February 21, 2026

First-Time Buyers Guide to Etobicoke and North York Emerging Markets in February 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The Toronto real estate market has shifted dramatically, and for first-time buyers, February 2026 presents a rare window of opportunity. After years of relentless price growth and bidding wars, Etobicoke and North York have emerged as two of the GTA’s most promising markets for entry-level homeownership. With inventory surging by 44%, benchmark prices down nearly 8% year-over-year, and the sales-to-new-listings ratio sitting at just 28.6%, the balance of power has firmly shifted to buyers. This comprehensive First-Time Buyers Guide to Etobicoke and North York Emerging Markets in February 2026 will help you navigate these changing conditions and identify undervalued pockets where your homeownership dreams can become reality.

The data tells a compelling story: Etobicoke North’s benchmark home price stands at $688,200, while the broader Toronto GTA benchmark has dropped to $924,100. Condo apartments, once the darling of investors, have seen the sharpest corrections—down 8.55% year-over-year to $560,200. Meanwhile, detached and semi-detached properties in strategic neighborhoods offer stability and long-term value. For first-time buyers armed with the right information, these market conditions create unprecedented access to quality homes in established communities.

Key Takeaways

✅ Buyer’s market conditions prevail in February 2026, with 5.8 months of inventory and significantly reduced competition for entry-level properties

✅ Etobicoke offers accessible entry points with benchmark prices at $688,200 and undervalued pockets in neighborhoods like Etobicoke North and Long Branch

✅ Condo apartments present the best value, down 8.55% year-over-year to $560,200, ideal for first-time buyers seeking affordability

✅ Negotiation power has shifted to buyers, with conditional offers becoming standard and sellers more willing to accommodate inspection and financing clauses

✅ Strategic timing matters: TRREB forecasts mid-to-high single-digit price declines in the first half of 2026 before stabilization, creating optimal purchasing windows

Understanding the February 2026 Market Shift in Toronto’s Suburbs

The Toronto real estate landscape has undergone a fundamental transformation that directly benefits first-time buyers exploring Etobicoke and North York. After years of seller dominance, inventory levels have surged to their highest January levels in over a decade, creating breathing room for buyers who previously felt priced out of the market.

The Numbers Behind the Shift

The statistics paint a clear picture of market rebalancing. Toronto sales dropped 26% compared to the five-year January average, while new listings climbed 11% during the same period. This supply-demand imbalance has pushed the months of inventory to 5.8—well above the balanced market threshold of 3-4 months. For context, this represents a 71% increase in months of supply compared to previous years.

The Ontario average home price fell 7% year-over-year to $745,800 in January 2026, reflecting broader affordability pressures that have finally begun to ease. In the GTA specifically, the benchmark price of $924,100 represents a 3.84% month-over-month decline and a 3.75% year-over-year drop. These corrections, while modest, signal a market “catching its breath” rather than crashing—creating ideal conditions for thoughtful, strategic purchases.

What This Means for First-Time Buyers

The shift to a buyer’s market fundamentally changes the home-buying experience. Multiple offer situations have become rare on entry-level properties, and conditional offers—once rejected outright—are now standard practice. Buyers can include home inspection clauses, financing conditions, and reasonable closing timelines without fear of losing out to competing bids.

This environment also allows for genuine price negotiations. Sellers who once received asking price or above are now accepting offers 5-10% below list price, particularly on properties that have sat on the market for 30+ days. For first-time buyers with limited budgets, this negotiating power can translate to thousands of dollars in savings or the ability to afford a better property than previously possible.

Understanding how to save and buy your first home becomes even more critical in this market, as proper preparation can maximize your purchasing power during this favorable window.

First-Time Buyers Guide to Etobicoke Emerging Markets: Where to Focus in February 2026

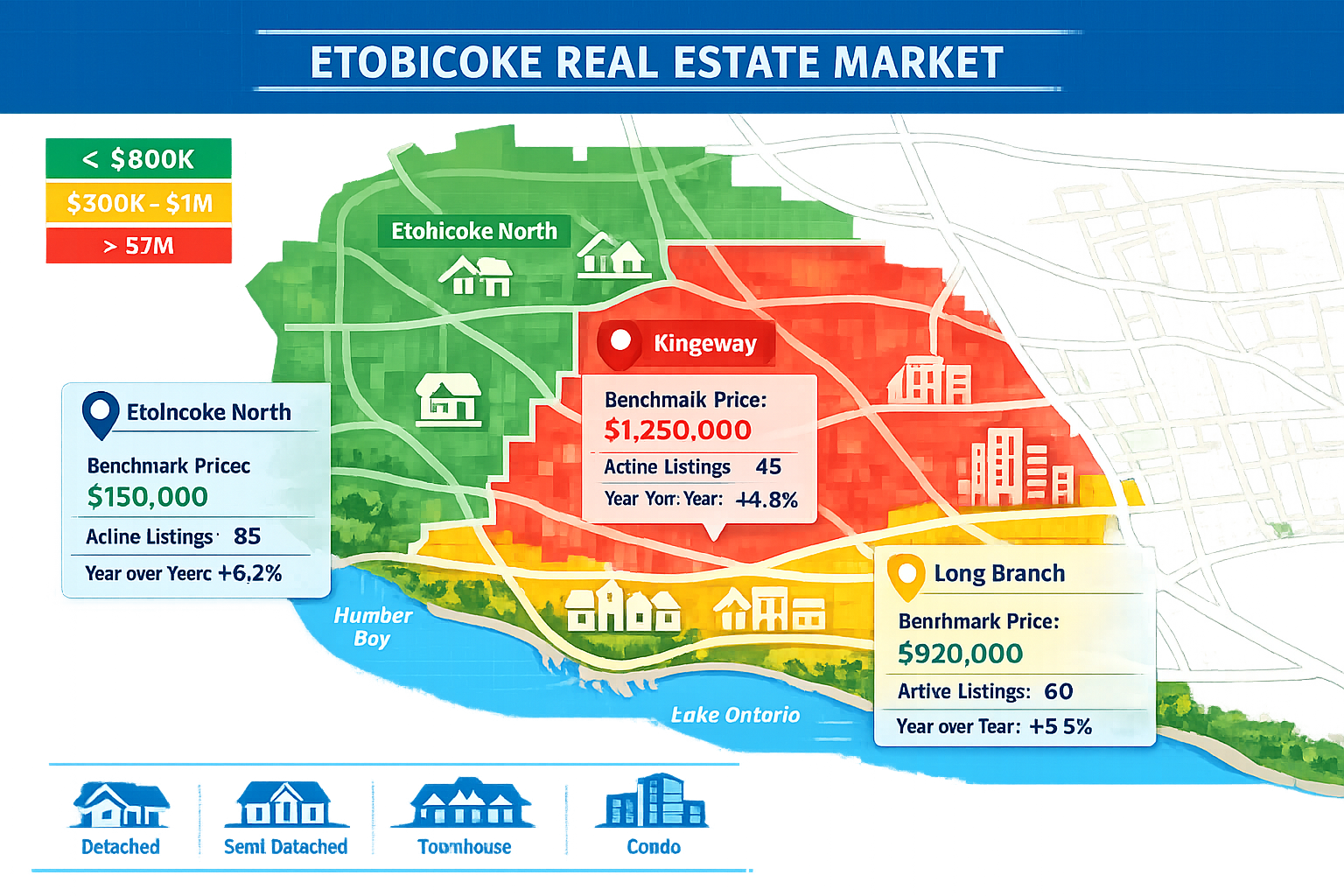

Etobicoke represents one of the GTA’s most diverse and accessible markets for first-time buyers in 2026. With its benchmark home price of $688,200—significantly below the GTA average—and a mix of property types spanning condos to detached homes, Etobicoke offers multiple entry points for buyers at different budget levels.

Etobicoke North: The Value Leader 🏘️

Etobicoke North stands out as the most accessible neighborhood for first-time buyers, with its benchmark price of $688,200 representing exceptional value compared to central Toronto locations. The area features a mix of older detached homes, semi-detached properties, and newer condo developments that cater to various buyer preferences.

The neighborhood benefits from excellent transit connectivity via the TTC subway and bus routes, making commutes to downtown Toronto manageable. Shopping amenities along Islington Avenue and Kipling Avenue provide everyday conveniences, while parks like Centennial Park offer green space for families. The demographic mix includes established families and young professionals, creating a balanced community atmosphere.

Property type breakdown in Etobicoke North:

| Property Type | Typical Price Range | Best For |

|---|---|---|

| Condo Apartments | $450,000 – $600,000 | Singles, young couples |

| Townhouses | $650,000 – $800,000 | Growing families |

| Semi-Detached | $750,000 – $950,000 | Families seeking space |

| Detached Homes | $900,000 – $1,200,000 | Long-term investment |

Long Branch: Waterfront Accessibility 🌊

Long Branch has emerged as a hidden gem for first-time buyers seeking waterfront proximity without premium pricing. Located in south Etobicoke along Lake Ontario, this neighborhood offers beach access, parks, and a village-like atmosphere while maintaining relative affordability.

Recent condo developments near the Long Branch GO Station have created inventory in the $500,000 – $700,000 range, perfect for first-time buyers who prioritize transit access and lifestyle amenities. The GO Train connection provides quick access to downtown Toronto and other GTA employment centers, making Long Branch particularly attractive for commuters.

Older semi-detached and detached homes in Long Branch’s residential pockets typically range from $800,000 to $1.1 million, positioning them as stretch goals for first-time buyers with higher incomes or larger down payments. The neighborhood’s lakefront trails, parks, and community events add lifestyle value that transcends pure real estate metrics.

The Kingsway: Premium Aspirations

While The Kingsway represents Etobicoke’s premium market with detached homes regularly exceeding $1.5 million, it’s worth understanding for first-time buyers planning long-term. The neighborhood’s tree-lined streets, prestigious schools, and proximity to the Humber River create enduring value that appreciates consistently.

For first-time buyers, The Kingsway’s condo apartments and townhouses offer more accessible entry points in the $600,000 – $850,000 range. These properties provide a foothold in a desirable neighborhood with potential for appreciation as buyers build equity and eventually trade up to larger homes.

Emerging Pockets Under $800K

Strategic first-time buyers should focus on these undervalued pockets in Etobicoke where inventory corrections have created opportunities:

- Markland Wood: Older condos and townhouses near the Etobicoke Creek ravine system

- Stonegate-Queensway: Mixed residential area with improving transit access

- Humber Heights: Established neighborhood with aging housing stock ripe for renovation

- Mimico: Transitioning area with new developments and GO Train access

These neighborhoods share common characteristics: good transit connectivity, established infrastructure, and property types under $800,000 that appeal to first-time buyers. The key is identifying properties that need cosmetic updates rather than structural repairs, allowing buyers to build equity through strategic renovations.

For buyers exploring these options, understanding mortgage refinancing strategies can help plan for future renovations and improvements.

First-Time Buyers Guide to North York Emerging Markets: Strategic Neighborhoods in February 2026

North York presents a different value proposition than Etobicoke, with its mix of high-rise condos, established single-family neighborhoods, and ongoing urban development. While specific February 2026 data for North York remains limited, broader GTA trends—including elevated inventory and stable pricing forecasts—apply directly to this diverse borough.

Condo Opportunities in North York Centre 🏢

North York Centre has experienced significant condo inventory growth, creating opportunities for first-time buyers in the $500,000 – $700,000 range. The neighborhood’s concentration of high-rise towers near Yonge Street and Sheppard Avenue provides excellent transit access via two subway lines, making it ideal for professionals working downtown or in the financial district.

The benchmark price for condo apartments across Toronto sits at $560,200—down 8.55% year-over-year—and North York Centre condos track closely with this average. Units in older buildings (1990s-2000s) offer the best value, particularly those requiring minor cosmetic updates that buyers can complete post-purchase.

Key advantages of North York Centre condos:

✨ Dual subway access (Yonge-University and Sheppard lines)

✨ Walkable amenities including Mel Lastman Square, libraries, and shopping

✨ Corporate employment nearby (office towers, corporate headquarters)

✨ Rental potential for future investment flexibility

✨ Lower maintenance compared to detached homes

Willowdale: Family-Friendly Value

Willowdale represents North York’s family-oriented market segment, with excellent schools, parks, and a strong sense of community. The neighborhood’s mix of detached homes, semi-detached properties, and townhouses creates options across different price points.

While detached homes in prime Willowdale locations exceed $1.5 million, semi-detached properties and townhouses in the $850,000 – $1.1 million range remain accessible for first-time buyers with dual incomes and substantial down payments. These properties offer more space than condos, making them suitable for growing families planning to stay long-term.

The neighborhood benefits from top-rated schools in both public and Catholic systems, adding family appeal that supports property values. Parks like Willowdale Park and Earl Bales Park provide recreational opportunities, while Yonge Street’s commercial corridor offers shopping and dining options.

Don Mills: Established Stability

Don Mills, one of Toronto’s first planned communities, offers mature neighborhoods with established infrastructure and good transit access. The area’s mix of property types includes original bungalows, renovated homes, and newer condo developments near the Don Valley Parkway.

First-time buyers should focus on townhouses and condos in the $650,000 – $850,000 range, particularly in complexes near Don Mills Station or along Sheppard Avenue. These properties provide solid value in a stable neighborhood with appreciation potential as the area continues to densify.

The Shops at Don Mills outdoor retail center adds lifestyle amenities, while the Don River ravine system provides green space and recreational trails. For buyers prioritizing work-life balance and community atmosphere, Don Mills delivers both.

Emerging Value Zones

Strategic first-time buyers exploring North York should investigate these emerging pockets where market corrections have created entry opportunities:

- York Mills: Older condos near York Mills Station in the $500,000 – $650,000 range

- Bathurst Manor: Established neighborhood with aging housing stock and renovation potential

- Lansing-Westgate: Mixed residential area with improving amenities and transit access

- Victoria Village: Transitioning neighborhood with townhouse opportunities under $900,000

These areas share characteristics that appeal to value-conscious first-time buyers: reasonable pricing, transit connectivity, and established community infrastructure. The key is identifying properties with good bones that need cosmetic rather than structural work, allowing buyers to build equity through strategic improvements.

Understanding current mortgage rate options becomes critical when evaluating these opportunities, as rate selection can significantly impact monthly carrying costs and long-term affordability.

Property Types and Pricing: Making Smart Choices in February 2026

Understanding the distinct characteristics and pricing dynamics of different property types helps first-time buyers make informed decisions aligned with their budgets, lifestyles, and long-term goals. The February 2026 market presents unique opportunities across all property categories, each with specific advantages for entry-level buyers.

Condo Apartments: Maximum Affordability 🏙️

Condo apartments represent the most accessible entry point for first-time buyers in both Etobicoke and North York, with benchmark prices at $560,200—down 8.55% year-over-year. This property type has experienced the sharpest corrections, creating exceptional value for buyers willing to accept shared amenities and condo fees.

Advantages of condo ownership:

- Lower entry price compared to freehold properties

- Minimal exterior maintenance (building handles repairs, landscaping)

- Amenities included (gym, party room, concierge in many buildings)

- Prime locations near transit and urban amenities

- Easier to rent if circumstances change

Considerations for condo buyers:

- Monthly maintenance fees typically $400-$700+ depending on building age and amenities

- Special assessments possible for major building repairs

- Less control over building decisions and renovations

- Potential rental restrictions in some buildings

- Resale competition in buildings with many units

For first-time buyers prioritizing location over space, condos in North York Centre or Etobicoke’s transit corridors offer unbeatable value. One-bedroom units in the $450,000 – $550,000 range and two-bedroom units in the $550,000 – $700,000 range provide comfortable living with manageable carrying costs.

Townhouses: The Middle Ground

Townhouses bridge the gap between condos and detached homes, offering more space and privacy than condos while maintaining relative affordability compared to detached properties. In Etobicoke and North York, townhouses typically range from $650,000 to $900,000 depending on location, age, and condition.

Freehold vs. condominium townhouses:

| Feature | Freehold Townhouse | Condo Townhouse |

|---|---|---|

| Ownership | Own land and structure | Own unit, share common elements |

| Maintenance | Full responsibility | Building handles exterior |

| Monthly Fees | None (or minimal HOA) | $200-$400+ condo fees |

| Control | Complete autonomy | Subject to condo rules |

| Price | Generally higher | Generally lower |

For first-time buyers with growing families or work-from-home needs, townhouses provide multiple bedrooms, dedicated outdoor space, and room for home offices. The property type offers a stepping stone toward eventual detached home ownership while building equity in a more affordable package.

Semi-Detached Homes: Space and Value

Semi-detached homes in Toronto benchmark at $1,142,700 as of January 2026, showing relative stability with only a 0.72% year-over-year decline. While this price point exceeds many first-time buyer budgets, strategic neighborhoods in Etobicoke and North York offer semis in the $850,000 – $1.1 million range.

Benefits of semi-detached ownership:

✅ More space than townhouses (typically 1,500-2,000 sq ft)

✅ Private yard for families with children or pets

✅ Renovation flexibility without condo board approval

✅ Strong appreciation potential in established neighborhoods

✅ Rental income possibilities (basement apartments where legal)

Semi-detached homes work best for dual-income first-time buyers with substantial down payments (20%+ to avoid CMHC insurance on properties over $1 million) and stable employment. The property type offers long-term value and flexibility that justifies the higher entry cost for buyers planning to stay 7-10+ years.

Detached Homes: Premium Investment

Detached homes in Toronto benchmark at $1,456,600 as of January 2026, placing them beyond most first-time buyer budgets. However, older detached homes in emerging Etobicoke and North York pockets occasionally appear in the $900,000 – $1.2 million range, particularly properties requiring significant renovations.

For first-time buyers with high household incomes, large down payments, or family financial assistance, detached homes represent the ultimate investment in space, privacy, and long-term appreciation. The property type offers maximum flexibility for renovations, additions, and lifestyle customization.

Realistic detached home scenarios for first-time buyers:

- Fixer-uppers in transitioning neighborhoods requiring $100,000+ in renovations

- Smaller lots or older homes in established areas at the lower end of market range

- Properties with legal rental income (basement apartments) to offset carrying costs

- Joint purchases with family members or friends to share ownership costs

Most first-time buyers should view detached homes as second or third purchases rather than initial entry points, focusing instead on condos, townhouses, or semis that build equity for eventual trading up.

Financial Preparation: Getting Mortgage-Ready in February 2026

The shift to a buyer’s market doesn’t eliminate the need for thorough financial preparation. In fact, proper mortgage readiness becomes even more critical when opportunities arise quickly and buyers need to act decisively. First-time buyers exploring Etobicoke and North York must understand current lending requirements, mortgage options, and strategic financial planning.

Understanding the 2026 Mortgage Landscape 💰

The mortgage environment in February 2026 reflects recent Bank of Canada rate adjustments and evolving lending standards. While rates have moderated from their 2023-2024 peaks, the mortgage stress test remains in effect, requiring buyers to qualify at either the contract rate plus 2% or 5.25%, whichever is higher.

Current mortgage rate environment (February 2026):

- 5-year fixed rates: 4.5% – 5.2% depending on lender and down payment

- Variable rates: 4.8% – 5.5% with potential for further adjustments

- High-ratio insured mortgages: Best rates available (down payment under 20%)

- Conventional mortgages: Slightly higher rates (down payment 20%+)

For first-time buyers, understanding how 2026 rate forecasts impact refinancing decisions helps inform whether to choose fixed or variable rate products based on personal risk tolerance and market outlook.

Down Payment Requirements and Strategies

Minimum down payment requirements in Canada follow a tiered structure:

- 5% minimum on the first $500,000 of purchase price

- 10% required on the portion between $500,000 and $1 million

- 20% required on any portion over $1 million (no CMHC insurance available)

Example down payment calculations:

| Purchase Price | Minimum Down Payment | CMHC Insurance Required |

|---|---|---|

| $500,000 | $25,000 (5%) | Yes |

| $700,000 | $45,000 (6.4%) | Yes |

| $900,000 | $65,000 (7.2%) | Yes |

| $1,100,000 | $220,000 (20%) | No |

For first-time buyers targeting properties under $800,000 in Etobicoke and North York, high-ratio insured mortgages (down payment under 20%) actually offer advantages: lower interest rates and access to the best mortgage products. The CMHC insurance premium (1.8% – 4% of mortgage amount) can be added to the mortgage principal, reducing upfront cash requirements.

Leveraging the First Home Savings Account (FHSA)

The First Home Savings Account (FHSA) represents a powerful tool for first-time buyers, offering tax-deductible contributions up to $8,000 annually (lifetime maximum $40,000) with tax-free withdrawals for qualifying home purchases.

FHSA advantages:

✨ Tax deduction on contributions (like RRSPs)

✨ Tax-free growth on investments within the account

✨ Tax-free withdrawals for first home purchase

✨ Stackable with HBP (Home Buyers’ Plan from RRSPs)

✨ No repayment required (unlike HBP)

Strategic first-time buyers should maximize FHSA contributions as early as possible, investing in balanced portfolios that grow funds while maintaining reasonable risk levels. Combined with RRSP Home Buyers’ Plan withdrawals (up to $35,000 per person), couples can accumulate substantial down payments through tax-advantaged accounts.

Credit Score Optimization

Minimum credit scores for mortgage approval vary by lender and mortgage type:

- 680+: Access to best rates from A-lenders (major banks)

- 650-679: Approval possible but with rate premiums

- 600-649: Limited options, higher rates, may require alternative lenders

- Below 600: Significant challenges, may need private lending

First-time buyers should check credit reports 6-12 months before house hunting, addressing any errors, paying down high-balance credit cards, and avoiding new credit applications. Simple strategies like keeping credit utilization below 30% and maintaining perfect payment history for 12+ months can boost scores significantly.

Pre-Approval: Your Competitive Advantage

In the February 2026 buyer’s market, mortgage pre-approval provides crucial advantages:

- Budget certainty before house hunting

- Rate holds (typically 90-120 days) protecting against increases

- Faster closing when offers are accepted

- Negotiating credibility with sellers

- Stress test clarity understanding maximum affordable price

Pre-approval involves submitting full documentation (income verification, employment letters, asset statements, credit authorization) to a lender who confirms maximum borrowing capacity. This process differs from pre-qualification (rough estimate based on stated information) and provides genuine commitment from the lender.

Working with experienced mortgage brokers who understand first-time buyer challenges ensures access to multiple lenders, competitive rates, and strategic advice tailored to individual circumstances.

Navigating the Buying Process: Strategies for February 2026 Success

The practical aspects of house hunting, making offers, and closing deals require strategic approaches tailored to current market conditions. First-time buyers exploring Etobicoke and North York in February 2026 benefit from understanding proven tactics that maximize value and minimize stress.

Strategic House Hunting 🔍

Effective house hunting begins with clear priorities and realistic expectations. First-time buyers should create a written list of must-haves (non-negotiable requirements) versus nice-to-haves (desirable but flexible features).

Must-have considerations:

- Location/commute: Maximum acceptable travel time to work

- Property type: Condo, townhouse, semi, or detached

- Bedrooms/bathrooms: Minimum required for household size

- Budget ceiling: Maximum affordable monthly payment

- Timeline: Desired closing date and flexibility

Nice-to-have features:

- Updated kitchens and bathrooms

- Finished basements

- Parking (especially for condos)

- Outdoor space size and privacy

- Specific amenities or finishes

In the current buyer’s market, patience pays dividends. Properties sitting on the market for 30+ days signal motivated sellers willing to negotiate. First-time buyers should resist urgency pressure and take time to view multiple properties, compare values, and make informed decisions.

Making Competitive Offers

The shift to a buyer’s market fundamentally changes offer strategy. Unlike the multiple-offer frenzies of 2021-2022, conditional offers with reasonable terms now succeed regularly in Etobicoke and North York.

Effective offer components:

- Price: Start 5-10% below asking for properties on market 30+ days

- Conditions: Include home inspection and financing clauses

- Deposit: Offer reasonable amount ($10,000-$25,000) held in trust

- Closing date: Accommodate seller preferences when possible

- Inclusions: Specify appliances, fixtures, and chattels included

Negotiation tactics for buyer’s markets:

- Request seller property disclosure statements before offering

- Identify property weaknesses (needed repairs, market time) to justify lower price

- Make clean offers on well-priced properties to avoid losing to competitors

- Use escalation clauses sparingly (less common in buyer’s markets)

- Be prepared to walk away if terms don’t meet your requirements

For properties requiring significant work, factor renovation costs into offer prices. A home listed at $750,000 needing $50,000 in updates justifies an offer around $680,000-$700,000, allowing budget for improvements while maintaining overall affordability.

Home Inspections: Non-Negotiable Protection

Professional home inspections represent the most important protection for first-time buyers. In the current market, sellers accept inspection conditions routinely, eliminating excuses for skipping this critical step.

What inspectors evaluate:

- Structural integrity: Foundation, framing, load-bearing walls

- Roof condition: Age, remaining life, leak evidence

- Mechanical systems: HVAC, plumbing, electrical

- Water intrusion: Basement moisture, drainage issues

- Building envelope: Windows, doors, insulation, ventilation

Quality inspections cost $400-$600 for condos and $500-$800 for houses, representing tiny investments relative to purchase prices. Inspectors provide detailed reports identifying immediate concerns, near-term maintenance needs, and long-term considerations.

Red flags requiring expert follow-up:

🚩 Foundation cracks or settlement issues

🚩 Roof leaks or structural damage

🚩 Electrical hazards (knob-and-tube wiring, overloaded panels)

🚩 Plumbing problems (polybutylene pipes, sewer backups)

🚩 Mold or moisture issues

When inspections reveal significant problems, buyers have three options: negotiate price reductions, request seller repairs, or walk away using the inspection condition. In buyer’s markets, sellers often agree to credits or repairs rather than risk losing deals.

Closing Preparation and Costs

Closing costs for first-time buyers typically total 1.5% – 4% of purchase price, covering various fees and expenses beyond the down payment.

Common closing costs:

| Expense | Typical Cost |

|---|---|

| Land Transfer Tax (Ontario) | 0.5% – 2% of price |

| Land Transfer Tax (Toronto) | Additional 0.5% – 2% |

| Legal Fees | $1,500 – $2,500 |

| Title Insurance | $250 – $400 |

| Home Inspection | $500 – $800 |

| Appraisal Fee | $300 – $500 |

| CMHC Insurance Premium | 1.8% – 4% of mortgage (if applicable) |

| Property Tax Adjustment | Varies by closing date |

| Utility Adjustments | Varies |

First-time buyer land transfer tax rebates in Ontario provide up to $4,000 relief on the provincial tax, significantly reducing closing costs for properties under $500,000. Toronto offers an additional rebate up to $4,475, creating combined savings up to $8,475 for eligible buyers.

Strategic buyers should budget conservatively for closing costs, maintaining emergency funds for unexpected expenses and immediate post-purchase needs (furniture, minor repairs, moving costs).

Long-Term Value: Building Wealth Through Strategic Property Selection

First-time home purchases represent more than shelter—they’re foundational wealth-building investments that compound over decades. Strategic property selection in Etobicoke and North York’s emerging markets positions buyers for long-term financial success through appreciation, equity accumulation, and lifestyle benefits.

Appreciation Potential in Emerging Markets 📈

Long-term real estate appreciation in Toronto has historically averaged 4-6% annually, though with significant year-to-year variation. The key for first-time buyers is identifying neighborhoods and property types positioned for above-average growth.

Factors driving appreciation:

- Transit infrastructure: New subway lines, GO stations, LRT routes

- Employment centers: Corporate headquarters, business districts, institutional employers

- Demographic trends: Population growth, immigration patterns, generational preferences

- Supply constraints: Limited development land, restrictive zoning, heritage protections

- Neighborhood improvements: Parks, schools, retail amenities, community investments

In Etobicoke, neighborhoods near future transit expansion (potential Eglinton West extension, improved GO service) offer appreciation upside. North York benefits from established subway infrastructure and ongoing densification around major intersections.

Property types with strong appreciation history:

- Well-located condos near subway stations (despite short-term corrections)

- Semi-detached homes in established family neighborhoods

- Townhouses in areas transitioning to higher density

- Detached homes on larger lots with development potential

First-time buyers should prioritize location over size, recognizing that smaller properties in superior locations typically appreciate faster than larger homes in less desirable areas.

Equity Building Strategies

Mortgage principal repayment represents forced savings that builds wealth automatically. On a $600,000 mortgage at 5% over 25 years, buyers pay approximately $3,500 monthly, with $1,000-$1,500 going toward principal in early years.

Accelerated equity building tactics:

✅ Increase payment frequency: Switch from monthly to bi-weekly accelerated payments

✅ Make lump sum payments: Use bonuses, tax refunds, or windfalls toward principal

✅ Increase payments annually: Add 5-10% to payments as income grows

✅ Refinance strategically: Lock in lower rates when available

✅ Avoid extending amortization: Keep 25-year schedule or reduce when possible

Over 5-7 years, disciplined first-time buyers can build $100,000-$150,000 in equity through combined principal repayment and modest appreciation. This equity becomes the down payment for trading up to larger properties, creating a wealth-building ladder.

Rental Income Opportunities

Legal basement apartments or accessory dwelling units provide rental income that offsets carrying costs and accelerates equity building. In Etobicoke and North York, legal rental units can generate $1,500-$2,500 monthly, significantly improving affordability.

Considerations for rental income properties:

- Zoning compliance: Verify legal status before purchasing

- Separate entrances: Essential for tenant privacy and property value

- Landlord responsibilities: Maintenance, tenant management, legal obligations

- Tax implications: Rental income reporting, expense deductions

- Mortgage qualification: Some lenders allow 50% of rental income toward qualification

First-time buyers purchasing properties with rental potential should understand mortgage qualification requirements and ensure proper legal compliance before advertising units.

Renovation Value-Add Strategies

Strategic renovations can accelerate appreciation and build equity faster than market forces alone. First-time buyers who purchase properties needing cosmetic updates can create instant equity through smart improvements.

High-ROI renovations for first-time buyers:

| Renovation | Typical Cost | Value Added | ROI |

|---|---|---|---|

| Kitchen refresh | $15,000 – $25,000 | $20,000 – $35,000 | 80% – 140% |

| Bathroom update | $8,000 – $15,000 | $10,000 – $18,000 | 90% – 120% |

| Basement finish | $25,000 – $40,000 | $30,000 – $50,000 | 100% – 125% |

| Flooring replacement | $5,000 – $10,000 | $6,000 – $12,000 | 100% – 120% |

| Paint and fixtures | $3,000 – $6,000 | $5,000 – $10,000 | 130% – 167% |

Avoid over-improving for the neighborhood—renovations should align with comparable properties rather than exceed local standards. A $100,000 kitchen in a $700,000 neighborhood rarely returns full value, while a $25,000 update delivers strong returns.

Tax Advantages of Homeownership

Principal residence exemption represents Canada’s most valuable tax benefit, allowing homeowners to sell primary residences completely tax-free regardless of appreciation. This contrasts sharply with investment properties, where capital gains face 50% inclusion rates.

Additional tax benefits:

- First-time buyer land transfer tax rebates (up to $8,475 combined in Toronto)

- Home office deductions for self-employed buyers (proportional to space used)

- Rental income deductions (mortgage interest, maintenance, utilities on rental portions)

- Energy efficiency rebates (federal and provincial programs for upgrades)

Over decades, the tax-free appreciation on principal residences compounds into substantial wealth. A $700,000 home appreciating at 4% annually reaches $1.3 million in 15 years—with the entire $600,000 gain tax-free.

Common Mistakes First-Time Buyers Must Avoid

Learning from others’ mistakes saves time, money, and stress. First-time buyers exploring Etobicoke and North York in February 2026 should avoid these common pitfalls that derail homeownership dreams or create financial hardship.

Mistake #1: Insufficient Financial Preparation ⚠️

Rushing into home purchases without adequate savings, credit optimization, or budget analysis leads to declined mortgage applications, settlement failures, or unsustainable carrying costs.

Prevention strategies:

- Save 12-18 months before serious house hunting

- Build emergency funds covering 3-6 months expenses beyond down payment

- Optimize credit scores to 700+ for best rates

- Get pre-approved before viewing properties

- Calculate true carrying costs including property tax, utilities, maintenance, insurance

Mistake #2: Emotional Decision-Making

Falling in love with properties before objective evaluation leads to overpaying, accepting unfavorable terms, or purchasing homes with hidden problems.

Prevention strategies:

- Create written criteria before house hunting

- View 15-20 properties to calibrate expectations

- Bring trusted advisors to viewings (parents, friends, agents)

- Sleep on decisions before making offers

- Walk away when terms don’t meet requirements

Mistake #3: Skipping Professional Guidance

DIY approaches to complex transactions risk costly mistakes, missed opportunities, or legal problems that professional guidance prevents.

Essential professionals:

- Mortgage brokers: Access to multiple lenders and best rates

- Real estate agents: Market knowledge, negotiation expertise, transaction management

- Real estate lawyers: Contract review, title protection, closing coordination

- Home inspectors: Property condition assessment, defect identification

- Insurance brokers: Appropriate coverage at competitive rates

The cost of professional services (typically 2-3% of purchase price total) pales compared to potential mistakes or missed savings from going alone.

Mistake #4: Ignoring Future Needs

Buying for today without considering 5-10 year life changes leads to outgrowing properties quickly, forcing expensive moves and transaction costs.

Future considerations:

- Family planning: Will you need more bedrooms?

- Career trajectory: Might job changes affect location needs?

- Aging parents: Could you need space for extended family?

- Work-from-home: Do you need dedicated office space?

- Lifestyle evolution: How might hobbies or interests change space needs?

Properties offering flexibility and growth potential justify premium prices compared to perfectly-fitted-today homes with no expansion options.

Mistake #5: Underestimating Ongoing Costs

Focusing solely on mortgage payments while ignoring property taxes, utilities, maintenance, insurance, and condo fees creates budget shortfalls and financial stress.

True monthly carrying costs:

- Mortgage payment: Principal and interest

- Property tax: Typically $250-$500+ monthly depending on assessment

- Utilities: $150-$300+ monthly (heat, electricity, water)

- Insurance: $100-$200+ monthly

- Maintenance: 1% of property value annually ($500-$800+ monthly for $700K home)

- Condo fees: $400-$700+ monthly for condos

- Special assessments: Variable for condos

A $700,000 property with a $600,000 mortgage might have $3,500 mortgage payment but $5,000+ total monthly costs when all expenses are included.

Expert Insights: What Industry Professionals Say About February 2026

Real estate professionals, mortgage brokers, and market analysts provide valuable perspectives on the current market dynamics affecting first-time buyers in Etobicoke and North York.

Market Outlook: Stability, Not Crisis 🎯

Industry experts emphasize that Toronto’s market is “catching its breath” rather than crashing. The corrections observed in early 2026 represent healthy rebalancing after years of unsustainable growth, creating opportunities rather than risks.

“The Toronto market isn’t collapsing—it’s normalizing. First-time buyers who’ve been priced out for years finally have breathing room to make thoughtful decisions without panic bidding. This is the healthiest market environment we’ve seen since 2019.”

TRREB forecasts project GTA average prices stable at $1M-$1.03M for full year 2026, with 60,000-70,000 sales expected. Mid-to-high single-digit price declines in the first half of 2026 should stabilize by summer, creating optimal purchasing windows in Q1-Q2.

Mortgage Strategy: Fixed vs. Variable Debate

Mortgage professionals note that the fixed versus variable decision depends heavily on individual risk tolerance and financial circumstances in February 2026.

Fixed rate advantages:

- Payment certainty for budgeting and planning

- Protection against potential rate increases

- Peace of mind for risk-averse buyers

- Qualification ease with stable payments

Variable rate advantages:

- Lower starting rates (typically 0.2-0.4% below fixed)

- Flexibility to benefit from future rate cuts

- Lower penalties for early payoff or refinancing

- Historical savings over 5-year terms

For first-time buyers with tight budgets, fixed rates provide security. Buyers with income flexibility and higher risk tolerance might benefit from variable rates if Bank of Canada continues cutting. Understanding how rate forecasts impact refinancing decisions helps inform this critical choice.

Neighborhood Selection: Location Still Paramount

Real estate agents emphasize that location fundamentals remain the primary driver of long-term value, even during market corrections.

Priority location factors:

- Transit access: Subway, GO Train, major bus routes

- Employment proximity: Reasonable commutes to job centers

- School quality: Top-rated schools for families

- Amenities: Shopping, dining, recreation, healthcare

- Safety: Low crime rates and community stability

Properties in superior locations maintain value during downturns and appreciate faster during recoveries. First-time buyers should prioritize location over size, recognizing that smaller homes in better neighborhoods outperform larger properties in less desirable areas.

Timing Considerations: Act Strategically

Market timing advice centers on strategic action rather than perfect timing. Experts note that waiting for absolute market bottoms often means missing opportunities as conditions improve quickly.

Optimal timing indicators:

✅ Personal readiness: Stable income, adequate savings, credit optimization

✅ Market conditions: Elevated inventory, reduced competition, negotiation power

✅ Rate environment: Favorable mortgage rates with reasonable holds

✅ Property availability: Suitable options in target neighborhoods and price ranges

✅ Life circumstances: Job security, relationship stability, location commitment

The February 2026 market checks most boxes for strategic first-time buyers with proper preparation. Waiting for further price declines risks missing the current window as inventory gets absorbed and competition increases.

Taking Action: Your Next Steps Toward Homeownership

The path from aspiring homeowner to successful first-time buyer requires systematic preparation and strategic execution. These actionable steps guide buyers through the process of purchasing in Etobicoke or North York’s emerging markets in February 2026.

Step 1: Financial Assessment and Preparation (Months 1-3) 📋

Immediate actions:

- Pull credit reports from Equifax and TransUnion, addressing any errors

- Calculate current savings and determine additional amounts needed for down payment and closing costs

- Create detailed budget tracking all income and expenses

- Open FHSA and maximize contributions for tax benefits

- Reduce high-interest debt to improve credit scores and debt ratios

- Gather financial documents (pay stubs, tax returns, bank statements, employment letters)

Target outcomes:

- Credit score 680+ (ideally 700+)

- Down payment saved (minimum 5% plus closing costs)

- Debt-to-income ratio under 40%

- Emergency fund covering 3-6 months expenses

- Complete financial documentation ready for mortgage application

Step 2: Mortgage Pre-Approval (Month 3-4)

Key actions:

- Research mortgage brokers specializing in first-time buyers

- Submit complete application with all supporting documentation

- Compare multiple lenders for best rates and terms

- Obtain rate hold (typically 90-120 days)

- Understand maximum borrowing capacity and comfortable payment levels

- Clarify mortgage features (prepayment options, portability, penalties)

Target outcomes:

- Formal pre-approval letter from lender

- Clear understanding of maximum affordable purchase price

- Rate hold protecting against increases during house hunting

- Confidence in monthly payment sustainability

Step 3: House Hunting and Offer Strategy (Months 4-6)

Strategic actions:

- Hire experienced real estate agent familiar with Etobicoke and North York

- Define clear criteria (must-haves vs. nice-to-haves)

- View 15-20 properties to calibrate expectations

- Research neighborhoods through visits at different times/days

- Attend open houses to understand market pricing

- Make strategic offers with appropriate conditions

- Negotiate effectively using market data and property weaknesses

Target outcomes:

- Accepted offer on suitable property

- Reasonable purchase price relative to market comparables

- Appropriate conditions protecting buyer interests

- Closing date aligned with financial readiness

Step 4: Due Diligence and Closing (Months 6-7)

Critical actions:

- Hire professional home inspector and attend inspection

- Review inspection report with agent and inspector

- Negotiate repairs or credits for significant defects

- Finalize mortgage with chosen lender

- Retain real estate lawyer for closing

- Arrange home insurance effective on closing date

- Conduct final walk-through before closing

- Prepare closing funds (down payment, closing costs)

Target outcomes:

- Satisfactory property condition or negotiated remedies

- Finalized mortgage with favorable terms

- Clear title and completed legal documentation

- Successful closing and key possession

Step 5: Post-Purchase Optimization (Ongoing)

Long-term actions:

- Build emergency fund for unexpected repairs

- Implement accelerated payment strategy to reduce amortization

- Plan strategic renovations with positive ROI

- Monitor mortgage renewal opportunities (typically 5 years)

- Track property value and neighborhood trends

- Consider rental income if property allows legal units

- Maintain property to preserve and enhance value

Target outcomes:

- Sustainable homeownership with manageable carrying costs

- Accelerated equity building through principal repayment

- Property value enhancement through strategic improvements

- Long-term wealth accumulation through appreciation

Conclusion: Seizing the February 2026 Opportunity

The First-Time Buyers Guide to Etobicoke and North York Emerging Markets in February 2026 reveals a rare convergence of favorable conditions for entry-level homeownership. With inventory up 44%, benchmark prices down 8% year-over-year, and negotiation power firmly in buyers’ hands, the current market presents opportunities unseen since before the pandemic.

Etobicoke’s benchmark price of $688,200 and accessible neighborhoods like Etobicoke North, Long Branch, and emerging pockets offer entry points under $800,000 across multiple property types. North York’s diverse market—from affordable condos in North York Centre to family-friendly options in Willowdale—provides alternatives for buyers with varying budgets and lifestyle preferences.

The condo apartment segment, down 8.55% year-over-year to $560,200, represents exceptional value for first-time buyers prioritizing location and affordability over space. Meanwhile, townhouses and semi-detached homes in strategic neighborhoods offer growth potential and family-friendly features for buyers with larger budgets.

Success in this market requires systematic preparation: optimizing credit scores, maximizing FHSA contributions, securing mortgage pre-approval, and working with experienced professionals who understand first-time buyer challenges. The shift to a buyer’s market means conditional offers, home inspections, and genuine price negotiations are not only possible but expected.

The window of opportunity won’t last indefinitely. TRREB forecasts predict stabilization by mid-2026, with inventory absorption and renewed buyer competition likely by summer. First-time buyers who act strategically in Q1-Q2 2026 position themselves to benefit from current corrections while building long-term wealth through property appreciation and equity accumulation.

Whether you’re targeting a $500,000 condo in North York Centre, an $700,000 townhouse in Etobicoke North, or a $900,000 semi-detached home in an emerging neighborhood, the February 2026 market offers pathways to homeownership that seemed impossible just two years ago.

Your next steps are clear:

- Assess your financial readiness and begin credit optimization today

- Maximize FHSA contributions to build tax-advantaged down payment funds

- Connect with mortgage professionals to secure pre-approval and rate holds

- Research target neighborhoods in Etobicoke and North York thoroughly

- Partner with experienced agents who understand first-time buyer needs

- Act decisively when suitable properties appear at reasonable prices

The dream of homeownership in Toronto’s established suburbs is within reach for prepared first-time buyers in February 2026. By following the strategies outlined in this comprehensive guide, you can navigate the market confidently, make informed decisions, and secure properties that serve as foundations for decades of financial success and lifestyle satisfaction.

The emerging markets of Etobicoke and North York await—are you ready to take the first step toward homeownership?