February 8, 2026

Bank Statement Loans for Self-Employed: How to Qualify and Maximize Rates in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

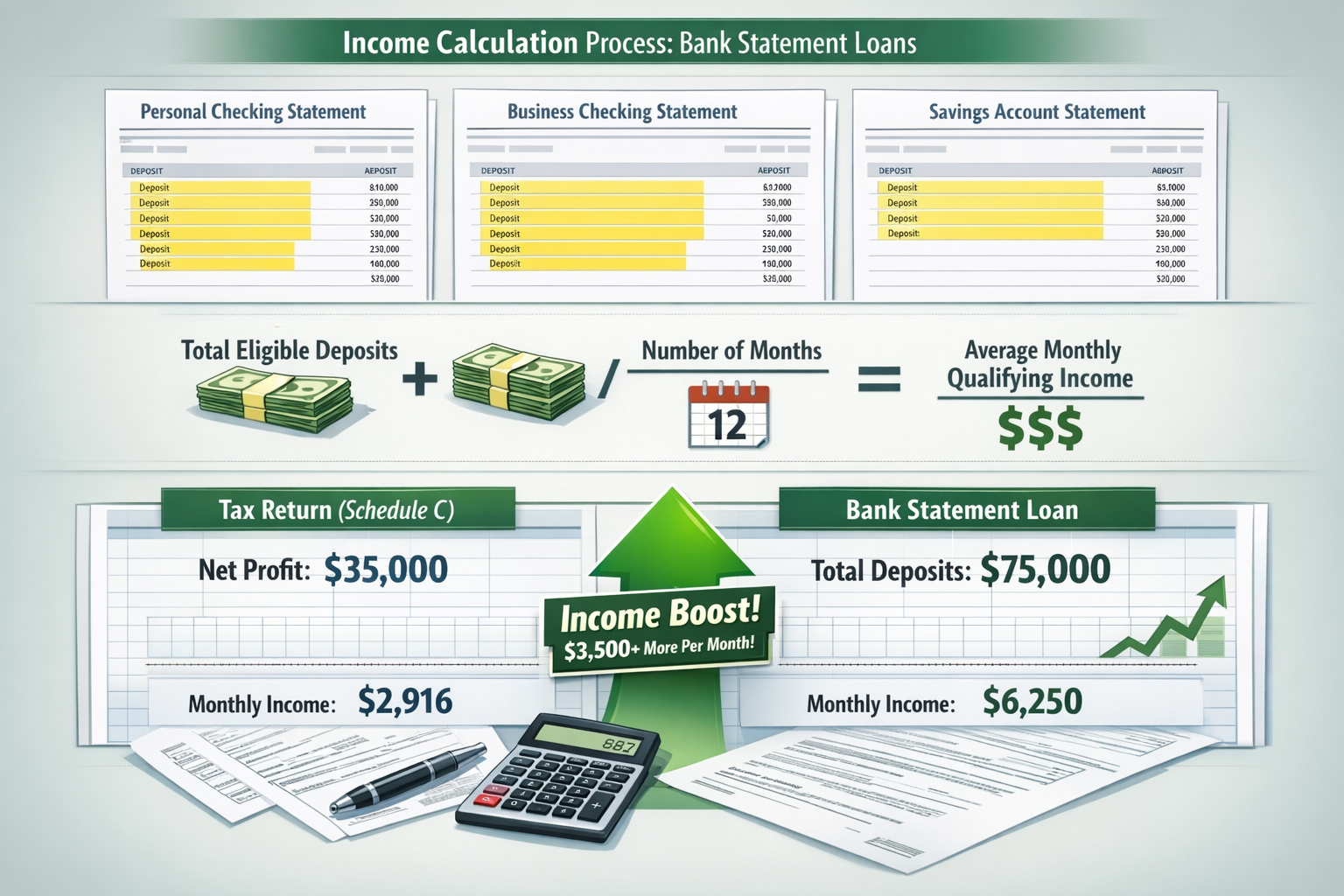

Self-employed professionals face a unique challenge in 2026: their actual income often far exceeds what appears on tax returns. A freelance consultant might deposit $75,000 annually into their accounts while showing only $35,000 in net profit on Schedule C after legitimate business deductions. This creates a frustrating barrier when applying for traditional mortgages. Bank statement loans solve this problem by using actual deposit history instead of tax returns, potentially boosting qualifying income by $3,500 or more per month. Understanding how to qualify for Bank Statement Loans for Self-Employed: How to Qualify and Maximize Rates in 2026 can unlock homeownership opportunities that conventional financing simply cannot provide.

Key Takeaways

✅ 12-24 month documentation flexibility: Borrowers with excellent credit (740+) and 25%+ down payments can qualify with just 12 months of bank statements, while most applicants need 24 months of consecutive statements[1].

✅ Income calculation advantage: Bank statement loans calculate income based on actual deposits rather than tax returns, potentially increasing qualifying income by thousands of dollars monthly compared to Schedule C net profit[1].

✅ 2026 rate landscape: Expect bank statement loan rates between 6.5%-7.5%, typically 0.5-1.5% higher than conventional mortgages but accessible to self-employed borrowers who cannot document income traditionally[2][3].

✅ Flexible qualification criteria: Minimum credit scores start at 620-640 FICO, debt-to-income ratios up to 50%, and loan amounts reaching $1.5-3 million for various property types[2][3][6].

✅ Strategic preparation pays off: Seasoning assets for 60+ days, combining business and personal accounts, and maintaining consistent deposits significantly improve approval odds and rate offerings[6].

Understanding Bank Statement Loans for Self-Employed Borrowers in 2026

Bank statement loans represent a specialized mortgage product designed specifically for self-employed individuals, entrepreneurs, freelancers, and business owners who struggle to document income through traditional means. Unlike conventional mortgages that rely heavily on W-2 forms and tax returns, these loans use bank deposit history as the primary income verification method.

What Makes Bank Statement Loans Different?

The fundamental difference lies in income calculation methodology. Traditional lenders examine tax returns, specifically Schedule C for sole proprietors or corporate tax returns for business owners. After deducting legitimate business expenses—vehicle costs, home office deductions, equipment depreciation, and operational expenses—the net profit often appears significantly lower than actual cash flow[1].

Bank statement loans flip this approach entirely. Lenders review 12-24 consecutive months of personal and/or business bank statements, adding all eligible deposits to calculate average monthly income[5][6]. This method captures the true earning power of self-employed professionals before tax-advantaged deductions reduce reported income.

“If Schedule C shows $35,000 net profit but bank statements demonstrate $75,000 in deposits, lenders qualify borrowers based on the $75,000 figure.”[1]

Who Benefits Most from Bank Statement Loans?

Several categories of self-employed professionals find exceptional value in bank statement financing:

- Independent contractors and 1099 workers who maximize tax deductions

- Small business owners with significant operational expenses

- Real estate investors utilizing depreciation and cost segregation

- Freelance professionals (consultants, designers, developers)

- Commission-based sales professionals with variable income

- Gig economy workers with multiple income streams

For self-employed professionals seeking specialized mortgage solutions, working with a best self-employed mortgage broker in Toronto can streamline the qualification process significantly.

The Income Boost Advantage 💰

The most compelling benefit of bank statement loans emerges in the income calculation. Consider this real-world scenario:

Traditional Mortgage Approach:

- Gross business revenue: $150,000

- Business expenses and deductions: $75,000

- Schedule C net profit: $75,000

- Qualifying monthly income: $6,250

Bank Statement Loan Approach:

- Total deposits over 24 months: $300,000

- Average monthly deposits: $12,500

- Qualifying monthly income: $12,500

This represents a $6,250 monthly income increase—or $75,000 annually—purely through different calculation methods. This dramatic difference can mean qualifying for a home worth $200,000-300,000 more than conventional financing would allow.

Bank Statement Loans for Self-Employed: How to Qualify and Maximize Rates in 2026 – Documentation Requirements

The cornerstone of bank statement loan qualification centers on providing the right documentation for the right duration. Understanding the 12-month versus 24-month decision significantly impacts approval likelihood and rate offerings.

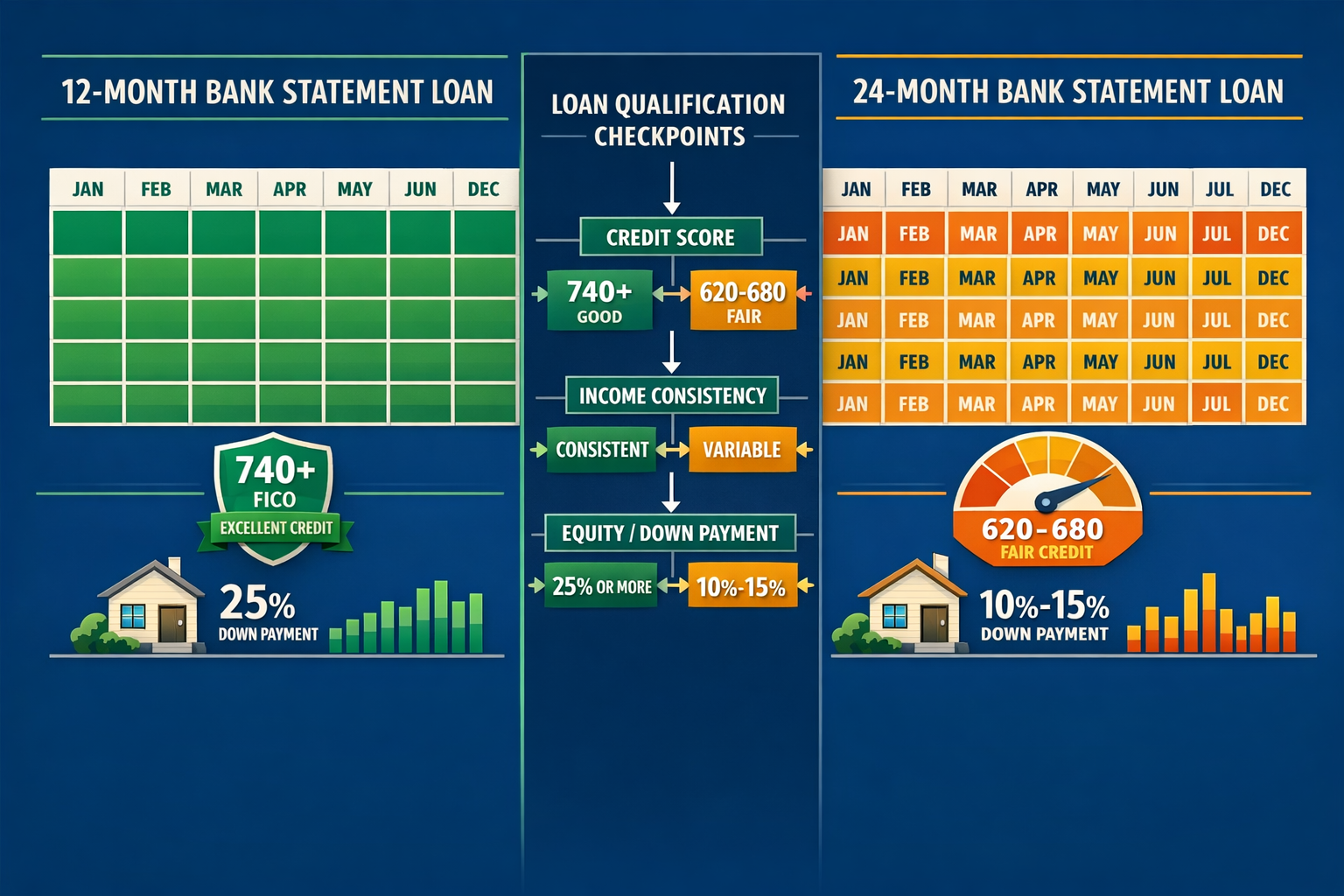

12-Month Bank Statement Qualification

Qualifying with just 12 months of bank statements offers faster processing and less documentation burden, but requires meeting stricter criteria[1]:

Credit Score Requirements:

- Minimum 740 FICO score (excellent credit)

- Clean credit history with no recent delinquencies

- Low credit utilization ratios (below 30%)

Income Consistency Standards:

- Minimal month-to-month deposit variability

- Steady, predictable income patterns

- Limited seasonal fluctuations

Equity and Down Payment:

- Minimum 25% down payment for purchases

- 75% maximum loan-to-value ratio for refinances

- Substantial cash reserves (typically 6+ months)

Self-Employment History:

- Well-established business (3+ years preferred)

- Same industry or related field experience

- Strong business fundamentals

24-Month Bank Statement Qualification

Most self-employed borrowers qualify using 24 months of consecutive bank statements, which provides lenders with a more comprehensive income picture[1]:

Broader Credit Acceptance:

- Minimum 620-640 FICO scores accepted[3][6]

- Some lenders (like Carrington) accept 600+ FICO[3]

- More tolerance for past credit challenges

Income Flexibility:

- Variable or seasonal income patterns accepted

- Multiple income streams combined

- Business growth trajectories considered

Lower Down Payment Options:

- Down payments as low as 10-15%

- Higher loan-to-value ratios available

- More accessible for first-time buyers

Newer Business Acceptance:

- Two years of self-employment history typically required[5]

- One year accepted with related work experience or education[5]

- Industry expertise valued over business longevity

What Counts as Eligible Deposits?

Understanding which deposits lenders include—and exclude—from income calculations proves critical for maximizing qualifying income:

✅ Included Deposits:

- Business revenue and client payments

- Freelance and contractor payments

- Commission income

- Rental income deposits

- Investment income and dividends

- Consistent transfers from business to personal accounts

❌ Excluded Deposits:

- One-time transfers between own accounts

- Loan proceeds or borrowed funds

- Tax refunds

- Gifts or inheritance deposits

- Non-recurring windfalls

- Reimbursements

Lenders typically apply an expense factor ranging from 0% to 50% depending on account type[5]. Personal account deposits might receive a 0% expense factor (100% counted as income), while business account deposits might have 25-50% deducted to account for business expenses before calculating qualifying income.

Combining Personal and Business Accounts

Most lenders allow—and encourage—combining deposits from both personal and business bank accounts to maximize qualifying income[1][7]. This approach captures the complete financial picture:

Strategic Account Combination:

- Business checking accounts showing client payments and revenue

- Personal checking accounts receiving transfers and personal income

- Savings accounts with consistent deposit patterns

- Multiple business entities under the same ownership

However, some lenders require choosing either personal OR business statements exclusively[1]. Understanding each lender’s specific policies helps optimize the application strategy.

For professionals in specific fields, specialized programs exist. Self-employed doctors and self-employed lawyers often qualify for enhanced terms given their professional credentials.

Maximizing Rates and Terms for Bank Statement Loans in 2026

The 2026 mortgage landscape presents unique opportunities for self-employed borrowers seeking competitive bank statement loan rates. Understanding the rate environment and optimization strategies can save tens of thousands of dollars over the loan lifetime.

2026 Rate Expectations for Bank Statement Loans

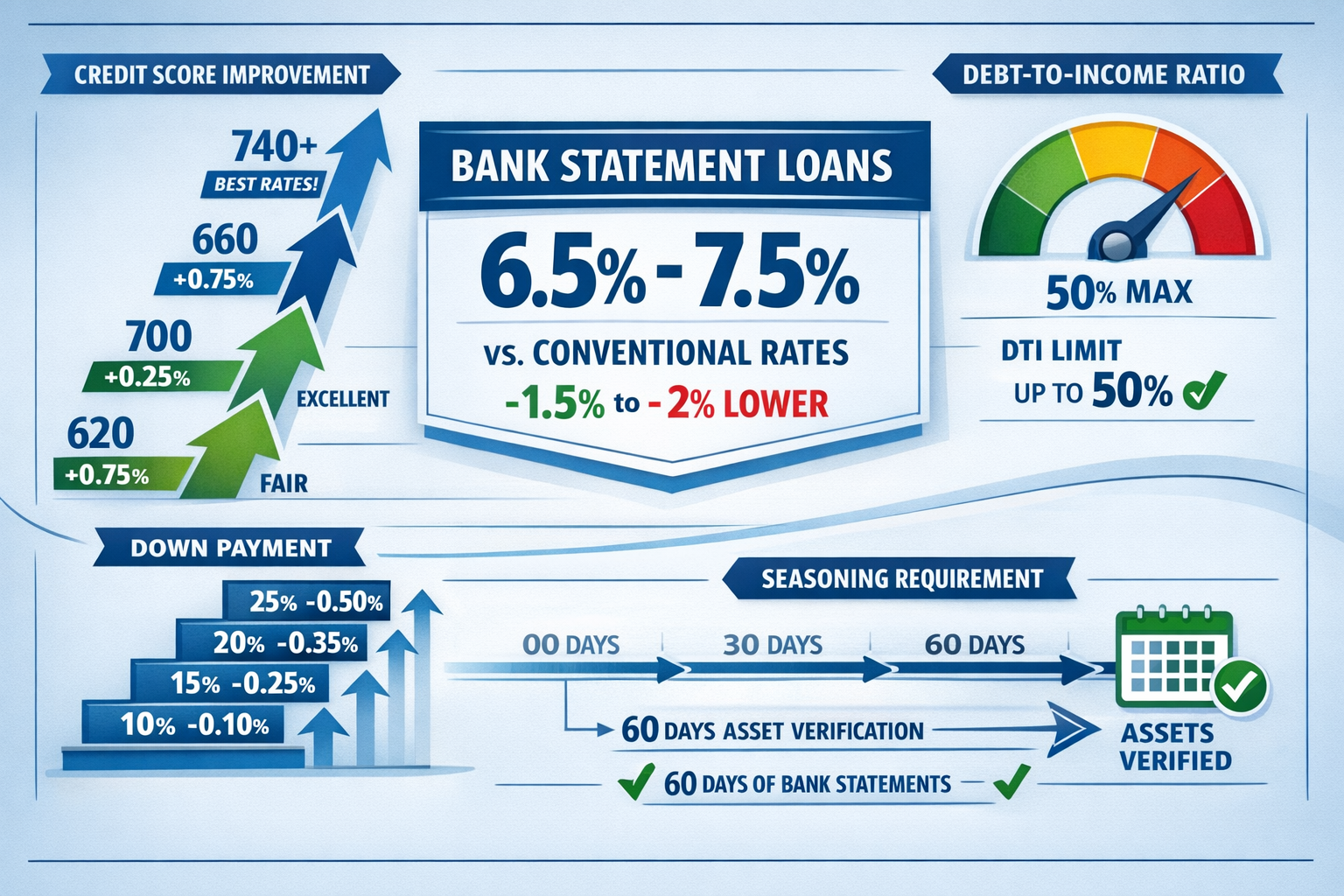

Bank statement loans typically carry interest rates 0.5-1.5% higher than conventional mortgage rates[2][3]. In 2026, borrowers should expect:

Bank Statement Loan Rate Range:

- Excellent credit (740+): 6.5-7.0%

- Good credit (680-739): 6.75-7.25%

- Fair credit (620-679): 7.0-7.5%

Conventional Mortgage Comparison (2026):

- Excellent credit: 6.0-6.5%

- Good credit: 6.25-6.75%

- Fair credit: 6.5-7.0%

While bank statement loans cost more, the qualification advantage often outweighs the rate premium. A self-employed borrower who cannot qualify for conventional financing at 6.25% but can secure a bank statement loan at 7.0% gains access to homeownership that would otherwise remain out of reach.

With the Bank of Canada’s recent rate decisions influencing the broader mortgage market, understanding how these changes affect alternative lending products becomes crucial.

Credit Score Impact on Rates and Terms

Credit scores dramatically influence both approval likelihood and rate offerings for bank statement loans:

| Credit Score Range | Minimum Down Payment | Expected Rate Premium | Maximum DTI Ratio |

|---|---|---|---|

| 740+ (Excellent) | 10-15% | +0.5% vs conventional | 45% |

| 680-739 (Good) | 15-20% | +0.75-1.0% vs conventional | 45-50% |

| 640-679 (Fair) | 20-25% | +1.0-1.25% vs conventional | 50% |

| 620-639 (Minimum) | 25%+ | +1.25-1.5% vs conventional | 43-45% |

Rate Optimization Strategy: Borrowers with credit scores in the 660-720 range should consider delaying their application by 3-6 months to improve credit scores. A 40-point improvement from 680 to 720 can reduce rates by 0.25-0.375%, saving approximately $50-75 monthly on a $400,000 loan—or $18,000-27,000 over a 30-year term.

For those looking to improve their credit profile, reviewing strategies to improve your credit score in Canada provides actionable steps.

Down Payment and Loan-to-Value Optimization

The down payment percentage directly correlates with rate offerings and approval likelihood:

Down Payment Tiers and Benefits:

10-15% Down Payment:

- Available for excellent credit (740+) borrowers

- Highest rate premiums

- Requires perfect income documentation

- Limited lender options

20-25% Down Payment:

- Eliminates mortgage insurance requirements

- Broader lender selection

- Moderate rate premiums

- Standard qualification criteria

25%+ Down Payment:

- Best available rates

- Maximum lender flexibility

- Can qualify with 12 months of statements[1]

- Compensates for credit or income weaknesses

Strategic Consideration: Borrowers with 15% available for down payment should evaluate whether waiting 6-12 months to accumulate 20% provides better long-term value through rate reduction and eliminated mortgage insurance.

Debt-to-Income Ratio Management

Bank statement loans offer exceptional DTI flexibility, accepting ratios up to 50%[2][4]—significantly higher than conventional mortgages that typically cap at 43-45%.

DTI Calculation for Bank Statement Loans:

Monthly qualifying income (from bank statements): $10,000

- Proposed mortgage payment (PITI): $3,000

- Auto loan: $500

- Student loans: $300

- Credit cards (minimum payments): $200

- Total monthly debt: $4,000

- DTI Ratio: 40% ✅ Approved

This flexibility proves invaluable for self-employed borrowers who may carry business debt, equipment financing, or multiple properties.

DTI Optimization Strategies:

- Pay down revolving debt before application

- Refinance high-payment debts to lower monthly obligations

- Remove authorized user accounts that don’t belong to you

- Document non-borrower income (spouse, partner) if applicable

- Increase qualifying income by including all eligible accounts

Asset Seasoning and Reserve Requirements

Lenders require 60-day seasoning for down payment and closing cost funds[6]. This means money must have been in your accounts for at least 60 days before application to count as genuine assets rather than borrowed funds.

Seasoning Timeline Strategy:

90+ Days Before Application:

- Consolidate funds into primary accounts

- Avoid large deposits or transfers

- Maintain consistent balances

60-90 Days Before Application:

- Finalize down payment account

- Document any large deposits with paper trail

- Build reserve accounts

30-60 Days Before Application:

- Cease unnecessary transfers

- Maintain stable balances

- Prepare bank statement copies

Reserve Requirements by Property Type:

- Primary residence: 6 months PITI reserves

- Second home: 9-12 months PITI reserves

- Investment property: 12+ months PITI reserves

Property Type and Loan Amount Considerations

Bank statement loans accommodate diverse property types and substantial loan amounts[2][3]:

Eligible Property Types:

- ✅ Primary residences

- ✅ Second homes and vacation properties

- ✅ Investment properties (1-4 units)

- ✅ Non-warrantable condominiums

- ✅ Mixed-use properties (residential + commercial)

Loan Amount Ranges:

- Standard programs: Up to $1.5 million[2]

- Jumbo programs: $1.5-3.0 million[3]

- Ultra-jumbo programs: $3.0 million+ (limited lenders)

Loan-to-Value by Property Type:

- Primary residence: Up to 90% LTV

- Second home: Up to 85% LTV

- Investment property: Up to 80% LTV

Investment-focused borrowers should explore alternative income verification options and understand how B-lender mortgage rates in Toronto compare to bank statement loan offerings.

Common Mistakes to Avoid When Pursuing Bank Statement Loans

Self-employed borrowers frequently encounter preventable obstacles during the bank statement loan process. Understanding these critical mistakes helps ensure smooth approval and optimal terms.

Mistake #1: Inconsistent or Incomplete Bank Statements

The Problem: Submitting bank statements with missing months, pages, or transactions raises red flags and can result in immediate denial.

The Solution:

- Request complete, consecutive statements covering all required months

- Ensure every page includes account holder name and account number

- Verify no months are skipped in the sequence

- Include all pages, even blank transaction pages

- Obtain official bank-issued statements (not screenshots or printouts)

Mistake #2: Large Unexplained Deposits

The Problem: Lenders scrutinize deposits exceeding 25% of average monthly income. Unexplained large deposits suggest borrowed funds or non-recurring windfalls that shouldn’t count toward qualifying income[6].

The Solution:

- Document all large deposits with source verification

- Provide invoices for large client payments

- Show tax refund documentation

- Explain one-time business transactions

- Avoid depositing borrowed money during the review period

Mistake #3: Mixing Business and Personal Expenses Carelessly

The Problem: Excessive personal expenses running through business accounts—or vice versa—complicates income calculation and raises questions about financial management.

The Solution:

- Maintain clear separation between business and personal finances

- Use business accounts exclusively for business transactions when possible

- Document any necessary crossover expenses

- Establish consistent transfer patterns from business to personal accounts

- Work with a bookkeeper to maintain clean records

Mistake #4: Failing to Prepare for Self-Employment History Verification

The Problem: Lenders verify self-employment through business licenses, tax returns, CPAs, or clients. Lack of documentation can derail applications.

The Solution:

- Maintain current business licenses and registrations

- File tax returns on time (even if using bank statements for income)

- Prepare CPA letter confirming self-employment status

- Compile client contracts or invoices demonstrating ongoing business

- Document business website, marketing materials, and professional presence

Mistake #5: Ignoring the Expense Factor Impact

The Problem: Borrowers assume 100% of deposits count as income, but lenders apply expense factors of 25-50% to business accounts[5].

The Solution:

- Understand your lender’s expense factor methodology

- Maximize personal account deposits when possible

- Maintain clean separation allowing lower expense factors

- Choose lenders with favorable expense factor policies

- Calculate realistic qualifying income before application

Mistake #6: Not Shopping Multiple Lenders

The Problem: Bank statement loan programs vary dramatically between lenders in terms of rates, fees, expense factors, and qualification criteria.

The Solution:

- Compare at least 3-5 specialized lenders

- Evaluate total cost (rate + fees) rather than rate alone

- Assess qualification requirements and flexibility

- Consider lender experience with self-employed borrowers

- Review customer testimonials and track record

Mistake #7: Applying Before Financial House is in Order

The Problem: Rushing into applications before optimizing credit, accumulating reserves, or seasoning assets leads to denials or poor terms.

The Solution:

- Plan 6-12 months ahead of desired purchase

- Address credit issues proactively

- Build reserves and season assets

- Stabilize income patterns

- Consult with specialized mortgage professionals early

Avoiding the top 5 mistakes self-employed homebuyers make significantly improves approval odds and final loan terms.

Step-by-Step Application Process for Bank Statement Loans

Successfully navigating the bank statement loan application requires understanding each phase and preparing accordingly. This systematic approach maximizes approval likelihood and optimal rate offerings.

Phase 1: Pre-Application Preparation (60-90 Days Before)

Financial Documentation Assembly:

- Gather 12-24 months of bank statements for all relevant accounts

- Review statements for completeness and address any missing pages

- Compile business documentation: licenses, articles of incorporation, DBA registrations

- Prepare identification documents: driver’s license, passport, Social Security card

- Assemble asset documentation: investment accounts, retirement accounts, additional properties

Financial Optimization:

- Pay down revolving debt to improve DTI ratios

- Build cash reserves to meet seasoning requirements

- Stabilize deposit patterns by maintaining consistent income flows

- Address credit report issues through dispute or resolution

- Consolidate accounts to simplify documentation

Lender Research and Selection:

- Identify specialized bank statement loan lenders

- Compare program requirements and rate offerings

- Evaluate lender reputation and customer reviews

- Assess responsiveness and self-employed expertise

- Determine best fit for your specific situation

Phase 2: Formal Application Submission (30-45 Days Before Closing)

Initial Application Package:

- Complete loan application (1003 form) with accurate information

- Submit all bank statements in organized, chronological order

- Provide business documentation establishing self-employment

- Include asset statements showing reserves and down payment

- Authorize credit report pull and review for accuracy

Income Calculation Review:

- Verify lender’s income calculation methodology

- Confirm expense factor application to business accounts

- Review qualifying income amount and ensure alignment with expectations

- Address any deposit questions proactively with documentation

- Clarify account combination approach (personal + business)

Rate Lock Decision:

- Evaluate current rate environment and trends

- Consider lock period length (30, 45, 60 days)

- Assess rate lock costs versus float risk

- Review rate lock agreement terms carefully

- Confirm rate lock in writing with all details

Phase 3: Underwriting and Documentation (15-30 Days Before Closing)

Underwriter Review Process: The underwriter analyzes all submitted documentation, calculates qualifying income, verifies assets, and assesses overall credit worthiness. This phase typically generates conditions—requests for additional documentation or clarification.

Common Underwriting Conditions:

- Large deposit explanations with source documentation

- Updated bank statements if application extends beyond initial submission

- Business verification through CPA letter or tax transcripts

- Asset seasoning documentation showing 60+ day history

- Credit inquiry explanations for recent credit applications

- Employment verification for any W-2 income included

- Property appraisal meeting value requirements

Condition Response Strategy:

- Respond promptly to all underwriter requests (within 24-48 hours)

- Provide complete documentation addressing every aspect of conditions

- Include explanatory letters when circumstances require context

- Maintain communication with loan officer throughout process

- Avoid new credit applications or large financial changes

Phase 4: Final Approval and Closing (0-15 Days)

Clear to Close Status: Once all conditions are satisfied, the loan receives Clear to Close status, authorizing closing preparation.

Pre-Closing Requirements:

- Final bank statements showing down payment and closing cost funds

- Homeowner’s insurance proof with lender named as mortgagee

- Wire transfer instructions for down payment and closing costs

- Final walkthrough of property (purchase transactions)

- Closing disclosure review confirming all terms and costs

Closing Day Checklist:

- ✅ Government-issued photo ID

- ✅ Cashier’s check or wire confirmation for closing costs

- ✅ Proof of homeowner’s insurance

- ✅ Review all closing documents before signing

- ✅ Ask questions about any unclear terms or charges

- ✅ Obtain copies of all signed documents

- ✅ Receive keys and property access

Post-Closing Considerations:

- Set up mortgage payment through automatic withdrawal

- File closing documents in secure location

- Update homeowner’s insurance with final loan details

- Begin building equity through consistent payments

- Monitor property value and refinance opportunities

For contractors and specialized professionals, understanding self-employed mortgages for contractors provides additional industry-specific insights.

Alternative Financing Options for Self-Employed Borrowers

While bank statement loans offer exceptional value for many self-employed professionals, understanding alternative financing paths ensures selecting the optimal solution for specific circumstances.

Stated Income Mortgages

Overview: Stated income mortgages allow borrowers to declare income without extensive documentation, relying primarily on credit score, assets, and down payment.

Ideal For:

- High-net-worth individuals with substantial assets

- Borrowers with complex income structures

- Privacy-focused applicants

- Those with minimal documentation available

Key Differences from Bank Statement Loans:

- Less documentation required overall

- Higher down payments typically needed (25-30%+)

- Rate premiums may be higher

- Stricter credit requirements (720+ often required)

Asset-Based Mortgages

Overview: Asset-based mortgages qualify borrowers based on total asset value rather than income, ideal for retirees or investors with substantial portfolios but limited income.

Qualification Approach: Lenders divide total liquid assets by 60-120 months to calculate “asset-derived income” for qualification purposes.

Example Calculation:

- Total liquid assets: $1,200,000

- Division factor: 60 months

- Qualifying monthly income: $20,000

Best For:

- Retirees with substantial investment portfolios

- Real estate investors with significant equity

- Business owners with illiquid business value but liquid assets

- High-net-worth individuals with minimal traditional income

Portfolio Loans from Community Banks

Overview: Some community banks and credit unions offer portfolio loans—mortgages they keep on their own books rather than selling to secondary markets, allowing more flexibility.

Advantages:

- Relationship-based underwriting

- Flexible documentation requirements

- Local decision-making authority

- Customized loan structures

Disadvantages:

- Limited availability

- Relationship requirements (existing accounts)

- Potentially higher rates

- Smaller loan amounts

Private Lenders and Alternative Financing

For borrowers who don’t qualify for bank statement loans or need faster closing timelines, private loan lenders in Ontario offer short-term solutions with flexible qualification criteria.

Private Lending Characteristics:

- Approval speed: 1-2 weeks typical

- Documentation: Minimal requirements

- Rates: Significantly higher (8-15%+)

- Terms: Shorter duration (6-24 months)

- Use case: Bridge financing, credit repair period, unique properties

Conventional Mortgages with Tax Return Documentation

Self-employed borrowers who can document sufficient income through tax returns should still consider conventional financing as the baseline comparison.

When Conventional Makes Sense:

- Tax returns show adequate qualifying income

- Minimal business deductions taken

- Established business with consistent profitability

- Lower rates justify documentation effort

Conventional Advantages:

- Lowest available rates (0.5-1.5% lower than bank statement)

- Broadest lender selection

- Standard qualification criteria

- Lower down payment options (5-10% possible)

Understanding how to get approved for a mortgage using your business income provides comprehensive comparison of all self-employed financing approaches.

Frequently Asked Questions About Bank Statement Loans

How much income can I qualify with using bank statements?

Lenders calculate income by adding all eligible deposits over 12 or 24 months, then dividing by the number of months to determine average monthly income[5][6]. They may apply an expense factor of 0-50% depending on account type. For example, $150,000 in total deposits over 24 months equals $6,250 monthly income. With a 25% expense factor, qualifying income becomes $4,688 monthly.

Can I use bank statement loans for investment properties?

Yes, bank statement loans are available for primary residences, second homes, and investment properties[2]. Investment properties typically require larger down payments (20-25%) and may have slightly higher rates, but they offer the same income calculation advantages as primary residence loans.

What if I have multiple businesses or income sources?

Most lenders allow combining income from multiple businesses and income sources by reviewing all relevant bank accounts[1][7]. This comprehensive approach captures total earning capacity across all ventures, potentially maximizing qualifying income significantly.

How long does the bank statement loan process take?

Typical timeline ranges from 30-45 days from application to closing, similar to conventional mortgages. Well-prepared borrowers with complete documentation and responsive communication can sometimes close in 21-30 days, while complex situations may extend to 60 days.

Can I refinance using bank statement loans?

Absolutely. Bank statement loans work for both purchase and refinance transactions, including cash-out refinancing. The same qualification criteria apply, with equity requirements varying based on refinance type and loan-to-value limits.

What happens if my income varies significantly month to month?

Seasonal or variable income is acceptable with bank statement loans, particularly when using 24 months of statements[1]. The averaging methodology smooths fluctuations, and lenders focus on overall trends rather than individual month variations. Providing context through business cycles or industry seasonality helps underwriters understand patterns.

Do I still need to file tax returns if using bank statement loans?

Yes. While bank statement loans don’t use tax returns for income qualification, lenders typically require proof that tax returns have been filed to verify legitimate self-employment status[5]. You don’t need to provide the actual returns in most cases, but demonstrating compliance with tax obligations remains important.

Conclusion: Maximizing Your Bank Statement Loan Success in 2026

Bank Statement Loans for Self-Employed: How to Qualify and Maximize Rates in 2026 represent a powerful financing tool that aligns with the financial realities of modern self-employment. By leveraging actual deposit history rather than tax-reduced income, self-employed professionals can unlock $3,500+ in additional monthly qualifying income, accessing homeownership opportunities that conventional financing cannot provide.

Your Action Plan for Bank Statement Loan Success

Immediate Steps (Next 30 Days):

- Gather 12-24 months of bank statements for all personal and business accounts

- Calculate your potential qualifying income using total deposits divided by months

- Review your credit report and address any errors or issues

- Research specialized lenders offering bank statement loan programs

- Consult with a self-employed mortgage specialist to assess your specific situation

Short-Term Preparation (30-90 Days):

- Optimize your credit score to access better rate tiers

- Build cash reserves meeting seasoning requirements (60+ days)

- Stabilize deposit patterns by maintaining consistent income flows

- Address any large or unusual deposits with proper documentation

- Compare multiple lender offerings to identify optimal terms

Long-Term Strategy (90+ Days):

- Maintain clean, organized financial records across all accounts

- Separate business and personal finances clearly

- Build substantial reserves exceeding minimum requirements

- Monitor rate environment and refinance opportunities

- Establish relationships with specialized mortgage professionals

The 2026 Advantage

The current mortgage landscape in 2026 offers self-employed borrowers more options than ever before. With rates in the 6.5-7.5% range for bank statement loans, the premium over conventional financing remains reasonable given the dramatic qualification advantage these programs provide.

Understanding that your actual earning capacity—reflected in bank deposits—matters more than tax return income opens doors previously closed to self-employed professionals. Whether you’re a freelance consultant depositing $75,000 annually while showing $35,000 in Schedule C income, a contractor with substantial equipment deductions, or a business owner reinvesting profits, bank statement loans recognize your true financial strength.

The path to homeownership as a self-employed professional requires strategic preparation, comprehensive documentation, and expert guidance. By following the qualification strategies, avoiding common mistakes, and optimizing every aspect of your application, you can secure competitive financing that reflects your actual earning power.

Ready to explore your bank statement loan options? Connect with specialized mortgage professionals who understand self-employed financing and can guide you through the process from initial consultation through successful closing. Your entrepreneurial success deserves financing solutions that recognize your true income potential.

For comprehensive guidance on self-employed mortgage strategies, access our self-employed mortgage Q&A resource to get instant answers to your specific questions.

References

[1] Bank Statement Loan Requirements – https://www.mcgowanmortgages.com/bank-statement-loan-requirements/

[2] Bank Statement Loans – https://crosscountrymortgage.com/mortgage/loans/non-qm/bank-statement-loans/

[3] Bank Statement Loans Self Employed Borrowers – https://nationalmortgageprofessional.com/news/bank-statement-loans-self-employed-borrowers

[4] Mortgage Self Employed 1099 Business Get Approved – https://themortgagereports.com/18303/mortgage-self-employed-1099-business-get-approved

[5] Bank Statement Loans – https://griffinfunding.com/non-qm-mortgages/bank-statement-loans/

[6] Bank Statements For Mortgages In Complete Guide To Requirements Red Flags And Approval Strategies – https://www.amerisave.com/learn/bank-statements-for-mortgages-in-complete-guide-to-requirements-red-flags-and-approval-strategies

[7] Bank Statement Loans – https://foundationmortgage.com/bank-statement-loans/