March 17, 2026

Self-Employed Toronto Buyers and the New $1.5M Insurable Threshold: Qualification Strategies for Luxury Homes in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The Toronto luxury real estate market has traditionally been out of reach for many self-employed professionals seeking insured mortgage financing. However, a groundbreaking policy change implemented in December 2024 has fundamentally altered this landscape. Self-Employed Toronto Buyers and the New $1.5M Insurable Threshold: Qualification Strategies for Luxury Homes in 2026 represents a significant opportunity for entrepreneurs, business owners, and independent professionals to access premium properties that were previously relegated to uninsured mortgage territory.

The increase of the maximum insurable mortgage threshold from $1 million to $1.5 million opens doors to a substantial segment of Toronto’s housing inventory, particularly in sought-after neighborhoods where average home prices hover between $1.2 million and $1.5 million. For self-employed buyers who often face additional scrutiny during the mortgage approval process, understanding how to leverage this new threshold while navigating income verification requirements is essential for success in 2026.

Key Takeaways

✅ The $1.5M insurable threshold allows self-employed buyers to access CMHC-insured mortgages for luxury Toronto homes with as little as 5% down, significantly expanding affordable options in premium neighborhoods.

✅ Alternative income verification methods including bank statement programs and stated income mortgages provide viable pathways for self-employed professionals who write off substantial business expenses.

✅ Strategic debt ratio management through business structure optimization, tax planning, and credit positioning can dramatically improve qualification amounts under the new rules.

✅ The 30-year amortization option (effective January 2025) reduces monthly payments by approximately 11-13%, helping self-employed buyers meet stress test requirements for higher-priced properties.

✅ Working with specialized mortgage professionals who understand self-employed income documentation is critical for maximizing approval chances and securing competitive rates in the luxury market segment.

Understanding the New $1.5M Insurable Threshold and Its Impact on Toronto’s Luxury Market

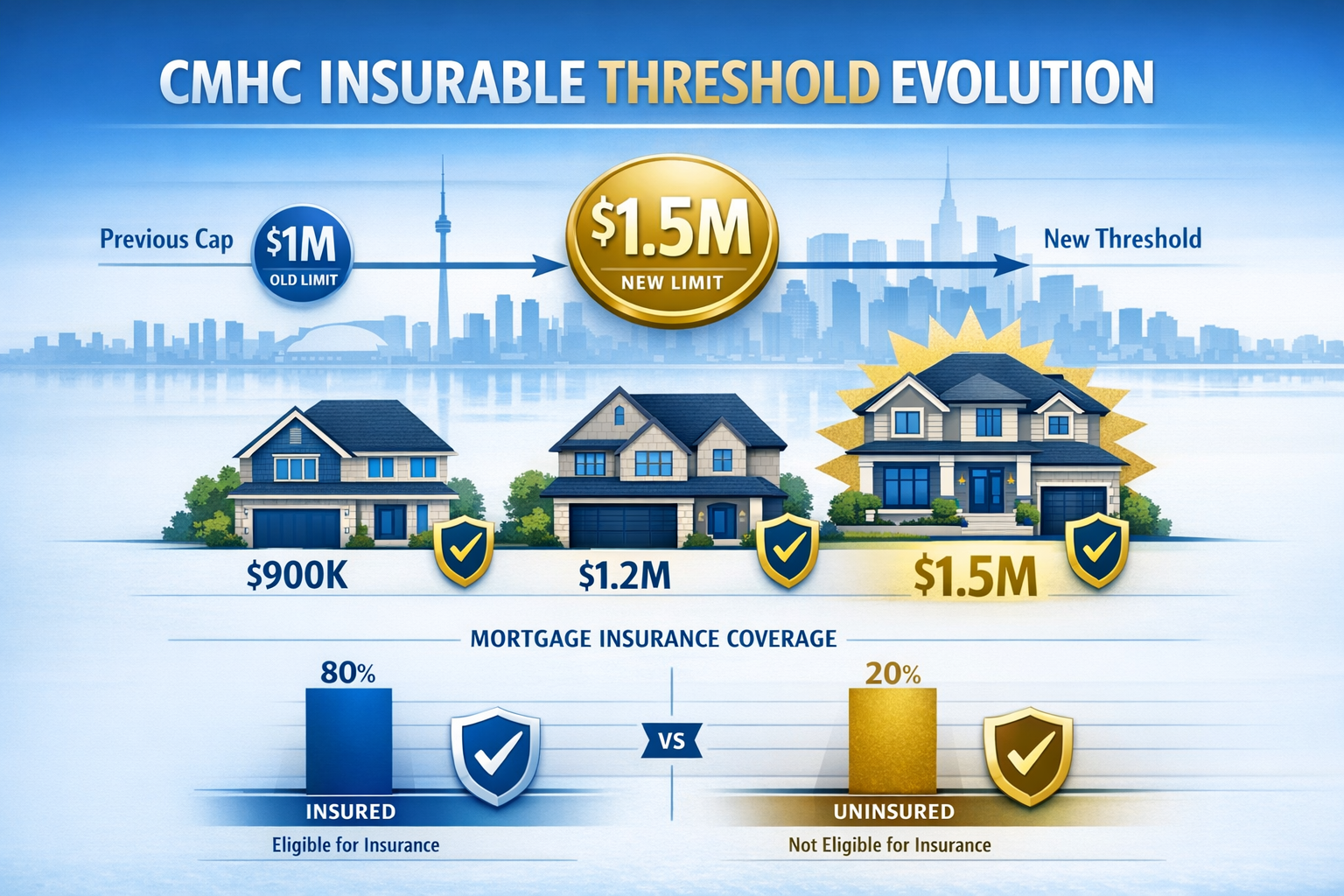

The Canadian mortgage landscape underwent a transformative shift when the federal government raised the maximum home value eligible for mortgage default insurance from $1 million to $1.5 million, effective December 15, 2024[1]. This policy change directly addresses the affordability crisis in high-cost urban centers like Toronto, where the average detached home price regularly exceeds the previous $1 million cap.

What Makes Insured Mortgages Advantageous?

Insured mortgages are backed by mortgage default insurance from providers like CMHC, Sagen, or Canada Guaranty. This insurance protects lenders against default risk, which translates to several key benefits for borrowers:

- Lower interest rates: Insured mortgages typically offer rates 0.15% to 0.40% lower than uninsured mortgages

- Reduced down payment requirements: As low as 5% down for properties under $500,000, and 5-10% for properties between $500,000 and $1.5 million

- More flexible qualification: Broader lender acceptance and standardized approval criteria

- Access to competitive products: Better mortgage features and prepayment privileges

For self-employed buyers specifically, the insured mortgage category provides access to more lenders willing to work with non-traditional income documentation. Many innovative mortgage solutions for self-employed Canadians have emerged specifically within the insured mortgage space.

The Toronto Luxury Market Sweet Spot 🏡

The $1.5 million threshold is particularly relevant for Toronto buyers because it captures a significant portion of the city’s housing inventory:

| Property Type | Average Price Range | Now Insurable? |

|---|---|---|

| Downtown Condos (2-3 bed) | $800K – $1.2M | ✅ Yes |

| Midtown Townhomes | $1.1M – $1.4M | ✅ Yes |

| North York Detached | $1.3M – $1.5M | ✅ Yes |

| Etobicoke Semi-Detached | $900K – $1.3M | ✅ Yes |

| Scarborough Detached | $1.0M – $1.4M | ✅ Yes |

Previously, buyers targeting these property types needed to provide a minimum 20% down payment and accept higher uninsured mortgage rates. Now, with the raised threshold, self-employed professionals can potentially enter these markets with down payments as low as 10% (for properties over $500K) while benefiting from insured mortgage pricing[1].

Insured vs. Uninsured: The Critical Distinction

Understanding the difference between insured and uninsured mortgages is fundamental for Self-Employed Toronto Buyers and the New $1.5M Insurable Threshold: Qualification Strategies for Luxury Homes in 2026:

Insured Mortgages (less than 20% down):

- Require mortgage default insurance premium (2.8% to 4.0% of loan amount)

- Subject to government-mandated qualification rules

- Must meet maximum property value limits ($1.5M as of December 2024)

- Typically offer better interest rates

- Broader lender participation

Uninsured Mortgages (20% or more down):

- No insurance premium required

- Individual lender qualification criteria apply

- No maximum property value restrictions

- Slightly higher interest rates

- More stringent income verification for self-employed

For self-employed buyers who may struggle with traditional income verification, the insured category often provides more standardized and accessible pathways to approval, particularly when working with brokers who specialize in self-employed mortgage solutions.

Self-Employed Income Verification Challenges and Solutions Under the New Rules

Self-employed professionals face unique challenges when qualifying for mortgages, challenges that become even more pronounced in the luxury home segment. The fundamental issue stems from the way business owners manage their finances: maximizing tax deductions to minimize taxable income often conflicts with demonstrating sufficient income for mortgage qualification.

The Self-Employed Income Dilemma

Traditional employed borrowers present straightforward income verification through T4 slips and employment letters. Self-employed individuals must navigate a more complex landscape:

Standard Documentation Requirements:

- Two years of complete personal tax returns (T1 Generals)

- Two years of Notices of Assessment (NOAs) from CRA

- Business financial statements (often T2125 or T2 corporate returns)

- Proof of business registration and GST/HST numbers

- Year-to-date profit and loss statements

The challenge? Many successful self-employed professionals show relatively modest net income on their tax returns after claiming legitimate business expenses like vehicle costs, home office deductions, meals and entertainment, and depreciation. A business owner earning $200,000 in gross revenue might only show $75,000 in net income after expenses—significantly limiting their mortgage qualification potential.

Alternative Income Verification Methods for 2026

Fortunately, the Canadian mortgage market has evolved to accommodate self-employed borrowers through several alternative qualification methods, particularly relevant for those targeting properties near the new $1.5M threshold:

1. Bank Statement Programs

These programs analyze business cash flow rather than taxable income. Lenders review 12-24 months of business bank statements to calculate average monthly deposits and determine qualifying income[2].

Advantages:

- Reflects actual business cash flow

- Captures income before tax deductions

- Faster approval process

- Suitable for established businesses with consistent deposits

Typical Requirements:

- Minimum 10-20% down payment

- Two years in business

- Strong personal credit score (680+)

- Consistent monthly deposit patterns

For self-employed professionals considering this approach, our guide on bank statement loans for self-employed borrowers provides comprehensive details on qualification criteria and lender options.

2. Stated Income Mortgages

Also known as self-declared income programs, these mortgages allow borrowers to state their income without traditional documentation. However, the stated income must be reasonable and verifiable through indirect means like business registration, professional licenses, or industry income averages.

Key Considerations:

- Typically require 15-35% down payment

- Higher interest rates (often 0.5-1.5% above prime programs)

- Stricter property appraisal requirements

- Best for professionals with complex income structures

3. Add-Back Programs

Some lenders offer programs that “add back” certain non-cash business expenses to increase qualifying income:

- Depreciation and amortization

- One-time business expenses

- Capital cost allowances

- Certain business use of home expenses

This approach bridges the gap between tax-minimization strategies and mortgage qualification needs, making it particularly valuable for self-employed borrowers navigating qualification without T4 slips.

Strategic Income Documentation for Luxury Home Qualification

When pursuing Self-Employed Toronto Buyers and the New $1.5M Insurable Threshold: Qualification Strategies for Luxury Homes in 2026, consider these documentation strategies:

12-18 Months Before Applying:

- Reduce aggressive tax write-offs to increase reported income

- Maintain consistent business banking patterns

- Ensure personal and business finances are clearly separated

- Build strong credit history with business credit cards

6 Months Before Applying:

- Gather all tax documents and financial statements

- Obtain updated business licenses and registrations

- Prepare explanations for income fluctuations

- Consider professional income verification services

During Application:

- Work with mortgage brokers experienced in self-employed files

- Provide comprehensive business context and industry information

- Be prepared to explain business model and revenue sources

- Consider co-applicants or guarantors if needed

Debt Ratio Management and Stress Test Strategies for Self-Employed Luxury Home Buyers

Successfully qualifying for a mortgage near the $1.5M threshold requires mastering two critical financial metrics: Gross Debt Service (GDS) ratio and Total Debt Service (TDS) ratio. For self-employed buyers, optimizing these ratios while navigating the federal stress test presents both challenges and opportunities.

Understanding Debt Service Ratios

Gross Debt Service (GDS) Ratio: This measures housing costs as a percentage of gross income. The calculation includes:

- Principal and interest payments (P&I)

- Property taxes

- Heating costs

- 50% of condo fees (if applicable)

Maximum GDS: Typically 32-39% for insured mortgages

Total Debt Service (TDS) Ratio: This measures all debt obligations as a percentage of gross income, including:

- All GDS components

- Credit card payments

- Car loans and leases

- Line of credit payments

- Other personal loans

- Child support or alimony

Maximum TDS: Typically 42-44% for insured mortgages

The Mortgage Stress Test Challenge 📊

All insured mortgage applications must pass the mortgage stress test, which requires qualification at the higher of:

- The contract rate plus 2%, OR

- The Bank of Canada’s benchmark rate (currently 5.25% as of early 2026)

This means if you’re offered a 4.5% mortgage rate, you must qualify as if the rate were 6.5%. For a $1.2 million mortgage, this dramatically impacts the required income:

| Mortgage Amount | Actual Rate (4.5%) | Stress Test Rate (6.5%) | Monthly Payment Difference |

|---|---|---|---|

| $1,000,000 | $5,067 | $6,320 | +$1,253 |

| $1,200,000 | $6,080 | $7,584 | +$1,504 |

| $1,350,000 | $6,840 | $8,532 | +$1,692 |

For self-employed buyers targeting luxury properties, navigating the 2026 mortgage stress test requires strategic planning and debt optimization.

Strategies to Improve Debt Ratios

1. Eliminate or Reduce Consumer Debt

Before applying for a mortgage near the $1.5M threshold, aggressively pay down:

- Credit card balances: Even if you pay them off monthly, lenders calculate 3% of the balance as a monthly payment

- Car loans: Consider paying off vehicles or switching to less expensive models

- Lines of credit: Reduce or eliminate balances; lenders calculate 3% of the limit as a payment

- Personal loans: Clear these entirely if possible

Impact Example: Eliminating $50,000 in consumer debt could increase your mortgage qualification by $150,000-$200,000.

2. Leverage the 30-Year Amortization Option

Effective January 1, 2025, eligible buyers can access 30-year amortizations for insured mortgages[1]. While this increases total interest paid over the life of the mortgage, it significantly reduces monthly payments:

$1.2M Mortgage at 4.5%:

- 25-year amortization: $6,666/month

- 30-year amortization: $6,080/month

- Monthly savings: $586 (approximately 11% reduction)

This reduction directly improves GDS and TDS ratios, potentially making the difference between approval and denial for self-employed buyers with strong income but tight ratios.

3. Optimize Business Structure for Income Reporting

Self-employed professionals should work with accountants to structure their businesses in ways that maximize mortgage-qualifying income:

For Incorporated Professionals:

- Balance salary vs. dividend distributions (salary is more mortgage-friendly)

- Consider increasing salary in the 1-2 years before applying

- Document retained earnings that could be distributed

For Sole Proprietors:

- Minimize discretionary expenses in application years

- Clearly separate personal and business expenses

- Maintain detailed records of add-back eligible expenses

4. Strategic Co-Applicant or Guarantor Use

When targeting properties near the $1.5M threshold, consider:

- Spousal co-application: Combining incomes (even if spouse is also self-employed)

- Business partner co-application: If purchasing investment property

- Parental guarantor: For younger self-employed professionals with strong income but limited history

Income Requirements for $1.5M Properties

To provide concrete targets, here are approximate income requirements for properties at various price points under the new threshold:

Assumptions: 10% down payment, 4.5% rate, 30-year amortization, property taxes at 1.2% of value, heating $200/month, no other debts

| Property Price | Down Payment | Mortgage Amount | Required Gross Income* |

|---|---|---|---|

| $1,000,000 | $100,000 | $900,000 | ~$185,000 |

| $1,200,000 | $120,000 | $1,080,000 | ~$225,000 |

| $1,400,000 | $140,000 | $1,260,000 | ~$265,000 |

| $1,500,000 | $150,000 | $1,350,000 | ~$285,000 |

*These are rough estimates; actual requirements vary by lender and individual circumstances. Self-employed applicants should consult with specialists who understand self-employed mortgage rates and qualification in Toronto.

Practical Action Plan: Positioning Yourself for Success in Toronto’s Luxury Market

Successfully leveraging Self-Employed Toronto Buyers and the New $1.5M Insurable Threshold: Qualification Strategies for Luxury Homes in 2026 requires a systematic approach that addresses income documentation, debt management, and strategic timing. Here’s a comprehensive action plan for self-employed professionals targeting luxury Toronto properties.

Phase 1: Financial Assessment and Preparation (12-18 Months Out)

Step 1: Calculate Your Current Qualification Capacity

Begin by honestly assessing your current financial position:

- Review the last two years of personal tax returns

- Calculate your average net income as reported to CRA

- List all current debts and monthly obligations

- Check your credit score and report for errors

- Estimate your available down payment funds

Step 2: Engage Professional Advisors Early

Assemble your team:

- Mortgage broker specializing in self-employed clients: Essential for navigating alternative qualification methods

- Accountant with real estate experience: To optimize tax strategy for mortgage qualification

- Real estate lawyer: For preliminary advice on property types and transaction structures

Working with professionals experienced in self-employed mortgage scenarios can save months of frustration and significantly improve approval odds.

Step 3: Implement Income Optimization Strategies

Based on your advisor consultations:

- Adjust business expense claims to increase reported income

- Establish consistent income patterns through regular salary (if incorporated)

- Document all income sources thoroughly

- Consider restructuring business operations for better mortgage qualification

Phase 2: Debt Optimization and Credit Building (6-12 Months Out)

Step 4: Execute Aggressive Debt Reduction

Create a targeted debt elimination plan:

- Pay off credit cards completely

- Eliminate or significantly reduce car loans

- Pay down lines of credit to zero or minimal balances

- Avoid taking on any new debt obligations

- Close unused credit accounts (carefully—don’t harm credit score)

Step 5: Build and Maintain Strong Credit

Credit score targets for optimal approval:

- Minimum: 680 for most insured programs

- Ideal: 720+ for best rates and terms

- Excellent: 760+ for maximum lender flexibility

Credit-building tactics:

- Keep credit card utilization below 30% of limits

- Make all payments on time (set up automatic payments)

- Maintain a mix of credit types (cards, installment loans)

- Don’t apply for new credit in the 6 months before mortgage application

Phase 3: Documentation and Application (3-6 Months Out)

Step 6: Assemble Comprehensive Documentation

Prepare a complete documentation package:

Personal Documents:

- Two years of complete tax returns (T1 Generals)

- Notices of Assessment from CRA

- Government-issued photo ID

- Proof of down payment source (bank statements, investment accounts)

- Rental history or current mortgage statements

Business Documents:

- Business registration and licenses

- Two years of business tax returns (T2125 or T2 corporate)

- Year-to-date profit and loss statement

- Business bank statements (12-24 months)

- Contracts or agreements showing ongoing business relationships

- Professional designations or certifications

Step 7: Pre-Approval and Property Search

Obtain mortgage pre-approval before house hunting:

- Provides realistic budget parameters

- Strengthens negotiating position with sellers

- Identifies potential qualification issues early

- Locks in rate (typically for 90-120 days)

When searching for properties, focus on neighborhoods where the $1.5M threshold provides maximum value. Consider exploring emerging Toronto markets where luxury properties remain within the insurable threshold.

Phase 4: Application and Closing (1-3 Months Out)

Step 8: Submit Complete Application

Work closely with your mortgage broker to:

- Submit to multiple lenders simultaneously (broker handles this)

- Respond promptly to any documentation requests

- Provide clear explanations for income fluctuations

- Be prepared for additional verification steps

Step 9: Navigate Underwriting and Conditions

The underwriting process for self-employed buyers often involves:

- Additional income verification requests

- Business verification calls or letters

- Explanation letters for unusual transactions

- Updated financial statements if process extends beyond 90 days

Step 10: Prepare for Closing

Final steps before taking possession:

- Arrange home insurance (high-value coverage for luxury properties)[3]

- Coordinate with real estate lawyer on closing details

- Confirm final mortgage funding with lender

- Plan for closing costs (typically 1.5-4% of purchase price)

Understanding legal fees and closing costs helps avoid last-minute financial surprises.

Special Considerations for Luxury Properties

When targeting properties near the $1.5M threshold, be aware of additional considerations:

High-Value Home Insurance 🏠

Luxury properties require specialized insurance coverage:

- Guaranteed replacement cost coverage: Ensures full reconstruction regardless of policy limits[5]

- Enhanced content coverage: Higher limits for valuables, art, jewelry

- Additional living expenses: Extended coverage if home becomes uninhabitable

- Liability coverage: Increased limits appropriate for high-net-worth individuals

Annual insurance costs for a $2M luxury home can reach $7,200 or more[4], so factor this into your GDS calculations.

Property Tax Implications

Higher-value properties carry proportionally higher property taxes:

- Toronto’s 2026 residential property tax rate: approximately 0.6-0.7% of assessed value

- Annual taxes on a $1.4M property: roughly $8,400-$9,800

- These must be included in GDS ratio calculations

Maintenance and Operating Costs

Luxury homes typically involve higher ongoing costs:

- Larger properties mean higher heating, cooling, and utility expenses

- Premium materials require specialized maintenance

- Landscaping and property upkeep for larger lots

- Potential HOA or condo fees in luxury developments

Timing the Market: Why 2026 Presents Unique Opportunities

Several factors make 2026 particularly advantageous for self-employed buyers targeting luxury properties:

New threshold implementation: Many buyers and agents are still adjusting to the $1.5M insurable limit, creating potential negotiating opportunities

Interest rate environment: With rates stabilizing after the high-rate period of 2022-2024, 2026 mortgage rates for self-employed borrowers remain competitive

Market conditions: Toronto’s real estate market has cooled from pandemic peaks, providing more balanced negotiating conditions

Lender competition: Multiple lenders now offer specialized self-employed programs, increasing approval options and rate competitiveness

Conclusion

The expansion of the insurable mortgage threshold to $1.5 million represents a watershed moment for Self-Employed Toronto Buyers and the New $1.5M Insurable Threshold: Qualification Strategies for Luxury Homes in 2026. This policy change democratizes access to Toronto’s luxury housing market, bringing premium properties within reach for entrepreneurs, business owners, and independent professionals who previously faced barriers in the uninsured mortgage category.

Success in this new landscape requires a strategic, multi-faceted approach:

✅ Understand the insured mortgage advantage: Lower rates, reduced down payments, and broader lender access make the sub-$1.5M market significantly more accessible than higher-priced alternatives.

✅ Master alternative income verification: Bank statement programs, stated income mortgages, and add-back strategies provide viable pathways around traditional T4-based qualification.

✅ Optimize debt ratios proactively: Aggressive debt reduction, strategic use of 30-year amortizations, and business structure optimization can dramatically improve qualification capacity.

✅ Plan 12-18 months ahead: Early preparation, professional advisor engagement, and systematic execution separate successful applicants from those who struggle with last-minute qualification challenges.

✅ Work with specialists: Mortgage brokers experienced in self-employed files understand the nuances of alternative documentation and can match you with appropriate lenders.

Your Next Steps

If you’re a self-employed professional considering a luxury Toronto property purchase in 2026:

Schedule a consultation with a mortgage broker specializing in self-employed clients to assess your current qualification capacity

Engage an accountant to review your business structure and tax strategy for mortgage optimization

Review your credit report and begin addressing any issues that could impact approval

Calculate your target price range using realistic debt ratios and income documentation methods

Start your documentation process by gathering the past two years of tax returns and business financial statements

Research neighborhoods where the $1.5M threshold provides optimal value in Toronto’s luxury market

The new $1.5M insurable threshold isn’t just a policy change—it’s an opportunity to access Toronto’s premium housing market with better rates, lower down payments, and more flexible qualification options than ever before. For self-employed professionals who approach the process strategically, 2026 could be the year that luxury homeownership becomes reality.

Don’t let self-employment status hold you back from your real estate goals. With proper planning, documentation, and professional guidance, the doors to Toronto’s luxury housing market are now wide open.

References

[1] New Toronto Mortgage Rules – https://landsignal.ai/blog/new-toronto-mortgage-rules/

[2] Insured Mortgage Rules And Affordability In 2026 A Practical Guide For Canadian Homebuyers – https://www.yourmortgageconnection.ca/index.php/blog/post/327/insured-mortgage-rules-and-affordability-in-2026-a-practical-guide-for-canadian-homebuyers

[3] High Value Home Insurance – https://bestbuyinsurance.ca/personal-insurance/high-value-home-insurance/

[4] High Value Home Insurance – https://standrewsinsurance.com/toronto/high-value-home-insurance/

[5] High Value Homes 2m 20m Insurance Considerations In Canada – https://totalriskmanagers.com/high-value-homes-2m-20m-insurance-considerations-in-canada/