March 9, 2026

BoC Rate Hold at 2.25%: How Self-Employed Toronto Renewers Can Negotiate Below 3.99% Variable Rates in March 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

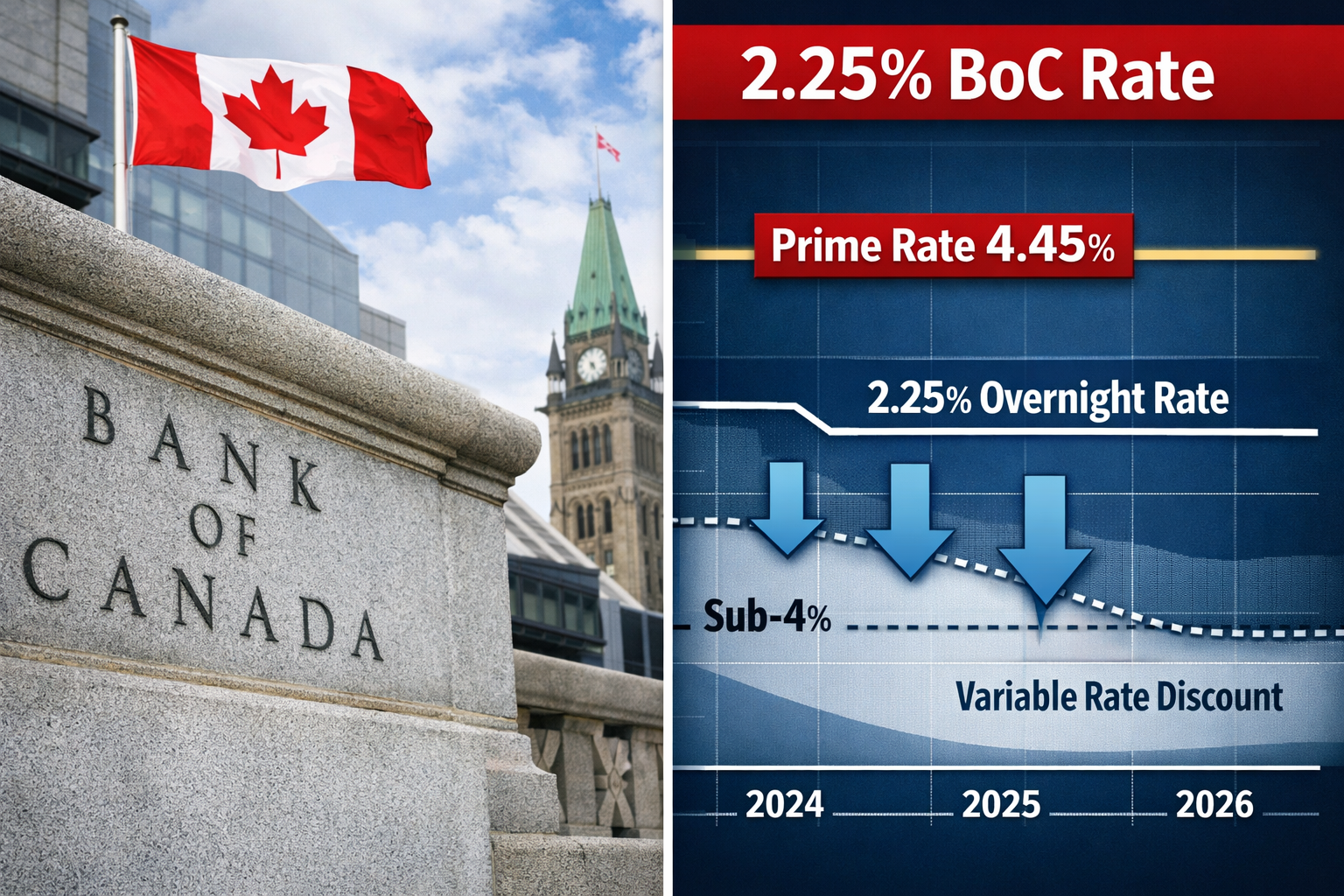

The Bank of Canada’s decision to hold its overnight rate steady at 2.25% presents a golden opportunity for self-employed mortgage holders in Toronto approaching renewal in March 2026. With the prime rate sitting at 4.45% and the next BoC announcement scheduled for March 18, 2026, savvy self-employed borrowers can leverage this stability to negotiate variable rates well below the 3.99% threshold—potentially saving thousands of dollars over their mortgage term.

Understanding how the BoC rate hold at 2.25% affects self-employed Toronto renewers seeking variable rates below 3.99% in March 2026 requires strategic preparation, strong documentation, and skilled negotiation. This comprehensive guide reveals exactly how to position yourself for the best possible rates in today’s stable interest rate environment.

Key Takeaways

✅ The Bank of Canada held its overnight rate at 2.25% on January 28, 2026, with market expectations showing minimal chance of rate changes through much of 2026[1][2]

✅ Prime rate stability at 4.45% enables self-employed borrowers to secure variable rates between 3.75% and 3.95% with proper documentation and negotiation

✅ Self-employed renewers face unique challenges but can overcome them by preparing comprehensive income verification and leveraging multiple lender competition

✅ March 2026 timing is strategic for renewals, occurring just before the March 18 BoC announcement, giving borrowers negotiating leverage in a stable rate environment

✅ Documentation strength directly impacts discount levels, with well-prepared self-employed applicants securing Prime minus 0.50% to Prime minus 0.70% discounts

Understanding the BoC Rate Hold at 2.25% and Its Impact on Variable Mortgage Rates

The Bank of Canada’s January 28, 2026 decision to maintain the overnight rate at 2.25% reflects a careful balancing act between controlling inflation and supporting economic growth. According to the official press release, the Bank is focused on “keeping inflation close to the 2% target while supporting economic adjustment to US trade restrictions”[2].

Current Economic Landscape in March 2026

The Canadian economic environment heading into March 2026 shows several key indicators that self-employed mortgage renewers should understand:

- CPI inflation: 2.4% in December 2025, slightly above the 2% target[2]

- Core inflation: Approximately 2.5%, showing persistent price pressures

- Economic growth: Projected at 1.1% for 2026 and 1.5% for 2027[2]

- Unemployment: 6.8%, remaining elevated with limited hiring plans[2]

- Prime rate: 4.45% (BoC rate of 2.25% plus standard 2.20% markup)

This stability creates a predictable environment for variable rate mortgages. Market expectations show negligible odds of near-term rate moves, with financial markets pricing the rate to remain at 2.25% through much of 2026[1].

How Variable Rates Are Calculated

Understanding the relationship between the BoC rate and your mortgage rate is crucial:

BoC Overnight Rate (2.25%) → Prime Rate (4.45%) → Your Variable Rate (Prime minus discount)

For self-employed borrowers with strong applications, typical discounts range from:

- Prime minus 0.50% = 3.95% variable rate

- Prime minus 0.60% = 3.85% variable rate

- Prime minus 0.70% = 3.75% variable rate

The goal for Toronto renewers in March 2026 is to secure that Prime minus 0.60% or better discount, bringing rates comfortably below the 3.99% threshold. Learn more about the differences in our comprehensive guide to fixed vs variable rates.

Why March 2026 Timing Matters

Renewing in March 2026—specifically before the March 18 BoC announcement—offers strategic advantages:

- Rate certainty: Lenders know rates will likely remain stable

- Competitive pressure: Spring market activity increases lender competition

- Negotiating leverage: You can lock in rates before any potential (though unlikely) changes

- Documentation time: Sufficient time to prepare comprehensive self-employed income proof

Self-Employed Mortgage Challenges and How to Overcome Them for Below 3.99% Rates

Self-employed borrowers face unique hurdles when negotiating mortgage rates, but understanding these challenges is the first step to overcoming them. The BoC rate hold at 2.25% creates opportunity, but self-employed Toronto renewers must still prove their creditworthiness to access variable rates below 3.99% in March 2026.

Common Self-Employed Mortgage Obstacles

Income Verification Complexity 📊

Unlike salaried employees with T4 slips, self-employed individuals must provide:

- Two years of complete Notice of Assessments (NOAs)

- Business financial statements

- Corporate tax returns (if incorporated)

- Proof of business continuity and stability

Income Write-Offs Impact 💰

Many self-employed professionals maximize tax deductions, which reduces reported income. This creates a paradox: excellent cash flow but lower qualifying income on paper.

Lender Risk Perception ⚠️

Financial institutions view self-employed income as less predictable, often requiring:

- Higher credit scores (typically 680+ minimum, 720+ for best rates)

- Larger down payments or equity positions

- Additional documentation beyond standard requirements

Strategies to Overcome Self-Employed Challenges

1. Prepare Comprehensive Documentation Early

Start gathering documents 90 days before renewal:

| Document Type | Purpose | Impact on Rate |

|---|---|---|

| 2 years NOAs | Income verification | Critical – Required |

| Business license | Legitimacy proof | Moderate |

| Bank statements (6 months) | Cash flow demonstration | High |

| Client contracts | Income stability | Moderate-High |

| CPA-prepared financials | Professionalism | High |

For detailed requirements, review our guide on documentation requirements for self-employed mortgage approval in Toronto.

2. Optimize Your Stated Income Approach

Consider these income calculation methods:

- Traditional stated income: Average of 2 years NOAs (most common)

- Gross-up method: Add back certain business expenses (available with some lenders)

- Alternative documentation: Bank statement programs for established businesses

3. Leverage Your Business Strengths

Highlight factors that reduce lender risk:

- ✅ Years in business (3+ years ideal)

- ✅ Industry stability (professional services, healthcare, tech)

- ✅ Diversified client base

- ✅ Recurring revenue streams

- ✅ Professional designations (CPA, lawyer, doctor)

Self-employed professionals in specific fields may have additional advantages. For instance, check out our specialized guide on self-employed mortgages for lawyers.

4. Strengthen Your Credit Profile

Target credit score benchmarks for rate tiers:

- 680-719: Qualify but limited discounts (Prime minus 0.30% to 0.40%)

- 720-759: Good discounts (Prime minus 0.50% to 0.60%)

- 760+: Best discounts (Prime minus 0.60% to 0.70%)

5. Maximize Your Equity Position

Loan-to-value (LTV) ratios significantly impact rates:

- Under 65% LTV: Best rates available

- 65-75% LTV: Standard rates

- 75-80% LTV: Slightly higher rates

- Over 80% LTV: Requires mortgage insurance, higher costs

For more strategies tailored to self-employed Canadians, explore our ultimate guide to securing a mortgage for self-employed Canadians.

Negotiation Strategies: How Self-Employed Toronto Renewers Can Secure Variable Rates Below 3.99%

With the BoC rate hold at 2.25% providing stability through March 2026, self-employed Toronto renewers have a strong foundation for negotiating variable rates below 3.99%. Success requires strategic timing, competitive positioning, and skilled negotiation tactics.

Step 1: Start the Process 120 Days Before Renewal

Timeline for March 2026 Renewal:

- December 2025: Begin document gathering and credit score optimization

- January 2026: Contact mortgage broker and submit applications to multiple lenders

- February 2026: Review offers and begin negotiation

- Early March 2026: Finalize terms and lock in rate before March 18 BoC announcement

Step 2: Leverage Multiple Lender Competition

Don’t rely on your current lender’s renewal offer. Self-employed borrowers should approach:

A-Lenders (Best Rates for Strong Applications)

- Major banks (TD, RBC, Scotiabank, BMO, CIBC)

- Credit unions (Meridian, DUCA, FirstOntario)

- Monoline lenders (MCAP, First National, RMG)

Current Market Rate Ranges (March 2026)

- Big Banks: Prime minus 0.40% to 0.55% (3.90% to 4.05%)

- Credit Unions: Prime minus 0.50% to 0.65% (3.80% to 3.95%)

- Monolines: Prime minus 0.55% to 0.70% (3.75% to 3.90%)

Pro Tip: Monoline lenders often offer the best rates for self-employed borrowers because they specialize in mortgages and have more flexible underwriting criteria.

Step 3: Use Strategic Negotiation Tactics

Tactic #1: Present Multiple Competing Offers

Once you have 2-3 written offers, use them as leverage:

- “Lender A offered Prime minus 0.60%. Can you match or beat this?”

- Show willingness to switch lenders if necessary

- Emphasize your strong application components

Tactic #2: Highlight Your Strengths

Create a one-page “borrower profile” showcasing:

- Credit score above 720

- Years of successful self-employment

- Equity position in property

- Clean payment history

- Professional industry/designation

Tactic #3: Bundle Products for Better Rates

Lenders often provide rate discounts for:

- Setting up automatic payments from their bank account

- Transferring investment accounts

- Taking bundled home/auto insurance

- Maintaining minimum account balances

Typical discount: 0.05% to 0.15% rate reduction

Tactic #4: Negotiate Beyond Rate

If a lender won’t budge on rate, negotiate:

- Prepayment privileges: 20% annual lump sum vs. standard 15%

- Portability options: Ability to transfer mortgage to new property

- Penalty calculations: Reduced penalties for early exit

- Cash back: $1,000-$3,000 for switching lenders

Step 4: Work With a Specialized Mortgage Broker

Self-employed borrowers benefit significantly from broker expertise:

Broker Advantages:

- Access to 30+ lenders vs. 1 bank

- Knowledge of which lenders favor self-employed applications

- Ability to position your application optimally

- No cost to you (lenders pay broker commissions)

- Expert negotiation on your behalf

For innovative approaches specifically designed for self-employed Canadians, see our article on innovative mortgage solutions for self-employed Canadians.

Step 5: Timing Your Rate Lock

With the March 18, 2026 BoC announcement approaching:

Best Practice: Lock your rate in early March (March 2-13) to:

- Secure current pricing before potential changes

- Complete underwriting before spring market rush

- Maintain negotiating leverage with “I need to decide this week” pressure

Rate Hold Periods: Most lenders offer 90-120 day rate holds, protecting you if rates rise while your renewal processes.

Real-World Rate Negotiation Example

Scenario: Self-employed consultant in Toronto, $650,000 mortgage, 55% LTV, 740 credit score

- Initial bank renewal offer: Prime minus 0.45% = 4.00% variable

- Broker shops to 5 lenders: Receives offers ranging from 3.80% to 3.95%

- Best offer: Credit union at Prime minus 0.65% = 3.80%

- Returns to bank: “I have 3.80% elsewhere, can you match?”

- Bank counters: Prime minus 0.60% = 3.85%

- Final decision: Takes credit union at 3.80%

Annual savings: $650,000 × 0.20% = $1,300 per year

To see current competitive rates available, check out current self-employed mortgage rates in Toronto.

Additional Considerations for Self-Employed Toronto Renewers in March 2026

Beyond securing a variable rate below 3.99%, self-employed Toronto renewers should consider several additional factors when navigating the BoC rate hold at 2.25% environment in March 2026.

Fixed vs. Variable Rate Decision

While this article focuses on variable rates, self-employed borrowers should evaluate both options:

Variable Rate Advantages (March 2026)

- ✅ Lower starting rate (3.75%-3.95% vs. 4.50%-4.80% fixed)

- ✅ BoC rate stability expected through 2026

- ✅ Lower penalties if you need to break mortgage

- ✅ Potential to benefit if rates decline

Fixed Rate Considerations

- ✅ Payment certainty for budgeting

- ✅ Protection if inflation persists and rates rise

- ✅ Peace of mind for risk-averse borrowers

Current Spread: Variable rates are approximately 0.65-0.85% lower than comparable fixed rates in March 2026.

For most self-employed borrowers with stable income, the variable rate advantage in a stable BoC environment makes it the optimal choice.

Tax Planning and Mortgage Strategies

Self-employed individuals can optimize their mortgage strategy through tax planning:

Income Timing Strategies

- Consider timing of income recognition for NOA purposes

- Balance tax deductions with mortgage qualification needs

- Plan 2-3 years ahead for future refinancing or purchases

Deductibility Considerations

- Investment property mortgages: Interest is tax-deductible

- Primary residence: Interest is not deductible

- Consider Smith Manoeuvre strategies for tax efficiency

Alternative Lender Options

If traditional A-lenders won’t offer rates below 3.99% due to income documentation challenges, consider:

B-Lenders

- Rates typically: 4.50%-6.50%

- More flexible income verification

- Bridge solution until income documentation improves

Alternative Documentation Programs

- Bank statement programs (use deposits instead of NOAs)

- Asset-based lending

- Stated income programs (limited availability)

While these options have higher rates, they can provide access to financing when traditional lenders decline.

Impact of Economic Factors on Future Renewals

Understanding broader economic trends helps with long-term planning:

US Trade Restrictions Impact The Bank of Canada specifically noted concerns about “economic adjustment to US trade restrictions”[2]. For self-employed Toronto renewers, this means:

- Potential slower economic growth affecting business income

- Importance of demonstrating business resilience

- Consideration of longer-term rate lock options

Inflation Monitoring With CPI at 2.4% and core inflation at 2.5%[2], there’s slight upward pressure. However, the BoC’s commitment to the 2% target suggests:

- Unlikely rate increases in near term

- Possible rate adjustments only if inflation accelerates significantly

- Variable rate remains attractive in this environment

Renewal vs. Refinancing Decisions

Some self-employed borrowers may benefit from refinancing rather than simple renewal:

Consider Refinancing If:

- You need to access equity for business investment

- You want to consolidate high-interest debt

- You’re purchasing additional investment property

- You want to restructure mortgage terms significantly

Stick With Renewal If:

- You’re satisfied with current mortgage structure

- You want to minimize costs and paperwork

- Your equity position hasn’t changed significantly

For insights on how renewals impact broader financial strategies, read about how 2026 mortgage renewals impact first-time home buyers refinancing in Toronto.

Common Mistakes to Avoid

Self-employed Toronto renewers should avoid these pitfalls:

❌ Accepting the first renewal offer without shopping around ❌ Waiting until the last minute to start the renewal process ❌ Failing to prepare documentation properly ❌ Not understanding penalty calculations on current mortgage ❌ Ignoring credit score until renewal time ❌ Assuming self-employed status disqualifies you from best rates

For a comprehensive list of common errors, review our guide on top 5 mistakes self-employed homebuyers make.

The Role of Professional Advice

Given the complexity of self-employed mortgage renewals, professional guidance is invaluable:

Mortgage Broker Benefits

- Specialization in self-employed applications

- Access to wholesale rates not available to public

- Experience positioning applications for approval

- Time savings (they do the shopping and negotiating)

Accountant Collaboration

- Strategic income planning for mortgage qualification

- Tax optimization strategies

- Documentation preparation and verification

- Multi-year financial planning

Financial Planner Input

- Overall debt management strategy

- Investment vs. mortgage paydown decisions

- Long-term wealth building considerations

- Risk assessment and insurance needs

Market Outlook Beyond March 2026

While the focus is on March 2026 renewals, understanding the longer-term outlook helps with term selection:

2026 Remainder Forecast

- BoC rate expected to remain at 2.25% through Q2 and Q3 2026

- Possible modest increase (0.25%) in Q4 2026 only if inflation persists

- Prime rate stability supporting variable rate attractiveness

Term Selection Strategy

- 3-year variable: Balanced approach, captures current low rates

- 5-year variable: Maximum rate discount, suitable if confident in stability

- Hybrid approach: Split mortgage between fixed and variable

Given current market conditions and the BoC rate hold at 2.25%, a 5-year variable rate below 3.99% represents excellent value for self-employed Toronto renewers in March 2026.

Conclusion

The Bank of Canada’s decision to hold its overnight rate at 2.25% through early 2026 creates an exceptional opportunity for self-employed Toronto mortgage renewers to secure variable rates below 3.99% in March 2026. With prime rate stability at 4.45% and market expectations showing minimal chance of near-term rate changes, the conditions are optimal for negotiating favorable terms.

Self-employed borrowers who prepare comprehensive documentation, leverage multiple lender competition, and employ strategic negotiation tactics can realistically achieve variable rates between 3.75% and 3.95%—representing Prime minus 0.50% to 0.70% discounts. These rates translate to significant savings over the mortgage term while maintaining the flexibility that variable mortgages provide.

Your Action Plan for March 2026 Renewal Success

Immediate Actions (Now – December 2025):

- ✅ Review your credit report and address any issues

- ✅ Gather 2 years of NOAs and business financial statements

- ✅ Calculate your current equity position (LTV ratio)

- ✅ Research current market rates and lender options

Short-Term Actions (January – February 2026): 5. ✅ Contact a mortgage broker specializing in self-employed applications 6. ✅ Submit applications to 3-5 lenders for competitive offers 7. ✅ Prepare your borrower profile highlighting strengths 8. ✅ Review and compare all offers received

Final Steps (Early March 2026): 9. ✅ Negotiate using competing offers as leverage 10. ✅ Lock in your rate before March 18 BoC announcement 11. ✅ Complete final underwriting and documentation 12. ✅ Confirm renewal terms in writing

The BoC rate hold at 2.25% environment won’t last forever. Self-employed Toronto renewers who act strategically in March 2026 can secure variable rates below 3.99%, positioning themselves for years of affordable mortgage payments while maintaining the flexibility to benefit from any future rate decreases.

Don’t settle for your lender’s initial renewal offer—with proper preparation and negotiation, rates below 3.99% are absolutely achievable for well-qualified self-employed borrowers in Toronto’s competitive mortgage market.

References

[1] Boc Interest Rate Decision – https://equalsmoney.com/economic-calendar/events/boc-interest-rate-decision

[2] Fad Press Release 2026 01 28 – https://www.bankofcanada.ca/2026/01/fad-press-release-2026-01-28/