March 10, 2026

The 26% Payment Shock Reality: Why Toronto Fixed-Rate Renewers Are Turning to Private Mortgages in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Imagine opening your mortgage renewal letter and seeing your monthly payment jump by $576 — every single month, forever. That is not a worst-case scenario. For thousands of Toronto homeowners renewing a fixed-rate mortgage in 2026, that is the reality. The 26% payment shock reality: why Toronto fixed-rate renewers are turning to private mortgages in 2026 is not a headline — it is a financial crisis unfolding quietly in living rooms across the GTA.

Key Takeaways 📌

- Fixed-rate borrowers renewing in 2026 face average payment increases of 15–26%, with some Toronto cases exceeding $576/month [1]

- Toronto mortgage arrears have quadrupled since 2022, hitting a projected 12-year high by December 2026 [2]

- 60% of Canadian mortgage holders renewing in 2025–2026 will see higher payments, according to Bank of Canada data [3]

- Private mortgages are emerging as a fast, flexible bridge solution for asset-rich borrowers who cannot meet traditional bank renewal criteria

- Relief is coming — TD Economics projects that by H2 2026, more renewals will see payment decreases than increases [10]

Understanding the 26% Payment Shock: The Numbers Behind the Crisis

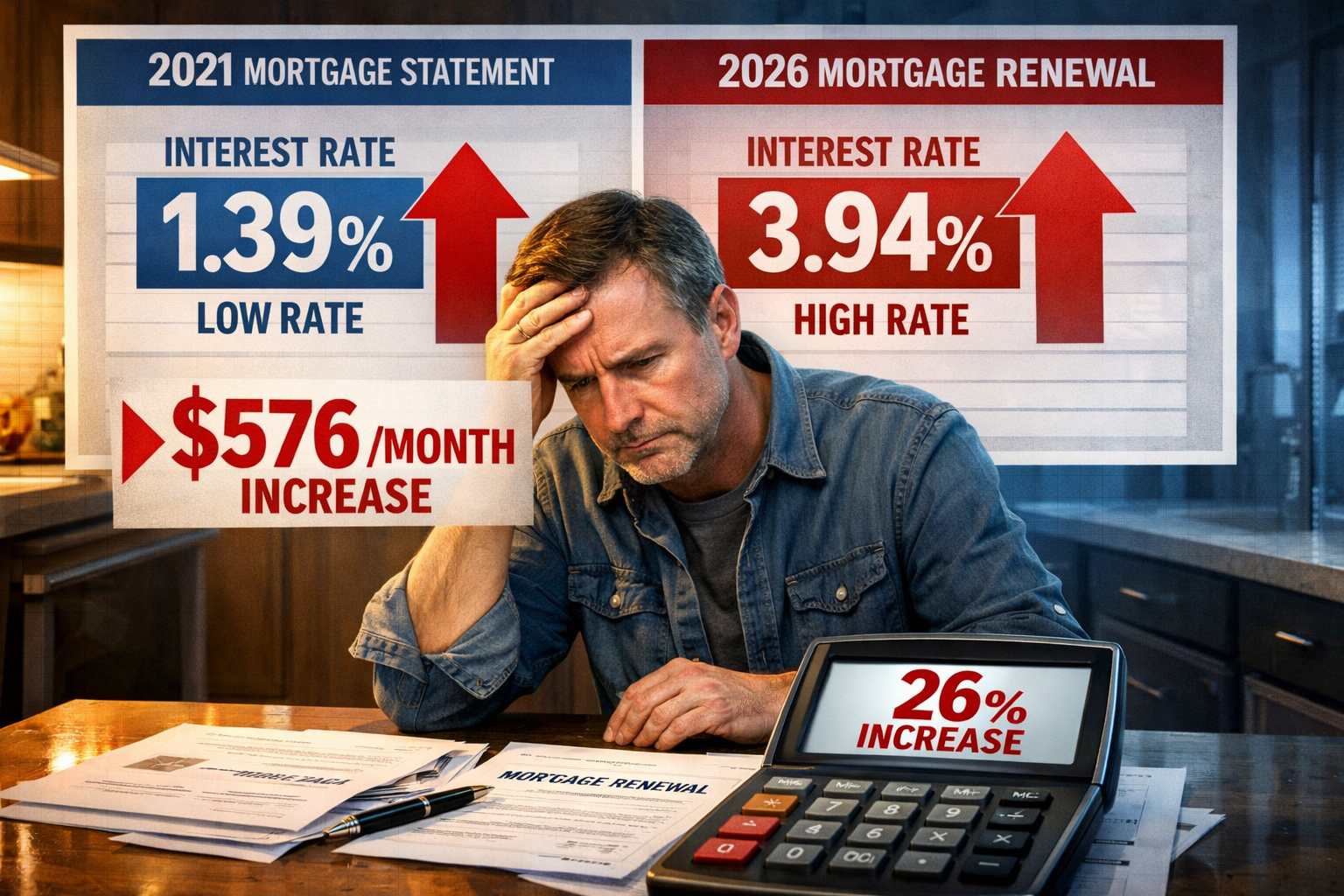

The term “payment shock” gets thrown around a lot. But mortgage specialist Simon Browning put a precise number on it in December 2025: a typical $2.1 million Toronto mortgage renewing from a pandemic-era rate of 1.39% to 3.94% generates a 26% payment increase — approximately $576 more per month, or nearly $7,000 per year [1].

That single calculation captures the 26% payment shock reality: why Toronto fixed-rate renewers are turning to private mortgages in 2026 in growing numbers.

The Scale of the Reset 💰

The numbers at a national level are staggering:

| Metric | Figure |

|---|---|

| Mortgages resetting 2026–2028 | $398 billion |

| Households affected | ~421,000 |

| Average monthly payment increase | $516/month |

| Aggregate new debt service cost (2026) | $2.6 billion |

| % of renewers facing higher payments | ~60% [3] |

For context, the Bank of Canada confirmed in its July 2025 analysis that approximately 60% of mortgage holders renewing in 2025–2026 will face higher payments, with fixed-rate borrowers bearing the steepest increases [3].

💬 “The mortgage delinquency story is not so much a national one but a much more localized and concentrated one.” — Tania Bourassa-Ochoa, CMHC Deputy Chief Economist [2]

Understanding fixed vs. variable rate dynamics is essential here. Fixed-rate borrowers locked in at historic lows during 2020–2021 are now facing the full brunt of the rate reset, while variable-rate holders absorbed increases gradually over time.

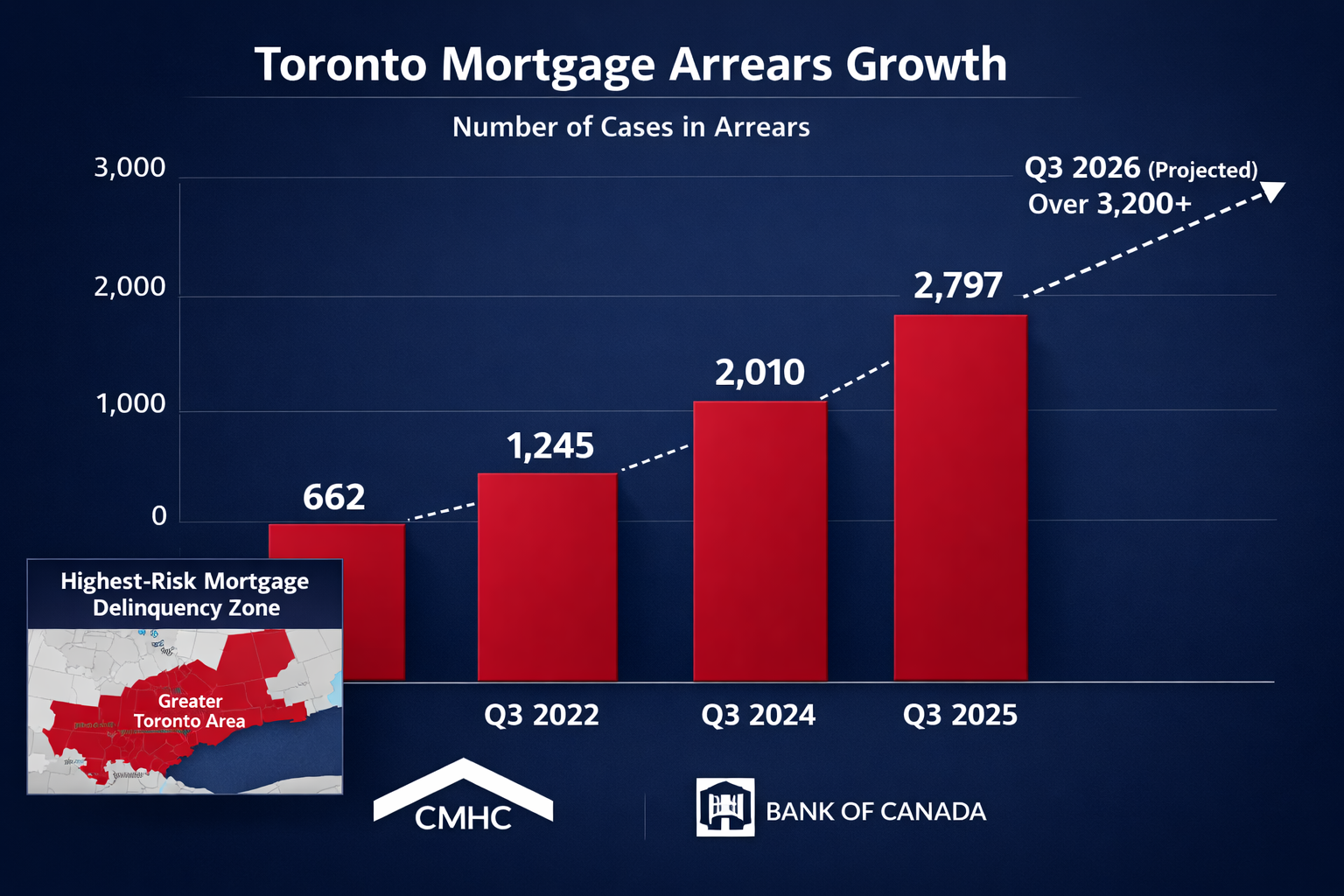

Toronto’s Arrears Crisis: Why the GTA Is Ground Zero

Toronto is not just facing a payment shock — it is facing a delinquency crisis that CMHC has called the “strongest and most persistent” in Canada [2].

The Arrears Numbers Tell the Story 📊

- Q3 2022: 662 Toronto consumers in mortgage arrears

- Q3 2025: 2,797 consumers in arrears — a 322% increase in three years

- December 2026 projection: 0.34% arrears rate — the highest since 2014

In February 2026, CMHC identified Toronto as the country’s most vulnerable region, citing three compounding factors:

- High household debt relative to income

- Declining home prices reducing equity buffers

- A weakening GTA labour market reducing income resilience [2]

This is precisely why mortgage delinquencies surging in 2025 has become a critical topic for Toronto homeowners. The stress test — introduced between 2016 and 2018 — has been credited with preventing even steeper arrears growth. Without it, regulatory analysis suggests delinquency increases would have been “much steeper” [2].

What’s Keeping Borrowers Afloat?

TD Economics’ chief economist Maria Solovieva identified a key factor in her March 2026 analysis: personal disposable income growth has exceeded pre-pandemic trends by a significant margin. This income cushion — not rate moderation — has been the “main mountaineer” preventing a full-scale mortgage crisis. Without it, debt service ratios would have peaked one percentage point higher [10].

The good news? TD projects that by H2 2026, the composition of renewals will shift toward relief, with more borrowers renewing into lower rates than higher ones as the pandemic-era cohort completes its reset [10].

Why Toronto Fixed-Rate Renewers Are Turning to Private Mortgages in 2026

This is the core of the 26% payment shock reality: why Toronto fixed-rate renewers are turning to private mortgages in 2026. When a bank says no — or offers terms that are simply unaffordable — private lenders are stepping in.

As of mid-February 2026, Ontario homeowners are “quietly turning to private mortgages” to navigate renewal gaps, with private lenders now positioned as the “first call” rather than a last resort for asset-rich households facing bank declines [5].

Who Is Turning to Private Mortgages? 🏠

Private mortgage borrowers in 2026 typically fall into one of these categories:

- Self-employed borrowers whose declared income doesn’t satisfy bank stress tests

- Homeowners with bruised credit due to missed payments during the rate shock period

- Equity-rich borrowers who need fast bridge financing before selling or refinancing

- Investors managing multiple properties with complex income structures

For self-employed Torontonians specifically, navigating the 2026 mortgage stress test has become a major challenge, making private options especially attractive.

Private vs. Bank Renewal: A Quick Comparison

| Feature | Bank Renewal | Private Mortgage |

|---|---|---|

| Approval speed | 2–4 weeks | 48–72 hours |

| Income verification | Strict T4/NOA required | Flexible / asset-based |

| Stress test required | Yes | No |

| Rate range | 4.5–6.5% | 7–12% |

| Term flexibility | 1–5 years | 6–24 months |

| Best for | Strong credit/income | Bridge, equity-rich, complex income |

The trade-off is real: private mortgage rates are higher. But for a borrower facing a bank decline or a payment they simply cannot absorb, a short-term private mortgage buys time to stabilize finances, improve credit, or wait for better market conditions.

To understand how private mortgages work in Ontario, it’s important to recognize them as a strategic bridge, not a permanent solution. Most borrowers use a 12–24 month private term to reset their financial position before returning to traditional lending.

The Strategic Case for Going Private 🔑

Consider this scenario:

A Toronto homeowner has a $900,000 mortgage renewing in 2026. Their small business income dropped during 2024–2025, and they cannot pass the bank’s stress test at the renewal rate. Their home has $400,000 in equity. A private lender approves them within 72 hours at 9.5% for 12 months — giving them time to rebuild income documentation and refinance with an A-lender.

This is exactly the type of situation where second mortgage options and private lending become powerful tools. The higher short-term cost is far less damaging than a forced sale or power of attorney situation.

For those worried about long-term affordability, exploring strategies for accelerated mortgage repayment after stabilizing can help rebuild equity faster once a borrower returns to traditional lending.

What Toronto Renewers Should Do Right Now

The 26% payment shock reality: why Toronto fixed-rate renewers are turning to private mortgages in 2026 does not have to be your story — if you act early.

Actionable Steps ✅

- Start renewal conversations 120–180 days early. Lenders can hold rates, and brokers need time to explore all options.

- Get a full mortgage review. Understand your current equity position, credit score, and income documentation before renewal.

- Compare all lender tiers. A-lenders (banks), B-lenders (trust companies), and private lenders all serve different borrower profiles.

- Consider a shorter term. With rates expected to ease further in late 2026, a 1–2 year term may be smarter than locking in for five years today.

- Explore refinancing. Refinancing at renewal can consolidate high-interest debt and reduce overall monthly obligations.

- Work with a licensed mortgage broker. Brokers have access to 30+ lenders and can match your profile to the right product — including private options — without impacting your credit score unnecessarily.

For first-time buyers or newer homeowners navigating this environment, the Toronto first-time home buyer’s guide to surviving the 2026 mortgage renewal shock offers a step-by-step framework.

Conclusion: The Shock Is Real — But So Are the Solutions

The 26% payment shock reality: why Toronto fixed-rate renewers are turning to private mortgages in 2026 reflects a genuine financial stress point — but it is not an unsolvable one. Mortgage arrears are rising, payments are jumping, and traditional bank renewals are failing a growing segment of GTA borrowers. But private mortgages, strategic refinancing, and proactive planning are giving thousands of homeowners a viable path forward.

The key insight: private mortgages in 2026 are not a sign of financial failure. For asset-rich, income-challenged borrowers, they are a smart, strategic bridge to better terms.

🏁 Your next step: Contact a licensed mortgage broker today to review your renewal options — ideally 4–6 months before your term expires. The earlier you act, the more options you have.

References

[1] 2026 Mortgage Renewal Shock What Toronto Ontario Homeowners Need To Know – https://www.cornellmortgages.ca/post/2026-mortgage-renewal-shock-what-toronto-ontario-homeowners-need-to-know

[2] Toronto Real Estate Boom 2026 Why The Gta Is Still Building And What It Means For Borrowers 758 – https://www.lendworth.ca/blog/lendworth-blog-1/toronto-real-estate-boom-2026-why-the-gta-is-still-building-and-what-it-means-for-borrowers-758

[3] Is Your Mortgage Set To Surge 60 Of Canadians Face Higher Payments By 2026 168 – https://www.lendworth.ca/blog/lendworth-blog-1/is-your-mortgage-set-to-surge-60-of-canadians-face-higher-payments-by-2026-168

[5] Why Investors Are Choosing Private Mortgages Over Condos In 2026 591 – https://www.lendworth.ca/blog/lendworth-blog-1/why-investors-are-choosing-private-mortgages-over-condos-in-2026-591

[10] Ca Mortgage Renewal Mission Possible – https://economics.td.com/ca-mortgage-renewal-mission-possible