March 15, 2026

Self-Employed Toronto Borrowers: Securing Sub-3.8% Fixed Rates in March 2026 Amid BoC 2.25% Hold

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage landscape in March 2026 presents a unique window of opportunity for self-employed Toronto borrowers. While major banks advertise fixed rates hovering between 4.21% and 4.66%, select mortgage brokers are offering qualified self-employed applicants access to sub-3.8% fixed rates—specifically in the 3.7% to 3.9% range. This opportunity emerges against the backdrop of the Bank of Canada maintaining its overnight rate at 2.25%, creating a favorable environment for those who can navigate the additional documentation requirements that come with self-employment income verification.

For entrepreneurs, contractors, and business owners in Toronto’s competitive real estate market, understanding how to access these preferential rates could translate into thousands of dollars in savings over a typical five-year term. With economic forecasts suggesting potential rate increases to 3.25% by 2027, the current moment represents a critical decision point.

Key Takeaways

- Sub-3.8% fixed rates (3.7%-3.9%) are currently available through select brokers for qualified self-employed Toronto borrowers in March 2026

- Bank statement programs allow self-employed applicants to qualify using 12-24 months of business banking activity rather than traditional tax returns

- The Bank of Canada’s 2.25% hold creates stability, but economists predict potential increases to 3.25% by 2027

- Self-employed borrowers need stronger documentation including two years of Notice of Assessments, business financial statements, and proof of business continuity

- Acting before mid-2026 could lock in rates before anticipated increases tied to inflation pressures and economic recovery

Understanding the Current Rate Environment for Self-Employed Toronto Borrowers

The March 2026 mortgage market reflects a complex interplay between central bank policy and lender-specific programs designed for non-traditional income earners. While the Bank of Canada maintains its benchmark rate at 2.25%—a position it has held steady to balance inflation control with economic growth—the mortgage rates available to consumers vary significantly based on employment status and documentation capacity.

The Gap Between Posted and Discounted Rates

Major Canadian banks currently post five-year fixed rates between 6.09% and 6.49%, but their discounted rates for well-qualified borrowers range from 4.21% to 4.66%. For self-employed borrowers specifically, mortgages for self-employed borrowers typically face additional scrutiny that can push rates higher—unless they work with specialized lenders and brokers.

The sub-3.8% rates available in March 2026 represent a significant discount even below standard discounted rates, accessible primarily through:

- Mortgage broker networks with access to alternative lender programs

- Credit unions offering competitive self-employed programs

- Monoline lenders specializing in non-traditional income verification

- Portfolio lenders with flexible underwriting criteria

Why the BoC 2.25% Hold Matters

The Bank of Canada’s decision to maintain rates at 2.25% through early 2026 provides a foundation of predictability. This “higher for longer” stance differs from the aggressive rate-cutting cycle some economists predicted in 2024-2025. For self-employed borrowers, this stability means:

✅ Predictable variable rate spreads for those comparing fixed versus variable options

✅ Lender confidence in underwriting longer-term fixed products

✅ Time to prepare documentation without rushing due to rapidly changing conditions

✅ Opportunity to shop rates across multiple lenders without fear of immediate increases

However, the current fixed vs. variable rates landscape suggests that locking in fixed rates now may provide protection against potential 2027 increases.

How Self-Employed Toronto Borrowers Can Access Sub-3.8% Fixed Rates

Securing rates below 3.8% as a self-employed borrower requires strategic preparation and understanding of alternative qualification pathways. Traditional mortgage qualification relies heavily on T4 employment income, but self-employed individuals must demonstrate income stability through different means.

Bank Statement Mortgage Programs

The most accessible route to sub-3.8% rates for self-employed Toronto borrowers involves bank statement programs. These specialized mortgage products allow qualification based on:

- 12-24 months of business bank statements showing consistent deposits

- Average monthly income calculations rather than taxable income

- Gross revenue analysis before business expense deductions

- Cash flow patterns demonstrating business stability

This approach particularly benefits self-employed borrowers who maximize business deductions to minimize taxable income—a common tax strategy that traditionally made mortgage qualification challenging.

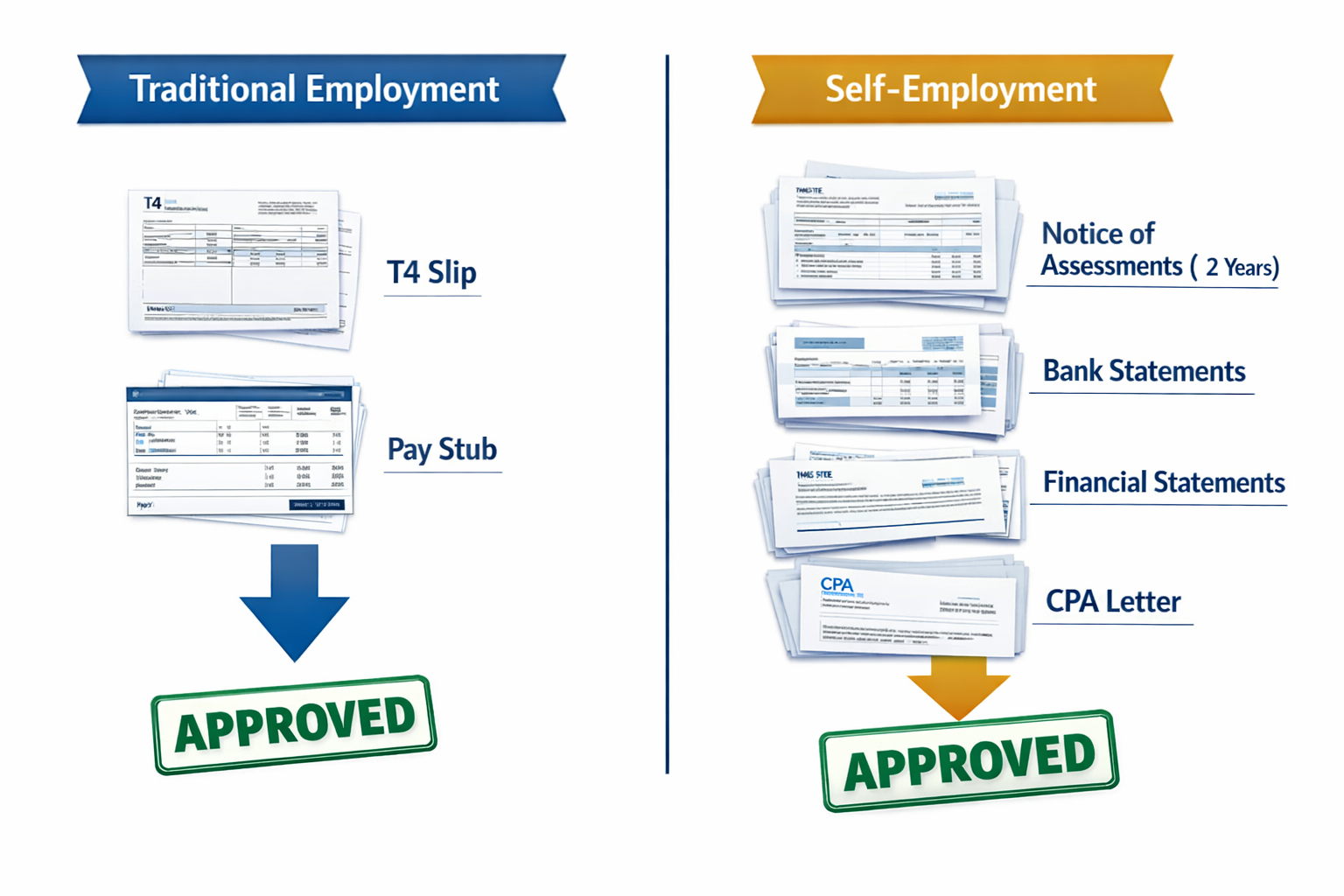

Essential Documentation Requirements

To access the most competitive rates, self-employed borrowers should prepare:

| Document Type | Requirement | Purpose |

|---|---|---|

| Notice of Assessments | 2 most recent years | Verify reported income to CRA |

| Business Financial Statements | 2 years | Demonstrate business profitability |

| Bank Statements | 12-24 months | Show cash flow and deposits |

| Business License/Registration | Current | Prove legitimate business operation |

| CPA Letter | Optional but valuable | Professional income verification |

| Credit Report | 680+ score preferred | Demonstrate creditworthiness |

For contractors specifically, our guide on self-employed mortgages for contractors provides additional qualification strategies.

Credit Score Thresholds

While borrowers with credit scores below 620 may still qualify for mortgages, accessing sub-3.8% rates typically requires:

- Minimum 680 credit score for most competitive programs

- 700+ score for optimal rate consideration

- No recent credit issues (collections, judgments, bankruptcies)

- Low credit utilization (below 30% of available limits)

Income Stability Demonstration

Lenders offering preferential rates to self-employed borrowers look for:

🔍 Minimum 2 years in the same business or industry

🔍 Consistent or growing revenue year-over-year

🔍 Diversified client base (not dependent on single contract)

🔍 Signed contracts for future work (particularly valuable for contractors)

🔍 Business continuity indicators (renewed licenses, ongoing expenses)

Strategic Timing: Why March 2026 Presents a Critical Window

The convergence of several factors makes March 2026 particularly advantageous for self-employed Toronto borrowers seeking favorable mortgage rates.

Economic Forecast and Rate Predictions

Current economic analysis suggests the Bank of Canada may begin gradually increasing rates in late 2026 or early 2027, with projections pointing toward a 3.25% overnight rate by the end of 2027. This anticipated increase stems from:

- Persistent inflation pressures in housing and services sectors

- Strong employment numbers suggesting economic resilience

- Global interest rate normalization following pandemic-era policies

- Government spending maintaining economic stimulus

For self-employed borrowers, this forecast creates urgency. A move from current sub-3.8% fixed rates to rates potentially approaching 4.5-5.0% by late 2027 would significantly impact affordability.

The Math Behind Rate Timing

Consider a $600,000 mortgage (typical for Toronto’s housing market):

At 3.8% (5-year fixed):

- Monthly payment: $3,087

- Total interest over 5 years: $109,428

At 4.8% (projected 2027 rate):

- Monthly payment: $3,428

- Total interest over 5 years: $128,252

Savings by locking in now: $341/month or $18,824 over the term

For self-employed borrowers who may face additional qualification challenges in a tightening credit environment, securing favorable rates now provides both financial savings and qualification certainty.

Seasonal Lender Competition

March 2026 also benefits from typical spring market dynamics where lenders compete aggressively for business ahead of the busy home-buying season. This competition creates:

- Promotional rate offerings from alternative lenders

- Flexible underwriting as lenders build their portfolios

- Broker incentives that can translate to better client rates

- New product launches targeting underserved markets like self-employed borrowers

Comparing Self-Employed Mortgage Options in Toronto’s 2026 Market

Self-employed Toronto borrowers have multiple pathways to mortgage approval, each with distinct rate implications and qualification requirements.

Traditional “A” Lenders

Major banks and traditional lenders offer the most stringent qualification but potentially competitive rates for borrowers with:

- Strong documented income (full tax returns showing sufficient income)

- Minimal business deductions (higher taxable income)

- Significant down payment (20%+ to avoid insurance premiums)

- Excellent credit (720+ scores)

Typical rates: 4.21% – 4.66% for self-employed with full documentation

Alternative “B” Lenders

B lender mortgage rates in Toronto provide middle-ground options for self-employed borrowers who don’t fit traditional criteria:

- More flexible income verification (bank statements accepted)

- Recent credit issues considered (case-by-case basis)

- Lower credit scores accepted (620-680 range)

- Higher debt service ratios permitted

Typical rates: 3.7% – 4.8% depending on risk profile

Private Lenders

For self-employed borrowers with unique circumstances, private lending offers:

- Minimal income verification (asset-based lending)

- Fast approval timelines (days rather than weeks)

- Credit challenges accepted (below 600 scores)

- Short-term bridge solutions (typically 1-2 years)

Typical rates: 6.99% – 11.99% (significantly higher but accessible)

Specialized Self-Employed Programs

The sub-3.8% rates available in March 2026 come primarily from specialized programs designed specifically for self-employed borrowers, featuring:

✨ Bank statement qualification (12-24 months)

✨ Industry-specific underwriting (understanding of business cycles)

✨ Relationship-based lending (considering full financial picture)

✨ Portfolio lending (lender keeps mortgage rather than selling)

For self-employed real estate investors specifically, DSCR loans offer additional qualification options based on rental property cash flow rather than personal income.

Common Mistakes Self-Employed Borrowers Make When Rate Shopping

Even with favorable market conditions, self-employed Toronto borrowers often sabotage their chances of securing optimal rates through preventable mistakes.

Mistake #1: Waiting Until After Tax Season

Many self-employed individuals complete their tax returns in April, then immediately seek mortgage approval. This timing creates problems:

- Maximized deductions reduce qualifying income

- Rush to find properties in competitive spring market

- Limited time to improve financial positioning

- Missed early-season promotional rates

Better approach: Review mortgage qualification requirements in January-February, adjust business expense strategies if home purchase is planned, and secure pre-approval before finalizing tax returns.

Mistake #2: Applying Only to Traditional Banks

The top 5 mistakes self-employed homebuyers make often include limiting applications to major banks. This approach overlooks:

- Alternative lenders with specialized self-employed programs

- Credit unions offering competitive rates with flexible criteria

- Mortgage brokers with access to 30+ lender options

- Monoline lenders focusing exclusively on mortgages

Mistake #3: Inconsistent Financial Documentation

Lenders scrutinize self-employed income carefully. Common documentation errors include:

❌ Mixing personal and business expenses in bank statements

❌ Irregular deposit patterns suggesting unstable income

❌ Large unexplained deposits triggering fraud concerns

❌ Gaps in business operation without clear explanation

❌ Declining revenue trends year-over-year

Mistake #4: Ignoring Credit Optimization

Self-employed borrowers sometimes neglect credit management, assuming income is the only factor. However:

- Every 20-point credit increase can improve rate by 0.1-0.2%

- Credit utilization above 50% raises red flags

- Multiple recent credit inquiries suggest financial stress

- Unreported credit issues can derail applications

Mistake #5: Not Understanding Rate vs. APR

The advertised rate isn’t always the true cost. Self-employed borrowers should compare:

- Annual Percentage Rate (APR) including all fees

- Lender fees (application, underwriting, administration)

- Broker fees (if applicable, though often lender-paid)

- Prepayment privileges and penalties

- Portability options for future flexibility

Preparing Your Self-Employment Documentation for Rate Optimization

Success in securing sub-3.8% rates requires meticulous preparation of financial documentation that tells a compelling story of income stability and business success.

The 90-Day Preparation Timeline

Months 3-4 Before Application:

- Review credit reports and address any issues

- Organize two years of tax returns and NOAs

- Compile business financial statements

- Gather business licenses and registrations

- Begin tracking monthly bank deposits

Months 1-2 Before Application:

- Obtain CPA letter verifying income

- Prepare written business overview

- Document future contracts/work pipeline

- Ensure business accounts show consistent activity

- Reduce personal credit utilization below 30%

Application Week:

- Update all documentation to most recent month

- Prepare explanation letters for any irregularities

- Gather proof of down payment source

- Compile references (business, personal, professional)

Working with a Mortgage Broker vs. Going Direct

For self-employed borrowers, working with an experienced mortgage broker offers distinct advantages:

Broker Benefits:

- Access to 30+ lenders including those specializing in self-employed mortgages

- Knowledge of which lenders accept bank statement programs

- Ability to position application optimally for each lender

- No cost to borrower (lenders pay broker commissions)

- Time savings through streamlined process

Direct Lender Approach:

- Relationship banking benefits if you’re an existing customer

- Simplified process with single institution

- Potential rate discounts for multiple products (banking, investments)

For most self-employed borrowers seeking sub-3.8% rates, the broker route provides access to the specialized programs offering these rates.

The Role of Down Payment Size in Rate Qualification

Down payment amount significantly impacts rate availability for self-employed Toronto borrowers, with distinct thresholds creating different opportunities.

The 20% Threshold

Putting down 20% or more offers several advantages:

🏆 Avoid mortgage insurance premiums (saving 2.8-4% of mortgage amount)

🏆 Access to best rates (insured vs. uninsured pricing)

🏆 More lender options (some won’t insure self-employed mortgages)

🏆 Stronger application (lower risk profile)

For a $750,000 Toronto property, this means having $150,000 down payment plus closing costs.

Alternative Down Payment Strategies

Self-employed borrowers with less than 20% down can still access competitive rates through:

- 5-19.99% down with mortgage insurance (CMHC, Sagen, Canada Guaranty)

- Gifted down payments from family (with proper documentation)

- RRSP Home Buyers’ Plan (up to $35,000 per person)

- Sale of previous property (portable equity)

For those investing in rental properties as a self-employed individual, different down payment rules apply, typically requiring 20% minimum.

Fixed vs. Variable: What Makes Sense for Self-Employed Borrowers in 2026?

The fixed versus variable rate decision takes on additional complexity for self-employed borrowers given income variability and qualification considerations.

Current Variable Rate Landscape

With the BoC holding at 2.25%, variable rates in March 2026 typically range from Prime – 0.5% to Prime + 0.5% (approximately 5.45% to 6.45% using a 5.95% prime rate). This makes fixed rates at 3.7-3.9% significantly more attractive.

Why Fixed Makes Sense for Self-Employed Borrowers Now

Several factors favor fixed rates for self-employed Toronto borrowers in March 2026:

- Payment certainty during business revenue fluctuations

- Protection against predicted rate increases to 3.25% BoC rate by 2027

- Qualification security (variable rate qualifying rate may increase)

- Budget stability for business planning

- Sub-3.8% opportunity unlikely to persist through 2026

When Variable Might Still Make Sense

Variable rates could benefit self-employed borrowers who:

- Expect significant income increases in coming years

- Plan to sell within 2-3 years (lower penalties)

- Have substantial cash reserves to handle payment increases

- Believe BoC will cut rather than raise rates (contrarian view)

The detailed analysis in our self-employed mortgage rates 2026 trends article provides additional perspective on this decision.

Navigating Stricter Lending Standards as a Self-Employed Borrower

The mortgage landscape in 2026 reflects stricter lending standards and higher scrutiny for self-employed clients, making preparation and proper positioning essential.

The Stress Test Impact

All mortgage applicants must qualify at the higher of:

- Contract rate + 2%, or

- 5.25% benchmark rate

For self-employed borrowers seeking a 3.8% rate, qualification happens at 5.8%, significantly reducing borrowing capacity. On a $600,000 mortgage:

- Actual payment at 3.8%: $3,087/month

- Qualification payment at 5.8%: $3,578/month

- Income required (28% GDS): $153,500 annually

This stress test particularly impacts self-employed borrowers whose income documentation may already be challenging.

Industry-Specific Considerations

Certain self-employed industries face additional scrutiny in 2026:

Higher Scrutiny:

- Hospitality and food services (pandemic recovery concerns)

- Retail businesses (e-commerce disruption)

- Freelance/gig economy workers (income stability questions)

- New businesses (less than 2 years operation)

More Favorable:

- Licensed professionals (doctors, lawyers, accountants)

- Skilled trades (construction, electrical, plumbing)

- Technology contractors (strong market demand)

- Established businesses (5+ years operation)

Taking Action: Steps to Secure Your Sub-3.8% Rate Before Mid-2026

With the window for optimal rates potentially closing as 2026 progresses, self-employed Toronto borrowers should act strategically.

Immediate Action Steps (This Week)

- Check your credit score and review reports for errors

- Gather financial documents (2 years tax returns, NOAs, bank statements)

- Calculate your budget using mortgage calculators

- Contact a mortgage broker specializing in self-employed mortgages

- Review business financials to understand qualifying income

30-Day Action Plan

- Week 1: Complete mortgage pre-qualification with broker

- Week 2: Address any documentation gaps or credit issues

- Week 3: Compare rate options across multiple lenders

- Week 4: Secure rate hold (typically 90-120 days)

Understanding Rate Holds

A rate hold guarantees your rate for 90-120 days while you:

- Search for properties

- Complete home inspections

- Finalize purchase agreements

- Complete final underwriting

Most lenders offer rate holds at no cost, and if rates drop during your hold period, many will honor the lower rate.

Questions to Ask Your Mortgage Broker

✅ What’s the lowest rate you can access for my profile?

✅ Which lenders specialize in self-employed mortgages?

✅ What documentation will optimize my application?

✅ How do bank statement programs compare to traditional qualification?

✅ What rate holds are available?

✅ What are the prepayment privileges and penalties?

✅ How does my business structure (sole proprietor, corporation) impact rates?

Conclusion

Self-employed Toronto borrowers face a remarkable opportunity in March 2026 to secure fixed mortgage rates below 3.8%—significantly better than the 4.21% to 4.66% range advertised by major banks. This window exists at the intersection of the Bank of Canada’s 2.25% rate hold, specialized lender programs accepting bank statement income verification, and competitive spring market dynamics.

However, this opportunity comes with an expiration date. Economic forecasts suggest potential rate increases to 3.25% by 2027, which would push mortgage rates substantially higher. For self-employed borrowers, the additional documentation requirements and qualification challenges make early preparation essential.

The path to securing these favorable rates requires:

- Comprehensive financial documentation spanning two years

- Strategic positioning of business income and expenses

- Strong credit profiles (ideally 680+ scores)

- Working with experienced brokers who access specialized lender programs

- Acting before mid-2026 to lock in rates before anticipated increases

For self-employed entrepreneurs, contractors, and business owners in Toronto’s competitive real estate market, the difference between a 3.8% and 4.8% rate on a typical $600,000 mortgage means $341 in monthly savings and nearly $19,000 over a five-year term. Beyond the financial savings, securing favorable financing now provides certainty in an uncertain economic environment.

The current mortgage rate environment won’t last indefinitely. Self-employed borrowers who organize their documentation, optimize their credit profiles, and work with knowledgeable mortgage professionals can capitalize on this unique market moment to secure financing that supports their homeownership goals while protecting their financial flexibility.

The time to act is now—before the window closes and rates return to higher levels that make Toronto homeownership even more challenging for self-employed Canadians.