $124,920 in total savings over 30 years, plus elimination of PMI[2]. For self-employed borrowers, this calculation becomes even more critical because larger down payments can compensate for non-traditional income documentation.

Credit Score Benchmarks

Credit scores play an outsized role for self-employed borrowers:

| Credit Score Range | Loan Options | Typical Rate Impact |

|---|---|---|

| 760+ | All programs, best rates | Baseline |

| 700-759 | Most programs | +0.25-0.50% |

| 660-699 | Limited programs | +0.50-1.00% |

| 620-659 | Alternative lenders only | +1.00-2.00% |

| Below 620 | Private/hard money | +2.00%+ |

Maintaining excellent credit becomes especially important when using alternative documentation methods. A 760+ credit score can offset the perceived risk of bank statement or stated income programs, keeping rates competitive with traditional mortgages.

Debt-to-Income Ratio Considerations

Lenders evaluate two DTI ratios:

Front-end ratio: Housing expenses (principal, interest, taxes, insurance) divided by gross monthly income. Most lenders require below 28%.

Back-end ratio: Total monthly debt obligations divided by gross monthly income. Maximum thresholds typically range from 43–50%, depending on loan type.

For self-employed borrowers using bank statement programs, the 40% expense factor application means deposits must be substantially higher to achieve the same qualifying income as tax returns. This mathematical reality makes DTI management critical.

Reserve Requirements

Lenders often require self-employed borrowers to maintain larger cash reserves after closing—typically 6–12 months of mortgage payments rather than the 2–3 months required for W-2 employees. These reserves demonstrate financial stability and provide a buffer against income fluctuations.

Strategic reserve planning includes:

- 💵 Maintaining separate savings accounts for reserves

- 📊 Documenting consistent savings patterns

- 🏦 Keeping reserves liquid (retirement accounts may not count)

- 📈 Building reserves before starting the mortgage process

For borrowers considering refinancing options, our guide on mortgage refinancing and switching lenders at renewal advantages for self-employed borrowers provides valuable strategies.

Lender Options: Finding the Best Self-Employed Mortgage Rates 2026

Not all lenders approach self-employed borrowers equally. Understanding which institutions offer the most favorable terms and flexible documentation requirements is essential for securing Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification.

Traditional Banks vs. Alternative Lenders

Traditional banks (major national and regional institutions) offer the lowest rates but maintain the strictest documentation requirements. They typically:

- Require full two-year tax return documentation

- Apply conservative income calculation methods

- Offer limited flexibility on documentation alternatives

- Provide the most competitive rates for well-qualified borrowers

Alternative lenders (credit unions, online lenders, non-QM specialists) provide greater flexibility with documentation but may charge slightly higher rates. They typically:

- Accept bank statement and alternative documentation

- Understand self-employed income structures better

- Offer more personalized underwriting

- Charge rates 0.25–1.00% higher than traditional banks

For detailed comparisons, explore our analysis of B-lender mortgage rates in Toronto and the growing demand for private or alternative lender mortgages.

Credit Unions and Community Banks

Credit unions often provide the “best of both worlds” for self-employed borrowers:

- ✅ Competitive rates approaching traditional bank levels

- ✅ Relationship-based underwriting with local decision-making

- ✅ Greater flexibility on documentation and income verification

- ✅ Willingness to consider full financial picture beyond formulas

The trade-off? Credit unions typically require membership and may have geographic restrictions. However, for self-employed borrowers with strong community ties, credit unions frequently deliver superior outcomes.

Mortgage Brokers and Their Advantages

Mortgage brokers serve as invaluable resources for self-employed borrowers, offering:

Access to multiple lenders: Brokers maintain relationships with dozens of lenders, including specialty programs for self-employed borrowers that aren’t advertised to the public.

Documentation expertise: Experienced brokers understand which documentation strategies work best for different income structures and can guide borrowers toward optimal approaches.

Rate shopping efficiency: Rather than applying with multiple lenders individually (which generates multiple credit inquiries), brokers shop your scenario across their network.

Advocacy during underwriting: When questions arise during underwriting, brokers advocate on your behalf and help address concerns proactively.

For self-employed borrowers navigating complex income structures, working with a knowledgeable broker often means the difference between approval and denial. Learn more about what mortgage brokers do and how they can help your specific situation.

Online Lenders and Fintech Solutions

The rise of fintech mortgage platforms has created new opportunities for self-employed borrowers:

- 🖥️ Streamlined digital applications

- 🤖 Automated income verification using bank account connections

- ⚡ Faster approval timelines

- 💡 Innovative underwriting algorithms that consider non-traditional factors

However, online lenders may lack the personal touch needed for complex self-employed scenarios. They work best for borrowers with straightforward income patterns and strong financial profiles.

Specialty Non-QM Lenders

Non-QM (non-qualified mortgage) lenders specialize in borrowers who don’t fit traditional lending boxes. For self-employed professionals, these lenders offer:

- Bank statement programs (12-month and 24-month options)

- Asset depletion loans (qualifying based on investment accounts)

- DSCR loans for investment properties

- Stated income programs for high-net-worth borrowers

While rates run 0.5–2.0% higher than conventional mortgages, non-QM lenders provide pathways when traditional options aren’t viable.

Documentation Preparation: Building Your Strongest Application

Success in securing Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification hinges on meticulous documentation preparation. The stronger your paper trail, the more competitive your rate and terms.

Essential Documents for Self-Employed Borrowers

Tax Returns (2 years):

- Personal returns (Form 1040) with all schedules

- Business returns (1065, 1120, 1120S) if applicable

- State tax returns

- Tax transcripts directly from IRS

Profit and Loss Statements:

- Year-to-date P&L prepared by CPA

- Previous year P&L

- Month-by-month breakdown showing income consistency

Business Bank Statements (12-24 months):

- All pages, including blank pages

- Statements showing consistent deposits

- Clear separation between business and personal accounts

Balance Sheets:

- Current business assets and liabilities

- Equipment and inventory valuations

- Accounts receivable aging

Business Licenses and Credentials:

- Professional licenses

- Business registration documents

- Proof of business continuity

Additional Income Documentation:

- 1099 forms from clients

- Contracts showing ongoing work

- Letters from CPAs verifying income

Organizing Documentation for Maximum Impact

Create a documentation timeline: Organize materials chronologically, making it easy for underwriters to track income trends and business growth.

Highlight income stability: Use cover sheets or summaries that emphasize consistent or growing income patterns across the two-year period.

Explain anomalies proactively: If one year shows lower income due to maternity leave, major equipment purchases, or business expansion, provide written explanations before underwriters ask.

Separate business expenses clearly: When using bank statement programs, clearly distinguish between business expenses and personal draws to demonstrate true income capacity.

Working with CPAs and Tax Professionals

Strategic tax planning for mortgage qualification requires balancing legitimate deductions with qualifying income:

Timing considerations: If planning to apply for a mortgage within two years, discuss income reporting strategies with your CPA. Sometimes minimizing deductions in the years preceding a mortgage application makes sense.

Add-back opportunities: Many business expenses (depreciation, home office deductions, vehicle expenses) can be “added back” to income for mortgage qualification purposes, even though they reduced taxable income.

CPA letters: A letter from your CPA explaining income calculations, business stability, and future income projections can strengthen your application significantly.

Common Documentation Mistakes to Avoid

❌ Mixing business and personal expenses: Commingled accounts raise red flags and complicate income verification.

❌ Incomplete bank statements: Missing even one month creates delays and additional scrutiny.

❌ Unexplained large deposits: Lenders must source all large deposits to ensure they represent income, not loans.

❌ Inconsistent business names: Using different business names across documents creates confusion and verification challenges.

❌ Last-minute tax amendments: Filing amended returns during the mortgage process triggers additional review and delays.

Rate Comparison and Shopping Strategies

Securing the best Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification requires strategic rate shopping and understanding how to compare offers effectively.

Understanding Rate Quotes and APR

Interest rate represents the cost of borrowing, while APR (Annual Percentage Rate) includes the interest rate plus fees, points, and other costs. For self-employed borrowers, APR comparisons become especially important because alternative documentation programs may include higher fees.

Example comparison:

- Lender A: 6.25% rate, 6.45% APR (lower fees)

- Lender B: 6.125% rate, 6.50% APR (higher fees)

Despite Lender B’s lower rate, Lender A may cost less over the loan term due to lower fees.

Fixed vs. Variable Rate Considerations

The fixed vs. variable rate decision carries unique implications for self-employed borrowers:

Fixed-rate advantages:

- 🔒 Predictable payments aid business cash flow planning

- 🛡️ Protection against rate increases

- 💼 Easier budgeting for variable income

Variable-rate advantages:

- 💰 Lower initial rates (typically 0.5–1.0% below fixed)

- 📉 Benefit from rate decreases

- 🔄 Flexibility for short-term ownership

For comprehensive analysis, review our guide on fixed vs. variable rates and mortgage rate guide for fixed or variable mortgage options.

Rate Lock Strategies

Rate locks protect against rate increases during the application process. For self-employed borrowers whose applications may take longer due to documentation requirements, rate lock strategies become critical:

Standard locks: 30–45 days, typically no cost Extended locks: 60–90 days, may include fees Float-down options: Allow capturing lower rates if they drop during the lock period

Timing Your Application

Seasonal patterns: Mortgage rates often follow seasonal trends, with slight increases during spring/summer buying seasons and potential decreases in fall/winter.

Economic indicators: Monitor Federal Reserve announcements, employment reports, and inflation data that influence rate movements.

Personal business cycles: Apply during strong income months when bank statements show robust deposits, strengthening your application.

Negotiation Tactics for Self-Employed Borrowers

Leverage competing offers: Obtain quotes from multiple lenders and use them as negotiation leverage.

Bundle services: Some lenders offer rate discounts for opening checking accounts or moving investment accounts.

Points buydown: Paying points (1% of loan amount = 1 point) can reduce rates by approximately 0.25% per point. Calculate whether the upfront cost justifies long-term savings.

Relationship discounts: Existing banking relationships may yield 0.125–0.25% rate discounts.

Overcoming Common Challenges for Self-Employed Mortgage Applicants

Even with proper preparation, self-employed borrowers frequently encounter specific challenges when pursuing Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification. Understanding these obstacles and their solutions increases approval odds.

Addressing Income Fluctuations

The challenge: Self-employed income naturally fluctuates seasonally and cyclically, which lenders view as risk.

Solutions:

- 📊 Provide multi-year income history showing overall upward trends

- 📝 Explain seasonal patterns with documentation (e.g., tax preparation services peak in spring)

- 💵 Maintain larger cash reserves to demonstrate ability to weather slow periods

- 📈 Provide signed contracts or recurring revenue documentation showing future income stability

Handling Business Write-Offs and Deductions

The challenge: Legitimate business deductions reduce taxable income, which reduces qualifying income for mortgages.

Solutions:

- 🏦 Use bank statement programs that look at deposits rather than taxable income

- ➕ Work with lenders who allow “add-backs” of non-cash expenses like depreciation

- 📋 Provide detailed P&L statements showing gross revenue before deductions

- 🎯 Plan tax strategies 2–3 years before mortgage applications

Managing Multiple Income Streams

The challenge: Income from multiple businesses, side hustles, or investment properties complicates verification.

Solutions:

- 📑 Organize documentation by income source with clear summaries

- 🏢 Consolidate business entities where practical before applying

- 💼 Work with experienced mortgage brokers who understand complex income structures

- 📊 Provide comprehensive financial statements showing all income sources

Dealing with Recent Business Changes

The challenge: Starting a new business, changing business structure, or expanding operations can disrupt income history.

Solutions:

- 📚 Document related work history in the same industry

- 🎓 Provide credentials demonstrating expertise in your field

- 💪 Increase down payment to offset shorter business history

- 🤝 Consider co-borrowers with traditional employment

Credit Issues Specific to Self-Employed Borrowers

The challenge: Business credit issues, high business credit utilization, or personal guarantees on business debt can impact personal credit.

Solutions:

- 🔄 Separate business and personal credit completely

- 💳 Pay down high-utilization business credit cards before applying

- 📝 Provide explanations for legitimate business credit issues

- ⏰ Allow time for credit recovery before mortgage applications

Maximizing Your Approval Odds and Securing Competitive Rates

Beyond documentation and lender selection, strategic actions can significantly improve approval odds and secure better Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification.

Pre-Approval Strategies

Obtain pre-approval before house hunting: Pre-approval provides:

- 💪 Negotiating power with sellers

- 🎯 Clear budget understanding

- ⚡ Faster closing timelines

- 🔍 Early identification of documentation issues

Soft pre-qualification first: Some lenders offer soft credit pulls for initial pre-qualification, allowing you to gauge approval odds without impacting credit scores.

Building Lender Relationships

Establish banking relationships early: Opening business accounts, maintaining deposits, and building history with potential mortgage lenders creates relationship equity that can influence approval decisions.

Demonstrate financial responsibility: Consistent deposits, maintained minimum balances, and avoiding overdrafts show financial management skills that lenders value.

Strategic Business Financial Management

Separate business and personal finances completely: Maintain distinct bank accounts, credit cards, and financial records to simplify income verification.

Maintain clean business accounting: Professional bookkeeping and accounting demonstrate business sophistication and make income verification straightforward.

Build business credit: Establishing strong business credit separate from personal credit provides additional credibility.

Timing Considerations

Plan 2–3 years ahead: If homeownership is a goal, structure business finances with mortgage qualification in mind from the beginning.

Avoid major business changes: Don’t change business structure, add partners, or make other significant changes during the 2-year look-back period.

Time large purchases strategically: Major equipment purchases or business expansions can reduce qualifying income; time these after mortgage closing if possible.

Working with Professionals

Assemble your team early:

- 🧾 CPA familiar with mortgage qualification strategies

- 🏡 Mortgage broker experienced with self-employed borrowers

- ⚖️ Attorney for business structure optimization

- 📊 Financial advisor for overall wealth management

Coordinate strategies: Ensure your CPA, mortgage broker, and financial advisor communicate and align strategies for optimal outcomes.

Conclusion: Taking Action on Self-Employed Mortgage Rates 2026

The landscape for Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification has never been more favorable. With rates stabilizing in the 5.9%–6.3% range and alternative documentation methods becoming mainstream, self-employed borrowers have unprecedented access to competitive mortgage financing[3][4].

The key to success lies in understanding that self-employment doesn’t mean settling for inferior rates or terms—it means choosing the right documentation pathway and lender for your specific situation. Whether through bank statement programs that unlock hidden purchasing power, DSCR loans that focus on property performance, or strategic tax planning that optimizes qualifying income, multiple routes lead to homeownership.

Actionable Next Steps

Immediate actions (this week):

- 📋 Gather 2 years of tax returns, bank statements, and P&L statements

- 🔍 Check your credit score and review reports for errors

- 💰 Calculate your available down payment and reserves

- 📞 Contact mortgage brokers experienced with self-employed borrowers

Short-term actions (this month):

- 🏦 Obtain rate quotes from 3–5 lenders using different documentation methods

- 🧾 Meet with your CPA to discuss income optimization strategies

- 📊 Organize documentation into clear, chronological files

- 💵 Address any credit issues or high debt balances

Medium-term actions (next 3–6 months):

- 🏡 Get pre-approved before serious house hunting

- 📈 Build additional reserves if below lender requirements

- 🔄 Refinance or consolidate debt to improve DTI ratios

- 📝 Establish consistent deposit patterns in business accounts

Long-term planning (ongoing):

- 💼 Maintain separation between business and personal finances

- 📚 Document all income sources meticulously

- 🎯 Plan major business decisions with mortgage impact in mind

- 🔍 Monitor rate trends and refinancing opportunities

The self-employed path to homeownership requires more preparation than traditional employment, but the destination remains equally accessible. By leveraging the strategies outlined in this guide—from alternative documentation methods to strategic down payment planning—self-employed borrowers can secure competitive rates and favorable terms in 2026’s mortgage market.

For personalized guidance tailored to your specific self-employed situation, explore additional resources on self-employed mortgages and consider working with professionals who specialize in helping entrepreneurs, freelancers, and business owners achieve their homeownership goals.

The opportunity is here. The tools are available. The only question remaining is: are you ready to take the next step toward securing your Self-Employed Mortgage Rates 2026: How to Secure the Best Rates Without Traditional Income Verification?

References

[1] Mortgage Self Employed 1099 Business Get Approved – https://themortgagereports.com/18303/mortgage-self-employed-1099-business-get-approved

[2] Selfemployed Mortgage Guide For Strategies To Get Approved – https://www.amerisave.com/learn/selfemployed-mortgage-guide-for-strategies-to-get-approved

[3] Mortgage Rate Trends 2026 – https://trussfinancialgroup.com/blog/mortgage-rate-trends-2026

[4] Current Mortgage Rates 02 06 2026 – https://fortune.com/article/current-mortgage-rates-02-06-2026/

[5] Best Mortgage Rates Self Employed – https://www.mortgage-os.com/guides/best-mortgage-rates-self-employed

[7] Rate Trends – https://www.bankrate.com/mortgages/rate-trends/