March 17, 2026

Mitigating 26% Renewal Shocks for Self-Employed Toronto Borrowers: Variable Rate Switches to Sub-3.5% in BoC Hold Era

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage renewal wave hitting Canada in 2026 has created unprecedented financial pressure for homeowners—but self-employed Toronto borrowers face a particularly complex challenge. With approximately 1.15 million Canadian homeowners confronting their “final reckoning” and payment increases averaging 26% for some renewal cohorts, the stakes have never been higher.[1] Yet amid this crisis lies opportunity: variable mortgage rates have dropped to as low as 3.35% as of March 2026, and the Bank of Canada’s rate hold at 2.25% since January has created a unique window for strategic borrowers to dramatically reduce their renewal shock.[1]

For self-employed professionals in Toronto—from contractors and consultants to freelancers and small business owners—mitigating 26% renewal shocks for self-employed Toronto borrowers through variable rate switches to sub-3.5% in the BoC hold era requires understanding both the mathematics of payment shock and the specialized qualification strategies that can unlock these favorable rates despite non-traditional income documentation.

Key Takeaways

✅ Payment increases of 20-26% are hitting many Toronto renewal borrowers in 2026, but variable rates as low as 3.35% can cut this shock significantly compared to fixed rates around 4.89%.[1]

✅ Self-employed borrowers face unique challenges in qualifying for best rates due to income documentation requirements, but specialized lenders and broker strategies can access sub-3.5% variable options.[2]

✅ The Bank of Canada’s rate hold at 2.25% since January 2026 has stabilized the variable rate environment, making strategic switches more predictable than during the 2022-2024 volatility period.[1]

✅ Starting renewal negotiations 4-6 months early and treating lender renewal letters as opening offers—not final terms—can unlock significantly better rates for self-employed borrowers.[2]

✅ Approximately half of borrowers facing payment increases can eliminate the shock entirely by extending amortization by 5 years, providing breathing room without switching lenders.[1]

Understanding the 26% Renewal Shock: Payment Calculations for Toronto Borrowers

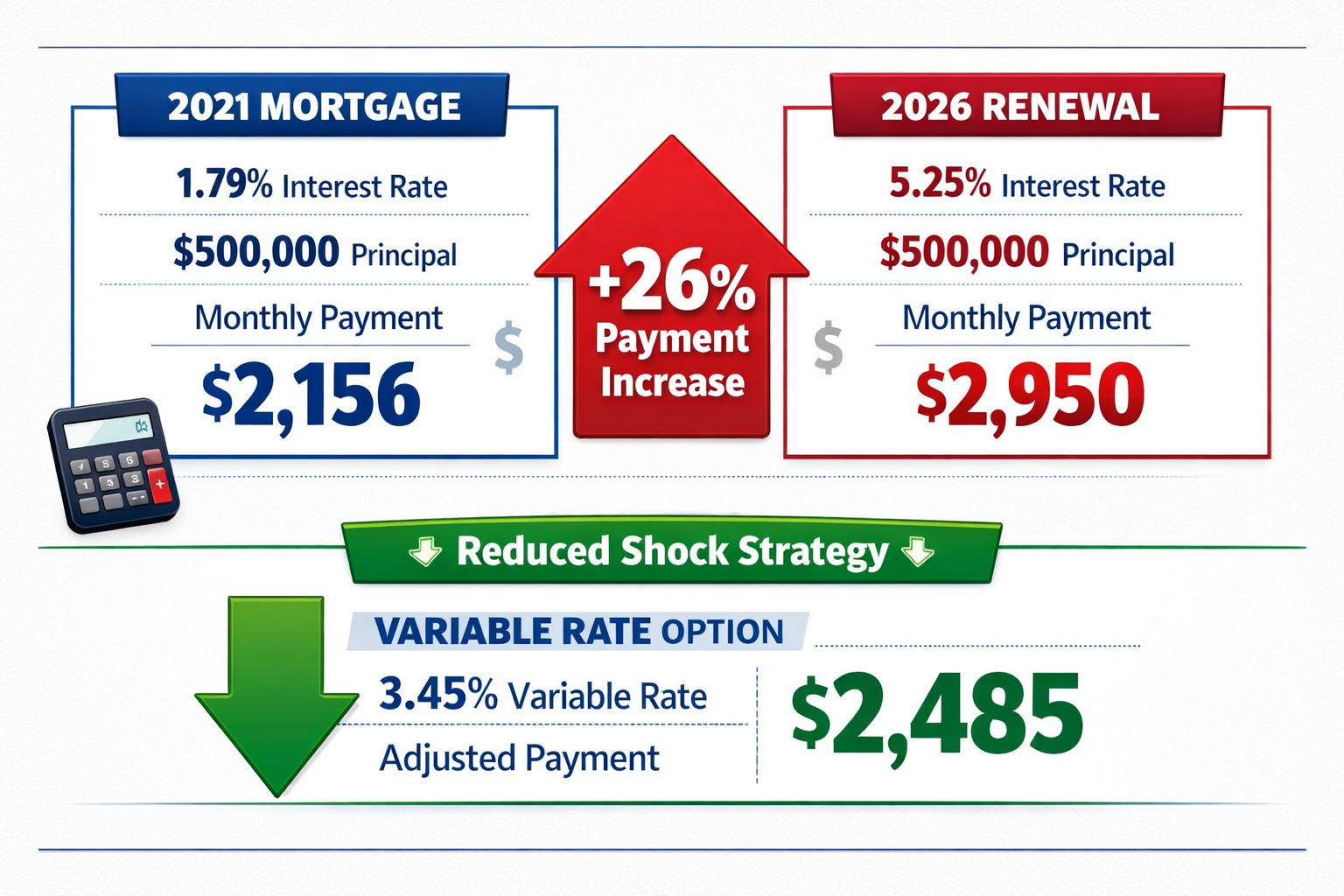

The mathematics behind renewal shock are straightforward but devastating for unprepared homeowners. Borrowers who locked in 5-year fixed mortgages in 2021 at historically low rates around 1.79% are now facing renewal offers between 4.89% and 5.25% for comparable fixed terms in 2026.[1][2]

Real-World Payment Impact Examples

Consider a typical Toronto mortgage scenario:

| Original Mortgage (2021) | Renewal Scenario (2026) | Payment Increase |

|---|---|---|

| Principal: $500,000 | Principal: $475,000 (after 5 years) | |

| Rate: 1.79% (5-yr fixed) | Rate: 5.25% (5-yr fixed) | |

| Monthly Payment: $2,156 | Monthly Payment: $2,950 | +$794 (+37%) |

| Alternative: 3.45% variable | $2,485 (+$329, +15%) |

For self-employed Toronto borrowers, this shock is compounded by fluctuating income patterns that make absorbing sudden $800+ monthly increases particularly challenging. A contractor experiencing seasonal revenue variations or a consultant between major projects faces dramatically different cash flow constraints than salaried employees with predictable biweekly paycheques.

The One-Third Still Facing Increases

Despite the Bank of Canada’s seven rate cuts between June 2024 and October 2025, approximately one-third of all Canadian mortgage holders are still expected to see their payments increase by the end of 2026.[1] This persistent challenge stems from the fact that many borrowers secured rates below 2% during the 2020-2021 pandemic period—rates so historically low that even today’s improved environment of 3.35%-3.95% variable options still represents a significant jump.

Toronto borrowers face heightened risk in this renewal wave. The Canada Mortgage and Housing Corporation (CMHC) specifically identifies Toronto (alongside Vancouver) as a region where “risks are becoming more evident” regarding mortgage arrears during the renewal period, suggesting local market conditions and property values create additional vulnerability.[3]

For those looking to understand the broader context of self-employed mortgage renewals in 2026, the combination of payment shock and income verification challenges creates a perfect storm that demands proactive strategy.

Why Variable Rate Switches to Sub-3.5% Make Sense in the BoC Hold Era

Mitigating 26% renewal shocks for self-employed Toronto borrowers through variable rate switches to sub-3.5% in the BoC hold era represents more than just rate arbitrage—it’s a strategic response to the current monetary policy environment and forward-looking rate expectations.

Current Variable Rate Environment (March 2026)

As of March 2026, competitive variable mortgage rates are available in the following ranges:

- Prime minus 0.90%: 3.35% (best available for well-qualified borrowers)

- Prime minus 0.65%: 3.60% (standard competitive offering)

- Prime minus 0.30%: 3.95% (accessible tier for self-employed with alternative documentation)

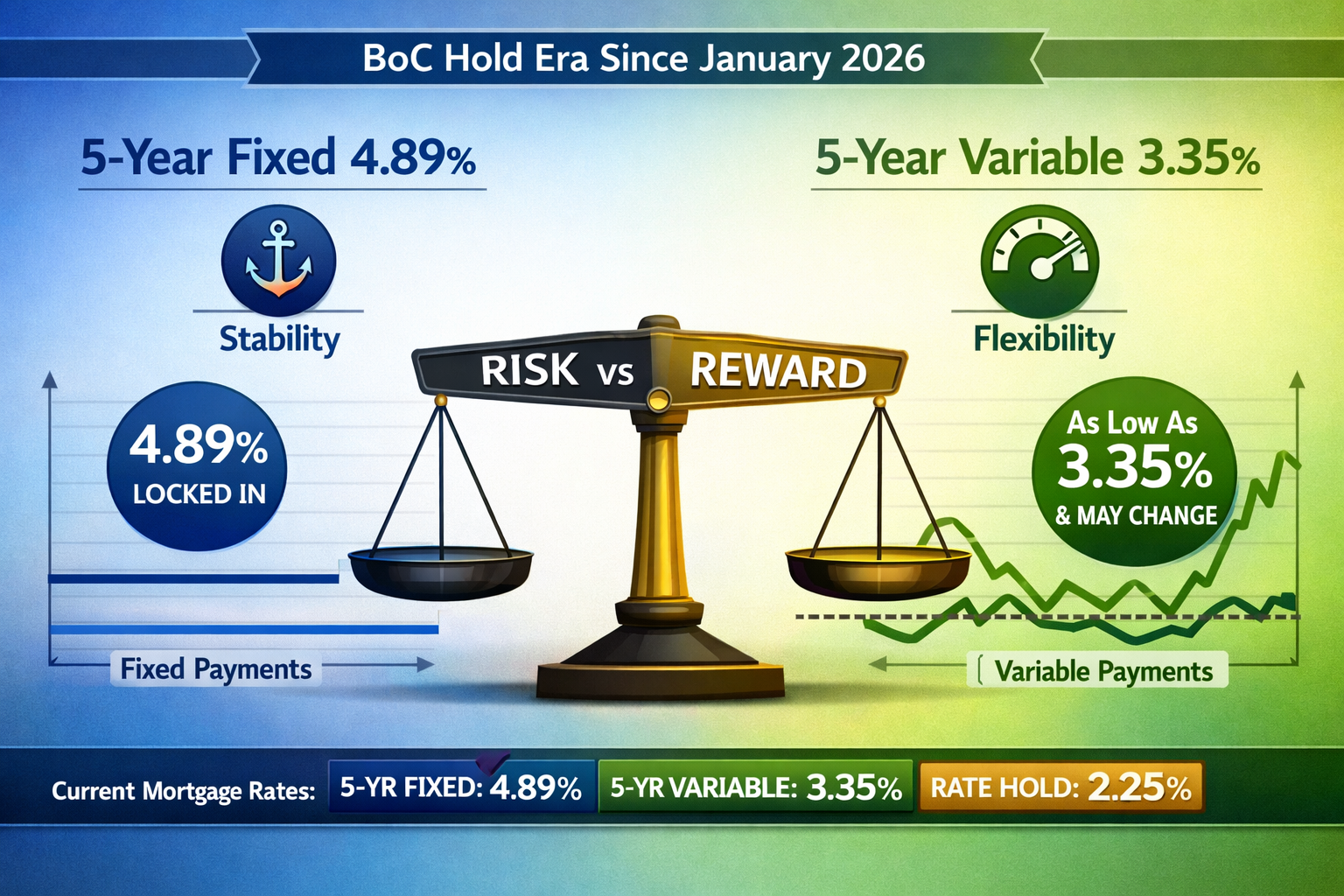

These rates represent a dramatic improvement from 18 months prior, when variable rates sat above 6% during the peak of the Bank of Canada’s tightening cycle.[1] The current prime rate of 4.25% (based on the BoC’s 2.25% overnight rate) has created a stable foundation for variable rate mortgages.

Bank of Canada Rate Hold: Stability Advantage

The Bank of Canada has held its policy rate steady at 2.25% since January 2026, following seven consecutive cuts totaling 175 basis points from the June 2024 peak of 5.00%.[1] This hold period creates several advantages for variable rate borrowers:

Predictability: Unlike the 2022-2024 period when rates rose rapidly and unpredictably, the current hold environment means variable rate borrowers can budget with greater confidence for at least the near-term horizon.

Downside optionality: If economic conditions weaken or inflation remains subdued, the BoC has room to cut rates further, which would immediately benefit variable rate holders. Fixed rate borrowers locked at 4.89% would miss this upside.

Immediate savings: The spread between 5-year fixed rates (approximately 4.89%) and 5-year variable rates (as low as 3.35%) represents 1.54 percentage points of immediate monthly savings—critical breathing room for self-employed borrowers managing fluctuating income.[2]

For self-employed borrowers exploring their options, understanding current fixed and variable mortgage rates in Toronto provides essential context for making informed decisions.

Risk Considerations: Variable vs. Fixed Trade-offs

Variable rates aren’t without risk. The key considerations include:

⚠️ Rate increase exposure: If the BoC resumes rate hikes (though not anticipated in early 2026), variable rate holders would see payments rise. Understanding trigger rates in variable mortgages becomes critical for risk management.

⚠️ Income stability matching: Self-employed borrowers with highly variable income should carefully assess whether variable mortgage payments align with their cash flow patterns.

✅ Break-even analysis: For a borrower choosing between 4.89% fixed and 3.45% variable, the BoC would need to raise rates by approximately 1.44 percentage points (six 25-basis-point hikes) before the variable option loses its advantage—a scenario considered unlikely in the current economic environment.

Qualification Strategies: How Self-Employed Toronto Borrowers Access Sub-3.5% Rates

The challenge for self-employed borrowers isn’t just finding low rates—it’s qualifying for them. Traditional lenders often view self-employed income as higher risk, requiring more documentation and sometimes offering less favorable terms. However, mitigating 26% renewal shocks for self-employed Toronto borrowers through variable rate switches to sub-3.5% in the BoC hold era is entirely achievable with the right approach.

Income Documentation Pathways

Self-employed borrowers typically have three main qualification routes:

1. Full Documentation (Traditional Approach)

- Requirements: 2 years of T1 Generals, 2 years of Notices of Assessment (NOA), business financial statements

- Income calculation: Lenders average 2 years of net income plus add-backs (depreciation, CCA)

- Rate access: Best available rates including sub-3.5% variable options

- Ideal for: Established businesses with consistent reported income

2. Stated Income Programs (Alternative Lenders)

- Requirements: Minimum 10-20% down payment, strong credit (680+), bank statements showing deposits

- Income calculation: Self-declared income verified through bank deposit patterns

- Rate access: Typically 0.25-0.75% higher than prime rates (3.60-3.95% variable range)

- Ideal for: Newer businesses, contractors with write-offs reducing taxable income

3. Asset-Based Qualification

- Requirements: Significant home equity (LTV below 65-70%), strong asset portfolio

- Income calculation: Reduced emphasis on income documentation

- Rate access: Competitive rates if strong equity position (3.45-3.70% variable)

- Ideal for: High-net-worth self-employed with substantial assets but complex income structures

For contractors specifically, specialized mortgage approval strategies can open doors that traditional applications might close.

Navigating the 2026 Mortgage Stress Test

All mortgage renewals involving a lender switch must pass the federal mortgage stress test, which requires qualification at the higher of the contract rate plus 2% or 5.25%.[2] For a 3.45% variable rate, borrowers must prove they can afford payments at 5.45%.

This creates a particular challenge for self-employed borrowers whose income documentation may be complex. However, several strategies can help:

✅ Maximize add-backs: Work with an accountant to identify all legitimate business expense add-backs (depreciation, home office, vehicle expenses) that increase qualifying income without changing tax liability.

✅ Leverage co-applicant income: If applicable, including a spouse or partner with traditional employment can strengthen the application.

✅ Reduce debt service ratios: Paying down credit cards, car loans, or lines of credit before renewal can significantly improve debt-to-income ratios. Approximately 60% of homeowners accumulated $20,000-$50,000 in additional unsecured debt between 2021-2025, creating monthly obligations of $600-$1,000 that count against qualification.[1]

✅ Consider debt consolidation: For borrowers with significant unsecured debt, consolidating into the mortgage during renewal can improve cash flow and qualification metrics.

Understanding how to navigate the 2026 mortgage stress test as a self-employed borrower is essential for successful renewal strategies.

Loan-to-Value Optimization: The 65% Threshold

Making strategic principal prepayments to bring your loan-to-value (LTV) ratio below 65% can unlock insurable-level rates at some lenders without triggering new mortgage insurance premiums.[2] For a Toronto home valued at $900,000, this means reducing the mortgage balance below $585,000.

This strategy is particularly powerful for self-employed borrowers because:

- Lower LTV ratios reduce perceived lender risk, offsetting concerns about income documentation

- Some lenders offer their best variable rates exclusively to borrowers below 65% LTV

- The equity position provides negotiating leverage when shopping multiple lenders

Actionable Renewal Timeline: 6-Month Strategy for Self-Employed Borrowers

Mitigating 26% renewal shocks for self-employed Toronto borrowers through variable rate switches to sub-3.5% in the BoC hold era requires proactive planning starting well before the renewal date. Toronto homeowners should begin the process 4-6 months before their renewal date and treat their lender’s initial renewal letter as a starting point for negotiation, not a final offer.[2]

Month 6 Before Renewal: Research and Assessment Phase

Action items:

- Review current mortgage terms, rate, and remaining balance

- Calculate potential payment at current renewal rates (both fixed and variable)

- Assess current home value and calculate LTV ratio

- Pull credit report and address any issues

- Research current self-employed mortgage rates in Toronto

Goal: Understand your baseline position and identify improvement opportunities.

Month 5 Before Renewal: Documentation Preparation

Action items:

- Gather 2 years of T1 Generals and Notices of Assessment

- Prepare business financial statements (if incorporated)

- Collect 3-6 months of business bank statements

- Document any income add-backs with accountant

- Review and optimize debt service ratios (pay down high-interest debt if possible)

Goal: Have all documentation ready for multiple lender applications.

Month 4 Before Renewal: Professional Consultation

Action items:

- Consult with a specialized self-employed mortgage broker

- Discuss fixed vs. variable options based on income stability

- Explore alternative lenders if traditional qualification is challenging

- Get pre-qualification from 3-5 lenders to compare offers

Goal: Understand all available options and identify best rate opportunities.

Month 3 Before Renewal: Formal Applications and Negotiation

Action items:

- Submit formal applications to top 3 lender choices

- Use competing offers as negotiation leverage with current lender

- Review all terms beyond just rate (prepayment privileges, portability, penalties)

- Consider switching lenders at renewal if significantly better terms available

Goal: Secure multiple firm offers and negotiate best possible terms.

Month 2 Before Renewal: Final Decision and Commitment

Action items:

- Compare all offers including total cost analysis (legal fees, appraisal costs if switching)

- Make final fixed vs. variable decision based on current BoC outlook

- Commit to best offer and begin formal approval process

- Arrange legal representation if switching lenders

Goal: Lock in optimal rate and terms with confidence.

Month 1 Before Renewal: Execution and Finalization

Action items:

- Complete all lender requirements (appraisal, updated documentation)

- Review and sign final mortgage commitment

- Coordinate with lawyer for closing (if switching lenders)

- Set up new payment schedule and budget accordingly

Goal: Seamless transition to new mortgage terms without disruption.

The Amortization Extension Strategy

For self-employed borrowers who qualify for renewal with their current lender but struggle with payment increases, approximately half could eliminate the payment jump entirely by extending their amortization by 5 years.[1] This strategy provides immediate relief without the complexity of switching lenders:

Example:

- Original: $475,000 balance, 20 years remaining, 5.25% rate = $3,235/month

- Extended: $475,000 balance, 25 years remaining, 5.25% rate = $2,950/month

- Savings: $285/month while maintaining same rate

This approach works particularly well for self-employed borrowers in temporary cash flow crunches or those prioritizing business reinvestment over accelerated mortgage paydown.

Managing Variable Rate Risk: Protection Strategies for Self-Employed Income Patterns

Choosing a variable rate mortgage to mitigate renewal shock makes financial sense for many self-employed Toronto borrowers, but managing the inherent rate volatility requires specific strategies aligned with fluctuating income patterns.

Cash Flow Buffer Building

Self-employed borrowers should maintain a mortgage payment reserve fund equal to 6-12 months of payments—double the typical 3-6 month recommendation for salaried employees. This buffer accounts for:

- Potential variable rate increases if BoC resumes hiking

- Seasonal income fluctuations common in self-employment

- Unexpected business expenses or revenue gaps

💡 Pro tip: Automate transfers during high-income months to build this reserve without relying on discipline during leaner periods.

Income Smoothing Techniques

Self-employed borrowers can reduce renewal shock vulnerability by:

✅ Incorporating and paying yourself a salary: Creates consistent, documentable income for future renewals ✅ Maximizing RRSP contributions: Reduces taxable income while building retirement savings that can serve as emergency reserves ✅ Strategic timing of business expenses: Coordinate major write-offs with renewal cycles to optimize qualifying income

For comprehensive guidance on tax strategies and benefit maximization, self-employed borrowers should work with specialized accountants who understand mortgage qualification implications.

Rate Lock Triggers: When to Switch from Variable to Fixed

Establish predetermined “trigger points” for converting from variable to fixed:

- If BoC raises rates to 3.00% (75 basis points above current 2.25%), reassess variable strategy

- If variable rate exceeds 4.50%, compare against available fixed rates

- If income becomes unstable, prioritize payment predictability over rate optimization

Most variable rate mortgages allow conversion to fixed rates at any time without penalty, providing flexibility to adapt as circumstances change.

Conclusion: Taking Control of Your 2026 Renewal

Mitigating 26% renewal shocks for self-employed Toronto borrowers through variable rate switches to sub-3.5% in the BoC hold era is not just possible—it’s a strategic imperative for thousands of homeowners facing unprecedented payment increases in 2026. With variable rates as low as 3.35% available to well-qualified borrowers and the Bank of Canada maintaining its hold at 2.25%, the current environment offers a unique opportunity to dramatically reduce renewal shock compared to fixed rate alternatives around 4.89%.[1][2]

The key to success lies in proactive planning and specialized expertise. Self-employed borrowers face unique qualification challenges, but with proper documentation preparation, strategic income optimization, and professional broker guidance, accessing sub-3.5% variable rates is entirely achievable—even for those with non-traditional income structures.

Your Next Steps

🎯 Start now: Don’t wait for your renewal letter. Begin the process 4-6 months before your renewal date to maximize negotiating leverage and option exploration.

🎯 Get professional help: Work with a specialized self-employed mortgage broker who understands both the rate environment and the unique qualification strategies for non-traditional income.

🎯 Document everything: Gather 2 years of tax returns, NOAs, bank statements, and business financials now—complete documentation is your strongest qualification tool.

🎯 Compare multiple lenders: Your current lender’s renewal offer is just a starting point. Get quotes from at least 3-5 lenders to ensure you’re accessing the best available rates.

🎯 Consider the full picture: Look beyond just the interest rate to prepayment privileges, portability options, and total cost of switching lenders if applicable.

The 2026 renewal wave represents both challenge and opportunity. For self-employed Toronto borrowers willing to take a strategic, informed approach, variable rate switches to sub-3.5% can transform what might have been a 26% payment shock into a manageable, even advantageous, renewal outcome. The tools, rates, and strategies are available—the question is whether you’ll take action early enough to maximize your options.

Don’t let renewal shock catch you unprepared. Start your renewal strategy today and take control of your mortgage future in this favorable BoC hold era.

References

[1] Watch – https://www.youtube.com/watch?v=lSQJu2PTr7M

[2] 2026 Mortgage Renewal Shock What Toronto Ontario Homeowners Need To Know – https://www.cornellmortgages.ca/post/2026-mortgage-renewal-shock-what-toronto-ontario-homeowners-need-to-know

[3] Mortgage Renewal Wave Strains Some Regions Borrowers – https://www.cmhc-schl.gc.ca/observer/2026/mortgage-renewal-wave-strains-some-regions-borrowers