March 16, 2026

Self-Employed Toronto Mortgages in a Stable 2.25% BoC Environment: Locking Sub-3.5% Variable Rates Before Mid-2026 Hikes

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The spring of 2026 presents a unique window of opportunity for self-employed professionals in Toronto’s competitive real estate market. With the Bank of Canada holding its benchmark rate steady at 2.25% and prime rates anchored at 4.45%, savvy borrowers are racing to secure variable mortgage rates before anticipated mid-year hikes disrupt the current stability. For self-employed Toronto mortgages in a stable 2.25% BoC environment, the challenge isn’t just finding favorable rates—it’s understanding how to leverage this brief period of predictability before market conditions shift. 🏠

The current mortgage landscape offers self-employed borrowers a strategic advantage that may not last. While traditional salaried employees navigate relatively straightforward approval processes, self-employed individuals must balance complex income verification requirements with timing considerations that could save—or cost—tens of thousands of dollars over a mortgage’s lifetime.

Key Takeaways

- Timing is critical: The Bank of Canada’s 2.25% rate is expected to hold through early 2026, but market forecasts predict increases by mid-year that could push variable rates significantly higher

- Variable rates currently range from 4.15-4.40% depending on loan-to-value ratios, with sub-3.5% targets requiring strategic positioning and strong self-employment documentation

- Toronto’s competitive lending market features over 340 mortgage brokers and 50+ private lenders, creating opportunities for self-employed borrowers to find specialized solutions[1]

- Documentation preparation is essential: Self-employed applicants need 2-3 years of tax returns, Notice of Assessments, and business financial statements ready for expedited approval

- Rate lock strategies should account for both current stability and projected volatility, with early 2026 presenting optimal conditions before anticipated mid-year Bank of Canada policy shifts

Understanding Self-Employed Toronto Mortgages in a Stable 2.25% BoC Environment

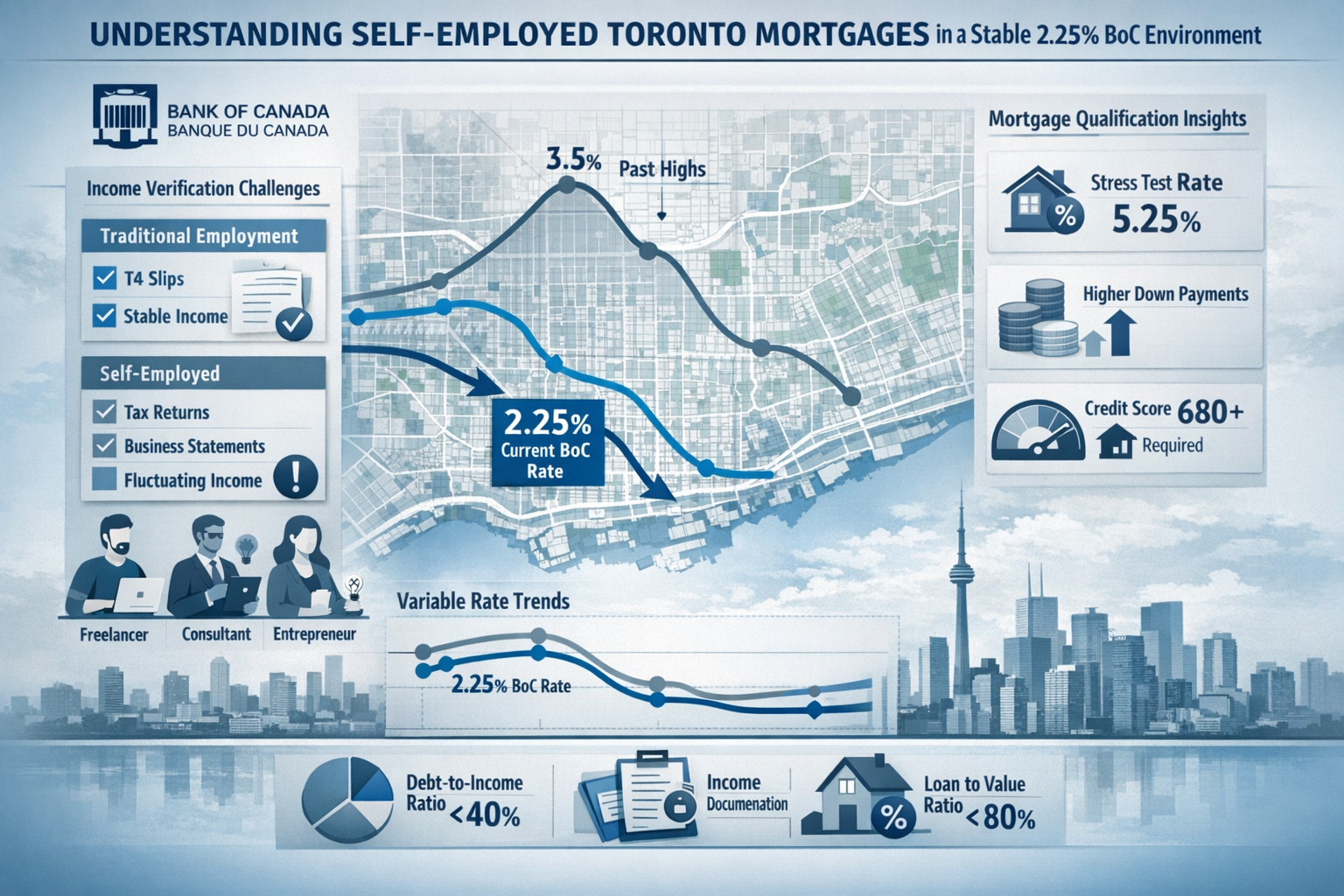

The relationship between Bank of Canada policy rates and mortgage accessibility for self-employed borrowers creates a complex but navigable landscape in 2026. With the BoC maintaining its overnight rate at 2.25%, prime rates have stabilized at 4.45%, establishing a foundation for mortgage rate calculations that directly impact variable mortgage products.

The Self-Employment Premium in Toronto’s Market

Self-employed professionals typically face additional scrutiny during mortgage applications compared to traditional employees. Lenders view self-employment income as inherently more variable, requiring enhanced documentation to prove consistent earning capacity. This perception often translates to:

- Higher interest rate premiums (0.10-0.50% above standard rates)

- Larger down payment requirements (minimum 10-20% versus 5% for salaried employees)

- More extensive income verification processes

- Stricter debt service ratio calculations

In Toronto’s expensive housing market, where the average home price continues to challenge affordability, these additional barriers can significantly impact purchasing power. However, the current stable rate environment provides a predictable backdrop for planning and positioning.

How the 2.25% BoC Rate Influences Variable Mortgages

Variable mortgage rates are directly tied to lenders’ prime rates, which move in lockstep with Bank of Canada policy decisions. The current 2.25% BoC rate has kept prime at 4.45%, creating a spread that determines variable mortgage pricing. For self-employed borrowers, understanding this relationship is crucial:

Rate Component Breakdown:

- Bank of Canada overnight rate: 2.25%

- Prime rate: 4.45% (prime = BoC rate + 2.20%)

- Variable mortgage rate: Prime + discount/premium

- Current variable rates: 4.15-4.40% (Prime – 0.30% to Prime – 0.05%)[1]

The “discount” from prime depends on several factors including credit score, down payment size, property type, and critically for self-employed applicants, income verification strength.

Toronto’s Competitive Lending Landscape

Toronto’s mortgage market offers distinct advantages for self-employed borrowers willing to shop strategically. With over 340 mortgage brokers operating in the city and more than 50 private lending institutions, competition drives innovation in self-employed mortgage solutions[1].

This competitive environment has produced:

| Lender Type | Typical Rate Range | Income Verification | Approval Timeline |

|---|---|---|---|

| Major Banks | Prime – 0.10% to Prime + 0.20% | Strict (2-3 years T1 Generals) | 3-5 weeks |

| Credit Unions | Prime – 0.25% to Prime + 0.10% | Moderate (2 years + business statements) | 2-4 weeks |

| Alternative Lenders | Prime + 0.50% to Prime + 1.50% | Flexible (stated income options) | 1-2 weeks |

| Private Lenders | 6.00% – 10.00%+ | Minimal (asset-based) | Days to 1 week |

For self-employed professionals seeking sub-3.5% variable rates, the path requires positioning in the top tier of qualification criteria—typically reserved for borrowers with exceptional credit (720+), substantial down payments (20%+), and ironclad income documentation.

Locking Sub-3.5% Variable Rates: Current Opportunities and Challenges

The pursuit of sub-3.5% variable rates in 2026 requires understanding both market realities and strategic positioning. Current market conditions show three-year variable rates ranging from 4.15-4.40% depending on loan-to-value ratios and insurance status[1]. Achieving rates below 3.5% demands exceptional qualification factors and often requires specialized lending relationships.

What Sub-3.5% Rates Actually Require

Securing variable mortgage rates under 3.5% in Toronto’s current environment isn’t impossible, but it requires meeting stringent criteria that challenge even well-positioned self-employed borrowers:

Essential Qualification Factors:

✅ Credit Excellence: Scores above 760 demonstrate exceptional financial management

✅ Substantial Equity: Down payments of 25-35% reduce lender risk significantly

✅ Proven Income Stability: Three years of increasing or stable self-employment income

✅ Low Debt Ratios: Total Debt Service (TDS) ratios under 35%

✅ Professional Designation: Certain professions (doctors, lawyers, accountants) receive preferential treatment

✅ Strong Banking Relationship: Existing clients with substantial assets often receive rate discounts

For self-employed lawyers and other professionals with established practices, these thresholds become more attainable. The key lies in presenting income documentation that eliminates lender uncertainty.

The Reality Check: Current Variable Rate Landscape

While the goal of sub-3.5% rates provides an aspirational target, understanding the actual current market helps set realistic expectations. As of early 2026, variable rates cluster around:

- Insured mortgages (less than 20% down): 4.15-4.25%

- Conventional mortgages (20%+ down): 4.20-4.40%

- High-ratio self-employed: 4.40-4.65%

- Alternative lender variable: 5.00-6.50%

The gap between current rates and the sub-3.5% target represents approximately 0.65-0.90%—a significant spread that translates to substantial monthly payment differences on Toronto’s high property values.

“In Toronto’s market, every 0.25% rate difference on a $750,000 mortgage equals approximately $115 per month or $1,380 annually. Over a five-year term, that’s nearly $7,000 in additional interest costs.”

Strategic Approaches to Rate Optimization

Self-employed borrowers pursuing the most competitive rates should consider these tactical approaches:

1. Rate Negotiation Leverage

Working with mortgage brokers who access multiple lenders creates competitive pressure. Toronto’s 340+ brokers compete aggressively for business, and self-employed Canadians can leverage this competition.

2. Income Presentation Strategies

Rather than simply submitting tax returns, work with accountants to prepare comprehensive income packages that include:

- Detailed business financial statements

- Contracts demonstrating future income

- Industry-specific income verification

- Professional corporation structures that optimize reported income

3. Hybrid Product Consideration

Some lenders offer variable rate products with features that effectively reduce the “true” rate through cashback incentives, fee waivers, or prepayment privileges that accelerate principal reduction.

4. Timing Optimization

With Bank of Canada rate stability expected through early 2026 but increases forecasted for mid-year, locking rates in Q1-Q2 2026 provides the best opportunity before market conditions deteriorate.

Before Mid-2026 Hikes: Timing Your Mortgage Strategy

The window for optimal mortgage positioning narrows as 2026 progresses. Market analysts and economists increasingly point toward mid-year rate increases as the Bank of Canada responds to evolving economic conditions. For self-employed Toronto borrowers, understanding this timeline transforms from academic interest to financial imperative.

Forecasting the Mid-2026 Rate Environment

While the Bank of Canada maintains its current 2.25% overnight rate through early 2026, several economic indicators suggest this stability won’t persist indefinitely:

Factors Pointing Toward Mid-2026 Increases:

📈 Inflation Persistence: Core inflation measures remaining above the BoC’s 2% target range

📈 Employment Strength: Robust job market data suggesting economic resilience

📈 Housing Market Heat: Toronto real estate showing renewed price appreciation

📈 Global Rate Pressures: International central bank policies influencing Canadian monetary decisions

📈 Consumer Spending: Strong retail and service sector performance indicating economic momentum

Market pricing currently suggests a 0.25-0.50% increase potential by Q3 2026, which would push prime rates from 4.45% to 4.70-4.95%. This seemingly modest shift would cascade through variable mortgage rates, potentially moving them from the current 4.15-4.40% range to 4.40-4.90% or higher.

The Cost of Waiting: A Financial Analysis

For self-employed borrowers considering whether to act now or wait, the mathematics provide clarity. Consider a typical Toronto mortgage scenario:

Scenario Comparison: Lock Now vs. Wait Until Post-Hike

| Factor | Lock Early 2026 | Wait Until Q3 2026 |

|---|---|---|

| Mortgage Amount | $750,000 | $750,000 |

| Variable Rate | 4.25% | 4.75% |

| Monthly Payment | $3,871 | $4,085 |

| Annual Cost | $46,452 | $49,020 |

| 5-Year Interest Paid | $147,890 | $159,635 |

| Difference | — | +$11,745 |

This $11,745 difference over five years represents the tangible cost of delaying action—and this assumes only a modest 0.50% increase. More aggressive rate hikes could amplify these costs significantly.

Optimal Action Timeline for Self-Employed Borrowers

Creating a strategic timeline maximizes the probability of securing favorable rates before market conditions shift:

Q1 2026 (January-March): Preparation Phase ⏰

- Gather 2-3 years of complete tax documentation

- Obtain updated credit reports and address any issues

- Consult with mortgage brokers to understand current qualification criteria

- Begin property search with pre-approval in hand

Q2 2026 (April-June): Execution Phase 🎯

- Finalize mortgage applications with multiple lenders

- Lock in rate holds (typically 90-120 days)

- Complete property purchases before anticipated mid-year rate announcements

- Consider trigger rate implications for variable products

Q3 2026 (July-September): Post-Hike Environment ⚠️

- If rates increase as forecasted, borrowers who locked earlier benefit immediately

- New applicants face higher qualification thresholds and rates

- Alternative lending options become more expensive

Q4 2026 (October-December): Reassessment 🔄

- Evaluate whether locked rates remain competitive

- Consider conversion to fixed if variable rates become unfavorable

- Plan for potential further increases in 2027

Documentation and Qualification: Positioning for Success

The foundation of any successful self-employed mortgage application rests on comprehensive, well-organized documentation that eliminates lender uncertainty. In Toronto’s competitive market, where self-employed borrowers face heightened scrutiny, documentation quality often determines approval outcomes and rate tiers.

Essential Documentation Package

Lenders evaluate self-employed income through multiple documentation layers, each serving to verify earning capacity and stability:

Core Documentation Requirements:

📄 Personal Tax Returns (T1 Generals)

- Minimum 2 years required (3 years preferred)

- Must show consistent or increasing income

- Line 150 (total income) receives primary focus

- Self-employed income from Line 135-143 undergoes detailed analysis

📄 Notice of Assessments (NOAs)

- CRA-issued confirmation of filed returns

- Verifies tax compliance and payment history

- Recent NOAs (within 90 days) carry more weight

📄 Business Financial Statements

- Profit and Loss statements for past 2-3 years

- Balance sheets showing business assets and liabilities

- Prepared by accountant (reviewed or audited statements preferred)

- Year-to-date statements for current year

📄 Business Registration Documents

- Articles of incorporation for incorporated businesses

- Business licenses and professional designations

- Partnership agreements if applicable

- GST/HST registration confirmation

📄 Additional Income Verification

- Contracts demonstrating ongoing work commitments

- Client letters confirming continued business relationships

- Bank statements showing consistent deposits

- Investment income documentation

Income Calculation Methods for Self-Employed Applicants

Lenders employ different methodologies to calculate qualifying income for self-employed borrowers, and understanding these approaches helps optimize presentation:

Traditional Two-Year Average Method

Most conservative approach: Lenders average Line 150 income over two years, often adding back certain deductions like CCA (Capital Cost Allowance) and home office expenses. This method disadvantages borrowers whose income has grown recently.

Three-Year Trend Analysis

For borrowers with increasing income trajectories, some lenders consider three-year trends and weight recent years more heavily, providing better qualification outcomes.

Gross Income Method

Alternative lenders may consider gross business revenue before expenses, particularly for established businesses with consistent revenue streams. This approach typically comes with higher rates but improves qualification amounts.

Stated Income Programs

For borrowers with complex income structures or significant write-offs, some lenders offer stated income programs requiring larger down payments (typically 35%+) but minimal income documentation. Rates for these programs sit 1.00-2.00% above standard rates.

Credit Optimization Strategies

Beyond income documentation, credit profiles significantly impact rate eligibility. Self-employed borrowers should focus on:

Credit Score Enhancement:

- Maintain credit utilization below 30% on all revolving credit

- Ensure all payments report on-time for minimum 12 months before application

- Avoid new credit applications in the 6 months preceding mortgage application

- Consider credit score below 620 as a red flag requiring remediation

Debt Service Ratio Management:

- Gross Debt Service (GDS): Housing costs should remain under 32% of gross income

- Total Debt Service (TDS): All debt payments should stay under 40% of gross income

- Pay down consumer debt before application to improve ratios

- Consider debt consolidation strategies if ratios exceed thresholds

Working with Specialized Mortgage Professionals

The complexity of self-employed mortgage applications makes professional guidance particularly valuable. Toronto’s extensive broker network includes specialists who focus exclusively on self-employed and freelance professionals:

Benefits of Specialist Mortgage Brokers:

✅ Lender Knowledge: Understanding which lenders offer favorable self-employed programs

✅ Documentation Guidance: Helping structure income presentation for optimal qualification

✅ Alternative Solutions: Access to non-traditional lenders when mainstream options fall short

✅ Rate Shopping: Comparing offers across Toronto’s 340+ broker network and 50+ private lenders[1]

✅ Application Strategy: Timing submissions and managing multiple applications simultaneously

For IT consultants, freelancers, and other self-employed professionals, these specialists understand industry-specific income patterns and can position applications accordingly.

Common Pitfalls to Avoid

Self-employed mortgage applications fail or receive unfavorable rates due to preventable errors:

❌ Aggressive Tax Write-Offs: While tax minimization makes sense for CRA purposes, excessive deductions reduce qualifying income for mortgage purposes. Strategic planning balances tax efficiency with mortgage qualification.

❌ Inconsistent Income Reporting: Discrepancies between tax returns, bank deposits, and stated income raise red flags and can result in application denial.

❌ Inadequate Down Payment: Self-employed borrowers often need 15-20% minimum down payment for optimal rates, yet many attempt qualification with 10% or less.

❌ Poor Timing: Applying immediately after business structure changes (incorporation, partnership changes) or during income transition periods complicates qualification.

❌ Single Lender Approach: Assuming one’s primary bank offers the best rates without shopping alternatives often results in paying 0.25-0.50% premium unnecessarily.

Strategic Alternatives and Contingency Planning

Even with optimal preparation, some self-employed borrowers face qualification challenges or rate outcomes that don’t meet the sub-3.5% target. Understanding alternative pathways and contingency strategies ensures access to Toronto real estate regardless of traditional lending obstacles.

Alternative Lending Solutions for Self-Employed Borrowers

When mainstream lenders can’t accommodate self-employed income structures or credit profiles, Toronto’s robust alternative lending market provides options:

B-Lenders (Alternative “A” Lenders)

These institutions specialize in borrowers who don’t fit traditional criteria but still represent reasonable risk:

- Rate range: Prime + 0.50% to Prime + 2.00% (currently 4.95-6.45%)

- More flexible income verification (may accept 1-2 years documentation)

- Credit scores as low as 600 accepted

- Higher fees (typically 1-2% of mortgage amount)

Private Lenders

For borrowers requiring maximum flexibility, private mortgage lenders focus primarily on property equity rather than income verification:

- Rate range: 6.00-12.00% depending on LTV and risk factors

- Minimal income documentation required

- Short-term solutions (typically 1-2 years)

- Higher fees (2-5% of mortgage amount)

- Useful as bridge financing while improving qualification profile

Credit Union Solutions

Ontario credit unions often provide middle-ground options with more flexible underwriting than major banks but better rates than private lenders:

- Relationship-based lending decisions

- Consideration of full financial picture beyond standard ratios

- Competitive rates for members with strong overall profiles

- Local decision-making authority

Fixed vs. Variable Rate Considerations

While this article focuses on variable rate opportunities, the anticipated mid-2026 rate increases merit consideration of fixed-rate alternatives:

Current Fixed Rate Environment:

Five-year fixed rates currently sit at approximately 3.89-3.91% for insured and high-LTV borrowers[1]. This creates an interesting comparison:

| Product Type | Current Rate | Mid-2026 Projected | 5-Year Average |

|---|---|---|---|

| Variable | 4.25% | 4.75%+ | ~4.50% |

| 5-Year Fixed | 3.90% | 3.90% | 3.90% |

If variable rates increase as forecasted, fixed rates may provide better long-term value despite appearing higher initially. However, variable products offer flexibility through:

- Ability to convert to fixed without penalty

- Typically lower penalties if breaking mortgage early

- Potential to benefit if rates decrease unexpectedly

For self-employed borrowers, the decision often hinges on risk tolerance and cash flow predictability. Those with variable business income may prefer fixed payment certainty, while those confident in income stability might embrace variable rate potential.

Hybrid Strategies and Rate Protection

Several strategies allow borrowers to balance rate opportunity with protection against increases:

Blended Rate Approach

Split mortgage between fixed and variable portions (e.g., 50/50 or 60/40 split), providing partial protection while maintaining upside potential.

Capped Variable Rates

Some lenders offer variable rates with maximum caps, limiting upside exposure while allowing downside benefit. These products typically carry 0.10-0.25% premium over standard variable rates.

Accelerated Payment Strategies

Regardless of rate type, maximizing prepayment privileges (typically 15-20% annually) reduces principal faster, minimizing interest rate impact over time.

Contingency Planning for Rate Increases

Prudent borrowers prepare for scenarios where rates move unfavorably:

Stress Testing Personal Finances

Ensure budget can accommodate payments at rates 2.00% higher than current levels—the standard stress test banks apply. If current variable rate is 4.25%, can household manage payments at 6.25%?

Maintaining Rate Conversion Options

When selecting variable products, prioritize lenders offering penalty-free conversion to fixed rates, providing exit strategy if rates rise aggressively.

Building Rate Increase Reserves

Set aside monthly savings equal to payment increases at 1.00% higher rates, creating buffer fund for rate shock scenarios.

Monitoring Trigger Rate Implications

For variable rate mortgages with fixed payments, understand trigger rate thresholds where payments no longer cover interest, requiring payment increases or term extensions.

Investment Property Considerations

Self-employed borrowers often pursue rental property investments as wealth-building strategies. The current rate environment creates specific considerations:

Rental Income Qualification

Lenders typically include 50-80% of rental income toward qualification, improving debt service ratios. However, self-employed borrowers with investment properties face compounded documentation requirements.

Cash Flow Sensitivity

Investment properties with thin margins become problematic if rates increase 0.50-1.00%. Ensure rental income provides adequate cushion above mortgage payments, property taxes, and maintenance costs.

Portfolio Approach

Some self-employed investors benefit from portfolio lending solutions where lenders evaluate total real estate holdings rather than individual properties, potentially offering better rates and terms.

Conclusion: Seizing the 2026 Opportunity Window

The convergence of Bank of Canada rate stability at 2.25%, prime rates holding at 4.45%, and anticipated mid-2026 policy shifts creates a narrow but significant opportunity for self-employed Toronto mortgage seekers. While achieving true sub-3.5% variable rates requires exceptional qualification factors, positioning for the most competitive available rates—currently in the 4.15-4.40% range—demands immediate strategic action.

Self-employed Toronto mortgages in a stable 2.25% BoC environment benefit from predictable rate foundations, but this stability won’t persist indefinitely. Market forecasts increasingly point toward rate increases by mid-year, potentially adding 0.50-1.00% to variable mortgage costs and thousands of dollars in additional interest over typical five-year terms.

Actionable Next Steps for Self-Employed Borrowers

🎯 Immediate Actions (Next 30 Days):

- Gather complete tax documentation for past 2-3 years

- Obtain current credit reports and address any issues

- Connect with specialized mortgage brokers focusing on self-employed Canadians

- Calculate realistic qualification amounts based on documented income

- Begin property search with clear budget parameters

📋 Short-Term Strategy (Next 90 Days):

- Submit applications to multiple lenders through broker network

- Secure rate holds protecting against increases during property search

- Optimize debt service ratios by paying down consumer debt

- Complete property purchase before anticipated Q3 2026 rate announcements

- Establish relationship with lenders offering conversion privileges

📈 Long-Term Planning (6-12 Months):

- Monitor Bank of Canada policy announcements and economic indicators

- Build payment increase reserves for rate volatility scenarios

- Maximize prepayment privileges to reduce principal exposure

- Reassess fixed vs. variable strategy as rate environment evolves

- Maintain documentation readiness for refinancing opportunities

The self-employed mortgage journey in Toronto’s expensive real estate market presents unique challenges, but the current rate environment offers a window that may not reappear. By combining thorough documentation preparation, strategic timing, and professional guidance from Toronto’s extensive broker network, self-employed professionals can secure favorable financing before market conditions deteriorate.

The difference between acting now and waiting until post-hike conditions isn’t merely academic—it represents tens of thousands of dollars in real costs over mortgage lifetimes. For self-employed Toronto borrowers ready to navigate the documentation requirements and qualification processes, early 2026 presents the optimal moment to lock competitive variable rates before the anticipated mid-year shift transforms the lending landscape.

References

[1] Toronto Ontario – https://myperch.io/mortgage-rates-canada/toronto-ontario/

SEO Meta Title: Self-Employed Toronto Mortgages: Lock Sub-3.5% Rates 2026