February 10, 2026

Buying Your First Home in Toronto’s 2026 Buyer’s Market: A Step-by-Step Guide

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

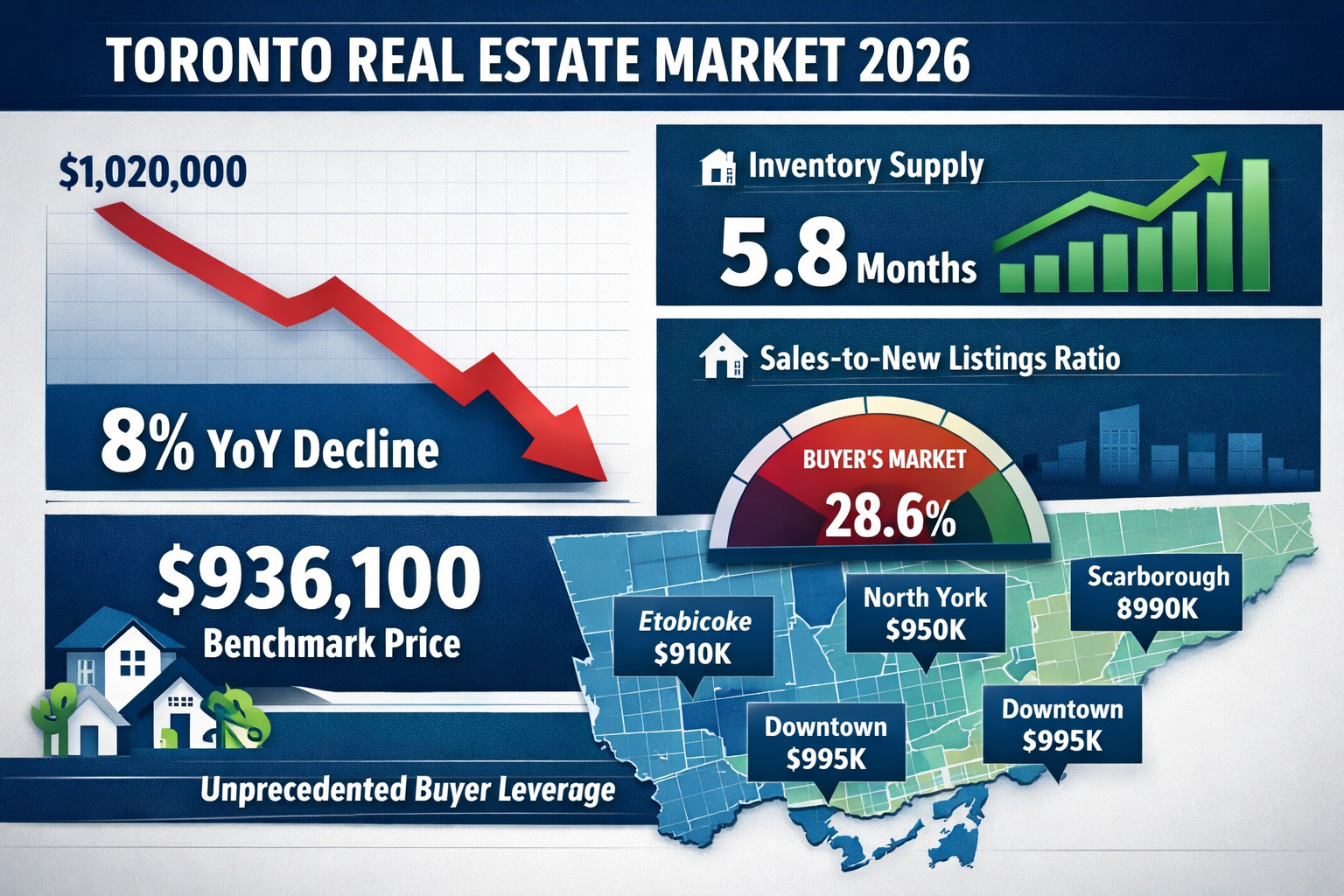

The Toronto real estate market has undergone a dramatic transformation. For the first time in years, first-time homebuyers hold unprecedented negotiating power. With benchmark prices plummeting to $936,100—an 8% year-over-year decline—and inventory levels reaching a 5.8-month supply, the tables have turned decisively in favor of purchasers[3]. This comprehensive guide to buying your first home in Toronto’s 2026 buyer’s market will equip you with the knowledge, strategies, and actionable steps needed to capitalize on this rare opportunity before market conditions shift once again.

The current market dynamics represent a significant departure from the frenzied bidding wars and seller-dominated conditions that characterized previous years. Sales activity has dropped 19.9% year-over-year, while the sales-to-new-listings ratio has fallen to just 28.6%[3]. For aspiring homeowners who have been priced out of the market, this window of opportunity demands strategic action and informed decision-making.

Key Takeaways

✅ Toronto’s housing market has shifted to a buyer’s market with 5.8 months of inventory supply and benchmark prices down 8% year-over-year to $936,100, creating unprecedented leverage for first-time purchasers[3].

✅ Strategic preparation is essential: improving your credit score, understanding mortgage pre-approval requirements, and calculating true affordability including closing costs will position you for success in negotiations.

✅ Condo prices offer the most accessible entry point for first-time buyers, though the segment has seen a 26% sales decline, meaning sellers are increasingly motivated to negotiate[3].

✅ Professional guidance matters: working with experienced mortgage brokers and real estate agents who understand current market conditions can save thousands of dollars and prevent costly mistakes.

✅ Act strategically but don’t rush: while the buyer’s market provides advantages, conducting thorough due diligence on property condition, neighborhood trends, and long-term value remains critical to making a sound investment.

Understanding Toronto’s 2026 Buyer’s Market Dynamics

What Makes 2026 a Buyer’s Market?

A buyer’s market occurs when housing supply exceeds demand, giving purchasers greater negotiating power and choice. Toronto’s current market exhibits all the classic indicators of buyer-favorable conditions. The 5.8-month inventory supply significantly exceeds the 4-month threshold that typically defines a balanced market[3].

The sales-to-new-listings ratio (SNLR) provides another critical indicator. At 28.6% for the Greater Toronto Area and just 26% for the City of Toronto specifically, these figures sit well below the 40-55% range associated with balanced conditions[3]. When the SNLR falls below 40%, sellers lose pricing power and buyers gain leverage.

Market conditions at a glance:

| Metric | January 2026 | January 2025 | Change |

|---|---|---|---|

| GTA Benchmark Price | $936,100 | $1,018,000 | -8.0% |

| Average Home Price | $973,289 | $1,041,000 | -6.5% |

| Total Sales | 3,082 | 3,848 | -19.9% |

| Active Listings | 17,975 | 17,150 | +4.8% |

| Sales-to-New-Listings Ratio | 28.6% | 31.0% | -2.4 pts |

This represents the first time in five years that average prices have fallen below $1 million[3], opening doors for buyers who were previously priced out of the market.

Price Trends Across Property Types

Different property segments have experienced varying degrees of price pressure. Understanding these trends helps first-time buyers identify where the best opportunities exist:

Condos have been hit hardest, with sales declining 26% year-over-year[3]. The investor demand that drove condo prices during the pandemic has largely evaporated, creating opportunities for owner-occupiers. The City of Toronto’s median price reached $749,500 in January 2026, down 6.3% year-over-year[3].

Freehold townhomes experienced a 24% sales decline, followed by semi-detached homes at 20% and detached homes at 14%[3]. The relatively smaller decline in detached home sales suggests this segment maintains stronger demand, though prices remain under pressure.

For first-time buyers working with limited budgets, condos and townhomes typically represent the most accessible entry points. The current market conditions make these segments particularly attractive for negotiation.

Expert Forecasts and Market Skepticism

The Toronto Real Estate Board (TRREB) forecasts 60,000 to 70,000 home sales in 2026[5], though the organization acknowledges expecting “mid to high single-digit year-over-year price declines in the first half of the year”[2]. TRREB projects the GTA average price range will settle between $1 million to $1.03 million for 2026[6].

However, market analysts express considerable skepticism about these optimistic projections. Critical observers cite “escalating trade tensions, weakening economy, and declining sales” as factors that contradict recovery expectations[2]. One analyst predicts 2026 is “more likely to underperform 2025 than rebound from it,” noting that employment growth is weakening and consumer confidence is declining[2].

For first-time buyers, this divergence in forecasts underscores an important reality: the current buyer’s market may persist longer than some expect, providing an extended window of opportunity for those who prepare strategically.

Preparing Financially for Buying Your First Home in Toronto’s 2026 Buyer’s Market

Assessing Your True Budget and Affordability

Before beginning your home search, establishing a realistic budget is essential. Many first-time buyers make the mistake of focusing solely on the purchase price without accounting for the full spectrum of costs involved in homeownership.

Calculate your maximum purchase price using the following factors:

💰 Gross Debt Service Ratio (GDS): Lenders typically require that your housing costs (mortgage payments, property taxes, heating, and 50% of condo fees if applicable) don’t exceed 32-39% of your gross monthly income.

💰 Total Debt Service Ratio (TDS): Your total debt obligations (housing costs plus car loans, credit cards, student loans, etc.) should not exceed 42-44% of gross monthly income.

💰 Down Payment Requirements:

- 5% minimum for homes under $500,000

- 10% for the portion between $500,000-$999,999

- 20% for homes $1 million and above

With Toronto’s median price at $749,500[3], many first-time buyers can enter the market with less than 20% down, though this requires mortgage default insurance (CMHC, Sagen, or Canada Guaranty).

Understanding Closing Costs

One of the most common first-time home-buyer mistakes is underestimating closing costs. These additional expenses typically range from 1.5% to 4% of the purchase price.

Essential closing costs to budget for:

- Land Transfer Tax: In Toronto, buyers pay both provincial and municipal land transfer tax. For a $750,000 home, expect approximately $23,100 in combined land transfer taxes.

- Legal Fees: $1,500-$3,000 for a real estate lawyer to handle the transaction

- Home Inspection: $400-$700 for a thorough property inspection

- Title Insurance: $250-$400 to protect against title defects

- Property Tax Adjustment: Reimbursing the seller for prepaid property taxes

- Moving Costs: $500-$2,000 depending on distance and volume

For comprehensive details on what to expect, review our guide on understanding closing costs in Toronto.

Leveraging the First-Time Home Buyer Tax Credit

The federal government offers several programs to assist first-time buyers. The Home Buyers’ Plan (HBP) allows you to withdraw up to $35,000 from your RRSP tax-free to purchase your first home (or $70,000 for couples). You have 15 years to repay these funds to your RRSP.

Additionally, the First-Time Home Buyer Incentive provides a shared-equity mortgage with the government contributing 5-10% of the purchase price (though income and price caps apply). The First-Time Home Buyers’ Tax Credit offers up to $1,500 in tax relief.

Learn more about maximizing these benefits in our comprehensive guide to the first-time home buyer tax credit in Canada.

Improving Your Credit Score

Your credit score directly impacts your mortgage approval and interest rate. In the current market, even a 0.25% difference in interest rate can save thousands of dollars over the life of your mortgage.

Quick credit score improvements:

🔹 Pay down credit card balances below 30% of available credit 🔹 Ensure all bills are paid on time (set up automatic payments) 🔹 Don’t close old credit accounts (length of credit history matters) 🔹 Dispute any errors on your credit report 🔹 Avoid applying for new credit in the months before mortgage application

For actionable strategies, see our 5 tips to rapidly improve your credit score.

Getting Pre-Approved for a Mortgage

Mortgage pre-approval serves two critical functions: it establishes your maximum borrowing capacity and demonstrates to sellers that you’re a serious, qualified buyer. In a buyer’s market, pre-approval strengthens your negotiating position by showing you can close quickly.

Pre-approval typically requires:

- Proof of income (recent pay stubs, T4s, NOAs for self-employed)

- Employment verification

- Down payment confirmation (bank statements, investment accounts)

- Credit check and authorization

- Debt documentation (credit cards, loans, leases)

Pre-approvals typically last 90-120 days and lock in an interest rate, protecting you if rates rise during your home search. Working with an experienced mortgage broker can help you access multiple lenders and secure the most competitive rates.

Step-by-Step Process for Buying Your First Home in Toronto’s 2026 Buyer’s Market

Step 1: Assemble Your Professional Team

Successful home purchases require expert guidance. In Toronto’s complex real estate market, the right professionals can save you tens of thousands of dollars and prevent costly mistakes.

Essential team members:

👥 Mortgage Broker: Unlike banks that offer only their own products, mortgage brokers access multiple lenders and can often secure better rates and terms. They understand how to position your application for approval and can navigate complex situations.

👥 Real Estate Agent: Choose an agent with deep knowledge of your target neighborhoods and experience representing buyers in negotiations. In the current buyer’s market, an agent who understands how to leverage market conditions is invaluable.

👥 Real Estate Lawyer: Required to complete the transaction, a good lawyer reviews agreements, conducts title searches, and ensures your interests are protected.

👥 Home Inspector: A thorough inspection can uncover hidden issues that affect property value and provide leverage for price negotiations or repair requests.

Step 2: Define Your Search Criteria

With Toronto’s diverse neighborhoods offering vastly different lifestyles and price points, clarity on your priorities prevents decision paralysis and wasted time.

Consider these factors:

🏘️ Location priorities: Proximity to work, transit access, school districts, amenities, neighborhood character

🏠 Property type: Condo, townhouse, semi-detached, or detached home

📏 Size requirements: Bedrooms, bathrooms, square footage, outdoor space

🔮 Future needs: Growing family, home office, rental income potential

💵 Investment vs. lifestyle: Resale potential, neighborhood appreciation trends, personal enjoyment

In the current market, with 17,975 active listings[3], buyers have significantly more choice than in previous years. This abundance allows you to be selective and patient in finding the right property.

Step 3: Research Neighborhoods and Property Values

Understanding neighborhood dynamics and recent sale prices empowers informed decision-making. In a declining market, recent comparable sales matter more than older data.

Research strategies:

📊 Look at sold prices (not asking prices) for comparable properties in the past 30-60 days

📊 Track days-on-market trends (longer DOM indicates weaker seller position)

📊 Identify neighborhoods with improving vs. declining fundamentals

📊 Assess future development plans that could affect property values

📊 Visit neighborhoods at different times (weekdays, weekends, evenings)

Websites like HouseSigma and Zolo provide transparent sold data for Toronto properties. Your real estate agent can also provide detailed comparative market analyses (CMAs) for specific properties.

Step 4: View Properties and Conduct Due Diligence

With your criteria defined and financing secured, begin viewing properties. In the current buyer’s market, taking time for thorough evaluation is not only possible but recommended.

During property viewings:

✔️ Bring a checklist of must-haves and deal-breakers ✔️ Take photos and notes (properties blur together after viewing several) ✔️ Ask about property history, previous offers, reason for selling ✔️ Observe building condition, maintenance quality, neighbor interactions ✔️ Request condo documents early (status certificates, reserve fund studies, meeting minutes)

Red flags to watch for:

⚠️ Signs of water damage or moisture issues ⚠️ Structural cracks or foundation problems ⚠️ Outdated electrical or plumbing systems ⚠️ Inadequate condo reserve funds ⚠️ High special assessments or pending litigation ⚠️ Properties that have been listed multiple times or with price reductions

Don’t skip the professional home inspection. Even in a buyer’s market, inspection contingencies protect you from inheriting expensive problems.

Step 5: Make a Strategic Offer

This is where the buyer’s market advantage becomes tangible. With the sales-to-new-listings ratio at just 28.6%[3], sellers face limited competition and increasing pressure to accept reasonable offers.

Offer strategy considerations:

💡 Price below asking: In the current market, offering 5-10% below asking price is often reasonable, especially for properties with longer days-on-market.

💡 Include conditions: Financing, inspection, status certificate review (for condos), and insurance approval protect your interests.

💡 Closing date flexibility: Offering flexibility on closing dates can make your offer more attractive without costing you money.

💡 Deposit structure: While larger deposits show commitment, ensure you’re comfortable with the amount at risk.

💡 Personal touches: In a slower market, a personal letter to sellers can sometimes tip the scales, though this is secondary to price and terms.

Your real estate agent should provide a comparative market analysis showing recent sold prices for similar properties. Use this data to justify your offer price and prepare for potential counter-offers.

Step 6: Navigate Negotiations

In a buyer’s market, sellers often counter initial offers, but their negotiating position is weaker than in balanced or seller’s markets. Understanding negotiation dynamics maximizes your advantage.

Negotiation tactics:

🎯 Start lower than your maximum: Leave room for compromise while staying within your budget

🎯 Use inspection findings: Request price reductions or repairs for issues discovered during inspection

🎯 Leverage market data: Reference recent sold prices and market trends to justify your position

🎯 Stay emotionally detached: Be prepared to walk away if terms don’t meet your requirements

🎯 Consider creative solutions: Sometimes non-price terms (included appliances, early possession, assumption of existing mortgage) can bridge gaps

Remember that with sales down 19.9% year-over-year[3], sellers are increasingly motivated. Properties sitting on the market for 30+ days indicate sellers may be more flexible than their listing price suggests.

Step 7: Finalize Mortgage and Complete Conditions

Once your offer is accepted, you typically have 5-10 business days to satisfy conditions. Work efficiently but thoroughly during this period.

Condition fulfillment checklist:

✅ Finalize mortgage approval: Submit all required documentation to your lender ✅ Complete home inspection: Schedule within 3-5 days of accepted offer ✅ Review condo documents: For condos, carefully review status certificate, declarations, rules, financial statements ✅ Secure insurance: Obtain home insurance quotes and select a provider ✅ Arrange lawyer: Provide your lawyer with agreement details and coordinate closing

If inspection reveals significant issues, you have three options: request repairs, negotiate a price reduction to cover repair costs, or exercise your condition and walk away from the deal.

Step 8: Close the Transaction

As the closing date approaches, your lawyer handles most of the heavy lifting, but you’ll need to complete several tasks.

Pre-closing requirements:

📋 Final walkthrough: Typically 24-48 hours before closing, verify property condition and that agreed-upon repairs are completed

📋 Transfer down payment: Wire funds to your lawyer (confirm wire instructions by phone to prevent fraud)

📋 Review closing documents: Your lawyer will explain all documents you’re signing

📋 Arrange utilities: Set up electricity, gas, water, internet, and other services

📋 Plan moving logistics: Book movers, arrange time off work, notify relevant parties of address change

On closing day, your lawyer will register the property in your name, transfer funds to the seller, and provide you with keys. Congratulations—you’re now a Toronto homeowner!

Maximizing Your Advantage in Toronto’s 2026 Buyer’s Market

Targeting Motivated Sellers

Not all sellers face equal pressure. Identifying motivated sellers provides additional negotiating leverage beyond general market conditions.

Signs of seller motivation:

🔍 Properties listed for 30+ days 🔍 Recent price reductions 🔍 Vacant properties (sellers carrying two mortgages) 🔍 Estate sales or divorce situations 🔍 Listings with language like “motivated seller” or “all offers considered” 🔍 Properties with minor cosmetic issues that deter other buyers

In the current market, with inventory levels elevated and sales declining across all property types[3], the pool of motivated sellers has expanded significantly.

Considering Alternative Property Types

While detached homes remain aspirational for many buyers, alternative property types often provide better value and appreciation potential for first-time buyers.

Condos offer the lowest entry price point, with Toronto’s median at $749,500[3]. Despite the 26% sales decline[3], well-located condos in buildings with strong financials remain solid long-term investments. Look for buildings with adequate reserve funds, low special assessment history, and desirable amenities.

Townhomes provide a middle ground between condos and detached homes, often including outdoor space and less restrictive condo rules. The 24% sales decline in this segment[3] suggests opportunities for negotiation.

For buyers interested in generating rental income, understanding the tax implications of basement rental income can help evaluate properties with income potential.

Understanding Mortgage Rate Dynamics

Interest rates significantly impact affordability and long-term costs. The Bank of Canada’s policy decisions directly influence mortgage rates, though the relationship is complex.

In 2026, fixed and variable rate mortgages each offer distinct advantages:

Fixed-rate mortgages provide payment stability and protection against future rate increases. If you plan to stay in your home for 5+ years and value predictability, fixed rates may be appropriate.

Variable-rate mortgages typically start lower than fixed rates and can save money if rates decline. However, they carry risk if rates rise unexpectedly.

Your mortgage broker can help analyze your risk tolerance, financial situation, and rate forecasts to determine the optimal choice for your circumstances.

Avoiding Common First-Time Buyer Mistakes

Even in a favorable buyer’s market, costly mistakes can undermine your financial position. Common pitfalls include:

❌ Maxing out your budget: Just because you’re approved for a certain amount doesn’t mean you should spend it all. Leave room for unexpected expenses and lifestyle flexibility.

❌ Skipping inspections: The inspection cost is minimal compared to the potential cost of hidden problems.

❌ Ignoring resale potential: Even if this is your “forever home,” circumstances change. Consider how easily you could sell if needed.

❌ Overlooking ongoing costs: Property taxes, condo fees, utilities, maintenance, and insurance add up quickly.

❌ Making emotional decisions: Falling in love with a property can cloud judgment and lead to overpaying.

For a comprehensive overview, review our guide on first-time home-buyer mistakes to avoid.

Planning for Long-Term Success

Homeownership extends far beyond the purchase transaction. Strategic planning ensures your investment supports long-term financial goals.

Consider these forward-looking strategies:

🏡 Build equity faster: Making accelerated payments or annual lump-sum contributions can significantly reduce your amortization period and interest costs.

🏡 Maintain an emergency fund: Aim for 3-6 months of expenses to handle unexpected repairs or income disruptions.

🏡 Track market conditions: Understanding when to refinance or access home equity can provide financial flexibility.

🏡 Plan for renewal: Mortgage terms typically last 5 years. Start researching renewal options 4-6 months before your term expires to avoid being locked into unfavorable rates.

🏡 Consider future modifications: Whether adding a rental unit, renovating, or expanding, understanding zoning and financing options for improvements maximizes your property’s potential.

Special Considerations for Toronto First-Time Buyers

Navigating Toronto’s Unique Market Characteristics

Toronto’s real estate market differs significantly from other Canadian cities in several important ways that affect first-time buyers.

Condo prevalence: Toronto has the highest concentration of condominium housing in Canada. Understanding condo governance, fees, and regulations is essential for most first-time buyers in the city.

Transit-oriented development: Properties near TTC subway lines, GO stations, and planned transit expansions typically command premium prices but also offer stronger appreciation potential and lifestyle convenience.

Neighborhood diversity: Toronto’s neighborhoods vary dramatically in character, demographics, amenities, and price points. Researching micro-markets reveals opportunities that broader statistics might miss.

Regulatory environment: Toronto-specific regulations like the vacant home tax, short-term rental restrictions, and multiplex zoning reforms affect property values and usage options.

Self-Employed Buyers in Toronto’s Market

Self-employed individuals face unique challenges when securing mortgage approval, but the current buyer’s market provides additional time to prepare applications properly.

Traditional lenders typically require two years of tax returns and often use conservative income calculations that disadvantage self-employed borrowers. However, alternative documentation methods and specialized lenders can help.

For detailed guidance, see our resources on obtaining a mortgage when self-employed and the ultimate guide to securing a mortgage for self-employed Canadians.

Understanding Market Timing and Future Outlook

While the current buyer’s market provides advantages, understanding potential future scenarios helps inform your decision timing.

Factors that could shift market dynamics:

📈 Interest rate changes: Further Bank of Canada rate cuts could stimulate demand and reduce buyer leverage

📈 Immigration policy: Changes to immigration targets directly affect housing demand in Toronto

📈 Economic conditions: Employment growth, wage increases, and consumer confidence influence buyer activity

📈 Supply constraints: Despite current elevated inventory, Toronto’s longer-term supply shortage remains unresolved[2]

📈 Government interventions: New programs, tax changes, or regulatory reforms can quickly alter market conditions

Market analysts suggest the current buyer-favorable conditions may persist through the first half of 2026[2], but predicting exact timing is inherently uncertain. The best approach focuses on personal readiness rather than attempting to time the market perfectly.

If you’ve prepared financially, identified suitable properties, and found favorable terms, proceeding with your purchase makes sense regardless of short-term market fluctuations. Real estate remains a long-term investment, and trying to time the absolute bottom often results in missed opportunities.

Conclusion: Taking Action in Toronto’s 2026 Buyer’s Market

Buying your first home in Toronto’s 2026 buyer’s market represents a unique opportunity that may not persist indefinitely. With benchmark prices down 8% year-over-year to $936,100, inventory at 5.8 months of supply, and the sales-to-new-listings ratio at just 28.6%[3], first-time buyers hold negotiating power unseen in years.

However, opportunity alone doesn’t guarantee success. Strategic preparation, thorough due diligence, and expert guidance transform market conditions into actual results. By following the step-by-step process outlined in this guide—from financial preparation through closing—you position yourself to capitalize on current conditions while avoiding costly mistakes.

Your Next Steps

Ready to begin your home-buying journey? Take these immediate actions:

1. Assess your financial readiness: Calculate your budget, review your credit score, and gather documentation for mortgage pre-approval.

2. Connect with professionals: Engage a mortgage broker who understands current market conditions and can access competitive rates. A knowledgeable real estate agent familiar with your target neighborhoods is equally essential.

3. Research neighborhoods: Identify 2-3 areas that align with your lifestyle priorities and budget constraints. Study recent sold prices and market trends.

4. Get pre-approved: Secure mortgage pre-approval to establish your buying power and strengthen your negotiating position.

5. Start viewing properties: With clear criteria and pre-approval in hand, begin touring homes and conducting due diligence.

6. Make strategic offers: Leverage current market conditions to negotiate favorable terms, but remain realistic and prepared to compromise.

7. Complete your purchase: Work efficiently through conditions, finalize financing, and close your transaction with confidence.

The current buyer’s market won’t last forever. Economic conditions, interest rate changes, or policy interventions could shift dynamics quickly. The buyers who benefit most are those who prepare thoroughly and act decisively when opportunity aligns with readiness.

Toronto’s real estate market has proven resilient over decades despite periodic corrections. While short-term price declines create entry opportunities, the city’s strong fundamentals—economic diversity, immigration, limited land supply—support long-term value appreciation. For first-time buyers entering the market strategically in 2026, today’s purchase price may look remarkably favorable in retrospect.

Your journey to Toronto homeownership begins with a single step. Whether you’re just starting to save for a down payment or ready to make offers tomorrow, the resources and strategies outlined in this guide provide a roadmap for success. The 2026 buyer’s market has opened doors that were firmly closed in previous years—the question is whether you’ll walk through them.

For personalized guidance on navigating Toronto’s real estate market and securing optimal mortgage financing, connect with experienced professionals who understand both current conditions and your unique circumstances. Your first home awaits, and the market conditions to make it a reality are here now.

References

[1] Foch Trrebs 2026 Outlook Underestimates Growing Market Risks – https://realestatemagazine.ca/foch-trrebs-2026-outlook-underestimates-growing-market-risks/

[2] Watch – https://www.youtube.com/watch?v=aADKW0XSsvQ

[3] Toronto Housing Market – https://wowa.ca/toronto-housing-market

[5] Gta Sales Prices Trreb 2026 – https://storeys.com/gta-sales-prices-trreb-2026/

[6] Gta Home Sales And Prices Expected To Remain Stable In 2026 Amid Ongoing Affordability Pressures – https://trreb.ca/gta-home-sales-and-prices-expected-to-remain-stable-in-2026-amid-ongoing-affordability-pressures/