March 12, 2026

Toronto Institutional Investors in Condos: How Private Mortgages Enable Larger Portfolio Acquisitions in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s condo market is undergoing a dramatic shift — and institutional investors are moving fast to capitalize. The story of Toronto Institutional Investors in Condos: How Private Mortgages Enable Larger Portfolio Acquisitions in 2026 is one of sophisticated strategy meeting market disruption. As traditional bank financing tightens and presale volumes hit 30-year lows, savvy institutional players are turning to private mortgage solutions to scale their condo portfolios faster, smarter, and with far greater flexibility than conventional lending allows.

Key Takeaways 📌

- Condo presales in the GTA collapsed to 1,600 units in 2025 — the lowest since 1991 — creating rare bulk-buy opportunities for institutional investors [5][9]

- OSFI’s Q1 2026 regulatory changes restrict traditional bank financing for multi-property investors, making private mortgages an essential tool for portfolio scaling [3]

- Private mortgages now represent ~20% of Ontario’s lending market, offering institutional buyers speed, flexibility, and bridge financing unavailable through banks

- Mortgage Investment Corporations (MICs) provide a passive alternative, delivering 7%+ yields backed by secured real estate collateral

- Purpose-built rentals are gaining ground, but distressed condo acquisitions via private financing remain a compelling strategy for 2026

The 2026 Toronto Condo Landscape: Why Institutions Are Paying Attention

The numbers tell a striking story. Greater Toronto Area condo presales fell to just 1,600 units in 2025 — a level not seen since 1991 — and CMHC projects new housing starts to remain near two-decade lows well into 2026 [9][5]. This supply freeze, paradoxically, creates a powerful entry point for institutional capital.

The Bank of Canada flagged in early 2026 that Toronto’s condo boom was built on a fragile foundation: roughly 70% of new condo financing depended on investor presales to unlock construction loans [1]. With micro-units (under 500 sq ft) making up 60% of new supply but only 30% of actual demand, the model has cracked [1]. Average benchmark prices have slipped to $938,000, down 7.9% year-over-year, and condo inventory sits at a bloated 8 months of supply [6].

💬 “Condos are no longer cash-flow positive at $655K average price and current rate levels — investors are exiting, and that’s creating bulk-buy opportunities.” — Victor Tran, Rates.ca [2]

For institutional buyers with access to flexible capital, distressed seller situations and bulk portfolio deals are now within reach. The key unlocking mechanism? Private mortgage financing.

New Regulatory Pressures Push Institutions Toward Private Lenders

OSFI’s Q1 2026 Capital Adequacy Requirements introduced a critical change: banks can no longer double-count rental income across multiple investment properties when qualifying borrowers [3]. For any investor where more than 50% of income is rental-derived, traditional bank mortgages become significantly harder to obtain.

Combined with the City of Toronto’s January 2026 luxury tax hike — where non-resident speculation tax on $5M+ properties now exceeds $250,000 combined with provincial Land Transfer Tax (effective April 1, 2026) — foreign institutional buyers face additional friction in the conventional lending space [3].

The result: private mortgage lenders have become the go-to solution for institutional portfolio scaling. To understand the full range of options available, explore what private mortgage options exist in Ontario and how they compare to bank products.

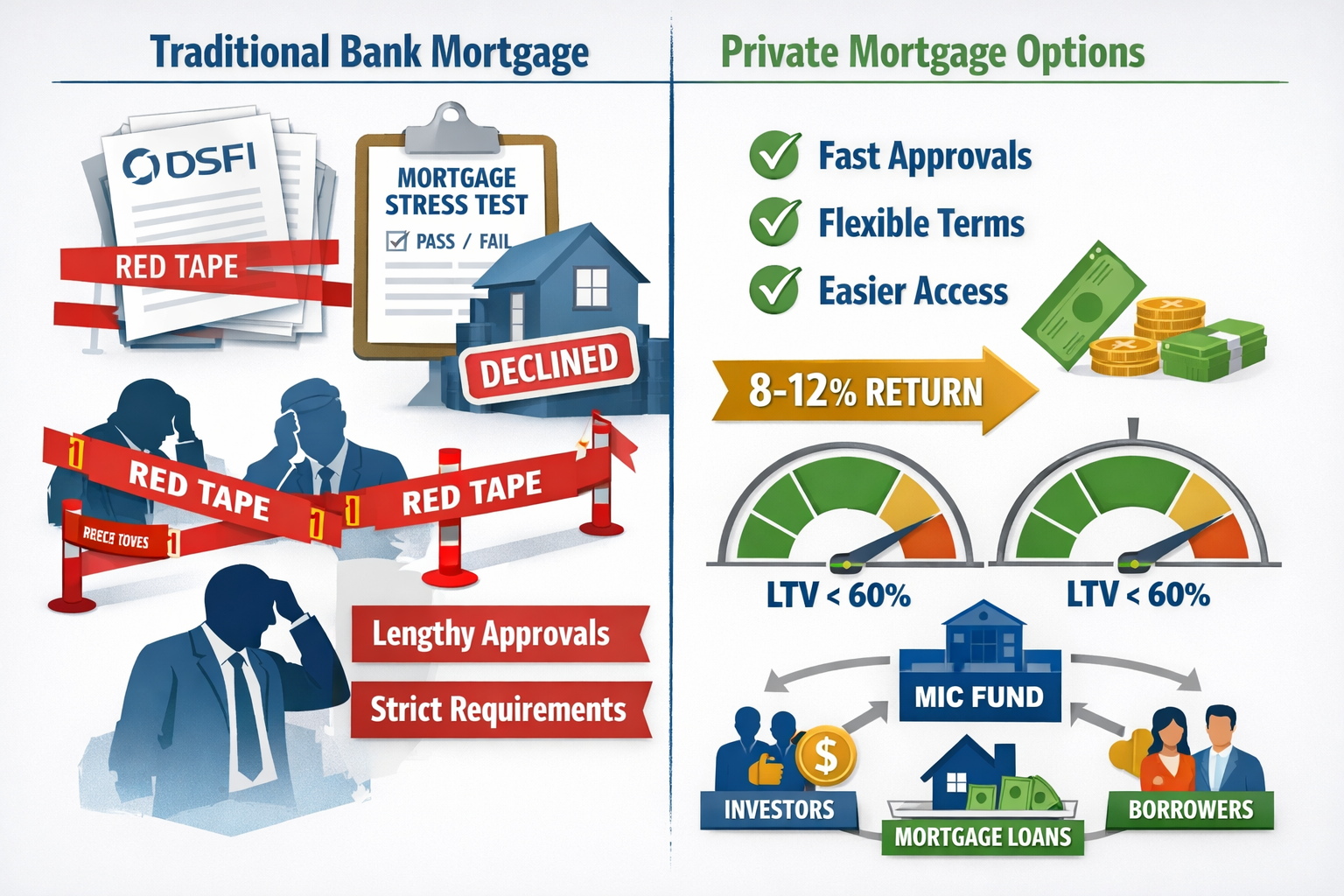

How Private Mortgages Enable Larger Portfolio Acquisitions in 2026

The core advantage of private mortgages for institutional condo investors comes down to three pillars: speed, flexibility, and scalability.

Speed of Execution 🚀

Traditional bank approvals for multi-property investment portfolios can take 60–90 days, especially under new OSFI income-counting rules. Private lenders can close in 5–15 business days, which is critical when acquiring distressed condo portfolios where sellers need fast resolution.

Flexible Underwriting Standards

Private lenders assess deals based primarily on asset quality and loan-to-value (LTV) ratios rather than borrower income documentation. Institutional buyers with complex corporate structures — holding companies, REITs, limited partnerships — often struggle to satisfy bank income verification requirements. Private lenders focus on the collateral: the property itself.

| Feature | Bank Mortgage | Private Mortgage |

|---|---|---|

| Approval Time | 60–90 days | 5–15 days |

| Income Verification | Strict (OSFI rules) | Asset/LTV focused |

| Multi-property Limits | Restricted (Q1 2026) | Flexible |

| Typical Rate | 5.5–6.5% | 8.99–12% |

| LTV Maximum | 80% | Up to 75–80% |

| Term Length | 5 years (typical) | 6–24 months (bridge) |

Bridge Financing for Portfolio Transitions

Many institutional investors use private mortgages as bridge loans — short-term financing that allows them to acquire a condo portfolio now, stabilize it with tenants or renovations, and then refinance into conventional or commercial lending once the asset performs. With the Bank of Canada’s overnight rate at 2.25%, private variable mortgage products starting at 8.99% represent a manageable carry cost for short-term bridge strategies [8].

Working with an experienced mortgage broker in Toronto is essential to navigating these complex multi-lender arrangements efficiently.

Mortgage Investment Corporations (MICs): The Passive Institutional Play

Not every institutional investor wants direct property management exposure. Mortgage Investment Corporations (MICs) offer a compelling alternative: pool capital into a fund that issues private mortgages, backed by real estate collateral, without the headaches of tenants, maintenance, or vacancy.

Firms like Atrium MIC report yields of approximately 7.01% with over 73% of their portfolio focused on the GTA — providing geographic concentration in Canada’s most liquid real estate market. For institutions seeking downside protection, secured credit instruments like MIC mortgages offer priority claims over equity in default scenarios [7].

Private mortgage lending now accounts for roughly 20% of Ontario’s total mortgage market, according to FSRA’s 2025–2026 oversight plan — a figure that reflects just how mainstream this financing channel has become. For current rate benchmarks, review the best private mortgage rates in Ontario to understand today’s lending environment.

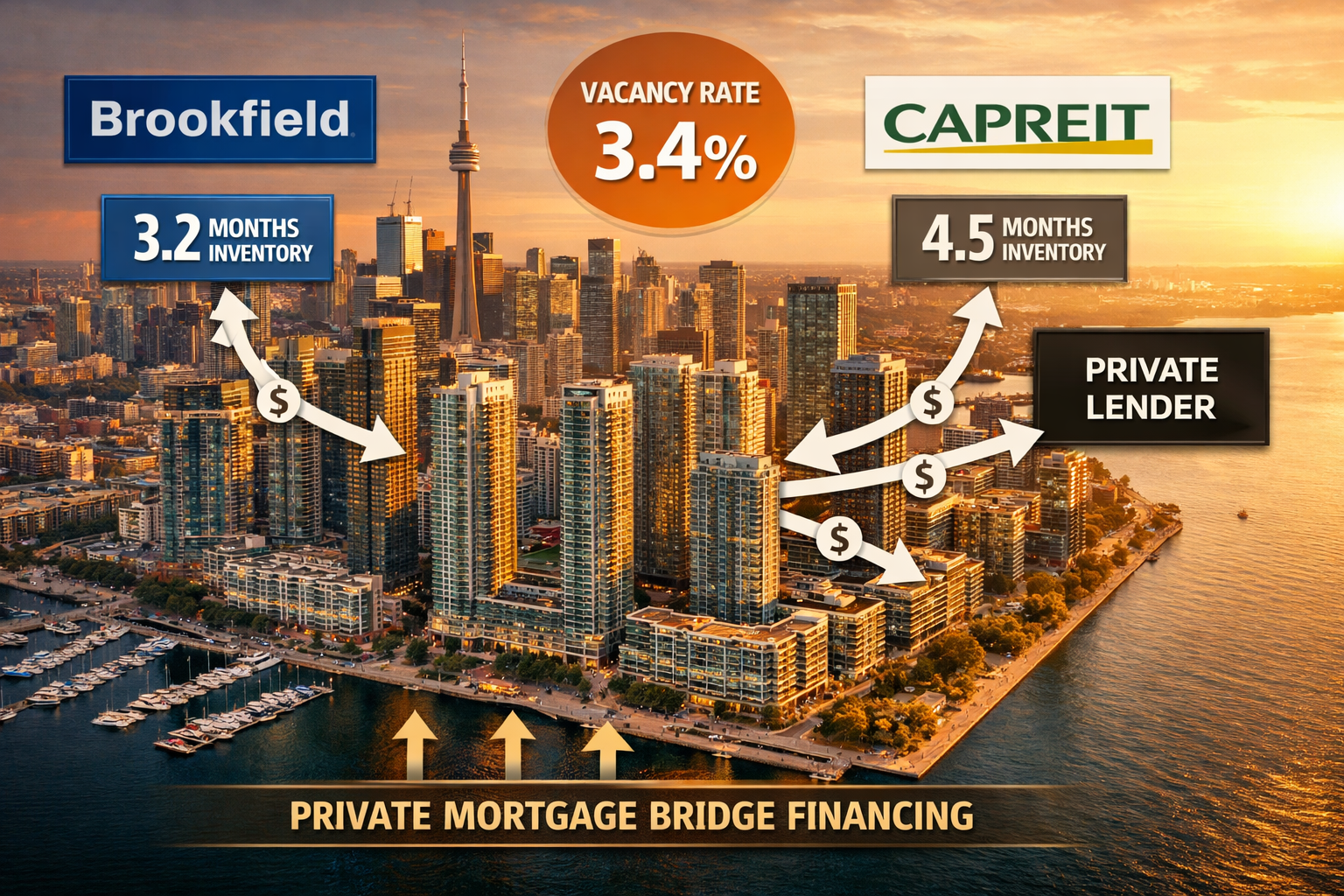

Institutional Strategy: Condos vs. Purpose-Built Rentals in 2026

The broader institutional real estate story in 2026 involves a strategic pivot: major players like Brookfield, CAPREIT, and Blackstone/Starlight are increasingly favoring purpose-built rental apartments over individual condo units [7].

The logic is straightforward:

- Purpose-built rentals offer stable demand, professional management scale, and a projected 3.4% vacancy rate in 2026 — far healthier than condo oversupply conditions

- Condo portfolios require managing hundreds of individual strata titles, condo fees, and board relationships — operationally complex at scale

However, distressed condo acquisitions via private financing remain attractive for a specific institutional strategy: bulk purchases of condo buildings or large unit blocks at below-market prices, followed by conversion to purpose-built rental management structures.

💡 ULI Toronto’s 2026 Emerging Trends report notes that institutional capital is pivoting toward sophisticated management platforms that can extract value from both asset classes — and private debt markets are providing the secured credit infrastructure to make this happen. [7]

For investors exploring rental property strategies, understanding how to invest in rental properties as a self-employed individual provides useful foundational context, even for those operating through corporate structures.

Key Risk Factors to Monitor ⚠️

Institutional investors using private mortgages for condo acquisitions in 2026 must account for:

- Higher carrying costs — private rates of 9–12% compress margins on low-yield condo units

- Refinancing risk — bridge loans must convert to permanent financing; ensure an exit strategy before entering

- Regulatory evolution — OSFI and FSRA continue tightening oversight of both borrowers and private lenders

- Market timing — with 8 months of condo inventory, price recovery timelines remain uncertain [6]

- Closing cost exposure — bulk acquisitions multiply transaction costs significantly; review a comprehensive guide to Toronto closing costs before modeling returns

For investors navigating the 2026 mortgage renewal environment, understanding how mortgage renewals impact refinancing decisions provides important context for portfolio-level financing strategy.

Additionally, institutional buyers should understand how the mortgage stress test applies when eventually transitioning from private to conventional financing — a critical step in any bridge loan exit strategy.

Conclusion: Actionable Next Steps for Institutional Investors 🏙️

The convergence of regulatory tightening, condo market distress, and private lending growth has created a rare window of opportunity for institutional investors in Toronto’s condo sector. Private mortgages are no longer a last resort — they are a strategic financing tool that enables faster acquisitions, flexible underwriting, and scalable portfolio growth that conventional banks simply cannot match in 2026.

Here’s what to do next:

✅ Audit your current portfolio financing — identify properties where OSFI’s new income-counting rules create refinancing needs

✅ Engage a specialized mortgage broker with institutional private lending experience to map out bridge financing options

✅ Model MIC investments as a passive complement to direct property holdings — 7%+ secured yields with GTA collateral exposure

✅ Target distressed condo sellers in the 8-month inventory environment, using private mortgage speed as a competitive advantage

✅ Plan your exit strategy first — know your refinancing pathway before drawing on private bridge capital

The Toronto condo market in 2026 rewards those who move decisively with the right financing structure. Private mortgages are the engine making larger, faster, and smarter portfolio acquisitions possible.

References

[1] Sparks At Bank Article 2026 2 – https://www.bankofcanada.ca/2026/02/sparks-at-bank-article-2026-2/

[2] Investors Buyers Toronto Condo Market – https://globalnews.ca/news/11489247/investors-buyers-toronto-condo-market/

[3] Playing By New Rules What Changed For Toronto Real Estate In 2025 2026 – https://www.getwhatyouwant.ca/playing-by-new-rules-what-changed-for-toronto-real-estate-in-2025-2026

[5] Watch – https://www.youtube.com/watch?v=z9gLi0M4o-c

[6] Blog Toronto Condo Market January 2026 Update – https://www.deeded.ca/blog/blog-toronto-condo-market-january-2026-update

[7] Uli Torontos View Of Emerging Trends In Real Estate 2026 Inching From Recovery To Reinvention – https://urbanland.uli.org/capital-markets-and-finance/uli-torontos-view-of-emerging-trends-in-real-estate-2026-inching-from-recovery-to-reinvention

[8] Watch – https://www.youtube.com/watch?v=iAj9QXZdn3Q

[9] Housing Market Outlook – https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/market-reports/housing-market/housing-market-outlook